Lucid Energy brought its Red Hills II gas plant in Lea County, N.M., on stream in the second quarter, part of an expansion that will continue into 2018. Source: Lucid Energy Group LLC

It’s safe to say few rigs are looking for natural gas in the Permian Basin, but that doesn’t mean operators are not finding it anyway—and plenty of it.

The Permian is delivering more than 2.4 million barrels per day of oil (MMbbl/d) and that number will grow substantially in the next few years, according to the U.S. Energy Information Administration (EIA). However, what cannot be overlooked is that about one-third of all the flow from the basin is now associated gas, with wells becoming gassier and wetter farther west in the Delaware Basin of West Texas and southeastern New Mexico.

Already, the Permian makes about 11% of U.S. gas production, according to the EIA.

Permian production was expected to reach 8.5 billion cubic feet a day (Bcf/d) in the third quarter, the EIA reported at the end of the second quarter. Estimates by others are that it will reach 8.8 Bcf/d by year-end. Estimates vary if excluding NGL extracted from the wet gas stream.

Second to Marcellus

In any case, all observers agree that, as the Permian rig count has nearly tripled since 134 in April 2016, more gas and NGL will be coming from the region than in many years. In fact, the rate of gas production growth is second only to the pace in the Marcellus Shale, sources say.

It’s no wonder midstream companies are competing for new gas contracts and scoping out construction sites. According to one midstream source, in the second quarter a gas producer in the Delaware Basin sent a request for proposals for gathering and processing capacity and received 28 responses. Several did not have any infrastructure to fill the order yet, but planned to build to suit. Some producers are asking for an equity stake in midstream facilities in exchange for dedicating their production to a new plant—a scheme many think will become more popular as midstream firms seek project funding.

Some recent blockbuster deals in the region indicate how much its gas potential has been recognized. Delaware Basin player EagleClaw Midstream Ventures LLC was acquired by Blackstone Energy Partners LP for $2 billion. Its Reeves County, Texas, processing capacity will grow to 720 million cubic feet a day (MMcf/d) by year-end, with an additional expansion planned in 2018.

Earlier in the year, Targa Resources Corp. bought Outrigger Energy LLC for $565 million plus contingencies that could move the price higher.

“The Permian is the biggest U.S. gas-producing region that is not named Marcellus,” RBN Energy LLC analyst Housley Carr wrote in a recent blog. The Marcellus is producing about 19.4 Bcf/d today. (Total Texas output was 21.1 Bcf/d as of the first quarter, according to the EIA.)

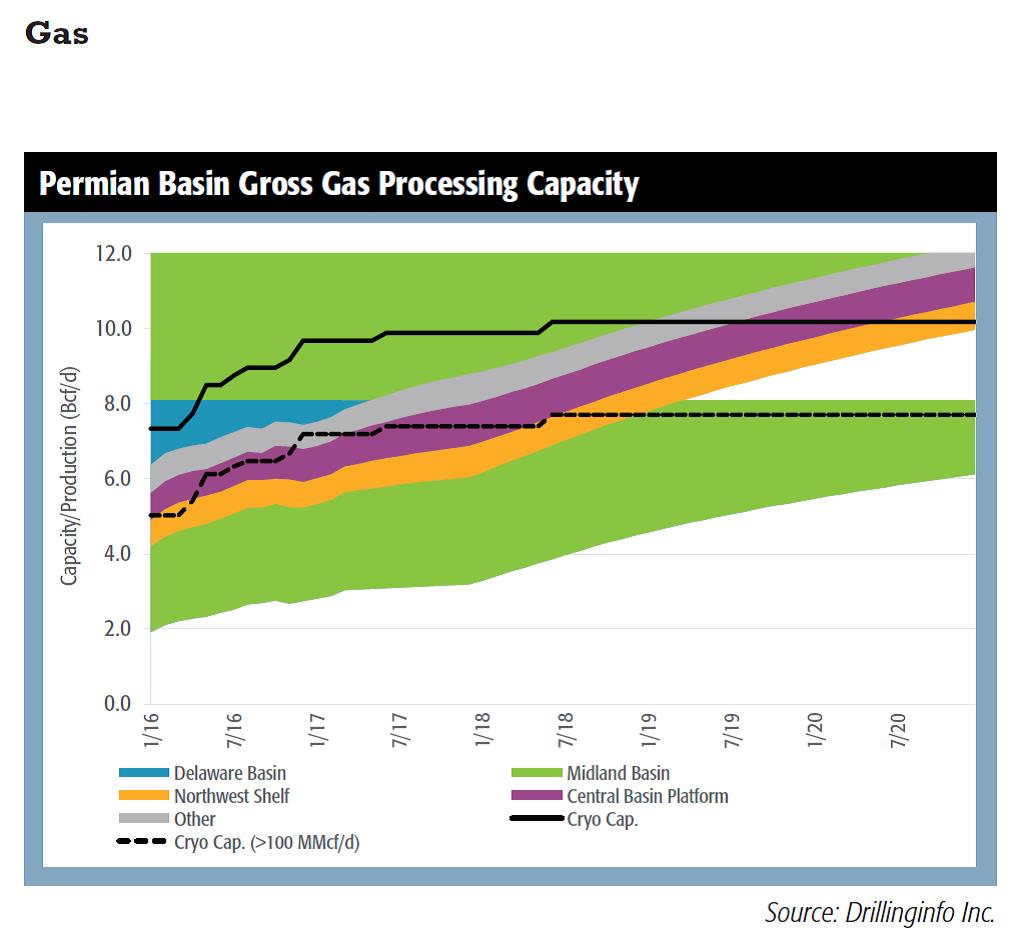

RBN analyst Sheetal Nasta blogged recently that Permian dry gas production “has climbed by 1.75 Bcf/d, or nearly 40%, in the past three years, to more than 6.3 Bcf/d in 2017 to date—and it’s poised to grow to nearly 12 Bcf/d over the next five years.” The analyst noted that these data are for dry, or residue, gas. The gross gas production including NGL is a few Bcf/d higher, Nasta said.

In comparison, total Lower 48 onshore production clocked in at 76.3 Bcf/d, according to the EIA—and the federal government has authorized export of 21.3 Bcf/d of that by LNG plants already operating, under construction, and/or proposed to handle production.

Caught by surprise

“What caught us by surprise is just how much gas the Permian is producing,” said Justin Carlson, an analyst with East Daley Capital Advisors Inc. in Centennial, Colo. Daily Marcellus production will grow by 11 Bcf from last year, he told Midstream Business, “to 35 Bcf/d by the end of 2019, but we think it could have been bigger if the Permian hadn’t shown up. We’re certainly seeing a lot of money being spent there.”

Despite the increase in gas exports that’s begun, the rise in Permian gas output foreshadows what Tudor, Pickering, Holt & Co. analysts predict will be “a brouhaha” of gas-on-gas competition among the Marcellus, Haynesville and Permian regions.

Low gas prices may not deter activity as much here as in other gas plays, however, as Permian drilling is driven by the oil price—producers’ gas is essentially a “free” byproduct.

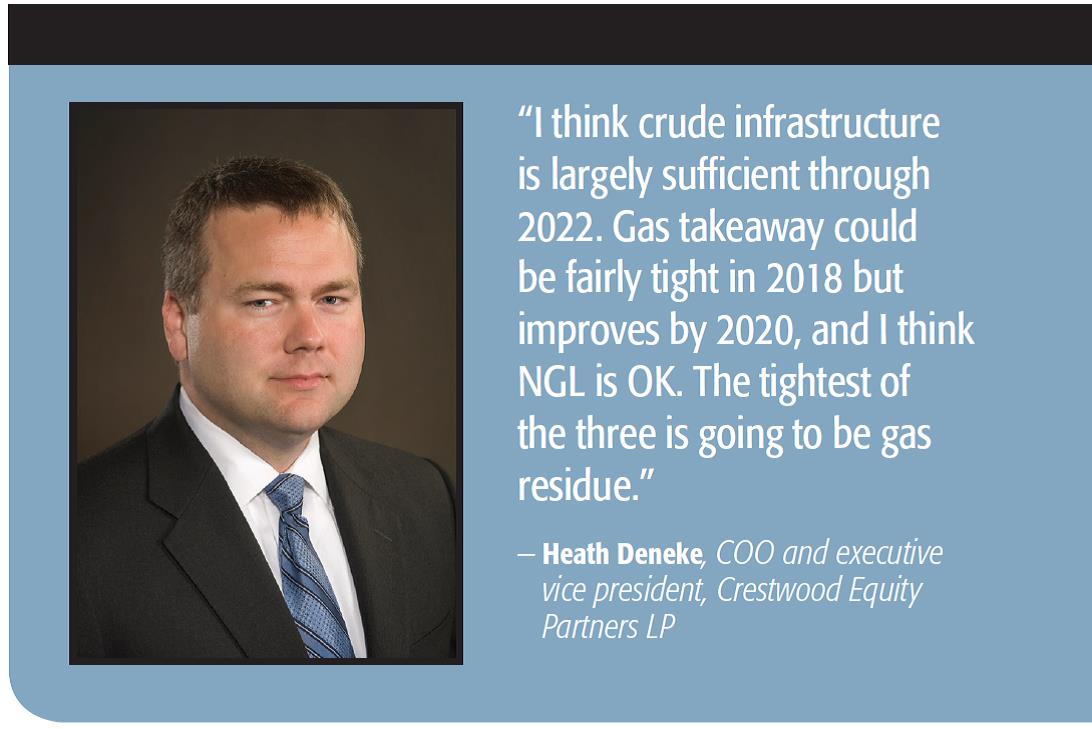

“In the Delaware, it’s really going to be the oil price, not the gas price, that drives activity,” Heath Deneke, COO and president of Crestwood Equity Partners LP’s pipeline services group, told Midstream Business. It has signed a joint venture (JV) with private-equity firm First Reserve Corp. to bulk up Crestwood’s Delaware footprint.

“The way we see it playing out, you’re going to have some volatility around gas prices with the Marcellus and Haynesville. I think there’s a wide range of outcomes, but the industry seems to be coalescing around $3/Mcf [million cubic feet].”

East Daley’s Carlson said the mighty Marcellus may cede some ground to the Permian after all, if lower gas prices cause Northeast producers to cut back their completions pace.

Back to the Permian

“The Marcellus is the top-tier gas basin, but here we are suddenly back in the 90-year-old Permian. If oil prices hold, it changes the dynamic for natural gas in the U.S.,” he said. “The Permian helps force gas prices lower in other basins. You can’t put another 3 ‘Bs’ out of the Permian and not expect something to give.”

Each midstream analyst and consultant has a different view, but all agree: The numbers are trending higher, whatever the scenario. Permian gas output could double by 2020 from current levels, they said. Although gross volumes will be less than the Marcellus by about half, Permian gas production is increasing nearly as fast on a percentage basis.

Total Permian gross gas output—wet and dry—could hit 13.7 Bcf/d in 2020 or, if accounting for NGL shrinkage, 10.3 Bcf/d, according to Bernstein Research analyst Jean Ann Salisbury’s report.

Drillinginfo Inc. is similarly bullish. “In the Permian, operators keep hitting new highs every month, reaching levels we’ve not seen before, so we keep revising our forecast, especially since this past January,” said Maria Sanchez, dry gas analyst. “It takes about three months after adding rigs to see gas production, so we’re really starting to see an increase in gas right now,” she told Midstream Business.

Sanchez said Drillinginfo estimates that, by year-end, total gas production will be about 8.8 Bcf/d, 10% more than in 2016. It could rise further to 10 Bcf/d by the end of 2018, she added. The dry gas number alone could be 6.5 Bcf/d by this December and rise to 7.6 Bcf/d by year-end 2018.

Morgan Stanley analysts placed some context around the surge in their recent report: “The Permian Basin should deliver supply growth similar to Appalachia through the balance of the decade,” they wrote.

Significantly, they increased their associated gas forecast despite lowering their oil price deck.

“By 2020, we expect [U.S.] total associated gas to grow by just over 8 Bcf/d up from about 7.5 Bcf/d previously, led by the Permian and Oklahoma Stack. This gas is roughly equivalent to all incremental planned LNG export projects and is geographically close to demand growth in the U.S. Gulf Coast.”

Their estimate incorporated an assumption of $55/bbl for West Texas Intermediate crude in 2018, down from $60/bbl previously. They warned, however, that oil prices remain a key risk to their call “as we see the two commodities as negatively correlated over the next few years.”

Waha wins and woes

Where is all this Permian gas going? Existing transportation patterns and plans for incremental capacity show it moves to all four compass points. But first, it emanates through the Waha trading hub near Fort Stockton in Pecos County, Texas, and also through the El Paso hub northeast of there.

Bernstein’s Salisbury wrote, “We believe that as of February 2017 when 5.8 Bcf/d of post-NGL gas was produced in the Permian, some 4 Bcf/d flowed eastward on the intrastate pipelines, 0.3 Bcf/d flowed to Mexico [awaiting further interconnects], 1.3 Bcf/d flowed westward [to Arizona and California] and 0.25 Bcf/d flowed northward.”

Sources estimate more than 12 Bcf/d could be flowing through Waha in the future, aiming primarily for the Texas coast and/or Mexico. But the gas surge could cause a bottleneck and poor price basis, according to RBN.

Citing Bloomberg data, RBM reported, “Spot gas prices at Waha so far this year are averaging 27 cents/MMBtu [million British thermal units] below the national benchmark at Henry Hub, compared with just 13 cents/MMBtu in the same period last year …”

The reasons it cited were mild weather, increased hydroelectric power generation in western markets and rising gas production trying to get through Waha.

Salisbury’s bullish stance on Permian oil growth drives growth in gas also, but she issued a warning: The scenario that is unfolding now is “a situation in which ‘free’ Permian gas is competing with very low-cost Marcellus gas for marginal growth.

Therefore, even though our outlook is for $3/Mcf gas for 2018 onward, there is downside risk to this price if the Permian continues to grow unconstrained.”

Inter-regional gas-on-gas competition is one challenge. The other is constraints within the Permian, especially in the Delaware Basin, that already have widened the differential between the Henry Hub and Waha prices. In addition, there has been as much as a 40cent/Mcf difference between the Waha and El Paso hubs.

RBN reported, “As Permian production growth occurs, pipeline takeaway capacity from [Waha], the primary trading hub … will become increasingly constrained, a trend that will drive pricing and flow dynamics into the early 2020s.”

There is 10.8 Bcf/d of takeaway from Waha now with more coming, it added, and 3.8 Bcf/d flows to the Gulf Coast. Another 3.1 Bcf/d could flow to Mexico—although, on the Mexican side, capacity is limited so only about half that flow is possible during the next few years. Another 2.9 Bcf/d heads west.

Mexico plans infrastructure for importing up to 9 Bcf/d vs. less than 4 Bcf/d currently, according to government authorities.

Bernstein’s Salisbury foresees differentials averaging 35 cents/Mcf in 2018 and, if all eastbound capacity is filled by year-end, possibly up to 75 cents, she wrote.

The midstream responds

Most major midstream firms are expanding throughout the Permian, especially to handle rising Delaware volumes. Last fall, a half-dozen firms added close to 1 Bcf of daily processing capacity. Since last October 2016, Energy Transfer Partners LP’s Trans-Pecos and Comanche Trail lines, along with ONEOK Inc.’s Roadrunner, began service with combined capacity of 3 Bcf/d through Waha.

Carlson said, “I believe you do need all these projects. The bigger concern for our client base is to be wary of the assets in development and the return they could get if gas prices go lower. In a nutshell, everyone can’t grow and everyone can’t win.”

Pipelines are not the main issue, however, warned Drillinginfo’s Sanchez.

“The real constraint is demand downstream of that,” she said. “Nameplate capacity is one thing, but downstream capacity [to take the gas] is another. If you look at the [differential to Nymex] at Waha, the market clearly believes that there is not yet enough demand on the existing corridors.”

Despite these concerns, many projects are moving forward. In the second quarter, Lucid Energy Group LLC started its Red Hills II processing plant in Lea County, N.M., with capacity of 310 MMcf/d, according to MidstreamBusiness.com. It may grow to 545 MMcf/d next year.

All told, Lucid has about 930 MMcf/d in operation or under construction throughout the Permian. Since it bought Agave Energy Co. in 2016, it has tripled capacity on the Agave system.

The Lucid companies, which also operate in the Midland Basin, are the largest privately held gas processor in the Permian, with 660 MMcf/d of capacity now, some under construction, and more than 3,300 miles of pipeline.

Delaware sub-basins

When considering next steps, Lucid’s President and CEO Mike Latchem told Midstream Business he breaks the Delaware into five sub-basins. All are critical to his growth plans and each has its own growth profile based on reserves and operator activity.

“We try to plan for areas where the associated gas rates per well are higher or where the oil economics are so good that we know more drilling is coming—and, with it, more gas,” he said.

At press time, Lucid was actively negotiating its next big project—this one in New Mexico. Investment decisions factor for what customers say they will need, current well results and plans for additional drilling, Latchem added.

It’s a formula being played out across the Permian Basin. Howard Midstream Energy Partners LLC recently signed a deal with WPX Energy Inc. to build a 400-MMcf/d cryogenic plant to serve WPX acreage in Lea and Eddy counties, N.M., and Reeves and Loving counties, Texas, in the Delaware. The $563-million partnership includes associated pipelines and some oil infrastructure. Funding is to be provided by international investors: Alberta Investment Management Corp. (AIMCo), which invests Alberta’s pension and endowment funds; GIC, Singapore’s sovereign wealth fund; and Alinda Capital Partners LLC, a $10 billion infrastructure investment firm.

It’s a formula being played out across the Permian Basin. Howard Midstream Energy Partners LLC recently signed a deal with WPX Energy Inc. to build a 400-MMcf/d cryogenic plant to serve WPX acreage in Lea and Eddy counties, N.M., and Reeves and Loving counties, Texas, in the Delaware. The $563-million partnership includes associated pipelines and some oil infrastructure. Funding is to be provided by international investors: Alberta Investment Management Corp. (AIMCo), which invests Alberta’s pension and endowment funds; GIC, Singapore’s sovereign wealth fund; and Alinda Capital Partners LLC, a $10 billion infrastructure investment firm.

WhiteWater Midstream LLC began building the Agua Blanca intrastate pipeline from Orla to Waha, serving portions of Culberson, Loving, Pecos, Reeves and Ward counties late in the second quarter. The 1.25 Bcf/d capacity of the 75-mile pipeline may be expanded to 1.75 Bcf/d. It is initially supported by more than 500 MMcf/d of long-term, firm-volume commitments and in-service is expected in the fourth quarter.

Meanwhile, Crestwood’s initial phase of the Nautilus gas gathering system in the Delaware began first flow. It includes 60 miles of pipeline owned by the JV with First Reserve and handles production dedicated by Shell Oil Co. across Loving, Reeves and Ward counties. “Shell is our anchor producer, but we’re open to other companies coming in,” Deneke said.

Meanwhile, Crestwood’s initial phase of the Nautilus gas gathering system in the Delaware began first flow. It includes 60 miles of pipeline owned by the JV with First Reserve and handles production dedicated by Shell Oil Co. across Loving, Reeves and Ward counties. “Shell is our anchor producer, but we’re open to other companies coming in,” Deneke said.

“Broadly speaking, the well economics in the Delaware are almost unrivaled, so the whole industry is gearing up and this system is one example of that. The Delaware is going to be a very robust basin for a long time to come,” he added.

The system will be expanded over the next two years. As a result, the JV is gearing up to build a series of facilities including a cryogenic plant at Orla with initial capacity of 100 MMcf/d. This and associated pipelines will connect Crestwood’s systems at Willow Lake in Eddy County to the north of New Mexico with the Nautilus system south, creating what Deneke called “our 100-mile super-system.”

Delaware growth

Regardless of drilling or commodity price scenarios, all outcomes point to growth for oil, gas and NGL out of the Delaware, Deneke said. “I think crude infrastructure is largely sufficient through 2022. Gas takeaway could be fairly tight in 2018 but improves by 2020, and I think NGL is OK. The tightest of the three is going to be gas residue.

“If you pick a $50-oil environment, you’d probably see up to 2 million barrels by 2020 out of the Delaware and, for gas, you’re looking at 6 or 7 Bcf/d, just out of the Delaware,” Deneke added.

Midstream executives have to cast a broad net to understand what’s happening upstream and respond in kind amid the competition. Crestwood’s Deneke said, “Permian dry gas production could be 5.7 Bcf/d in 2017 and … some forecasts go as high as 13 to 15 Bs a day in a few years.

“You really don’t have a deterministic forecast to rely on because there are so many variables involved. And think of the amount of capital needed to ramp up activity to be able to produce those growth forecasts and build enough infrastructure.

“What I do like, though, and what is unique about the Permian, is that all scenarios point to growth for oil, gas and NGL.”

Leslie Haines can be reached at lhaines@hartenergy.com or 713-260-6428.

Recommended Reading

How Diversified Already Surpassed its 2030 Emissions Goals

2024-04-12 - Through Diversified Energy’s “aggressive” voluntary leak detection and repair program, the company has already hit its 2030 emission goal and is en route to 2040 targets, the company says.

BKV CEO Chris Kalnin says ‘Forgotten’ Barnett Ripe for Refracs

2024-04-02 - The Barnett Shale is “ripe for fracs” and offers opportunities to boost natural gas production to historic levels, BKV Corp. CEO and Founder Chris Kalnin said at the DUG GAS+ Conference and Expo.