Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

The enigmatic U.S. crude oil export ban taunts an energy sector mired in sluggish times: How can a can-do industry be stymied by a can-do country’s can’t-do rule?

Rather than fret, consider this: the industry has not been thwarted, not really. Think of crude exports as a once-and-future boom. Here in the present, the world is developing an appetite for natural gas and NGLs, and U.S. energy players are acting to feed it.

“Via pipelines to our near north and south neighbors or via LNG, it’s all about: How do we get more supply to a bigger market?” Greg Haas, Houston-based director for Stratas Advisors, told Midstream Business. “The supply of NGL has gone up dramatically in the U.S. as a result of shale gas and liquids-rich production. This stems from the upstream’s prime directive to supply, supply, supply.”

But domestic demand for NGL has not cooperated in joining the upward climb, resulting in a surplus.

“Ethane used to be a highly valued specialty product,” Haas said. “Now it’s very low-priced, and in fact, being rejected because it’s worth more as fuel in some locations.”

Other gas liquids, like propane and butane, are enduring market struggles as well as a result of wildly successful shale play production, Haas said.

“We have got a lot of new propane supply coming out of the natural gas and associated gas and wet gas regions,” he said. “If you look at propane prices, they too have crashed. And if you look at storage facilities in the U.S., we are at historic levels of propane storage. So it’s almost like the gas glut has become an NGL glut on ethane and propane.

“I believe butane will be next,” Haas continued. “Butane prices have already come down substantially, and we may see a considerable glut in butane stocks and continued price declines continue on.”

Too much

But there is an upside to slumping propane prices and heavy stock levels— it makes the product more attractive to buyers in other countries.

Global propane prices have typically been set by the Saudi Aramco monthly contract price, known as ACP. The Saudi national oil company bases this on the price of naphtha because, like propane, naphtha is a petrochemical feedstock. In a recent report, the U.S. Energy Information Administration (EIA) noted that in 2005, the U.S. propane price at the Mont Belvieu, Texas, NGL hub carried a three-cent per gallon premium to ACP. At the time, the U.S. was a net importer of propane.

Since then, U.S. propane has sold at a discount to the international price, peaking at 89 cents per gallon below ACP in 2012. A spread of this magnitude prompted construction of new export terminals. As capacity grew, the spread narrowed, but the margin remains large enough to encourage more propane shipments overseas.

The target-rich environment for exports has historically been within the hemisphere, where U.S. exporters have supplied customers in Mexico, the Caribbean and South America. Exports to those markets doubled between 2010 and 2013, the EIA reported, from 88,000 barrels per day (bbl/d) to 198,000 bbl/d. But it’s Europe where business has really boomed, quadrupling from 25,000 bbl/d in 2012 to nearly 100,000 bbl/d in the first eight months of 2015. U.S. sellers are now making inroads into markets previously controlled by producers in Russia, North Africa and the Middle East.

Asia is another region that had traditionally been dependent on Middle East suppliers, along with refinery and natural gas plant production within the region. Here again, the shift to imports from the U.S. reflects a pivot in global trade dynamics. U.S. exports almost tripled in the region to 189,000 bbl/d in the first eight months of 2015 from 65,000 bbl/d during the same period in 2014. The fastest-growing segment for propane demand in Asia is the petrochemical sector, and the EIA forecasts this to continue to drive increases in U.S. exports, assuming pricing trends remain more or less where they are now.

Bountiful butane

Butane also falls into the “too much of a good thing” category. It’s used in cooking in many parts of the world where pipeline-supplied gas is not available and can be refined into an alkylate and blended into gasoline to enhance oxygenates and antiknock properties. But NGL from shale plays is too plentiful for domestic consumption alone.

“It seems to be swamping the ability of U.S. industry to absorb all this new supply of butane,” Haas observed.

The sector has responded. Exports of normal butane more than tripled from January 2013 to January 2014, then set a monthly record this year of more than 4 million bbl in June. For the first eight months of this year, butane exports ran 20.2% above the same period in 2014. And opportunities are out there as global customers seek diversification of supply.

Ukraine, for example, is experiencing a 15% annual average consumption growth of propane and butane, Reuters reported. The news agency cited analyst projections of a 60% increase by 2020, with imports expected to grow from 60% to 80% of total supply. Chronic political tension with its primary supplier, Russia, has encouraged Ukraine to look elsewhere. The country is proceeding with imports from Poland and the Netherlands.

By any other name …

Closer to home, exports of processed condensate are stirring interest. Houston-based Cheniere Energy Inc. has a site in Ingleside, Texas, near the Port of Corpus Christi, to develop a crude and condensate export terminal.

How much condensate is shipped elsewhere is unclear. It’s been a little more than a year since the U.S. Department of Commerce Bureau of Industry and Security issued a private decision to Pioneer Natural Resources and Enterprise Products Partners LP that allowed lease condensate that had been processed through a distillation tower to be exported, defining processed lease condensate as a refined product and therefore exempt from the ban.

However, condensate derived wholly from natural gas remains under the heading of crude oil under the U.S. export classification system’s 2709 Schedule B category. Inquiries by EIA researchers concluded that U.S. exports of processed lease condensate averaged 85,000 bbl/d in the first seven months of this year. The researchers discovered an unusual piece of data: 21,000 bbl/d of crude oil exported to Brazil in July.

Exceptions to the rule

The statistical nugget stuck out as an anomaly because the ban only provides exceptions for crude shipments to Canada and Mexico. Also, with its own crude production increasing, Brazil would not appear to be a market with much growth potential. The EIA estimates Brazilian crude oil reserves at 15 billion bbl and production at 2.95 million bbl/d (MMbbl/d) in 2014. By 2016, Brazil’s production is expected to exceed consumption, although imports of refined products will continue with the U.S. as the leading supplier.

The EIA looked into the discrepancy and confirmed that the exports were of leased processed condensate to be used as a diluent for heavy crude oil, illustrating the difficulty of tracking a product that eludes classification. For companies that wish to devise a strategy and are frustrated about the lack of information available, the EIA feels your pain and complained in its own “Today in Energy” report:

“Clearly, it is not very satisfactory to have one shipment of processed condensate be reported as [condensate derived wholly from natural gas] within the 2709 Schedule B category and be counted as crude oil in EIA’s data systems while other processed condensate shipments are reported within the 2710 Schedule B category and are therefore counted as petroleum products by EIA.”

While its use today is mostly as a diluent, early low-compression internal combustion engines could run on a form of condensate called natural gasoline. In the 1930s, engines with higher compression ratios were introduced that required fuel above octane levels of 30 to 50. Today, condensate is added to heavy crudes from Canadian oil sands, Venezuela and Mexico to move the oil through pipelines.

“It’s basically used as a diluent for the most part up in Canada, which is the best market, I believe, for U.S. condensates,” Haas said. “Their appetite for diluents is voracious and can probably absorb all our condensate, even at our forecasts that we see for NGL production.

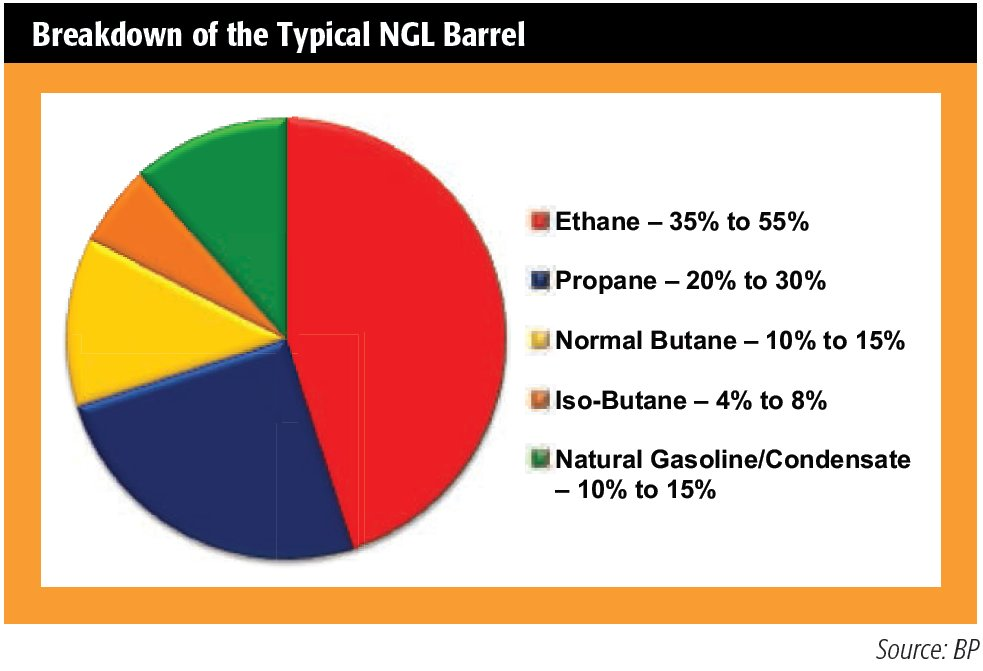

“Condensate is, at best, maybe 15% of the NGL barrel,” he added. “The greatest percentage of the NGL barrel is ethane and then propane and then the butanes and then you get to one-sixth or less is condensate. We could use all that up in Canada if we could produce it and get it to them.”

Flowing south

In the other direction, there is a scramble to get natural gas to Mexico’s buyers. San Antonio-based Howard Midstream Energy Partners LLC has joined with Mexican partner Grupo Clisa to design, build and operate the Nueva Era Pipeline System, which is set to begin construction in mid-2016 with an expected in-service date of June 2017.

Drawing its gas from South Texas, the system will originate with the 30-inch, 190-mile Impulsora Pipeline at Howard’s Webb County, Texas, hub, cross the border into the state of Nuevo Leon. The project already has commitments to transport 504 million MMBtu/d of natural gas to power plants in the Escobedo and Monterrey areas.

Howard isn’t alone, of course. There is a host of other midstream players in the game, including Energy Transfer Partners, Sempra Energy and Kinder Morgan.

“There’s a tremendous opportunity right now for the United States to be exporting to Mexico,” Erica Bowman, Washington-based vice president of research and policy analysis & chief economist for America’s Natural Gas Alliance, told Midstream Business.

“It’s already happening. When you look at what we’ve done between 2009 and 2013, you see that U.S. exports to Mexico have already doubled, and there’s going to be so much more pipeline capacity added.”

In 2014 alone, Bowman said, another 2.7 billion cubic feet per day (Bcf/d) of capacity linked U.S. producers to Mexican buyers, bringing the total export capacity to 8.5 Bcf/d. And that does not even include the slew of projects in the works.

The economics beckon because the country’s growth demands increases in power generation and natural gas is a key part of the policy by the Secretaría de Energía to pursue fuel diversification. As opposed to the trend in the U.S., where natural gas is displacing coal in power generation, Mexico seeks to use gas as a substitute for fuel oil, which is expected to decline in use by 5% annually between 2006 and 2016. Coal use is still expected to rise by 4.3% annually.

Mexican gas demand

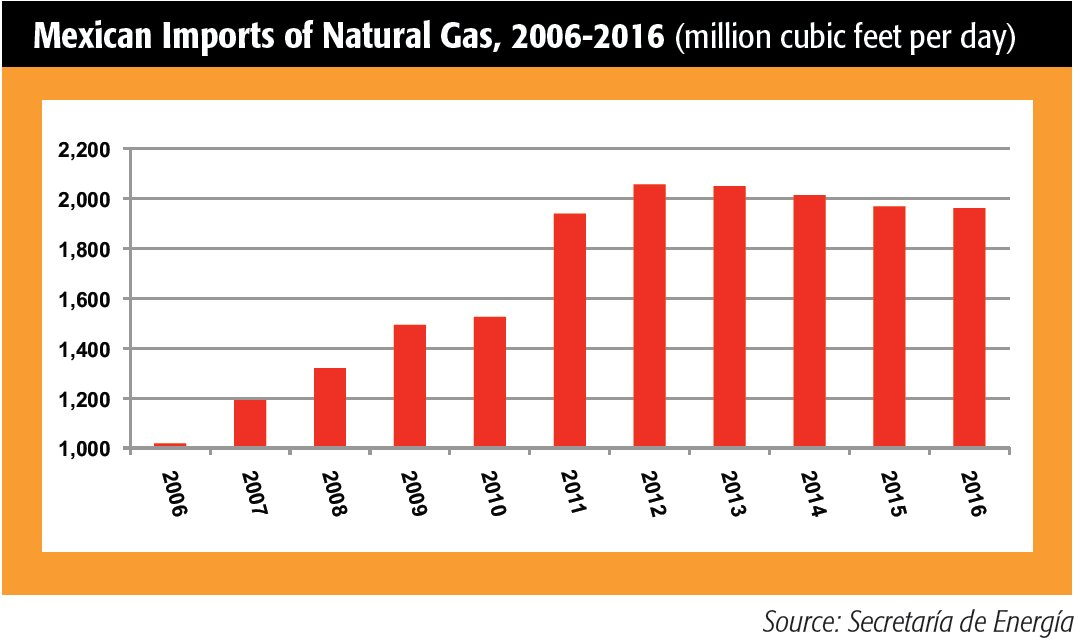

Mexico’s annual average increase in natural gas usage was projected to rise by 3.3% in 2006-2016, from 6,531 MMcf/d at the start of the period to 9,031 MMcf/d by next year, a 38.3% total increase.

“Mexico is a huge, huge opportunity if we can get it right,” Peter Bowden, Houston-based managing director and global head of midstream energy investment banking for Jefferies, told attendees at Hart Energy’s recent Midstream Texas conference in San Antonio.

There are obvious impediments to exporting to this market, among them Mexico’s own abundant reserves. The EIA lists 17 trillion cubic feet (Tcf) of proved gas reserves at year-end 2014, with 545 Tcf of technically recoverable shale gas reserves, the sixth-largest unconventional gas resource in the world. At issue is the Mexican energy sector’s ability to exploit it, at least in the short term, as the country’s oil and gas production declines. While the Eagle Ford geologic formation extends across the border, play activity is mostly restricted to the U.S.

“With any major investment, there are risks inherent but I would argue that, at least in Mexico’s current situation, they’ve experienced an incredible amount of growth domestically with respect to their manufacturing sector, and they’re really looking to natural gas as their fuel of choice,” Bowman said. “So from that perspective, I think that there’s a lot of opportunity for the United States to be filling that void.”

She acknowledged security issues as well, with drug cartels plaguing the border. However, energy resources have a knack for being located in some of the world’s more volatile areas and oil and gas companies have become experienced in dealing with those risks.

“A lot of the projects are more pipeline projects being built to carry the gas deeper into Mexico,” Bowman said. “I think as economic development continues to occur, that’s only going to contribute to a more secure situation because you have people that have jobs and are focused on those jobs, which I think may alleviate some of the security concerns.”

Can LNG compete?

The gloom permeating the industry’s outlook has seeped into the gas liquefaction market as well. Can LNG compete globally with commodity prices remaining stubbornly low? Will demand hold up with China apparently less willing to kick its coal habit than it has indicated in the past?

Cheniere, operator of the Sabine Pass Export Terminal that will launch the large-scale LNG export era when it starts shipping in January, answers with a definitive yes.

“Our message of optimism comes back to the fact that the U.S., from where we sit, really has a secure place in the middle of the global cost curve for both oil and gas, and that’s going to continue to facilitate investment in both the midstream and the upstream segments and continue to allow growth,” Michael Manteris, the company’s director of strategic planning, said at the Midstream Texas conference. “Very importantly, from our perspective, it’s not just the core of the best rock in the Marcellus and the Utica for gas. We’ll be buying gas from all over the country and from all different basins, and so we can see the continued need for investment and growth in all the shale plays, including some of the traditional gas plays.”

LNG exports are the first demand-side response to the U.S. gas supply glut, he reminded attendees. It is not priced relative to coal, a hydrocarbon clearly in decline as if faces regulatory pressures to lower greenhouse-gas emissions.

Customer friendly

The U.S. approach is also more customer-friendly than buyers find elsewhere, Manteris said.

“The total commitment that they have to make in order to secure U.S. LNG is much less than they have to make anywhere else,” he said. “In the U.S., because of our robust upstream and our robust midstream markets as well as our capital markets, the commitment that the gas buyers have to make is on the reservation fee. Our customers pay a reservation fee and whenever they want to lift gas, they tell us and they come get it. They pay for the commodity plus fuel. Our customers are only on the hook for the reservation fee.”

By contrast, competitors’ projects in other parts of the world are stranded gas assets that have no other way of being developed unless it’s for the LNG export market. Buyers are forced to commit to both the liquefaction facility and the commodity.

“In an environment in which balance sheets are stressed and everyone’s trying to conserve LNG and you want the least amount of commitment, this is a real driver for gas buyers,” he said.

Those are short-term approaches, but long term, LNG will continue to surpass oil and pipelined natural gas as the fastest growing fuel in the world. McKinsey Solutions expressed concern in a recent report that delays in final investment decision for LNG export facilities could create a very tight global market starting in 2023. Annual average demand will grow by 4% to 6% until 2030 and another 45 million tonnes per annum (mtpa) in capacity will need to be approved by 2020 to keep up. Present global capacity is about 295 mtpa, according to the Stratas database.

Bullish on gas

McKinsey’s figures equate to an additional 6 Bcf/d to meet demand by 2025. Cheniere is more bullish: it believes another 8.5 Bcf/d will be needed. But Manteris insisted that his calculations are not based on China returning to its ways of white-hot annual growth of 8% to 10% forever. Cheniere has its eyes on LNG legacy production sites in Southeast Asia and North Africa that are fed by natural gas fields in terminal decline.

“We have customers, especially at Corpus Christi—utility buyers—who are replacing old contracts with new contracts,” he said. “This is just to replace declining LNG production from legacy sites.”

So there is and will continue to be demand. The question is: With global commodity prices so low, can you make money shipping LNG abroad? You can, in part because the cost of shipping has fallen dramatically in the last couple of years, from $150,000 a day to $30,000.

Here’s the math for LNG exports to Europe:

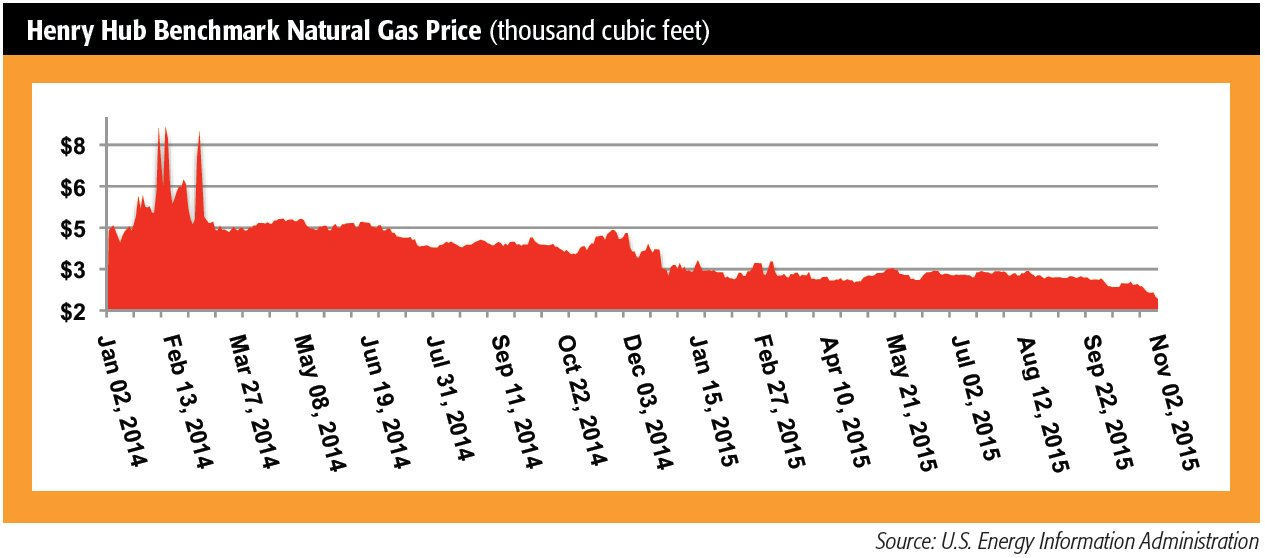

• European Union imported gas price: $6.71/MMBtu (September 2015);

• Henry Hub price: $2.47 (Sept. 30, 2015);

• Cost of fuel for shipping: About 15% or $1; and

• Shipping cost: About $1.

Fuel is a variable cost, but the margin is still more than $2 per MMBtu. The cost of moving LNG to Asia will be higher, of course, but still profitable.

“On the question of whether our customers will lift right now,” Manteris said, “the short answer is yes.”

Not going anywhere

On the question of whether the Obama administration is inclined to lift the ban on U.S. crude oil exports any time soon, the short answer is no.

Energy Secretary Ernest Moniz told lawmakers at a recent Senate Energy and Natural Resources Committee hearing that, while a decision on the ban is the responsibility of the Commerce Department, ending it does not make sense because the U.S. imports 7.64 MMbbl/d of crude oil.

Republican senators complained that the ban is outdated, a relic of a time when OPEC ruled the global oil market and “Love Will Keep Us Together” by the Captain & Tennille ruled the airwaves.

They noted that the shale boom has produced abundant light crude but the refining sector is built to handle heavy crude. Therefore it makes economic sense, they said, to export light while continuing to import heavy. Their arguments were not helped much by recent reports that total crude imports rose for three straight months between April and July.

But another piece of legislation, the Merchant Marine Act of 1920, commonly known as the Jones Act, clouds the political optics for crude exports, Haas said. The act requires ships using marine ports in the U.S. meet compliance requirements that they be U.S.-flagged, U.S.-built, U.S.-owned and U.S.-manned.

“It’s a very protectionist way of regulating an industry, which we’ve done for nearly 100 years,” he said.

“If I’m an Eagle Ford producer and I move my barrel to the Gulf Coast—say a loading terminal in Corpus Christi—and I have a willing buyer—say up in Paulsboro, N.J.—and I want to tank that barrel from Corpus Christi to Paulsboro, N.J., I have to use a Jones Act tanker,” he said. “Jones Act tankers are in such short supply that it costs me about $6 to rent and secure a tanker to move that barrel just a two-day journey or so.”

By contrast, if that same producer is approved for a swap arrangement with Mexico and wants to move that barrel south, a Jones Act tanker is not required because the ship will travel directly from a U.S. port to a foreign port. The distance may be roughly the same, but hiring a non-Jones Act vessel will lop two-thirds off of the transportation expense.

“It’s probably cheaper to import Nigerian or Brent crude right now than to hire a Jones Act vessel to move Eagle Ford crude just up and around the coast,” Haas said. “I can’t imagine that’s a palatable political reality. If U.S. regulators and legislators remove export restrictions, nearby foreign nations could get our oil for $2 per bbl, while the refiners in the East Coast and the drivers in the very city that approves this change, Washington, D.C., would have to pay $6 per bbl to get Eagle Ford oil.”

Cost-effective

If those costs are not driving government policy, they do drive business thinking.

“One of the things that I really like to look at when I’m thinking of crude oil exports is: If I just look at Brent and WTI [West Texas Intermediate], what is the expectation of the marketplace?” asked Arthur J. “A.J.” Brass, CEO of Gravity Midstream LLC, at Midstream Texas.

“At the end of the day, what are people who are really putting money on the line saying about this? We can look at the futures market and what the forward curves look like for Brent-WTI.”

The futures prices now trend upward. In 2014, the forward price expectation was that WTI would trade at a $10 to $11 discount to Brent for the foreseeable future.

“At those numbers, there ought to be a pretty vibrant opportunity to export crude, assuming a shift in the regulatory environment,” Brass said. “Those numbers made perfect sense.”

Of course, they didn’t stick. Six months later, the Brent-WTI differential was down to about $7. For December, the spread is less than $3. Even if the ban were to be lifted, the margins are too squeezed to make it feasible—for now.

Brass wasn’t finished asking questions. “What are breakevens of U.S. production relative to international?” he said. “When we look at a host of OPEC producing countries, we see that their net production costs are substantially higher than what we see in the U.S. Granted, in this flat-price environment, everything is marginal, but when we stack our production costs against international production costs, we should accept that we are the low-cost manufacturer of oil.

“Long term,” he said, “that will lead to exports.”

The Brent-WTI differential will widen as prices rise, benefiting U.S. sellers competing against overseas producers with higher production costs.

Gravity’s strategy is based on the logic of pragmatic optimism. Opportunities may be scarce, but that provides time to prepare for when they return in force.

“As a midstream industry, we need to look at how we are viewing our assets with regard to exports,” Brass said. “What can we do with storage and tankage in times that we can’t get oil to export and how are we going to be ready?

“Because exports will come,” he insisted. “We are the cost-competitive manufacturer of oil. It’s just a matter of waiting it out until the price deck returns.”

Recommended Reading

Permian NatGas Hits 15-month Low as Negative Prices Linger

2024-04-16 - Prices at the Waha Hub in West Texas closed at negative $2.99/MMBtu on April 15, its lowest since December 2022.

BP Starts Oil Production at New Offshore Platform in Azerbaijan

2024-04-16 - Azeri Central East offshore platform is the seventh oil platform installed in the Azeri-Chirag-Gunashli field in the Caspian Sea.

US Could Release More SPR Oil to Keep Gas Prices Low, Senior White House Adviser Says

2024-04-16 - White House senior adviser John Podesta stopped short of saying there would be a release from the Strategic Petroleum Reserve any time soon at an industry conference on April 16.

Core Scientific to Expand its Texas Bitcoin Mining Center

2024-04-16 - Core Scientific said its Denton, Texas, data center currently operates 125 megawatts of bitcoin mining with total contracted power of approximately 300 MW.

What's Affecting Oil Prices This Week? (April 15, 2024)

2024-04-15 - While concerns about the stability of oil supply are increasing, Stratas Advisors does not expect oil supply to be disrupted – unless there is further escalation in the Middle East.