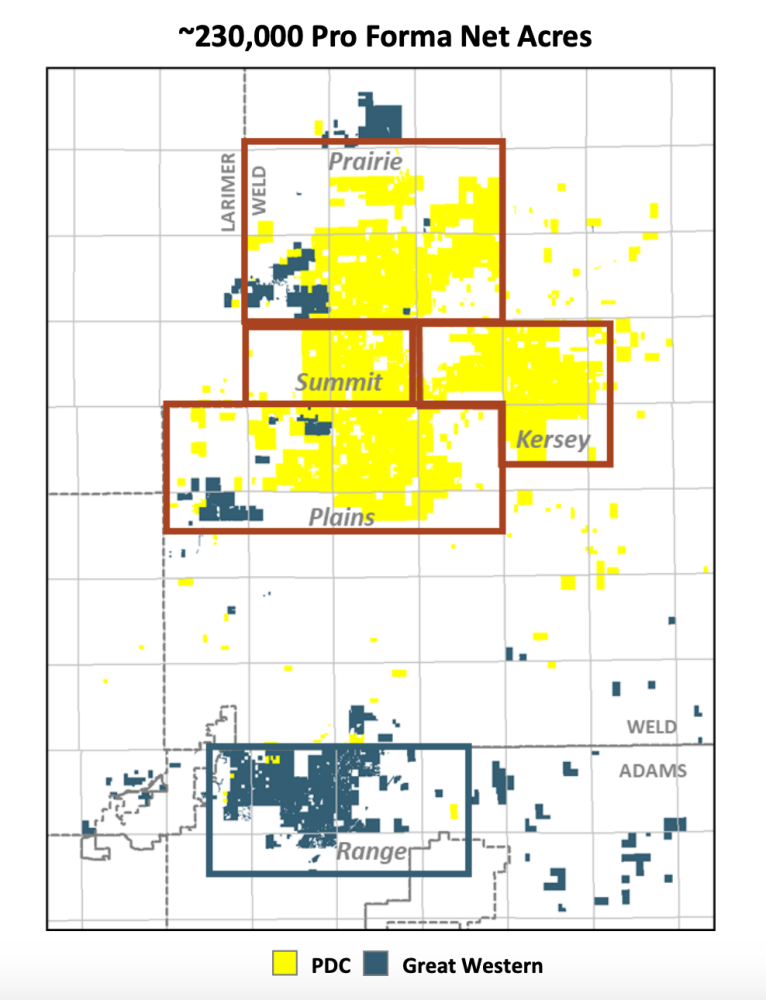

Based in Denver, Great Western Petroleum focuses in the Wattenberg with 54,000 net acres primarily in Colorado’s Adams County and about 55,000 boe/d (42% oil / 67% liquids) of PDP. (Source: Hart Energy)

PDC Energy Inc. agreed on Feb. 28 to acquire Great Western Petroleum LLC in a transaction valued at roughly $1.3 billion, including net debt of approximately $500 million, that analysts say will add much-needed inventory in the Wattenberg Field in Colorado’s Denver-Julesburg (D-J) Basin.

“Coupled with our existing high-quality inventory, this core Wattenberg acquisition adds meaningful scale to PDC while also demonstrating our commitment to—and confidence in—the future of safe and responsible energy development in the state of Colorado,” President and CEO Bart Brookman commented in a company release.

Great Western, a privately held D-J Basin operator owned by affiliates of EIG, TPG Energy Solutions LP and The Broe Group, focuses in the Wattenberg with 54,000 net acres primarily in Colorado’s Adams County and about 55,000 boe/d (42% oil / 67% liquids) of PDP. In total, Great Western has 315 operated locations, of which about 125 are DUCs/approved permits.

The acquisition of Great Western, which analysts from Tudor, Pickering, Holt & Co. (TPH) said removes M&A overhang and allows for an increase to shareholder returns, boosts PDC Energy’s D-J Basin position to roughly 230,000 net acres. PDC also holds some 25,000 net acres in the Delaware Basin in the Permian.

“On the equity, a deal was not all that surprising to us given concerns on the inventory side (and good to see the company not transact in expensive M&A) and will help remove some of the M&A overhang on the stock, but basin and county exposure (outside of Weld) is a bit surprising,” the TPH analysts wrote in a research note on Feb. 28.

The purchase price implies roughly $24,000 per boe/d flowing metric if assuming no undeveloped acreage value, the analysts also noted.

PDC Energy will fund the transaction by issuing roughly 4 million shares of common stock to Great Western shareholders valued at $227.6 million and about $543 million of cash.

The transaction, which CFO Scott Meyers said will lead to “industry-leading shareholder returns,” is expected to be financed with cash on hand and borrowings under the company’s credit facility. PDC does not expect its pro forma leverage ratio to exceed 1.0x upon closing anticipated in the second quarter.

“While our primary goal is to honor and consistently grow the base dividend, we plan to aggressively buy back a significant portion of our stock while we trade at an unwarranted discount to our intrinsic value, our peers and the broad market in general,” Meyers said in the release. “At our current share price, we not only plan to fully exhaust our new plan in under two years—but we also project to retire more shares by the end of the third quarter than we’re issuing in association with the Great Western acquisition.”

PDC Energy plans to run three rigs and 1.5 crews in the second half of 2022 on the combined D-J asset with pro-forma capex of about $900 million and $1 billion. Pro-forma production for the second half of the year is expected to be roughly 250,000 to 260,000 boe/d and 82,000 to 87,000 bbl/d of oil.

PJT Partners is exclusive financial adviser to PDC, and Davis, Graham and Stubbs LLP is PDC’s legal counsel. Citi is exclusive financial adviser to Great Western, and Latham & Watkins LLP is Great Western’s legal counsel.

Recommended Reading

Kissler: OPEC+ Likely to Buoy Crude Prices—At Least Somewhat

2024-03-18 - By keeping its voluntary production cuts, OPEC+ is sending a clear signal that oil prices need to be sustainable for both producers and consumers.

Canadian Natural Resources Boosting Production in Oil Sands

2024-03-04 - Canadian Natural Resources will increase its quarterly dividend following record production volumes in the quarter.

Uinta Basin: 50% More Oil for Twice the Proppant

2024-03-06 - The higher-intensity completions are costing an average of 35% fewer dollars spent per barrel of oil equivalent of output, Crescent Energy told investors and analysts on March 5.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

Marathon Chasing 20%+ IRRs with Los Angeles, Galveston Refinery Upgrades

2024-02-01 - Marathon Petroleum Corp. is pursuing improvements at its Los Angeles refinery and a hydrotreater project at its Galveston Bay refinery that are each boasting internal rate returns (IRRs) of 20% or more.