Far West Texas, below the New Mexico border, is considered one of the most remote regions of the country, yet on a spring day in March you wouldn’t know it. Oilfield traffic congests the few two-lane highways traversing the desert, narrow ribbons of asphalt pocked with potholes. At the intersection of Highway 285 and Highway 652 in Reeves County, haulers carrying water, sand and oil line up three deep to make a turn. A food trailer selling hot lunches is the only “restaurant” within an hour in any direction. It seems the lonely highways of West Texas aren’t so lonely after all.

Here in the southern Delaware Basin, a sub-basin of the greater Permian Basin, a capillary network of gravel roads fingers off the paved roads, accessing well sites in locations that may have gone decades without having a human set foot there—if ever. Dozens of well signs announce what lies beyond the gate, revealing leases by companies big and small: BHP, Anadarko, ConocoPhillips, Cimarex, RKI and Capitan.

Trent Russ, field superintendent for drilling for Cimarex Energy Co., said the southern Delaware has been humming for three years. When Cimarex arrived to explore the play, however, there were no roads, he said, “just javelinas, rattlesnakes, mule deer and cow tracks.”

And no old wells, either. Culberson County, where Cimarex is focused, was virgin territory. “The wells here are all new. It’s an untapped area,” Russ said. The industry has recognized the resource opportunity as well.

This bustle of activity might, however, just be the last vestiges of the 2014 oil boom. Since a high of 568 in November, some 283 rigs have exited the Permian Basin, a 50% retreat and going, according to data from Baker Hughes. The decline parallels the trend nationwide, where rig counts are off some 50% since their peak last year, following the downdraft in oil prices. Cimarex, as a data point, has reined in its Delaware Basin rig fleet from 18 at the high to three.

The sudden drop in Permian land rigs since the beginning of the year gets real just east of Odessa, Texas. Topping a rise on Business 20, some 40 spires of idled drilling units with bright yellow crowns pierce the blue sky in Helmerich & Payne’s yard. They are far from the only ones.

Trent Russ says all wells in Culberson County are new. "It's an untapped area."

Comparing year-over-year EIA data shows the precipitous drop in rigs in the Permian.

“There has been a drastic reduction in activity,” said David Howard, a managing director for energy research for Calgary energy analytics firm ITG Investment Research. “Rig counts are way off, and operators are pulling in capital budgets from 30% to 60%—and that’s the right response.”

At top, David Howard, a managing director for energy research for ITG Investment Research, said, "Whatever price does end up being the new normal, it will be north of where we are today." Above, Darrell Koo, vice president of energy research at ITG Research, has participated in studying the Permian's economics.

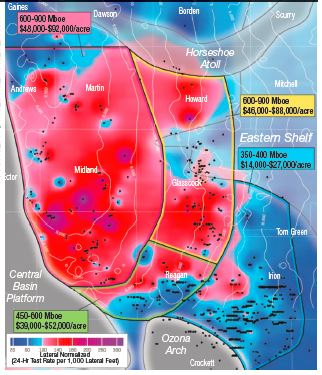

An ITG Research heat map shows the most economic locations in the Midland Basin.

A special place

The oil and gas industry nationwide has reacted swiftly and sharply to the sudden plummet of global oil prices but, alas, the century-old Permian Basin was just gaining its legs as an unconventional shale oil play. Will the world oil glut cut the knees from under the budding Permian?

“The Permian Basin is a game changer for the country and for the world,” said Pioneer Natural Resources chairman and CEO Scott Sheffield. He estimates the Midland Basin Spraberry and Wolfcamp plays alone—where Pioneer concentrates—contain 75 billion barrels of recoverable oil. At its recent peak last year, the Permian represented 15% of the total global rig count.

“The Midland Basin is one of the top five fields in the world, and the Delaware Basin is probably going to be right up there,” Sheffield said. “The world is going to need it, and it’s going to come back.”

Howard and ITG cohort Darrell Koo, vice president of energy research, parse the Permian’s economics based on productivity, recovery and price. Their findings should give Permian players comfort.

“The future of the Permian is bright, even if oil prices don’t recover,” said Howard. “There is a lot of resource, some of the most economic resource in the Lower 48, if not the world. I mean, it’s a pretty special place.”

The Lower 48 shale oil renaissance is driven by three marquee plays, he said—the Bakken, the Eagle Ford, and more recently, the Permian Basin. ITG has concluded that the Permian Basin has the largest resource, due to multiple commercial zones, with economics on par with any unconventional play. “The core of the Permian Basin is as economic as some of the best of the Eagle Ford.”

And with some of the largest resource potential in the world, regardless of what happens to price, operators in the core of the basin are in a strong position relative to peers that don’t have such inventory, he said. “Whatever price does end up being the new normal, it will be north of where we are today, and anything better than today is going to be quite economic for the Permian—especially as service costs adjust to reduced demand.”

High-grading to high ground

This is Sheffield’s fifth downturn since he entered the industry in 1975. Given the current economic environment, “we’re probably better prepared as a company than we have been for any other downturn,” he said.

The company had the foresight to hedge 90% of its 2015 oil production at $71 per barrel and has more than 50% secured at $70 for 2016. Last year, it sold $800 million of assets and, in early November, raised $1 billion in an equity offering. “That prepared us for the Saudi’s decision not to cut production and let oil prices fall in late November,” Sheffield said.

Another $1 billion is expected from an Eagle Ford midstream sale, now in progress. “We hope to enter [the early part of] this downturn with a couple of billion dollars of cash on the balance sheet,” he said confidently.

Almost as if he knew it was coming.

If any company represents the Midland Basin, it’s Pioneer. The Dallas-based operator is the most active driller in the Midland, and holds a massive 825,000 acres there. As of year-end, it produced 115,000 boe/d from the play.

Although flush with near-term cash and cash flow, Pioneer nonetheless throttled back its 2015 planned spend by 45% compared with last year. Emphasizing reduced margins tied to lower oil prices, he said the company will focus on optimizing returns, capital efficiencies and production by high-grading drilling to its best areas. Fifteen of its previous 25 Permian rigs have been released or stacked.

“Everybody’s focused on cost structure,” he said. “We’re trying to gain as much back from the service companies as possible.” Already, Pioneer has experienced a 13% shrink in drilling costs, and expects at least a 20% retraction by year-end.

“The economics are still very good even at $43 oil,” he emphasized, referencing the price in mid-March. “Even using today’s five-year strip prices, the economics are attractive when you look at a 20% cost reduction.”

In the Midland Basin, Pioneer is high-grading its drilling operations to “sweet spots,” areas that for various reasons, including geology and available infrastructure, generate the best returns in the portfolio. The company is operating six of its current 10 Permian rigs in its northern Midland Basin operations in Midland and Martin counties. And although Sheffield has previously compared this region to “13 Bakken shales,” due to its stacked-pay nature, Pioneer will in fact immensely narrow its drillbit focus in the short term.

“We’re focused on one zone primarily, being our best zone, the Wolfcamp B.”

"The Midland Basin is one of the top five fields in the world, and the Delaware Basin is probably going to be right up there," said Scott Sheffield, Pioneer Natural Resources chairman and CEO. "The world is going to need the Permian, and it's going to come back."

It’s thicker, under higher pressure than other zones, and has the most oil in place, he said. Newer wells come on at 2,000 bbl/d. “Wolfcamp B wells pay out quickly and have the best recovery—and we have 20 to 30 years of Wolfcamp B inventory.”

Similar to the operating efficiencies it has realized in its Eagle Ford Shale program, Sheffield believes concentrating on a single zone will deliver “tremendous efficiencies”—and thus better margins—from its Wolfcamp B focus.

“Where we have a certain rig drilling repetitive wells in the same zone in the same area, we see dramatic improvement in time on wells and cost efficiencies. That gives us a lot of confidence that we’re going to have strong economics in the 2015 campaign despite the downturn.”

Already, Pioneer has increased its average lateral lengths to 9,000 feet and upsized its completions recipe in this acreage, including a 50% increase in sand volume to 15 million pounds per well. The company posts average EURs for these longer-lateral wells at 900,000 boe, but reveals the past 20 wells put on production exceed 1 million boe EURs. Where Pioneer deploys this method in the Eagle Ford, it gets a 20% to 30% uptick in reserves for an additional 10% in costs. The Permian tests are less than a year old.

“The question is, will putting in more fluid and sand be worthwhile in a $50 price environment vs. $100? We’ll have to wait another year before we have a verdict,” Sheffield said.

When economics improve sufficiently, Pioneer will begin drilling other zones including the Lower Spraberry, Wolfcamp A, Wolfcamp D, Jo Mill and Middle Spraberry, in that order of priority. “There’s a lot of oil in those zones,” he said.

In its southern Midland Basin region, where it operates a joint venture with Sinochem, Pioneer is pulling all rigs from the southern extent of the area, and will concentrate four rigs in the northern Upton and Reagan county areas.

“The north part of the south is as good as our northern Midland Basin acreage,” said Sheffield, with EURs exceeding 800,000 boe. “But the bottom part of the south typically makes wells at 400,000 to 500,000 boe EUR,” due to depth and pressure issues. “There’s a big difference in the delineation of our southern acreage.”

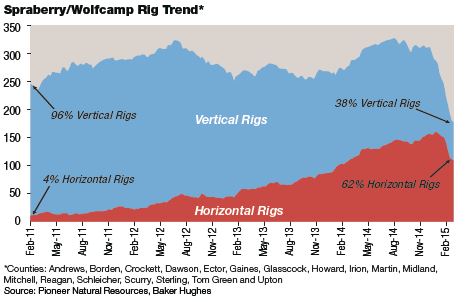

In the past four years, horizontal rigs in the Permian Basin gained ground on verticals, but the recent pullback saw vertical rigs retract by a larger percentage.

Higher GOR gives the western half of the Delaware Basin better EURs, according to ITG Investment Research.

Squeezing efficiencies

One positive side effect of the downturn is a renewed emphasis on squeezing efficiencies out of each well. Beyond enhanced completions, Pioneer is driving cost efficiencies in a number of ways. “We’re pushing the envelope on new technologies,” Sheffield said.

First, it is testing a modified two-string casing design reduced from three, by eliminating the intermediate string, for a potential cost savings of $500,000 to $1 million per well. The trick is in the mud systems: the deeper the well, the more difficult to place cement along the length of the string. Currently, the company has had success in about a third of its acreage, in the southern Wolfcamp joint-venture region, by circulating cement from the bottom up and top down to encase the longer string. “We hope to develop mud systems that will work on 100% of the wells,” he said.

Additionally, the company expects to save $300,000 per well using dissolvable plug technology, thus eliminating the need for coil tubing drill-outs following fracture stimulation. To wring more resource out of its best acreage, Pioneer is testing downspacing and well staggering between its Wolfcamp A, B2 and B3 zones.

Drilling activity in 2015 will be concentrated around existing infrastructure and tank batteries to maximize capital spending in the drillbit. A host of infrastructure projects are being delayed as well.

Once known as a manufacturing machine of the Wolfberry play—a vertical drilling program stimulating a column of stacked zones—Pioneer has laid down its vertical rigs with no plans to revive them. The reason: Returns from the horizontal drilling program trump the verticals, even in today’s environment. “Our Wolfberry returns were good,” said Sheffield, “but not nearly as good as horizontal drilling.”

Even with a reduced rig count, Pioneer aims to place up to 170 wells on production in 2015, just 40 shy of 2014 numbers. Its $1.2 billion Permian Basin capex represents 70% of its total company spend for the year. Sheffield models $55 as the average oil price for 2015, and even at that price projects Permian IRRs will reach as high as 55% on the best wells, and average 35% to 40%.

Sheffield said the company will gear back up when he sees certain signals: U.S. oil inventories decrease from all-time highs; industry production flattens and declines; global demand picks up; and cost reductions reach at least 20%. “When we see those signals happen, we’ll use the $2 billion of cash on hand to jumpstart the rig count.” That could begin as early as July, and he hopes to be running a full fleet of 25 rigs in the Permian by year-end or early in 2016, if his predictions prove out.

“We’re being cautious to make sure 2016 isn’t another $50 oil price world,” he said. “We will start the rigs back up as soon as we have confidence.”

Mashing the margins

ITG reports the breakeven WTI price in the core of the Midland Basin, assuming a 10% rate of return and before cost cuts and efficiency gains, at $50. “At $50 WTI, operators frankly aren’t making a ton of money,” said Howard.

Many operators, though, are telegraphing service cost reductions already approaching 20% and moving higher. The impact of a 20% reduction in well cost is roughly a drop of $10 in the weighted average breakeven across the basin, he said. Under that scenario, in the best part of the Midland Basin, breakeven metrics drop to $40 a barrel. “At today’s prices, that makes all the difference.”

With its Bone Spring drilling program in full swing, the Wolfcamp south of the New Mexico border provided a different opportunity set for Cimarex Energy. Unlike the Bone Spring, "It's a true unconventional shale. It's a regional opportunity," said John Lambuth, vice president of exploration.

ITG’s base-case scenario in the Midland Wolfcamp play suggests a typical well in the core area has an EUR of 600,000 to 700,000 boe, but evidence shows recoveries in some instances could be as high as 900,000 or 1 million barrels of oil, as Pioneer reports. A move in EUR from 600,000 to 900,000 barrels per well reduces breakeven costs by another $10.

While operators are reporting cost reductions, Howard said he’s yet to see it in the data. Instead, as operators gain efficiency on drilling a well, they tend to reinvest the cost savings into larger completions with more sand.

“So while well costs remain relatively constant, you end up with a longer lateral with a lot more sand, which ends up being a better well. If you get better wells and a reduction in well costs, that well could break even at $30,” said Howard. “The core Permian Basin operators are going to be just fine.”

Howard defines the core of the Midland Basin as Martin, Midland, Andrews, Ector, northern Upton and western Glasscock, but “the very best of the best so far has been in Midland County. That’s where the highest rates are today.”

Further, he argues, operators here have proven up four solid economic zones—with some operators talking up to 13 potentially economic zones. The best zone, in terms of consistent results, appears to be the Wolfcamp B, he said, followed by the A, with a little less consistency in the C and D (or Cline) zones. “The surprise is the Spraberry, which is doing remarkably well for some operators.”

The most economically challenged region of the Midland Basin is Crockett and Irion counties, said Howard, at the southern extent of the basin. Average wells in this area test on the order of 60 to 70 boe/d per 1,000 lateral feet drilled, roughly half of the average in the core. “It is shallower, where you have less reservoir pressure and energy.” On the upside, the wells cost less to drill on the whole, which allows operators to eke out a bit more return, “but at $50 oil, we expect on the fringe of this play that base-case wells are making single-digit returns.”

Test results in the Wolfcamp C and B look “very strong” down here, with the A zone weaker. Howard said the southern Midland would find its mojo again at $60 oil combined with a 25% reduction in costs, or $70 under the established cost environment.

“On the whole, the Midland Basin is economic today at $50 WTI, but it’s barely economic,” Howard said. The best wells, at 1 MMboe EUR, are making money at today’s well costs. “On the flip side of that average, a lot of wells are not making money.”

Upside in the basin comes at a slightly better oil price, he said. “You don’t need $90 oil, but at $70 and above, you would start to see rigs return. And if well costs drop and breakevens move to $40, you’re doing pretty good.”

West-side story

At 50-to-1 odds, a thoroughbred named Mine That Bird won the Kentucky Derby in 2009. In March 2015—and at much better odds—Cimarex Energy spudded Mine That Bird 38-1H in Culberson County, Texas. The planned 15,000-foot total depth well keeps the Cimarex tradition of naming its southern Delaware Basin Wolfcamp wells after Kentucky Derby winners. Tim Tam, Gallant Fox and Twenty Grand are other horses back in the limelight with impressive results. In fact, Cimarex’s central gas processing plant is named Triple Crown.

The theme of naming its wells after winners has paid off. Its five newest Wolfcamp D long-lateral wells with upsized fracks produced an average 2,236 boe/d at peak 30-day rate. Its first Wolfcamp A long lateral well showed a 1,491 boe/d peak 30-day IP, a 25% increase over wells with half the lateral length.

At realized $50 oil ($3 gas), the favored D zone wells generate a 73% internal rate of return.

“We’re seeing very good returns there,” said John Lambuth, Cimarex vice president of exploration. The Wolfcamp D is gassier than the A zone [26% oil vs. 50%], with a large NGL and condensate component. With the gas, “all three combined lead to a very economic well.”

Cimarex holds 100,000 net acres in the Culberson area, about half in a 50-50 joint-development agreement with Chevron Corp., which it operates, targeting the Wolfcamp shale and Bone Spring sand. Another 130,000 net acres prospective for Wolfcamp are held in Reeves and Ward counties to the east. Cimarex led the charge into this unexplored land in 2009, which it deemed “the surface of the moon,” because “there was literally no production—nothing,” Lambuth said.

With its Bone Spring drilling program in full swing, the Wolfcamp south of the New Mexico border provided a different opportunity set for the company. Unlike the Bone Spring, he said, “it’s a true unconventional shale. It’s a regional opportunity.”

The past year saw a step change for Cimarex in terms of long laterals and frack design, he said. The company has drilled 10 Wolfcamp wells in Culberson County with extended laterals, and all of its go-forward wells there will be 7,500 to 10,000 feet. “That’s our new norm.” Reeves County wells will follow suit where acreage blocks allow. On average, the company is pumping 10% more fluid and 40% more sand per stage. Stages have more than doubled, from 20 to 43.

Compare: a 5,000-foot lateral costs $7.6 million, produces 1,550 boe/d on a 30-day rate and generates an IRR of 49%. A 10,000-foot lateral costs $11.9 million, produces 2,500 boe/d and generates a 73% rate of return. “That’s a nice uplift. I’d rather pay that incremental value to drill the 10,000-foot well than pay for that $7.6 million well twice,” he said.

Lambuth noted that softening service costs of about 20% overall have already reduced well costs from $9 million and $13.5 million, respectively, for a 5,000- and 10,000-foot lateral.

Cimarex’s romance with the Bone Spring play goes back to 2008, and it is now a leader in developing this geologically varied interval. A turbodite sand, the Bone Spring requires detailed mapping to be successful, Lambuth said.

“It’s sharpshooting. We target specific sections that we go after. With each well we drill we learn a bit more, then more opportunity presents itself to us. It’s not a play in which we take all of our net acreage and divide by four to come up with the number of locations.”

In 2014, Cimarex spent $337 million to drill 81 gross wells targeting Second and Third Bone Spring in Eddy and Lea counties, New Mexico, as well as Second Bone Spring in Culberson County, Texas, and Third Bone Spring in Ward County, Texas. While he likes the results in all three areas, “we’ve had exceptional results drilling Second Bone Spring wells in our White City area in Eddy County,” he said.

Again, the company has upsized its frack recipe here, from nine to 15 stages, and has seen a 64% jump in cumulative production over 180 days.

Lambuth credits major changes in completion designs for elevating the Avalon Shale in Cimarex’s portfolio, also. “We had a nice uplift in that play, with wells now producing very good returns. Avalon wells are becoming competitive with other programs there.”

However, in spite of a 25% production growth rate last year, the downdraft in oil price has forced a change of plans for Cimarex, as well. Wholly naked of commodity hedges, it slashed its Delaware rigs by a factor of six, to three total. Two are now in Culberson County seeking Wolfcamp. The third is working in Reeves County.

“If we get encouragement on commodity and service costs bottoming out, at that point we’ll reassess, and there’s a good chance we’ll bring rigs back in,” Lambuth said. “We need more clarity on what will happen in the coming months. We’re just looking for an expectation of a certain cash flow, then we’ll be ready to make further investments.”

When Cimarex does add rigs, they will first go to the Wolfcamp play in the south, where lease expires beckon; the Bone Spring will have to wait. “That’s not motivated by the quality of the resource or economics,” he said. “We have a fantastic opportunity in Eddy County.”

Delaware economics

ITG divides the Delaware Basin into two fundamental plays: the Bone Spring/Avalon development, and the Wolfcamp Shale. The Bone Spring, with a half decade of drilling, has the most data. ITG defines the best of the Bone Spring play along a corridor that includes Lea County and the eastern portion of Eddy in New Mexico, and Loving, Winkler and Ward counties in Texas. At base well costs, Howard makes the call at $60 for breakeven.

Model in a 20% drop in vendor costs and the breakeven shifts to $50 WTI, then calculate an increase in well performance from historical results of a 500,000 EUR, “and it could push easily down to sub-$40,” said Howard. “That would put it on par with what we see in the Midland Basin.”

Operators in the southern and western Delaware Basin are chasing the Wolfcamp Shale in Culberson and northern Reeves counties. Here, the Wolfcamp is a gas condensate play, with 30% to 50% liquids at the wellhead. The mix results in high EURs—from 900,000 to 1.5 MMboe (6 to10 Bcf).

“With a 20% well-cost drop, we’re looking at a $46 base-case breakeven, and $33 for the high case. This is a very strong area,” Howard said.

Moving eastward across the southern Delaware, into southern Reeves County, the Wolfcamp GOR becomes decidedly oilier. “It’s an oil window. That play has a lot of promise and excitement around it,” Howard said.

Data here shows clear visibility in two zones, with EURs between 500,000 and 700,000 boe. Economics break even between $40 and $50, he said. “And we expect the well results from the southern Delaware to improve quite remarkably over the next 12 to 18 months.”

Devon Energy holds 285,000 net acres in Eddy and Lea counties, New Mexico, prospective for the Second Bone Spring play. "That has offered some of the highest returns and most repeatable performance we have in the company," said Tony Vaughn, executive vice president of E&P.

Devon’s shuffle

With more than half of its oil stream protected above $90 per barrel through 2015, and 40% of its gas stream just above $4 per Mcf, Devon Energy is holding its Permian rig fleet steady through the year at 14. However, where those rigs are planted is a different story. Devon is for now shutting down its southern Midland Basin drilling program and focusing its rig activity entirely in the northern Delaware Basin in New Mexico, where it has 5,000 locations to tackle.

“We’re in a dynamic business environment right now,” said Tony Vaughn, Devon executive vice president of E&P. “Commodity prices dropped materially, and the cost environment is still in flux. We’re trying to maximize returns by centering our investments on repeatable projects that offer the most capital- efficient returns. We’re high-grading to tier-one areas.”

Devon holds 285,000 net acres in Eddy and Lea counties prospective for the Bone Spring play. “That has offered some of the highest returns and most repeatable performance we have in the company,” he said. “The only area we have that is better is DeWitt County in the Eagle Ford.”

Vaughn wouldn’t divulge returns, but declared these wells saw the most robust initial production rates per dollar spent in Devon’s portfolio, “and that corresponds to some of the best ultimate recoveries and returns.”

Like other operators, Devon is fast moving to a new and upsized completion design to rock the returns. Thirteen Bone Spring wells completed in the fourth quarter modeled 1,600 pounds of sand per foot, compared with 600 pounds previously, and 16 frack stages over 13 before. Thirty-day IPs jumped 60% for an additional $700,000 spend. Now, the company is testing as much as 3,000 pounds of sand per foot in an effort to push the margins.

“We’re trying to find the top end pretty quickly,” Vaughn said. “We’ve been putting capital into these completions to find the point where we maximize present value in each of those wells to find the recipe that offers the highest returns.”

That spend involves more data captured than in the past, including conventional cores, fluid samples, bottom-hole pressure and temperature data on most wells to compress the learning curve. He noted rock properties change “fairly dramatically” in the Second Bone Spring moving from northern Eddy County to southern Lea County. “It’s not like there’s one recipe that will work.”

Pushing 3,000 pounds of sand downhole in the current commodity price environment, however, may be the limit, as incremental costs approach $3 million. “We’re probably going to have to back off. We’re probably going to find it’s too high of a cost for the incremental results.” He anticipates 1,500-2,000 pounds of sand per foot will prove most economic.

Devon is also testing pilot wells into the upper Second Bone Spring interval. Its first test showed a 30-day IP of 1,150 boe/d. Additionally, it recently drilled its first well into the Leonard Shale (aka Avalon), and the Wolfcamp, each in the northern Delaware Basin. First results out of the Leonard produced 800 boe/d over 30 days, which he deemed encouraging.

The company’s funding of its southern Midland Basin project, however, is tapped out. Once the drilling carry with joint-venture partner Sumitomo Corp. dries up in early 2015, Devon plans to wind down drilling operations and move out—for now.

“We were aggressive in the Midland Basin in 2014,” said Vaughn, “and in 2015 we are not. We invested quite a bit there and appraised a number of ideas. Some were positive, some didn’t work. We wish we had found more tier-one resource.

“In the southern Midland Basin, at $50 oil, the economics look very challenged to me.”

Although it’s dropped company-wide capex by 20%, Devon still plans to spend some $1.3 billion in the Permian Basin this year, most in the Delaware, and more than its Eagle Ford budget.

“We’re putting a lot of capital into the Permian and have high expectations for high returns,” he said. “We’re focused on the Second Bone Spring, because that offers the greatest returns. A large portion of our 2015 capital plan will stay right there in that Second Bone Spring interval.”

Long view

Contrary to popular belief, not every Permian operator has made the switch to horizontal drilling, particularly the private operators. Tim Dunn, CEO of Midland, Texas-based CrownQuest Operating and its affiliate, CrownRock LP, said heretofore the company has drilled roughly 850 vertical Wolfberry wells, and is just now completing its first horizontal.

“Our vertical results have been outstanding,” he said. “We’re very happy with them, and have not been looking for a way to get away from our vertical results.” But there is enough horizontal activity in the north end of the Midland Basin, where CrownRock has about 85,000 net acres in Midland, Martin, Howard and Glasscock counties, that the prospectivity looked too tempting to pass up. Dunn dedicated one rig to the endeavor.

“It looks like horizontal has a chance to be better than the verticals, and you can put a lot more horizontal straws into a section than vertical straws.”

With a $100-million commitment, CrownRock started as a partnership between private-equity firm Lime Rock Partners and CrownQuest Operating, in which Lime Rock holds 60% interest and CrownQuest operates. All of CrownQuest’s drilling activity presently is for CrownRock assets. The two companies have been working in tandem for eight years, and at year-end 2014, CrownRock had distributed roughly $250 million, generated earnings in excess of $1 billion, and sold $820 million in properties. “We’ve had a good run,” Dunn said.

CrownQuest Operating can sustain its Midland Basin activity because it is 77% hedged in 2015 at $88.95, and roughly 45% hedged for the three years following at around $86. "We're in pretty good shape," said Tim Dunn, CEO.

The momentum continues. In 2014, CrownRock drilled 210 wells with 12 rigs. Since, it has dropped two rigs, and is now running nine verticals and plans for one horizontal rig to target Wolfcamp A or B ongoing. It can sustain that activity because it is 77% hedged in 2015 at $88.95, and at roughly 45% for the three years following at around $86. “We’re in pretty good shape,” he said matter-of-factly. CrownRock currently produces about 20,000 boe/d.

Combined with the cash flow from the hedges, CrownRock additionally succeeded in banking $350 million in a public bond raise in January, and has no bank debt as a result. “We are not being limited by capital constraints. At this point, everything we do is based on what we perceive as the optimum economic opportunity.”

Sustaining that rig count, however, still depends on generating an expected margin (nondisclosed), and that starts with vendors. “They understand we all have to adapt, or we can’t continue on,” he said. “We’ve been working hard to reset our costs where we can continue at a material level, and if we can’t hit that target, then we’ll have to cut back further. We’ve made good progress toward our goal.”

Dunn anticipates a lower price environment “for a good while,” he said.

“I don’t think oil prices are going to come roaring back, but we’re drilling wells with a 50-year life, and as long as you have a robust margin that allows the company to be sustainable at that margin, then you’re setting yourself up for good things. We think investing when prices are low is good.”

Pondering the effect of the downturn, Dunn is less concerned about assets, and more about people. “We as an industry went through quite a substantial inefficiency bringing on new people and getting them trained, and so, are we going to have to go through that again in the future? We’re trying to prepare for several tough years. We don’t want our infrastructure and our partnership with people to fall apart, but you can’t do things that aren’t sustainable.”

CrownRock’s drilling budget of $374 million this year compares to $443 million last year.

“We’ve got plenty of available cash, but cash is a precious commodity. We’re always judicious about making a capital commitment, especially in an environment like this.

“That being said, we believe this is a great time to invest—if you can get the margins.”

Survivor

Where oil production is already seeing declines in the Eagle Ford, Bakken and Niobrara unconventional plays, the EIA in March reported a 21,000 bbl/d production increase in the Permian Basin offset all of the other decreases.

Baird analyst Ethan Bellamy, in a March report, said, “Permian growth is attributable to a 19% month-over-month increase in production per rig (vs. 2% average) as the vertical-to-horizontal rig shift takes hold. Bakken, Eagle Ford and Niobrara sequential productivity improvements were more modest at 3%, 3% and 5%, respectively.”

Even with rigs dropping like flies, Permian producers just keep getting better when pressed against the wall.

Devon’s Vaughn thinks the industry will grow stronger as a result of the slowdown. “For those companies that have a long-term view, it’s a time to retool, do some quality technical work, and to prepare for another ramp up in activity.”

“The world needs the Permian Basin, and the U.S. needs it,” Pioneer’s Sheffield said. He noted that production from the Eagle Ford and Bakken shale plays was beginning to flatten even under the higher price environment, and each might have already passed its peak. Conversely, the Permian is the last U.S. basin with a long-term growth profile, he said.

“The Permian was on its way to growing production 400,000 barrels per day per year,” he said. “In a $50 to $60 price environment, it will be flat, but at $70, it will continue to grow about half that rate, or 200,000 barrels per day per year.”

Sheffield believes the Permian has lasting power: “It will be a survivor and continue to grow.”

Recommended Reading

DXP Enterprises Buys Water Service Company Kappe Associates

2024-02-06 - DXP Enterprise’s purchase of Kappe, a water and wastewater company, adds scale to DXP’s national water management profile.

ARM Energy Sells Minority Stake in Natgas Marketer to Tokyo Gas

2024-02-06 - Tokyo Gas America Ltd. purchased a stake in the new firm, ARM Energy Trading LLC, one of the largest private physical gas marketers in North America.

California Resources Corp., Aera Energy to Combine in $2.1B Merger

2024-02-07 - The announced combination between California Resources and Aera Energy comes one year after Exxon and Shell closed the sale of Aera to a German asset manager for $4 billion.

DNO Acquires Arran Field Stake, Continuing North Sea Expansion

2024-02-06 - DNO will pay $70 million for Arran Field interests held by ONE-Dyas, and up to $5 million in contingency payments if certain operational targets are met.

Report: Devon Energy Targeting Bakken E&P Enerplus for Acquisition

2024-02-08 - The acquisition of Enerplus by Devon would more than double the company’s third-quarter 2023 Williston Basin production.