The future is bright for activity in the Permian Basin as development accelerates in the region. (Source: Shell)

The 2019 outlook for shale remains dynamic on many levels. Operators and oilfield service companies continue to push the limits of technology and business processes, enhancing their chances of meeting investor expectations and extending the miracle of shale both geographically and temporally. During the past 12 months, companies broadened the application of longer laterals and high-intensity fractures, unlocking additional potential in places like the Permian, Powder River and Anadarko basins. However, companies did not stop with changes in the field. Instead, companies increasingly cast attention on their business processes, looking for opportunities to drive out costs. The combination of these collective efforts is a key driver behind changes in the 2019 forecast.

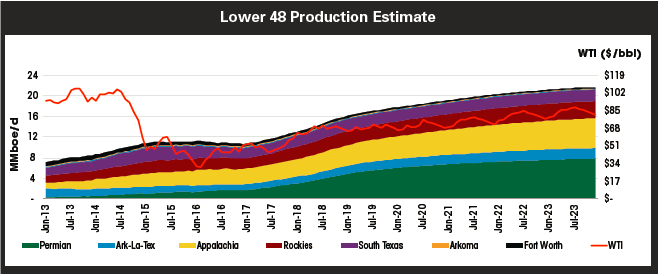

Shale and tight resource production is estimated to average 20.5 MMboe/d in 2019, an increase of 2.9 MMboe/d versus 2018 estimates. At the resource level, the Permian Basin remains king. Current 2019 estimates for the Wolfcamp, Bone Spring and related reservoirs have production averaging 5.9 MMboe/d. Breaking this down, the Delaware sub-basin Wolfcamp contributes 50%, the Midland sub-basin Wolfcamp contributes 32% and the Bone Spring contributes 18%. The Alpine High is commingled with the Delaware sub-basin Wolfcamp. This may change in the next year given the ramping activity and Apache’s commitment to the play. In the Midland sub-basin, the Wolfcamp reigns supreme with 1.9 MMboe/d of production. Outside the Permian, expect the Anadarko and Powder River basins to notch growth of 0.22 MMboe/d and 0.04 MMboe/d, respectively. Elsewhere, look for the Appalachia plays to post gains of 0.57 MMboe/d (3.4 Bcf/d), driven in part from increased flows to the west and northwest and to the south. In summary, the plays with the greatest December 2019 versus December 2018 year-on-year growth are the Delaware-Wolfcamp at 0.76 MMboe/d (35%), the Scoop at 0.11 MMboe/d (32%) and the Stack at 0.13 MMboe/d (29%).

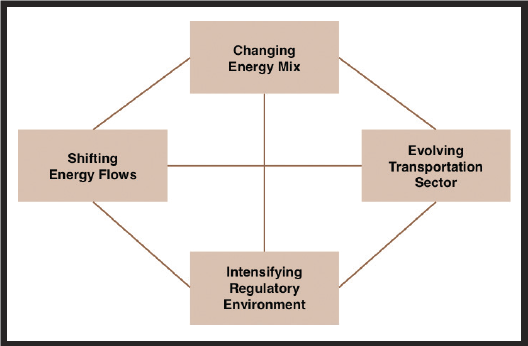

Four themes shaped Stratas Advisors’ views on U.S. production in 2018: a changing energy mix, shifting energy flows, an intensifying regulatory environment and an evolving transportation sector. These themes weigh on the company’s views individually and collectively in varying degrees depending on the time horizon and the level of intensity anticipated from each theme.

At this juncture, a review of the Stratas themes and the role of each in the forecast will clarify the 2019 outlook.

Changing energy mix

The subject of a changing energy mix is multifaceted. Beginning with the obvious, liquids production from shale and tight resources is light and very light (field condensate).

At Stratas, production streams by grade and country of origin are tracked. In recent years, increases in unconventional resource production have been met by reductions in other areas like Venezuela. Using Venezuela as a case study, it is quickly seen that there are two dimensions presented by this change—the first is geographical and the second is crude quality. While the shift from South America to North America is not that great of a deal, the shift from heavy sour crude to light sweet and ultralight grades can be much more impactful. Sophisticated refineries, such as those in the U.S., are specifically designed to handle heavier crudes. This is not to say they are unable to handle light feedstock, just that the economics can vary. Suffice it to say that changes in mix introduce complexity to an already complex system.

Shifting energy flows

Staying with the Venezuela case study, it is easy to see that crude shipments are shifting about as a result of the shifting energy mix. However, this is but the tip of the iceberg with respect to energy flows. To put things in perspective, the U.S. is a top global producer. More to the point, production increases in shale have been outstripping changes in domestic demand, leading to increased exports and decreased imports from OPEC members and others. Looking to the horizon, it seems reasonable to project rising exports in the coming years. Projects connecting the Permian Basin and other productive areas to export terminals will serve to support longer-term development across North America. This is not novel but worth repeating nonetheless: Good long-term visibility is a critical success factor for all segments of the value chain. Long-term visibility in upstream hinges on having sound understandings of the resource geology, effective engineering and comparative economics.

Intensifying regulatory environment

Try as it might, the industry’s ability to foretell the future is far from perfect. That reality allows the introduction of the third theme—an intensifying regulatory environment. Some are likely to challenge the notion of intensifying regulations. After all, regulations appear to be loosening at the U.S. Environmental Protection Agency, and the current administration appears friendly to the industry.

However, battle lines have been redrawn. Industry opponents have retrenched back to state and local jurisdictions. Colorado’s Proposition 112, defeated in the November midterms, was a proposal that could have severely impacted oil and gas activities across the state. In the most austere interpretation of Prop 112, every square mile of Colorado could have been subjected to scrutiny. Regardless of the proposition’s outcome, companies in Colorado are feeling regulatory intensity.

Elsewhere, the ongoing sagas of the Dune Sagebrush Lizard in the Permian Basin and the sage grouse continue. In the case of the lizards, one study after another continues to hamper some efforts. Add to that the policies and restrictions arising from climate change and the swirling efforts by groups in California, the Pacific Northwest and elsewhere, and a case can be made for a tightening regulatory environment.

Evolving transportation sector

Stratas’ last theme, an evolving transportation sector, speaks to both the near and long term. In the near term, industrial transportation is transitioning in real time. Changes to emissions on the open seas are leading mariners to consider early retirements of vessels versus installation of scrubbers. With new vessels, options for propulsion now include low-sulfur diesel, LNG and more. In passenger cars, marketing of electric vehicles appears on the rise. Clearly, more options will be introduced down the road.

Looking ahead

With this canvas, consider the road ahead for operators, service companies and investors in shale. In short, 2019 will resemble 2018 in that growth and financial discipline chatter will be common themes around shale water coolers, and risk and uncertainty will dominate international affairs. Familiar trends will continue to resonate in the new year as Shale 2.0 becomes another year older.

It is with this backdrop that modestly higher average prices are expected to support slightly higher spending in 2019. West Texas Intermediate (WTI) prices are expected to average $68.71/bbl in 2019, up from $67.03/bbl in 2018. Meanwhile, natural gas is expected to average $3.30/Mcf, up from just over $3. These prices lend support to a double- digit increase in capital spending versus 2018.

Spending levels throughout the year are projected to remain relatively stable with about half going to the Permian Basin. Most Permian spending will land in the Wolfcamp formations, with slightly more of the Wolfcamp spending finding a home in the Delaware sub-basin. More generally, unconventional resources will gobble up more than 90% of total 2019 spending. Even though 2019 spending is projected higher compared to 2018, rising net cash generation and persistent financial discipline will sustain improving financial metrics for the industry.

Despite higher overall spending and increased efforts to convert drilled but uncompleted wells to producer status, the ROP growth is expected to slow in 2019. Several factors will contribute to the slowing growth rate. First, a number of critical bottlenecks, including infrastructure constraints, have stymied upstream progress in recent years. While a number of infrastructure projects are on schedule to alleviate some bottlenecks, other factors, including acute labor shortages, will continue to aggravate upstream efforts in 2019.

Regardless of the obstacle, shalers have proven their mettle, delivering both economic results and production growth. While 2019 promises to deliver more growth, companies are no longer content with growth for growth’s sake. Instead, whether by choice or circumstance, companies increasingly are changing to meet today and tomorrow’s energy needs.

Production estimates

The year-on-year production for December 2019 is estimated at 0.7 MMbbl/d, down from an estimated 1.4 MMbbl/d in 2018. The all-important shale oil segment is projected to finish 2019 at about 8.2 MMbbl/d, an increase of about 1 MMbbl/d over December 2018. Permian shales are poised for growth of about 0.9 MMbbl/d of growth and represent a little more than half of total shale production in the U.S. In other shales, the Midcontinent and Rockies also are expected to add to growth.

Moving on to Lower 48 natural gas, increases in shale gas will be partly offset by declining conventional volumes. Wellhead volumes from shale resources are expected to rise by about 8 Bcf/d versus December 2018. During this same period, conventional production will likely contract by about 2 Bcf/d, leading to net growth of approximately 6 Bcf/d. Compared to 2018, this represents about a 50% reduction in modeled growth.

In spite of multiple challenges in recent years, oil and gas companies have persevered, remaining competitive when some counted them out. Persistently low prices forced shalers to create new models and solutions. Backward integration, once the provenance of large integrated companies, is now found across independents. Operators scoped out costs, identified opportunities for reductions and delivered savings.

Many insiders and observers alike refer to modern well designs as Shale 2.0. However, a detailed review of wells across major shales reveals that progress has been more evolutionary than revolutionary. Lateral lengths increased progressively over many years. Just how did the transition take shape? From the beginning of the shale era back in the mid-2000s when lateral lengths averaged a little more than 2,000 ft, companies pushed the limits of technology by extending the path by another 500 ft or so. Every few years, those early efforts paid off and a new standard was ushered in. Today, companies are largely looking to drill 1.5-mile to 2-mile horizontal section lengths, or 7,500 ft to 10,000 ft. While longer laterals have been drilled, the optimal length on modern completion designs fall in this range.

Much has been written on reduced cluster spacing, shorter stage intervals and increased stage counts. Suffice it to say that progression in completions also has been evolutionary in nature. Companies try new approaches, make adjustments, try and try again until they find something that works. This is a core part of the DNA of shale companies—master scientists with proven track records, backed by investors willing to take risks. The net result is a shale industry ready, able and willing to compete on the world stage.

Read each of the December E&P "2019 Unconventional Yearbook" articles:

Key Players: Maintaining the Stride, Staying Ahead

Drilling Becomes Standardized While Completions Get Customized

Transformation Continues for Delaware Basin Operator

Sand, Water Logistics Shift into High Gear

Oil, Gas Industry Discovers Innovative Solutions To Environmental Concerns

Recommended Reading

Ohio Utica’s Ascent Resources Credit Rep Rises on Production, Cash Flow

2024-04-23 - Ascent Resources received a positive outlook from Fitch Ratings as the company has grown into Ohio’s No. 1 gas and No. 2 Utica oil producer, according to state data.

E&P Highlights: April 22, 2024

2024-04-22 - Here’s a roundup of the latest E&P headlines, including a standardization MoU and new contract awards.

US EPA Expected to Drop Hydrogen from Power Plant Rule, Sources Say

2024-04-22 - The move reflects skepticism within the U.S. government that the technology will develop quickly enough to become a significant tool to decarbonize the electricity industry.

For Sale? Trans Mountain Pipeline Tentatively on the Market

2024-04-22 - Politics and tariffs may delay ownership transfer of the Trans Mountain Pipeline, which the Canadian government spent CA$34 billion to build.

TotalEnergies to Acquire Remaining 50% of SapuraOMV

2024-04-22 - TotalEnergies is acquiring the remaining 50% interest of upstream gas operator SapuraOMV, bringing the French company's tab to more than $1.4 billion.