Oil and Gas Investor asked analysts from Tudor, Pickering, Holt & Co., RBC Capital Markets and Baird for their top picks in the SMID-cap sector. (Source: Hart Energy)

[Editor's note: A version of this story appears in the July 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The positive sentiment that spilled over into energy in the wake of the first takeover in many months—the purchase of Anadarko Petroleum Corp. by, in the end, Occidental Petroleum Corp.—lasted but a little while. The warm glow of “who’s next?” discussions heightened hopes among investors. But, within weeks, a further buying opportunity arose as crude collapsed in its worst sell-off since late last year.

As usual, small- and mid-cap (SMID) E&P stocks were most vulnerable. Remarkably, a handful of smaller E&P stocks set new 52-week lows, even though the West Texas Intermediate (WTI) price, at $57.91 per barrel (bbl) on May 23, 2019, was still roughly 35% above the low in crude prices last Christmas Eve at $42.53/bbl.

Oil and Gas Investor asked analysts for their top picks in the SMID-cap sector. Coming ahead of the recent sell-off in the group, sparked by global trade concerns and other factors (see “On the Money: Confusion Or Complacency?”), the recommendations may now offer still better bargains given what are in some cases more attractive entry points for investors.

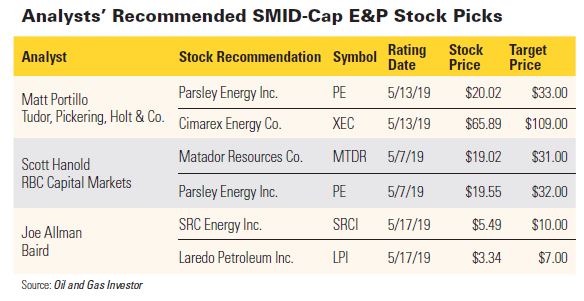

Matt Portillo, managing director of E&P research at Tudor, Pickering, Holt & Co. (TPH), favors the fundamentals of Parsley Energy Inc. and Cimarex Energy Co. In addition, given expectations of M&A activity re-emerging, Portillo views the E&Ps “as the two most likely consolidation candidates if the integrateds are looking for more bite-sized acquisitions in the mid-cap sector.”

As background, “we think M&A is going to be a huge component of the 2019 and 2020 discussions when it comes to the upstream sector,” said Portillo. One part of M&A is expected to involve the majors—Exxon Mobil Corp., Royal Dutch Shell Plc and BP Plc—who are likely to be “acquisitive over the next three or four years” as they look to add quality or depth of shale inventory. Potential targets identified by Portillo are Concho Resources Inc. and Pioneer Natural Resources Co.

Mergers Of Equals

The other part of M&A is expected to be “mergers of equals, with low premium bids, in the mid-cap universe,” said Portillo. This is likely to be driven by smaller E&Ps’ need for scale in order to remain competitive with the large-cap producers. In addition, as E&Ps have undertaken a shift in their business models to more moderate growth, “cost synergies from general and administrative [G&A]) cuts coming from mergers will be a big driver,” according to Portillo.

“We think you’re going to see more strategic deals going forward in the Permian that will likely block up larger acreage packages and allow for lower cost of development and more scale on the asset front,” he said. As potential partners in “mergers of equals,” he offered up Callon Petroleum Co., Carrizo Oil & Gas Inc., PDC Energy Inc. and SM Energy Co.

Focusing largely on fundamentals, “our favorite name in the mid-cap sector is Parsley,” said Portillo. Positive factors include potential upside to 2019 production estimates; advantageous acreage affording low development costs vs. smaller peers; and Matt Gallaher taking the helm as CEO and steering Parsley to “moderation of growth and acceleration of free cash flow.”

to see more

strategic deals

going forward

in the Permian

that will likely

block up larger

acreage packages

and allow for

lower cost of

development and

more scale on

the asset front,”

said Matt Portillo,

managing director,

E&P research, at

Tudor, Pickering,

Holt & Co.

In addition, Portillo termed “constructive” Parsley’s initiatives to improve rates of return on its wells by changing the spacing design in its development program, or “up-spacing.”

Capital Efficiency

“In a world where you’re trying to maximize capital efficiency, you’re less focused on net present value per section, and more focused on the incremental rate of return per well,” noted Portillo. “Parsley has taken proactive steps to up-space their well design to improve well productivity. Not every E&P can do that, because not every E&P has the acreage and the scale to give up inventory to drive improvements in their rates of return. We think PE is in a good position from that perspective.”

As for G&A, Portillo noted Parsley had “pro-actively taken steps in the right direction” and trimmed its labor force by 8%. “With the industry no longer chasing growth for growth’s sake, a lot of operators have changed their long-term trajectory and capital allocation plans,” he continued. “We think it is a very good sign that Parsley has already made the change and is improving its cost structure and margins.”

On valuation, said Portillo, Parsley screens attractively on 2020 estimates. The stock trades at only about 4 times enterprise value-to-EBITDA (EV-to-EBITDA) and 8 times price-to-earnings ratio (P/E). Its balance sheet is in “very good shape,” with net debt-to-EBITDA moving to below 1 turn. Its free-cash-flow (FCF) yield is approaching 5%, and return on capital employed (ROCE) will be in the “low teens” next year.

One upside catalyst also discussed by Parsley is the potential monetization of its mineral ownership. “I don’t think the market is giving them credit for that right now,” said Portillo. “We think that’s worth roughly $750 million.” Similarly, a strategic process is being run to evaluate Parsley’s water infrastructure assets, for which TPH assigns a price tag of around $400- to $500 million.

The TPH price target for Parsley is $33 per share, offering potential upside of almost 65% from its $20.02 per share close on the May 13 interview. “We view Parsley as one of the most likely takeout targets in the next three or four years,” affirmed Portillo. “We think that’s a fair level in an M&A scenario.”

Cimarex, also recommended by Portillo, has plenty of factors in its favor: an attractive valuation; a play on a potentially strengthening basis in Midland crude oil prices; and, as with Parsley, the potential that the company may be a takeout target. At $65.89 per share on May 13, the stock has some 65% upside potential to the TPH target price of $109 per share.

On projected metrics for 2020, Cimarex is trading at only about a 4 times multiple of EV/EBITDA and 8 times P/E multiple. The company offers a 6% FCF yield and is expected to generate a 15% ROCE. Its leverage, after its acquisition of Resolute Energy Corp., is estimated at a modest 0.7 times net debt/EBITDA.

Cimarex’s production is weighted somewhat more than its peers to natural gas, at 41% of output, with oil at 31% and NGLs at 28%. However, Portillo sees the oil component rising to close to 38% in a few years and, importantly, Cimarex benefiting from much improved Midland differentials.

Improving Midland Basis

“We’re constructive on Midland basis improving over the next year as new pipeline capacity starts up, and Cimarex offers a leveraged way to play that because it hasn’t committed to long-haul capacity for crude out of the basin,” said Portillo. “So as Midland prices improve—and we think Midland will trade at a premium to WTI at Cushing by the first half of 2020—Cimarex will be a big beneficiary of that.”

In addition, “we think NGL prices, broadly speaking over the next 18 months, are poised to improve in the U.S. due to dock capacity expansions,” he continued. “We see about 600,000 bbl/d of LPG export capacity coming on, which will ultimately improve propane price realizations and, in turn, give upside leverage to NGL realizations. And Cimarex produces a lot of NGL,” he noted.

As for attracting suitors, “we think Cimarex could be an interesting acquisition target over the medium term for the likes of Chevron Corp. or BP, given the scale and quality of its acreage in the Permian,” said Portillo. For example, “CVX already has a large, high-quality acreage footprint in the Permian, so it’s more about the ability to drive accretion through acquisitions of smaller producers. We think XEC fills that bill for them.”

Scott Hanold, analyst at RBC Capital Markets, pointed to three E&Ps stocks he sees likely to outperform: Matador Resources Co., Parsley Energy and WPX Energy Inc. Price targets for the stocks are $31, $32 and $17 per share, respectively, representing potential upside from a May 7 closing price of over 60% for Matador and Parsley, and 35% for WPX.

Commenting on recent sector volatility, Hanold said investor support for the group depended primarily on re-establishing “some stability in the commodity price.” Obviously, the fourth-quarter dive in WTI last year from roughly $75/bbl to $45/bb was unnerving, he said, but investors don’t need to see prices climb back to $70/bbl. If steady within a range, for example, $55 to $60/bbl “would work.”

to see SMID-caps

join together

in “mergers of

equals that are

done at small

premiums,”

according to Scott

Hanold, analyst

at RBC Capital

Markets.

Investors want to see SMID-caps join together in “mergers of equals that are done at small premiums,” said Hanold, so that they can counter the key headwinds they typically face. These include innately lower economies of scale; the steeper decline rates that usually come with a smaller production base; and “a little heavier level of G&A and interest costs” per barrel.

Attracting Buyers

In investors’ eyes, greater size is also critical in terms of attracting buyers, according to Hanold, as the market largely thinks SMID-caps are unlikely to get bought “because they don’t provide enough scale. For an Occidental Petroleum or Chevron, for example, they don’t move the needle. They’re not going to buy a SMID-cap name; they’ve got to buy something with scale.”

For existing SMID-caps to gain traction in the interim, said Hanold, they must be able to demonstrate they have good acreage, a business model that works, a clean balance sheet and visibility that they can bridge the gap to FCF, or at least show the ability to “manage the outspend in a reasonable timeframe.”

Plans outlined by Matador address the latter question. The company is outspending cash flow in 2019, but there is “ample capacity on the revolver to fund the anticipated outspend of $175-to $200 million,” based on RBC’s $64/bbl price deck for WTI this year, according to Hanold. In addition, plans to mitigate the outspend are in place, and results are materializing faster than first expected.

What’s unusual about Matador is that it has a differentiated business model, one in which it’s effectively “building a large midstream company at the same time that it’s building an organic E&P company in the northern Delaware,” explained Hanold. “Management views the midstream as a strategic asset to support its upstream growth at a low cost relative to other third party options,” he said.

Managing the level of outspend is a top priority for the Matador management team. Initiatives taken to date include reducing the rig count to six, divesting noncore assets in prior legacy operating areas in the Eagle Ford and Haynesville, and improving efficiencies and/or reducing service cost in its operations. Indications are that reaching FCF neutral levels may be possible in a couple of years.

Matador brought a joint-venture (JV) partner into its midstream company, San Mateo, through a 49% sale of the asset to private-equity sponsor Five Points Capital. The JV partner helps share in the ongoing capital costs of the infrastructure buildout, which also brings in business from third-party customers. The infrastructure has four-stream pipes for oil, natural gas, NGL and water.

Interestingly, the Matador management team has one of the highest insider ownership positions, at over 5%, among SMID-cap companies. It is the same team that, over a period of years, put together from scratch—“brick by brick”—what is now a 130,000-net-acre position in the Delaware, according to Hanold. “They’re heavily invested in the play,” he said. “They believe in it.”

As for Parsley, now that it has transitioned from being a “high-growth outspender” to being a “mid-to-high-teens growth, FCF generator,” there’s a lot to like, according to Hanold.

“At recent commodity prices, I expect Parsley to be FCF positive by the third quarter of this year, which for a SMID-cap growing at a 15%-plus clip is pretty attractive to me. You don’t see that from a lot of E&Ps,” he commented. “And in 2020, I expect over $200 million of FCF and 16% organic production growth based on a $66/bbl WTI forecast.”

Moreover, Parsley has made clear, noted Hanold, that the company will adhere to its $1.35- to $1.55 billion capex budget for 2019, based on a low-$50/bbl price deck, even if crude goes measurably higher. “Once they cross that FCF neutral line, the plan is not to cross back,” he emphasized. “Their view is that once they pivot to FCF neutrality, they’re going to do whatever they need to do to maintain that position.”

Also, with CEO Matt Gallagher bringing a more operational focus, the company has clearly made a “pivot toward much more of a long-term development plan with its very ample resource base,” noted Hanold. This has involved more blocking and tackling, acreage swaps and trades, etc. “Moving to development is the right thing to do. Investors aren’t paying for decades of inventory.”

Hanold credits the management team at WPX for its strategic success and for making “the right moves.”

‘The Right Moves’

“They’ve made all the right decisions,” he said. “They’ve pared off noncore assets and focused on their best assets. They made a good acquisition in the Delaware Basin where most of the good results have occurred. They’ve done a great job of lining up infrastructure ahead of time so they’re not constrained or suffering big discounts on price realizations. They’ve made the right moves.”

Hanold described WPX as being highly disciplined and committed to a $1.1- to $1.3 billion capex budget, including nonop and midstream opportunities, for 2019. At current strip pricing, this would allow WPX to target $100 million in FCF. In terms of improving efficiency in the Permian, WPX saw a 27% reduction in drilling times in the first quarter of 2019 vs. the 2018 average, he noted.

The $17-per-share target price for WPX is based on a 10% discount to net asset value calculated for WPX at $60/bbl WTI and Henry Hubb at $2.75 per thousand cubic feet. The discount is somewhat narrower than the average of the E&P coverage in light of WPX’s strong Delaware position and the RBC view of WPX as a “top-tier operator.”

Hanold summed up WPX and its management: “Great rocks, great planning and great infrastructure.”

Joe Allman, CFA, Baird’s senior research analyst in New York, offered outperform ratings on two E&P stocks whose target prices, if realized, represent near doubles from recent levels. Denver-based SRC Energy Inc. was designated a “fresh pick” as Baird raised its target by $1 to $10 per share, while Laredo Petroleum Inc. was upgraded from neutral to outperform with a $7-per-share target.

Regarding SRC’s activity in the D-J Basin, the passage of Senate Bill 181 means the Colorado regulatory environment is “much better than it has been for the last five years,” said Allman, as it has “taken the teeth out of any further potential ballot initiative that could create sweeping changes to the industry. An industry that was facing an existential threat less than a year ago has a much brighter outlook today.”

Expansion of the D-J Basin’s gas processing capacity is also expected to help brighten the outlook for SRC, which has had 20,000 barrels of oil equivalent per day (boe/d) of net production shut in, according to Allman, citing the company’s 10-Q filing with the SEC for the first quarter. New capacity due to come on in 2019 includes the DCP Midstream O’Connor 2 plant and the Latham I and II plants of Western Midstream Partners.

181 means

the Colorado

regulatory

environment

“is much better

than it has been

for the last five

years,” said Joe

Allman, senior

research analyst

at Baird. The bill

“has taken the

teeth out of any

further potential

ballot initiative

that could create

sweeping changes

to the industry.”

Relieving The Bottleneck

Relieving the bottleneck will be the 300 MMcf/d DCP Midstream O’Connor 2 plant and bypass, due to come online in June, which will add approximately 45 MMcf/d of new gas production capacity for SRC. This should roughly match the gas component of the current shut-in volumes, assuming a production mix for SRC of 40% natural gas (48 MMcf/d), 40% oil (8,000 bbl/d) and 20% NGL (4,000 bbl/d). (Note: The liquids-rich natural gas has to flow and be processed at the O’Connor 2 plant in order to recover the NGL component.)

The O’Connor 2 plant addition “alone will provide the capacity to handle essentially all of SRC’s shut-in production,” said Allman. “This plant is scheduled to start up in June, and the plant and the related bypass will ramp up over the succeeding months.” Beyond the O’Connor 2 plant’s 300 MMcf/d new capacity will also come from the two Latham plants’ 200 MMcf/d apiece in the latter part of 2019.

In the 2020 to 2022 period, a further 1 Bcf/d of capacity from DCP’s Bighorn plant is scheduled to come onstream in three stages, with the first stage adding 200 to 300 MMcf/d in mid-2020.

“We think SRC’s bottlenecks will be significantly reduced, if not gone, by the end of 2019 and completely gone during 2020,” said Allman.

As for Laredo, the jump in the Baird target price—to $7 from $3 per share earlier—follows the company’s change of course as regards well spacing. Whereas previously Laredo focused on more densely drilled well patterns to maximize net asset value [NAV] per spacing unit, its new course is to drill more widely spaced wells that “likely will result in greater productivity per average well,” according to Allman.

Besides drilling wider-spaced wells, Laredo has reduced G&A, and one of its largest shareholders, SailingStone Capital Partners, has called for further G&A reductions and, among others, an evaluation of strategic alternatives, he noted. In addition, a new key executive, Jason Piggot, has come in as president and will transition to CEO in the fourth quarter. “It’s a company in transition,” said Allman.

Just over a year ago, in its first-quarter 2018 conference call, Laredo announced plans to drill 32 wells per section in an Upper Wolfcamp/Lower Wolfcamp drilling spacing unit, Allman recalled. After oil decline rates proved steeper than anticipated, plans have now been revised to four to eight wells in each of the two target zones in expectation of improved productivity per well.

Even with productivity impaired last year due to tightly spaced wells, proved developed finding and development (F&D) costs came in at $12.57/bbl, noted Allman, and better levels of F&D are anticipated for the coming year. For example, well costs have declined by $500,000 to $7 million for a 10,000-foot-lateral well, helped by 25% lower costs for in-basin sand and completion services.

Even with Laredo management running counter to industry trends—and raising its drilling and completion budget to $400 million from an earlier $300 million—management has predicted it will be FCF neutral in 2019 and in 2020. Allman views these estimates as conservative, with projections of over $40 million of FCF in both 2019 and 2020.

His $7 per-share target for Laredo is based on a discounted cash flow-based NAV.

“The turnaround is already underway,” said Allman.

Chris Sheehan can be reached at csheehan@hartenergy.com.

Recommended Reading

Imperial Expects TMX to Tighten Differentials, Raise Heavy Crude Prices

2024-02-06 - Imperial Oil expects the completion of the Trans Mountain Pipeline expansion to tighten WCS and WTI light and heavy oil differentials and boost its access to more lucrative markets in 2024.

US Gulf Coast Heavy Crude Oil Prices Firm as Supplies Tighten

2024-04-10 - Pushing up heavy crude prices are falling oil exports from Mexico, the potential for resumption of sanctions on Venezuelan crude, the imminent startup of a Canadian pipeline and continued output cuts by OPEC+.

Oil Broadly Steady After Surprise US Crude Stock Drop

2024-03-21 - Stockpiles unexpectedly declined by 2 MMbbl to 445 MMbbl in the week ended March 15, as exports rose and refiners continued to increase activity.

Exxon’s Payara Hits 220,000 bbl/d Ceiling in Just Three Months

2024-02-05 - ExxonMobil Corp.’s third development offshore Guyana in the Stabroek Block — the Payara project— reached its nameplate production capacity of 220,000 bbl/d in January 2024, less than three months after commencing production and ahead of schedule.

Russia Orders Companies to Cut Oil Output to Meet OPEC+ Target

2024-03-25 - Russia plans to gradually ease the export cuts and focus on only reducing output.