Source: Hart Energy

In the past year, the Midland and Delaware have become exclusive neighborhoods—the oil and gas industry’s Midtown Manhattan and Beverly Hills, without the view.

Acquisitions in the Permian averaged $30,000 per acre in January. Companies talked up low breakeven prices and rich internal rate of returns as they entered huge deals.

Now, on the cusp of a recovery, E&Ps in the Permian and other cost-effective shale plays are boosting capex by 50% or more compared to 2016, analysts said.

Enter the oilfield services sector, which may play spoiler to the E&Ps.

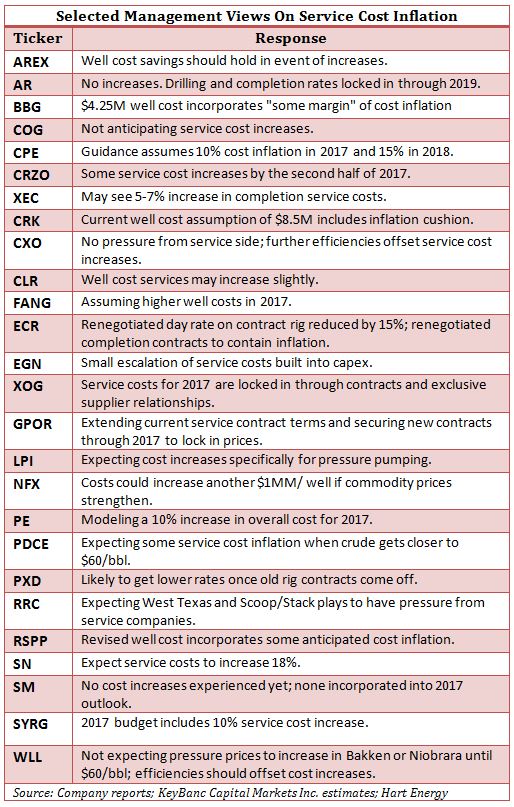

Many operators, having survived in part because of lower service costs, are preparing for a wave of inflation that could bump up prices by 10% to 15%. The cost for rigs, pressure pumping, proppant and transportation all stand to see price adjustments.

In some sub-plays, that could mean the difference between breaking even on prices and just breaking.

Rising prices are already hitting some E&Ps, and not just in the Permian. In the Oklahoma Stack, the Bakken and Eagle Ford, price inflation is expected or evident. In the Eagle Ford, for example, Sanchez Energy Corp. (NYSE: SN) projects cost inflation to hit 18%.

The industry is clearly ready to drill as OPEC production cuts have oil prices rising. In 2017, the rig count is expected to rise by 40% after the aggregate number of rigs have either increased or held flat in 32 of the past 36 weeks.

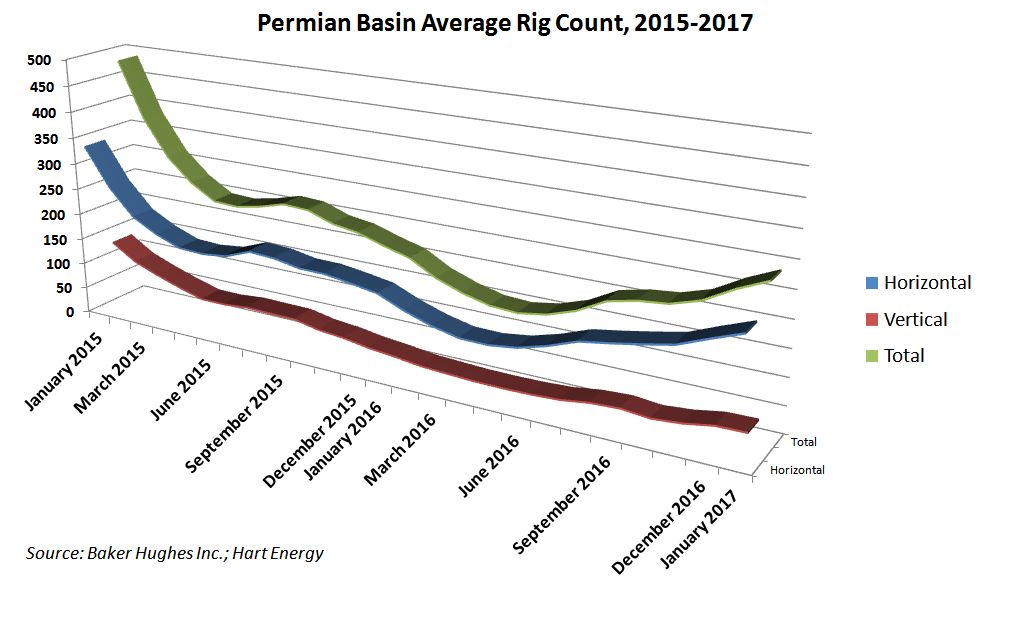

The Permian has shown the greatest appetite. Since rig counts bottomed, 250 rigs have returned to Lower 48 shale plays—half of them in the Permian.

In late January, Delaware operator Laredo Petroleum (NYSE: LPI) noted that drilling efficiencies have led to gains that will be somewhat offset by “recent increases in service costs” which have gone up 16% in one month.

“Capital costs for Upper and Middle Wolfcamp wells drilled on multiwell pads are expected to be about $6.4 million for a 10,000-ft lateral completed with 1,800 pounds of sand per ft,” Laredo said in a Jan. 17 report. A month earlier, well costs were reported to be about $5 million.

Parsley Energy Inc. (NYSE: PE) is planning for a 10% increase in overall costs by the end of 2017 and 5% on average for the year. Diamondback Energy Inc. (NASDAQ: FANG) estimates well costs will rise by up to $5.5 million this year, compared to less than $5 million in 2016.

“Most operators in our universe are factoring in 5% to 15% service cost inflation for 2017, primarily in the Permian,” said David Deckelbaum, an analyst at KeyBanc Capital Markets, in a Jan. 23 report. “However, we expect E&Ps to build on the knowledge gained regarding efficiencies during the downturn that should allow for efficient capital deployment despite modest increases in service cost.”

As active rig count ramps up and operators accelerate activity in 2017, “the question of whether E&P companies can retain the cost advantages that they have built over the downturn arises,” Deckelbaum said.

Larger pad sizes, faster drilling and improved completion techniques should help to offset some price increases, he said. And the market will have to tighten significantly before more measurable cost increases are seen, likely in second-half 2017.

But prices will increase, analysts, E&Ps and service companies say.

At Their Mercy

Many companies have touted improved efficiencies and technology for dramatic well cost reduction while downplaying services companies’ price reductions. Overall, the industry’s well costs have gone down roughly 40%.

“We think that has largely due to service pricing having come drastically down the last two years,” J. David Anderson, senior analyst at Barclays, told Hart Energy. “In fact many of the service companies that we currently cover are at negative EBITDA margins, which is simply unsustainable. Drilling efficiencies have played a role—there’s no doubt about it. But that only represents one-third of well costs.”

And now, demand for rigs is growing, led by the Permian.

Barclays Research estimates that Permian production will grow the most in 2017, by 350,000 barrels per day (bbl/d) compared to 2015. The Bakken is expected to decline by 40,000 bbl/d and the Eagle Ford is projected to fall by 150,000 bbl/d.

“Of the major basins, the Permian has had the largest increase in horizontal rigs since May, increasing by roughly 100,” said Jackson Sandeen, a Wood Mackenzie senior research analyst.

Generally, E&Ps in West Texas could realize greater margins and have already felt a labor/ equipment pinch in fourth-quarter 2016 driven by demand.

What continues to draw so large-scale deals to the Permian is what is now driving rig count: assets account for about 60% of resources with breakeven prices below $40 oil, according to Barclays.

“The Permian is likely to see the largest uptick in spending year-over-year, but producers also plan to boost spending in the Eagle Ford and Bakken,” said Warren Russell, an analyst at Barclays.

Price increases could be felt more acutely for operators elsewhere, Sandeen said in a January report, “U.S. Upstream: Five things to look for in 2017.”

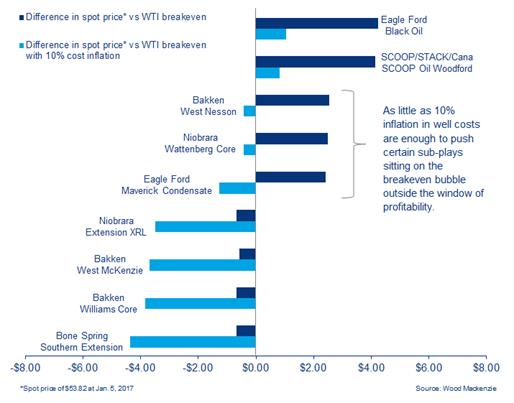

Utilization rates continue to rise across the service sector and the Wood Mackenzie’s base-case is well costs rising by 10%. That includes pressure pumping up by 20% and already-strong pricing power by proppant suppliers intensifying.

“Expect inflation to rise as South Texas and Williston Basin assets compete for resources in a $55 to $60/ bbl price environment,” he said.

At 10% cost inflation, some plays begin to falter. Breakevens go up just 6%—but still enough to shove parts of the Bakken, Niobrara and the Eagle Ford out of their profit zones.

“While seemingly marginal, this uptick renders many positions out of the money until further improvements are made in either well productivity or prices,” the firm said.

And pricing could also go even higher if service companies decide to opt for margin over market share—providing service at large discounts.

“This would essentially leave upstream E&Ps at the mercy of service partners, which have been shouldering the brunt of the pain since oil's pullback,” Sandeen said.

‘Something Higher’

For several months, operators have downplayed the potential for service prices to knock their cost savings off stride. But recently, sentiment has changed.

David Tameron, senior analyst at Wells Fargo Securities, said in recent conversations E&Ps have acknowledged they will see “10% to 15% service cost inflation year over year.”

Service companies have clung to the edge of the downturn with margins in 2016 more than 20% below the historic average, Tameron said.

Major service companies Schlumberger Ltd. (NYSE: SLB) and Halliburton Co. (NYSE: HAL) are being unambiguous about pricing.

Schlumberger CEO Paal Kibsgaard said in January that a sustainable operating environment would require “significantly more pricing.” Halliburton CEO David Lesar said E&Ps’ budgets should probably use “something higher” than 5% to 10% to account for price increases.

From a service perspective, Sandeen said the risk to a robust recovery is two-fold: equipment and manpower and transportation.

“The quality of available capacity—equipment and manpower—may not be enough to service the increased demand and service costs move sharply above our estimated average,” he said.

The challenge stumping analysts and operators is grasping how much of rig capacity is mothballed or how quickly it can return to service, he said.

Anderson said the supply chain is a large part of how services bill operators. Proppant, maintenance, repair and upgrading of equipment needed in the field and transportation are the basic barometers.

“There’s a lot of pressure pumping and land rigs idle right now, but getting it back to work is going to take some time—longer than people realize,” he said.

And the “last mile trucked”—meaning transporting sand, equipment and materials to well sites—is increasingly problematic for E&Ps and service companies.

“Trucking has been a major issue and is going to continue to be a pinch spot for many of these companies,” Anderson said.

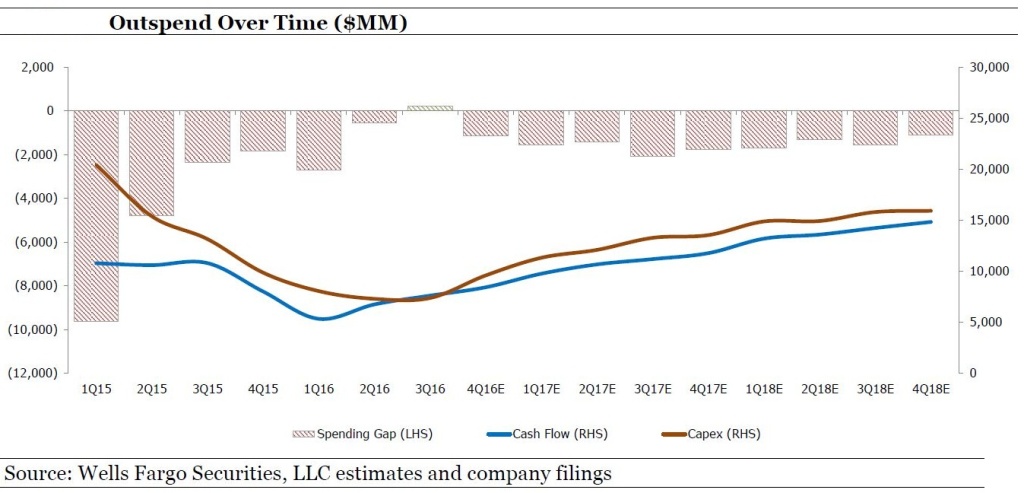

But Tameron noted that E&Ps have certain tendencies that lend themselves to drilling anyway.

While companies will continue with their “growth within cash flow” mantra, Tameron said old habits die hard. Companies outspent cash flow by 145% in 2015 and 111% in 2014.

“Our estimated 2017 capital spend is 116% of cash flows,” he said.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Biden Totters the US LNG Line Between Environment, Energy Security

2024-01-30 - Recent moves by U.S. President Joe Biden targeting the country’s LNG industry, which has a number of projects in the works, are an attempt to satisfy environmentalists ahead of the next upcoming presidential election.

EQT’s Toby Rice: US NatGas is a Global ‘Decarbonizing Force’

2024-03-21 - The shale revolution has unlocked an amazing resource but it is far from reaching full potential as a lot more opportunities exist, EQT Corp. President and CEO Toby Rice said in a plenary session during CERAWeek by S&P Global.

The Problem with the Pause: US LNG Trade Gets Political

2024-02-13 - Industry leaders worry that the DOE’s suspension of approvals for LNG projects will persuade global customers to seek other suppliers, wreaking havoc on energy security.

Pitts: Producers Ponder Ramifications of Biden’s LNG Strategy

2024-03-13 - While existing offtake agreements have been spared by the Biden administration's LNG permitting pause, the ramifications fall on supplying the Asian market post-2030, many analysts argue.

Belcher: Election Year LNG ‘Pause’ Will Have Huge Negative Impacts

2024-03-01 - The Biden administration’s decision to pause permitting of LNG projects has damaged the U.S.’ reputation in ways impossible to calculate.