With more than 10 prospective pay zones and EURs of between 1 million and 2 million boe, appetites are whet for a slice of the Powder River Basin’s more than 1 million acres. (Source: Jeremy Charles)

A version of this story appears in the November 2017 edition of Oil and Gas Investor. Subscribe to the magazine here.

In late September, Maurice W. Brown Oil & Gas LLC (Bidder No. 33) was heatedly battling Titan Exploration LLC (No. 18) and Navigation Powder River LLC (No. 38) for parcels southwest of Wright, Wyo., along Highway 387 and Cosner Road in Campbell County.

The 815 acres that were in play in southwestern Campbell are in a Powder River Basin hot spot operated by EOG Resources Inc. (NYSE: EOG), Devon Energy Corp. (NYSE: DVN), Anschutz Exploration Corp., Liberty Resources LLC and others.

For the Bureau of Land Management’s Parcel 62, a bidder, No. 70, dropped out after Cheyenne-based Brown’s automated bid—set to raise any competitor by $1—posted $13,001 an acre. Houston-based Titan jumped in with $13,500. Brown auto-raised. Within 51 seconds, Titan was at $15,000. Brown won with $15,001.

For Parcel 63, Titan sparred with Navigation, seeing Navigation’s $3,501 and raising to $12,000. Within 19 seconds, the match grew to $16,001. Navigation won.

Wold Energy Partners's leasehold was put together with more than 160 transactions, said Jarred Kubat, the company's vice president of land, legal and regulatory.

For 64, Nos. 70 and 74 were one-on-one, taking the contest to $12,000. Titan showed up in the final seconds with $12,501 and won.

Over at 65, Titan was sparring with Brown, which had briefly sparred with Navigation. The top bid had grown from about $5,000 to $12,000 in the prior 70 seconds. Brown won with $12,001.

In the bidding for 66, Navigation showed up in the last 14 seconds against Brown’s auto-raise and pushed Titan out. The parcel went to Brown for $16,851. Some three minutes earlier, the top bid had been $4,000.

Of the BLM’s $38.74 million of winning offers for 106,687 acres that morning, these 815 acres alone drew $11.2 million. Mark Pearson, president and CEO of privately held Liberty, noted that a BLM sale in February saw similarly competitive bids. “Tracts around us went for an average of $9,500 an acre and, for some tracts, the high bid went to more than $16,000 an acre.”

In that round, when top bids totaled $129 million for 183,155 acres, Brown, Titan and Navigation sparred as well, wining with up to $12,500. Another hot block went to Midland, Texas-based Carlow Exchange Properties LLC for $13,500. The highest-bid parcel, $16,500 an acre, was won by Durango, Colorado-based Peak Powder River Acq Res LLC.

Jarred Kubat, vice president of land, legal and regulatory for privately held Wold Energy Partners LLC, said the sale this past spring “really lit this basin on fire in our neighborhood.”

Visiting with Investor via phone a day after the September sale, he said, “Yesterday, we saw those same comps. You had $16,000-an-acre-plus parcels offsetting previous comps that were $13,000 an acre, which shows that the competition is not only remaining but increasing.”

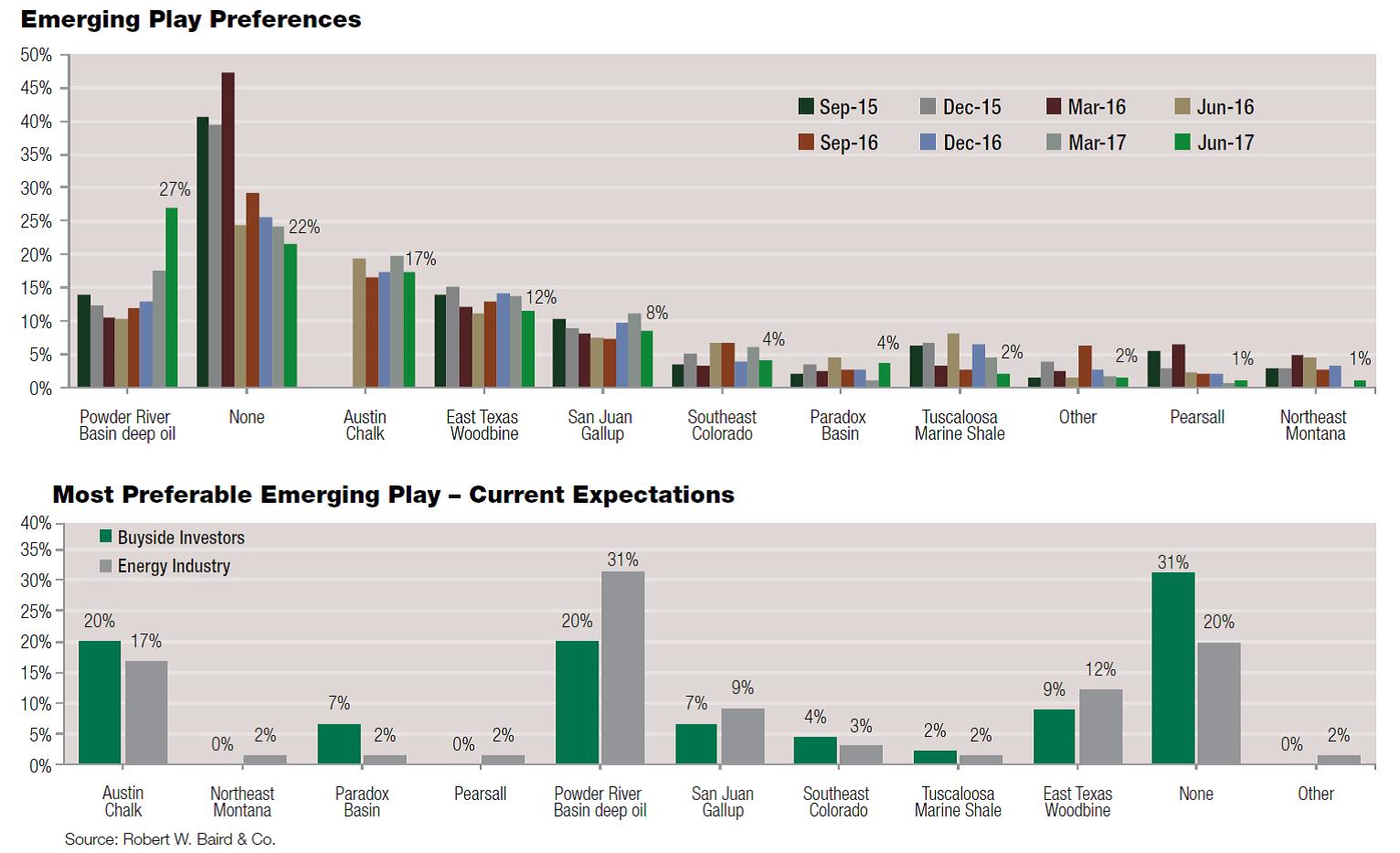

R.W. Baird & Co. Inc. analysts reported this summer that quarterly survey participants’ “emerging-play preferences” had grown to 31% for the Powder from 11% nine months earlier. The basin was the most cited; in second place, “None.”

“This positive sentiment reflects the incremental rig activity in the state of Wyoming ...,” they reported.

Before Thanksgiving Day of 2014, there were 63 rigs drilling throughout Wyoming, according to the Baker Hughes Inc. (NYSE: BHGE) count. That declined to seven in the summer of 2016. In September, the number was 25. Wold Energy reported that the Powder count was 16 in early October.

Pearson said that, for several months, there were no rigs. “You’ve gone from no work going on to what I would call an active exploration program showing great promise. It’s not just one company it’s working for.

“And you have a lot of infrastructure in place. It will take some time to work out the best completion recipes and the best well designs, but industry is on its way to doing that.”

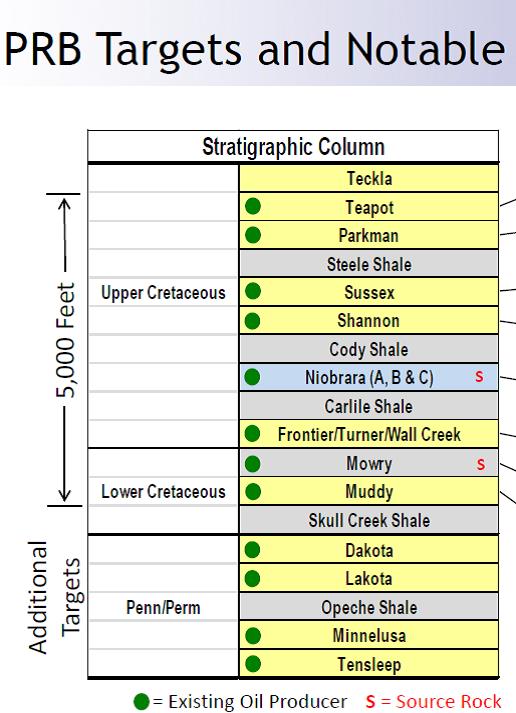

The 5,000-Foot Column

Overall, the Powder’s stratigraphic column of six targeted Cretaceous sandstones—Teapot, Parkman, Sussex, Shannon, Frontier/Turner and Muddy—and two source rocks—Niobrara and Mowry—goes on and on. “You’re talking about 5,000 feet of column,” said Joe DeDominic, Anschutz president and COO.

More than 17,000 productive verticals have been drilled into these formations historically along with upper Pennsylvanian-age sandstones Dakota, Lakota, Minnelusa and Tensleep and, altogether, have produced 3.1 billion barrels of oil equivalent (Bboe), 84% oil. Of this, 2.15 billion barrels have come from the Frontier/Turner, Muddy and Minnelusa. An additional 600 million have been produced from Shannon, Dakota and Tensleep.

The verticals have produced an average of between 100,000 and 400,000 boe each. Altogether, potential targets total 14, counting three within the Niobrara—A, B and C—DeDominic said. Denver-based Anschutz estimates it has more than 6,500 gross locations in Converse, Campbell and Johnson counties—just in the Cretaceous rocks—with net resource potential of 1.1 Bboe.

Holding 360,000 net acres, the longtime Rockies operator began to transition in 2013 to oil-rich, producing areas, letting go of legacy acreage in more challenging areas, such as New York. The Powder was a compelling choice, DeDominic said. “We had some history, some knowledge, some background in the Powder. It was at the top of our list.”

The company also holds pieces of the Piceance, D-J and Green River basins, “but the Powder is, by far, the largest project in our portfolio. You’re starting to see industry come around to how the basin stacks up against other—higher-profile, if you will—basins.”

The basin has gone from no rigs in 2016 to an active exploration program, said Mark Pearson, president and CEO of Liberty Resources.

In a report this spring, Samson Resources II LLC compared the Powder with the Delaware Basin. Both have multiple targets along more than 4,000 feet of column, are overpressured and buried at more than 7,000 feet, have significant original oil in place, include conventional as well as unconventional targets and are primarily oil-bearing.

Samson holds some 153,000 net acres, 80% HBP, in Converse, Campbell and Johnson counties. It estimates 3,200 gross locations, 720 net; economic locations, 800 gross and 160 net. The potential, when applying modern completion and lateral designs, “could prove to be the next Permian Basin,” it added.

One difference is the water cut. Tudor, Pickering, Holt & Co. (TPH) analysts reported this summer that most of the Powder wells produce less than a half-barrel of water per boe in the first few months as well as after two years online.

Court Wold, vice president and CFO of Denver-based Wold Energy, said, “Water disposal is not as burdensome in the Powder where we have 20% to 30% water cuts, compared with the Delaware and some other basins where operators may have four or five times the volume of water as oil.”

Meanwhile, as for sourcing frack water and disposing flowback, operators reported no concerns.

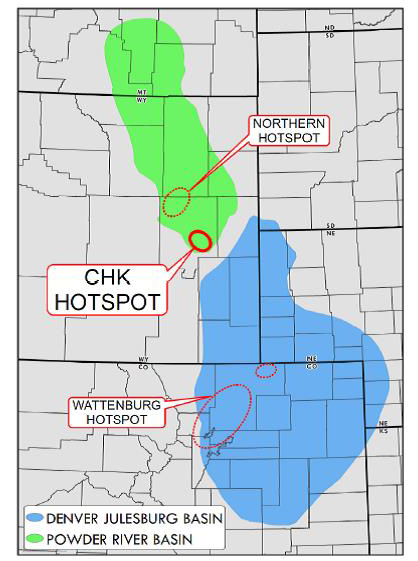

Hot Spots

Denver-based Anschutz had looked at adding in the D-J Basin, DeDominic said, but it was very competitive. “We were unsuccessful in building a large leasehold there.”

In the Powder, it could grow. Its average working interest across the basin is 60%; net revenue interest, 82%. Two-thirds are held by production. Of 226 wells in which it has an interest, 12 are operated. It’s a nonop partner “with pretty much every operator that’s up there.”

Net production is some 3,000 boe/d from Parkman at 8,000 feet to Mowry at 13,000 feet. Its 2017 capital program has two rigs drilling a 12-well program: six Frontier, four Niobrara and two Turner. About half of these are in the extension of the northern hot spot at the western intersection of Campbell and Converse counties; the other half are on the northern edge of the southern hot spot in central Converse, where Chesapeake Energy Corp. (NYSE: CHK) is actively drilling.

DeDominic said of the hot spots, “Those source rocks are more mature and that oil has been cracked into gas, so there is a higher gas content in some of those zones. We’ve seen areas up to 80% gas, but it’s localized and more isolated to some of the deeper formations.”

The source rocks—Niobrara and Mowry—stretch from the basin’s southern tip into Montana. “They cover the whole basin, but there are very few tests in the northern half of the basin.”

The basin's sandstones are "the low hanging fruit" at $48 oil, said Joe DeDominic, president and COO of Anschutz Exploration.

The first Shannon producer was drilled in 1890, “so there’s a lot of historical data out there.” All of the conventional zones have seen the bit.

“It’s taken our geologic team a long time to go over that information to high-grade areas to drill that are Tier 1.” With vertical pilots to check the data, Anschutz has confirmed a 50-mile swath in which the formations’ attributes are very similar.

While horizontal holes and fracture stimulation have made economic amounts of oil production possible from super-tight rock, operators in the Powder are primarily landing in the sandstones. “And the reason why, including ourselves, is that’s the low-hanging fruit.

“At $48 oil, we need the best stuff to make the margins work, which we can make work. The Niobrara and Mowry [shale] at today’s cost and today’s commodity prices are challenged, so, as an industry, we need to continue to improve those results.”

1- to 2-Million-boe EURs

Chesapeake entered the Powder in 2007, primarily chasing Niobrara Shale. Spending in the play was suspended in 2015, but its science work didn’t stop.

In the beginning, its Niobrara spacing was too close and laterals were short and understimulated, it recently summarized. Spacing in the condensate window is now some 1,100 to 1,320 feet, and frack intensity has been increased with tighter cluster spacing and more proppant. It expects to also test the Niobrara A and C benches for the possibility of stacked/staggered horizontals.

A 9,500-footer in Niobrara B made 130,000 boe, 70% oil, in its first 120 days; a 4,500-footer, 120,000, 46% oil; a 6,100-footer, 160,000, 63% oil. A first Mowry well was flowing between 4.5- and 5 million cubic feet per day (MMcf/d). Coring is planned for untested Parkman benches next year; one well IPed 763 boe/d, 94% oil.

Organic entry with scale isn't possible now. "If you want to assemble 10,000 acres or greater, that's over," said Court Wold, Wold Energy vice president and CFO.

EURs from Sussex are between 750,000 and 1.35 MMboe per well. The first-quarter 2018 drill cost is expected to be $160 per foot. Completion costs this year were some $257 per foot.

Chesapeake’s primary focus currently, however, is on the Turner. Its Rankin 5-33-68 1H produced 79,000 barrels of oil during its first 120 days from a 4,500-foot lateral with a peak rate of 2,886 boe/d, 51% oil. Sundquist 9-34-71 13H produced 209,000 bbl from a 7,100-foot lateral its first 180 days; the 2,560 boe/d peak rate was 80% oil. Its more recent Graham 23-35-71 15H had a peak rate of 1,700 boe/d, 80% oil, from 4,500 feet of lateral.

Tim Beard, vice president of Chesapeake’s Gulf Coast and Rockies business units, said, “We’ll probably continue drilling up to 2-mile laterals going forward.” A third rig was due to start work in October—also drilling Turner. Plans through year-end 2018 are for six Turner spacing tests, five tests of the southern hot spot’s boundaries and 20 wells in its high-graded acreage.

Its Turner drilling cost was $351 per foot earlier this year; completion, $542 per foot. Chesapeake expects drill costs to decline to $244 a foot in early 2018; completion, to $352 a foot.

The current Turner EUR is 1.3 to 2.1 MMboe. Breakeven is $30 to $35 a barrel. The rate of return is 40% to 60% at $50 oil and $3 gas.

Michelle Hileman, Chesapeake manager, geosciences, said, “With the Turner performing the way it has and with some additional adjustments, we’ve added over $1 billion of development value since October of 2016.”

The producer expects to exit 2019 at about 35,000 boe/d from the basin. It currently has 290,000 net acres.

Tim Beard, Chesapeake vice president, Gulf Coast and Rockies business units, said initial horizontal interest in the Powder targeted the shale. "People weren't out there looking for the tight sands as much."

Beard said, “The Turner is over the vast majority of our acreage. However, it’s not over all 290,000. The quality does change somewhat across our acreage. There are slightly thicker areas and slightly thinner areas. But, overall, we have a nice sandstone package that we will be able to drill over the majority of our position.”

The Turner and Sussex are about 500 feet of column. “We know where they are over our acreage because we have more than 100 vertical penetrations to the Turner just in our footprint. Plus, we have 3-D seismic coverage over the entire area that is prospective for Turner and Sussex.”

Chesapeake is currently producing some 19,000 boe/d gross from Sussex, Niobrara and Turner. It estimates it has some 2.7 Bboe of gross recoverable resource—about 1 million per operated potential location. About 1.28 Bboe is estimated from Mowry; 900 million, Niobrara and Turner; 380 million, Parkman and Sussex; the balance, other formations.

In its hot spot, mapping suggests virtually any section overlays four prospective landing zones, including multiple zones in the Parkman.

Early on, operators primarily chased source rocks, which likely delayed horizontal development in the Powder, Beard said. While the Barnett, Fayetteville and Marcellus, for example, successfully produce from source rock, these are gassy; getting economic amounts of oil out of shale can be more difficult.

“People weren’t out there [in the Powder] looking for the tight sands as much,” Beard said. “They weren’t thinking necessarily that ‘I’m going to go chase the sands.’”

Hileman said, “A lot of these tight sands are orders of magnitude higher porosity and higher perm. They’re overpressured and their deliverability and economics are, in a lot of cases, second to none. I think those sand plays are really attractive at current commodity prices.”

‘Rival The Core Permian’

Denver-based Liberty operates in both the Powder and the Bakken. In the dolomitic middle Bakken, porosity is between 4% and 8%; permeability, between 10 and 40 micro-darcies, except in the area of Sanish and Parshall fields, where it is some 200 to 300 micro-darcies, Pearson said.

In the Frontier/Turner, porosity is between 4% and 9%; permeability, between 100 and 300 micro-darcies.

“That’s why they produced with conventional vertical wells. They had oil and gas trapped in there but didn’t have the permeability to come out in any large quantities—maybe 1,000 barrels or 10,000 barrels or a couple hundred barrels, but that was it,” DeDominic said.

TPH held a one-day Powder conference in Denver in June that drew 200 attendees, Pearson said. “They had to turn people away.” In September, SunTrust Robinson Humphrey Inc. held a Powder conference that reached capacity and was standing room only.

The Permian has multiple-zone potential. Pearson said, “Suddenly people ask, ‘Where else can we have a hydrocarbon system that has a several-thousand-foot interval that is tight?’” The attraction here is “you’ve got 4,000 to 5,000 feet of section with 10 to 12 pay zones.”

While the horizontal Powder is still in its early stages, he said, it appears to be competitive with other oil plays. “In the last year and a half, the Frontier/Turner is working with great economics—equivalent to the best of the Midland Basin or the Delaware and the best of the Bakken. And we not only have that zone; we’ve got 10 other zones to go after.

“So it is seen as the up-and-coming ‘next basin,’ similar to what the Permian was a few years ago.”

The Frontier/Turner has been the go-to formation for many operators, Pearson said, with a number of wells posting EURs of 1 to 2 MMboe. “And you have others making the Shannon work, the Teapot work, the Niobrara work—or getting close to it.”

TPH analysts reported in June that the industry has tested the entire column now, from Teapot to Mowry, and higher-intensity fracks are driving results “that rival the core Permian acreage.” They added, “Of particular note is the Turner Formation.” EURs are some 150,000 boe per 1,000 feet of lateral, more than 70% oil.

“Assuming a $7.5-million well cost for a 7,500-foot lateral and $3 an Mcf [gas], we estimate 10% after-tax rate-of-return breakeven economics of $30 to $35 a barrel.” In addition, “while the Turner is the most economic formation in our view, our analysis shows that enhanced completions have brought several additional targets—Parkman, Sussex, Frontier, Mowry—in the money at current strip prices.”

Well Density

In the Niobrara in Campbell County, where Liberty is a neighbor of EOG, Pearson said, “You have a deep system that is overpressured and has double or triple the oil in place compared with the Frontier/Turner and with two clear benches that would be equivalent to the Niobrara B and C intervals of the D-J Basin.

“That will allow us to put that wine-rack development in place for multiple intervals in the Niobrara and then multiple other zones, including the Frontier/Turner that is the keystone zone that will really pay for everything.”

Liberty has some 16,000 net acres and, with a minority-interest partner, owns a total of some 20,000 net acres. It began putting this together by buying a position held by Casper-based Ridge Energy Partners LLC, which had obtained the acreage from Bill Barrett Corp. (NYSE: BBG).

The leasehold is some 70% HBP, primarily from shallow, legacy, coalbed-methane (CBM) production. Most of it is held to Mowry. Liberty was drilling a three-well Frontier/Turner program at press time with one on production.

“There are more than 5,000 vertical wells that penetrate the Frontier in the Powder River Basin. That’s an incredible geological dataset for anyone coming into the basin. And, to go into a play—that was already geologically very well-defined—with a new widget was very exciting.”

That new widget is the fractured horizontal. “Instead of wells that might produce 100,000 to 200,000 barrels, I suddenly have something in my toolbox that will allow 1-million-barrel-EUR wells across the basin.”

In some cases, this is being achieved with just one-section laterals, he added. “I think it will depend on where you are, but, around us, most of the development is moving to 10,000-foot laterals.”

In the Powder, each zone is fairly ubiquitous, but each can change in character. “There is more geological variation across the Powder than the Williston Basin, for example, but, if you get 1- to 2-million-barrel EUR out of a single zone—whether it’s 5,000- or 10,000-foot laterals—you’ve got an economic play.”

The higher-perm, higher-porosity nature of the Powder sandstones also means “you need fewer wells to develop a given area. That’s why most operators are looking at two to four wells per section in the Frontier, whereas it’s four to eight in the Bakken.”

Liberty’s completions in the Bakken have been with slickwater. “Liberty has always been a big slickwater proponent in the middle Bakken and the Three Forks,” Pearson said.

In the Frontier/Turner, operators are testing different recipes. Liberty pumped one with slickwater and will pump one with crosslinked gel to see what the difference may be. “Other companies are doing the same kind of thing. Industry as a whole is still in the learning phase, but we’re encouraged by what we’re seeing.”

Beard at Chesapeake said its frack designs are different per formation. In the shale, “we’re going to pump more sand, which typically means more water, more stages. It’s going to be a combination of slickwater and crosslinked gel,” he said.

In the sandstones, “what you’re going to do there is pump less sand, have longer stage lengths and less water. We use a hybrid-style slickwater-then-gel—slickwater at lower sand concentrations, moving to a gelled system at higher sand concentrations.”

Proppant Load

Simmons & Co. International senior analyst John Daniel went on a Powder field trip this summer—taking his kids along, citing “too much Xbox” at home and “with corporal punishment increasingly frowned upon.” One oilfield service provider he spoke to “believes customers will test up into the Montana region as the scope of the play is expected to extend a great distance.”

As for proppant loading, operators are using between 4- and 7 million pounds of sand, “but several customers are testing as much as 20 million pounds per well.” In the area of the heated contest for BLM leases, sand was arriving at a frack job in boxes. Along about 90 miles between Wright and Douglas, “we passed nearly 20 trucks with box-style sand storage. We eventually stopped counting.”

Completion recipes depend on the formation, Anschutz’s DeDominic said. Shallower zones, such as the Parkman, get small fracks; deeper zones, along with the Niobrara and Mowry, of course, get larger jobs.

“Historically, the basin has been understimulated.” Jobs have been upward of 1,000 pounds of proppant per lateral foot. But operators, including Anschutz, are stepping up toward 2,000 per foot, where it makes economic sense.

Rather than throwing “the largest completions in the world” at a formation, “you need to consider the spacing of your wells, the spacing of your stages, how many clusters and how many perforations per stage, etc. We are aligned with that philosophy more than with really big, massive fracks in this basin.”

Long laterals—two sections up to 10,000 feet—are also proving to be economic in returns while reducing surface footprint. “In fact, our company plan is to drill long laterals wherever possible. We’re permitting long laterals in every area we can.”

Wold Energy CEO Jack Wold said operators are collaborating more and more. “There’s no formal consortium, but, on an informal basis, operators are talking on nearly a daily basis.

“There has been a tremendous learning curve on completions, but we still lack R&D that other basins benefitted from over the past several years. Finally, in 2017, we are seeing bigger frack jobs coming to the basin and available services are improving.

“There is a lot of testing between slickwater and 100 mesh sand and hybrid jobs. We’re also testing sand vs. ceramic in the deeper formations.”

Additional large-parcel leasing in the core is virtually done, said Court Wold. “If you want to assemble 10,000 acres or greater, that’s over, unless you’re willing to reach into one of the processes and buy someone.”

The operator’s roughly 150,000 net acres were put together with more than 160 transactions. Kubat said, “Singles and doubles HBPed with one or two producing wells. We’re nearly 80% HBPed. A few were a few thousand acres; others were 500.”

Permian, Stack, Powder

Devon Energy gained its position in the Powder in 1996 from Kerr-McGee Corp. and added 253,000 net acres from RKI Exploration & Production LLC in December 2015. It now holds 450,000 net acres.

In the Turner in its southern leasehold, it’s testing what can be produced from both the upper and lower portions of the formation. John Raines, vice president of Devon’s Rockies business unit, said, “We’ve seen really clean sands on the logs in the upper portion as well as in the lower portion, and we’re testing stacked/staggered development.”

The Niobrara and Mowry are ubiquitous across the basin. Some of the conventional zones are expansive and resource-play-like, but “none of these are going to be uniform or ubiquitous across the basin. By definition, these stratigraphic plays terminate at some point.”

But, north and south, the range of porosity and permeability are fairly consistent, “so, with the 450,000 net acres we have and the way it’s blocked up, we’re able to get in and pretty consistently access the highest-quality rock.”

Michelle Hileman, Chesapeake manager, geosciences, said, "A lot of these tight sands are orders of magnitude higher porosity and higher perm."

Of rigs drilling for Devon, 90% were at work in the Permian and in the Stack play in the Anadarko Basin. At an investment conference in September, the Powder was the subject of one of its slides—in the appendix.

It currently has three rigs drilling for it there—having landed wells in the Turner, Parkman and Teapot so far this year. Its overall Powder net production is 18,000 BOE/d, 80% oil.

Its capital spend has come to be devoted almost entirely to stacked-pay basins—the Delaware, the Anadarko and the Powder. “There was a bit of a downtick in activity in the Powder when oil prices hit the skids, but there still has been a lot of good, consistent work that’s been done that has led to some really good results.”

Most of its legacy position is in Campbell County; most of what it bought from RKI is in Converse County. Formations targeted this year have been Turner, Parkman, Teapot and Niobrara. “It’s very likely in 2018 we will test some additional zones horizontally,” Raines said, “but we’ll probably do that more under the radar.”

Devon is coring and logging up to three vertical wellbores in Converse County that will, later, be used as monitoring wells. These verticals are where Devon wants more data—and also to a deeper depth.

“Well control in the Powder is quite variable,” Raines said. Devon’s northern leasehold is well populated with deep-well data, while “the south is pretty sparse.”

Where it would like more deep-well intel, it is able to leverage its roughly 8,000 square miles of seismic. “It’s a big competitive advantage for us.”

During the year, Devon let some leasehold expire and sold some, “but nothing in our core area.” It continues to do acquisitions in the core and small divestitures elsewhere. Most of its leasehold is HBP. In its federal units, there are some obligations, “but, by and large, a vast majority of our acreage is held.” Most rights are held to basement.

In the more conventional, shallower Parkman and Teapot, completions are not very intense, he added. “The reservoir quality is really good, so you don’t have to create that.” In the Turner and Niobrara, completions have been more intense.

“The Niobrara, we’re keeping tight for now, but, on the Turner, we’ve moved our base design for a two-mile lateral up to 18 million pounds of 100-mesh sand and 230,000 barrels of slickwater. So we’re right at that 2,000-pounds-per-foot threshold, which is up pretty significantly from anything you would have seen in the basin even a year or two ago.”

Transactions

Liberty expects to exit the Powder in the next six to 12 months and exit the Bakken a year or two later. “We’re 3.5 years in our current funding cycle,” Pearson said, “so we’re not looking to acquire any more acreage in the Powder.”

That is, if any were available. “We’ve found it hard to expand our base. We hoped to get in with our initial 20,000 net acres and, now, the only way to grow is through company acquisitions, and those tend to be expensive.”

There is an exit-with-upside option for others, though, and “a number of companies are looking at a roll-up strategy and to IPO with significant size. There is no pure-play public company in the Powder. There is clearly an opportunity for that in the next year or two.”

Some operators that have built and sold in other popular plays are looking at the Powder, he added. “We’ve already seen unsolicited offers for our acreage, looking to come in and put 100,000 to 200,000 net acres together with a view to IPO.”

Kubat at Wold Energy said two transactions in the basin are particularly interesting. EOG bought Yates Petroleum Corp.—obviously for its Delaware Basin leasehold, but including Powder acreage—and Devon bought Powder acreage from RKI, while announcing a deal with another operator in the Stack.

The Powder was “kind of a footnote” in each of the announcements, Kubat said, “but it’s become more notable in the last few months.”

Seaport Global Securities LLC analysts wrote of SM Energy Co. (NYSE: SM), which is focusing on its Permian position, in mid-August that it “isn’t likely to shed” its Powder leasehold “before mid-2018 at the earliest.” SM has some 156,000 net Powder acres—about 114,000 of these contiguous—primarily in northwestern Converse County.

It’s in a joint venture with Schlumberger Ltd. there. “Additional tests in the Niobrara are planned …, which management believes could garner further upside if successful,” Seaport Global reported.

SM has reported that it is currently testing Shannon and Frontier. Four laterals—three in Frontier; one in Shannon—of more than 9,000 feet each had 30-day IPs of between 1,449 and 2,387 boe/d, 80% oil or more.

Court Wold said some privately held operators might sell this year. “Several entities that aggregated operated positions over the last several years are in a position to move into pad development, which will trigger additional A&D in the coming months.”

Devon’s Raines said there is very little left in the Powder for leasing. “There is still quite a bit of federal acreage. They’ve been ratcheting up the number of acres offered. So there is still some acreage to be had.

“But it seems like you’re going to a federal auction or, to get anything chunky, buying someone out.”

Anschutz’s DeDominic said, “I would say the bulk of the land rush is over. If you want to come in and get a position today—and I know there are a few companies that have been trying—it’s difficult to put together a large position.

“You can put 5,000 or 10,000 acres together in one contiguous piece maybe, if you’re willing to pay up and really work on it. It will take some time. But you’re going to have to have the stars aligned or buy someone out.”

Raines said, “You have a lot of private equity on the sidelines right now, looking for a home. I think part of that is due to that the entry cost in the Permian and Midcontinent is causing a lot of people to reconsider the Powder.”

John Raines, Devon Energy vice president, Rockies business unit, said, with the way its 450,000 net acres are blocked up, "we're able to get in and pretty consistently access the highest-quality rock."

Anschutz isn’t looking to add large tracts to its leasehold currently. “We’re very selective. Sometimes I use the word ‘surgical’ in what we’re adding to our position. We’re really trying to focus on bolting on and also increasing our working interest in the areas that we like.”

It’s been doing that with trades. Other operators are doing the same, he added. “A lot of companies have generally a blocked-up position and some are trying to increase working interest in areas they operate. So, we’re seeing more trades, and it makes good business sense.”

Raines added, “We don’t limit trades to acreage trades. We’ve been really active in working with some of our peer companies in doing data trades.”

Federal Land

Chesapeake’s Beard said the Powder’s activity decline until this year was also because several operators were devoting capital to other assets in their portfolios that were more attractive or that they understood better at the time. A low oil price further dampened interest.

Chesapeake itself “slowed down in 2015 with low commodity prices. With no drilling obligations, the team had additional time to figure out ‘What is going to bring value to our acreage position?’”

DeDominic said an early detractor was that a great deal of Powder leasehold wasn’t on the market, and much of it was held by production—including a large amount by late-20th-century CBM wells. Those wells hold the entire stratigraphic column.

“If you have a shallow gas well in the coal seam, you can hold all depths with that, which is what was happening. So there was no incentive for anyone to test [the deeper Powder], drill it, spending risk dollars when they could get into the Bakken or the D-J or the Midland Basin or wherever else and they knew it worked.”

In addition, many operators don’t care to work on federal land, and “a lot of the minerals are federal minerals.” Potential bidders need to nominate tracts for auction that isn’t HBPed, wait for environmental studies and wait for approval. “So that has a longer runway.”

He and other operators are finding that the BLM is stepping up its process, however. Liberty’s Pearson said, “A year ago, it was taking 12 to 18 months, but, now, we’re getting federal permits in six months.” Wold Energy’s Kubat said, “We’ve had a number of ADPs approved in less than 60 days.”

Beard said that, “while we’re not 100% satisfied with the speed, it’s getting much better. We just had permits turn around in a matter of months; in the past, it was two years.

“We got a handful the other day that were just a few months old. So things are turning around from a permitting perspective.”

Jack Wold said, “The basin is quickly becoming a world-class resource play with billions of barrels to be recovered.” As the land-grab phase is nearing an end, “we think the Powder River Basin is in the early innings of the horizontal-development life cycle.”

Wold Energy’s leasehold is primarily in Campbell and Converse counties. It drilled a well that had a 30-day IP of 1,150 bbl/d from the Shannon, “which has been a somewhat underappreciated formation,” he said. “It’s very prolific, and we see great potential from it in our general area.”

Plans are for a continuous-drilling program primarily in the Frontier/Turner across its leasehold. He estimates Wold Energy has some 380,000 net effective acres of Frontier/Turner, Shannon and Niobrara pay.

Differentials for oil in the Powder have improved greatly from as much as $8 less than Cushing to about $3, operators said, likely because more Bakken oil is being hauled south via Dakota Access.

Devon’s Raines said it’s become even better than that. “Generally speaking, in the past few months we’ve seen [the] Guernsey [Wyoming spot price] trading virtually flat to WTI and, in the past few weeks, we’ve seen a premium to WTI.”

DeDominic said that, while the Powder may be just taking off, it’s almost caught up. “I think it’s up and coming. You look at the horizontal well counts and results. About a year ago, we did some comparisons, trying to understand how the Powder stacked up against these other oil basins.

“We had 26% the number of horizontal wells the D-J or Delaware or Midland had, but individual well results comparable to or better than these other, more mature basins. The pace is also picking up.

“But we’re not in the stage of full development mode. We’re not seeing operators drilling six- or eight- or 10-well pads yet. Most operators are drilling two-well pads. We’re drilling one unit with four wells right now.

“It’s not quite at the level of some of the other basins at this point, but it’s coming along very quickly.”

Fastest Draw

News about the number of drilling permits being issued by the state of Wyoming may be greatly misleading. In Wyoming, an owner with a fraction of an acre in a drilling spacing unit (DSU) can receive a drilling permit, making it the operator.

Thus, operators are seeking and receiving hundreds—some even more than 1,000—permits in advance. Mark Pearson, president and CEO of Liberty Resources LLC, said, “Permitting in Wyoming is a little strange in that it is ‘first to permit’ in a DSU. It’s not ‘Who’s the majority operator?’

“You’ve seen companies rack up hundreds and thousands of permits without necessarily doing a lot of drilling—just to get the permits on the acreage.”

Pearson is familiar with a two-section DSU in which one operator had a permit for two wells and a nonop WI owner received permits for the third and fourth wells.

He and others have taken the issue to the Wyoming Oil & Gas Conservation Commission, asking that it at least allow the majority working interest owners to dispute a permit within three business days of issuance, as North Dakota allows. “They have declined to change their system. They say they’re not going to.”

This applies to drilling on federal land too, as a state permit is needed there—in addition to a federal permit. Pearson said that, often, the nonoperator receiving the permits has no intention of drilling. “It’s a two-year permit, and you can get a two-year extension on that,” he said.

Meanwhile, Liberty is receiving permits across its more than 20,000 net acres “to get ahead of this permit race.” It has 270 permits now “even though we’ve only drilled two wells so far and we’re about to drill our third well,” Pearson said.

“But this will allow either ourselves or a future owner of our acreage to move ahead with a multi-rig, continuous drilling program—and this will be the key to unlocking the inherent value in this multizone basin.”

John Raines, Devon Energy's vice president of the Rockies business unit, said, “In Wyoming, permitting has been a bit of a hot topic. With all the money in the basin, you have this race going on to file state permits and capture operatorship.”

Like Pearson, he has seen companies with less than 1% WI capture operatorship, “which is inefficient, to say the least.” He has heard “a limited amount of conversation that the state is thinking about changing the rules, and I hope they will consider that.”

Wold Energy CEO Jack Wold said, "The basin is quickly becoming a world-class resource play with billions of barrels to be recovered."

This year, through August, the Wyoming Oil & Gas Conservation Commission had issued more than 4,900 permits, according to its files. Raines said, “You don’t see that even in the Permian Basin. And, certainly, the level of permitting doesn’t correspond with the level of activity.”

Tim Beard, Chesapeake Energy vice president of the Gulf Coast and Rockies business units, said the good news for it is that it’s the operator in its nine federal units, “so that can’t happen to us there. Outside that acreage, it’s competitive and, at times, quite bizarre.”

Nissa Darbonne can be reached at ndarbonne@hartenergy.com.

Recommended Reading

Deep Well Services, CNX Launch JV AutoSep Technologies

2024-04-25 - AutoSep Technologies, a joint venture between Deep Well Services and CNX Resources, will provide automated conventional flowback operations to the oil and gas industry.

EQT Sees Clear Path to $5B in Potential Divestments

2024-04-24 - EQT Corp. executives said that an April deal with Equinor has been a catalyst for talks with potential buyers as the company looks to shed debt for its Equitrans Midstream acquisition.

Matador Hoards Dry Powder for Potential M&A, Adds Delaware Acreage

2024-04-24 - Delaware-focused E&P Matador Resources is growing oil production, expanding midstream capacity, keeping debt low and hunting for M&A opportunities.

TotalEnergies, Vanguard Renewables Form RNG JV in US

2024-04-24 - Total Energies and Vanguard Renewable’s equally owned joint venture initially aims to advance 10 RNG projects into construction during the next 12 months.

Ithaca Energy to Buy Eni's UK Assets in $938MM North Sea Deal

2024-04-23 - Eni, one of Italy's biggest energy companies, will transfer its U.K. business in exchange for 38.5% of Ithaca's share capital, while the existing Ithaca Energy shareholders will own the remaining 61.5% of the combined group.