Warnings about the presence of Pemex pipelines in Puebla, Mexico. (Source: Shutterstock)

Permian Basin producers’ dreams of more than doubling piped-gas exports to Mexico to feed nine planned Mexican liquefaction plants continue to be overshadowed by a lack of pipeline transport capacity south of the border.

“If sufficient pipeline infrastructure can be put in place within Mexico itself, these proposed facilities could collectively become a significant driver of U.S. gas exports to Mexico,” BTU Analytics analyst Bailey McLaughlin wrote on April 14 in a blog post.

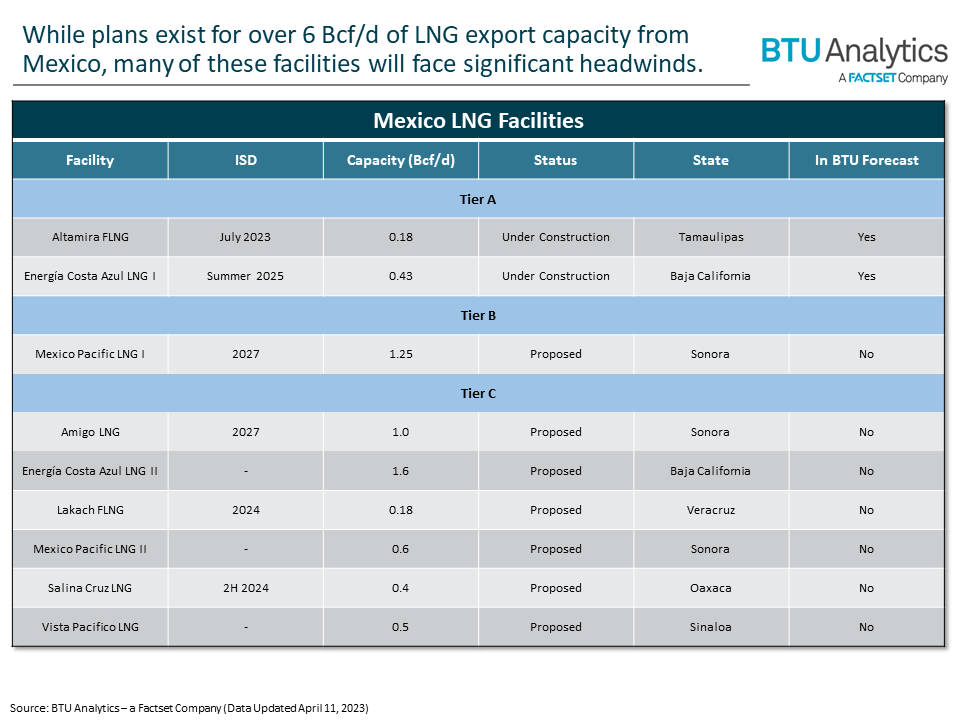

Even though plans exist to develop 6.1 Bcf/d of Mexican LNG export capacity, many of the planned facilities will face significant headwinds, McLaughlin said.

Mexico, home to sizable oil and gas reserves, continues to suffer primarily from a lack of gas production to cover domestic demand amid state-owned Petroleos Mexicanos’ (Pemex) inability to boost reserves and production.

RELATED

Pemex Looks to Hike Production, Boost Self-Sufficiency, Reduce Imports

An abundance of gas production from U.S. shale plays has allowed the North American country to benefit from Mexico’s production woes.

Between April 6 to April 12, 2023, U.S. piped-gas exports to Mexico averaged 5 Bcf/d, according to the U.S. Energy Information Administration (EIA)—about 5% of total U.S. gas production of 100.7 Bcf/d. This compares to about 5.9 Bcf/d for the same week a year ago — 6% of 96 Bcf/d of total production.

Combining U.S. piped-gas exports to Mexico with potential demand tied to the Mexican LNG projects, gas volumes sent to Mexico could reach about 11 Bcf/d.

“However, supply-side solutions are needed for any of these projects to reach fruition,” McLaughlin said. “Due to the often-beleaguered midstream environment in Mexico, the further one gets from the U.S. border and Permian gas, the less reliable the supply needed to feed these facilities becomes.”

RELATED

West Texas Exports ‘Record’ Gas Volumes to Mexico

North American West Coast eyes Asian markets

The Russia-Ukraine conflict has boosted Europe’s demand for U.S. LNG and led to cargoes being diverted from Asia. A number of new domestic liquefaction facilities under construction — and others approved but not yet in construction — aim to capitalize on robust demand expected in both markets.

“However, an opportunity exists on the North American West Coast to directly target Asian markets,” said BTU Analytics’ McLaughlin. “With ample pipeline capacity to the U.S.-Mexico border and cheap Permian gas desiring an end market, Northwest Mexico is one area poised to potentially fill this niche.”

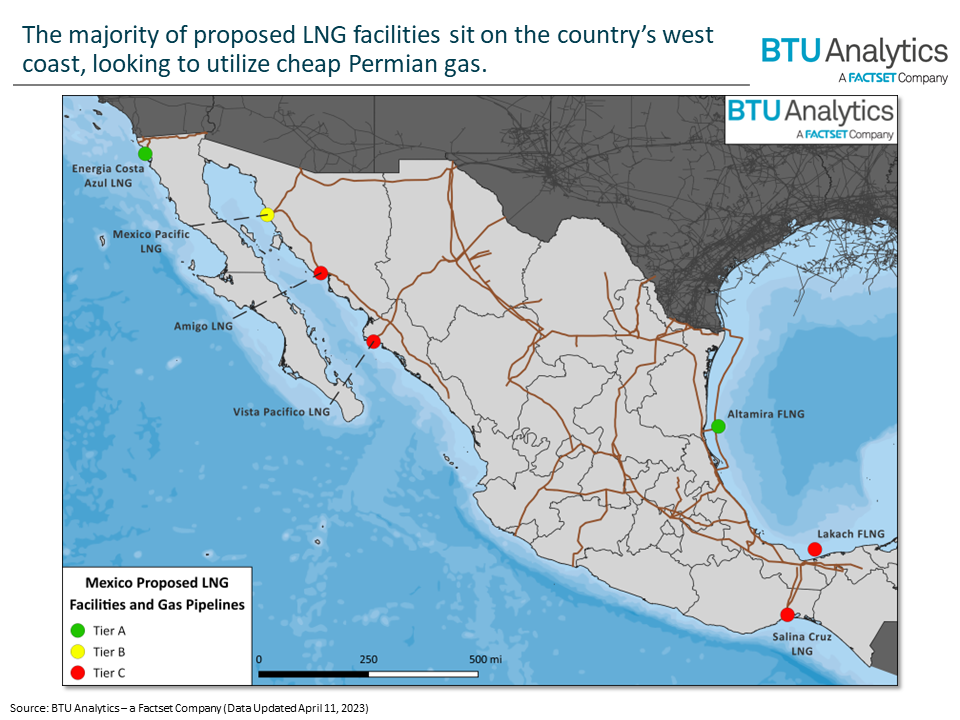

BTU’s proposed list of LNG facilities in Mexico is split into three tiers based on the likelihood of each reaching final investment decision (FID).

Tier A: The Altamira floating LNG (FLNG) unit is currently under construction and slated for shipment to its proposed home off the coast of Tamaulipas, a state in the northeast region of Mexico. The FLNG unit is expected to start operations this summer and tap into existing infrastructure on the Sur de Texas pipeline. Energía Costa Azul LNG I, a project in Baja California, Mexico, is the only facility currently under construction and expected online in the summer of 2025.

Tier B: While yet to reach FID, Quantum Energy’s Mexico Pacific facility holds sales and purchase agreements for nearly all of the 1.25 Bcf/d of capacity associated with its two initial trains. However, current pipeline infrastructure within Sonora and Chihuahua states would only allow one train to run at full utilization and would require construction of ONEOK’s proposed Saguaro Connector pipeline, according to BTU.

Tier C: Projects in this tier include Vista Pacifico LNG, Amigo LNG, Lakach FLNG and Salina Cruz LNG, among others. Even though Vista Pacifico has potential due to open capacity on currently operational pipelines, BTU Analytics is less optimistic on projects such as Salina Cruz and Amigo, owing to a lack of existing infrastructure and the facilities being farther downstream.

Recommended Reading

OEP Completes Acquisition of TechnipFMC’s Measurement Solutions Business

2024-03-27 - One Equity Partners said TechnipFMC’s measurement solutions business will be rebranded as Guidant and specialize in measurement technology, automation solutions and global systems.

Hess: Pre-emption Provision Doesn't Apply to Buyout Deal With Chevron

2024-02-27 - Hess Corp. said on Feb. 27 that a pre-emption provision does not apply to its proposed $53-billion buyout by Chevron Corp. and it remains "fully committed" to the deal.

EQT, Equitrans Midstream to Combine in $5.5B Deal: Reports

2024-03-11 - EQT Corp.'s deal would reunite the natural gas E&P with Equitrans Midstream after the two companies separated in 2018.

Ithaca Energy to Buy Eni's UK Assets in $938MM North Sea Deal

2024-04-23 - Eni, one of Italy's biggest energy companies, will transfer its U.K. business in exchange for 38.5% of Ithaca's share capital, while the existing Ithaca Energy shareholders will own the remaining 61.5% of the combined group.

DXP Enterprises Buys Water Service Company Kappe Associates

2024-02-06 - DXP Enterprise’s purchase of Kappe, a water and wastewater company, adds scale to DXP’s national water management profile.