The recently announced transactions between Bonanza Creek Energy, HighPoint Resources, Extraction Oil & Gas and now Crestone Peak suggest that the sort of regional consolidation previously predicted may be gaining steam. (Source: Hart Energy)

This is an excerpt from the Ralph E. Davis Associates (RED) Weekly E&P Update Newsletter.

The drop in oil prices that began in 2019 (and was greatly amplified by the COVID-19 pandemic) led to a paradigm shift in the U.S. upstream oil and gas business. After several years where companies focused on either “lease and flip” and “growth at any cost” strategies, investors began to demand more disciplined capital deployment, a reduction in debt-fueled growth, and an ability to generate free cash flow.

In a world where most upstream companies, especially private ones, followed a single-basin (“pure-play”) model and many of the plays’ drilling economics were challenged by low commodity prices, a natural and expected reaction was a consolidation of companies to gain economies of scale, reduce overhead costs, and high-grade their drilling investments. Despite the apparent logic, however, there were relatively few consolidations other than a few large deals in 2020. Consolidations of small to midsized regional players seemed to make a lot of sense, but as we’ve noted before, some of those deals, particularly among privately-held companies, are hindered by governance issues; that is, how will the relative value contribution of each company be determined, and who will control the board and constitute the management team?

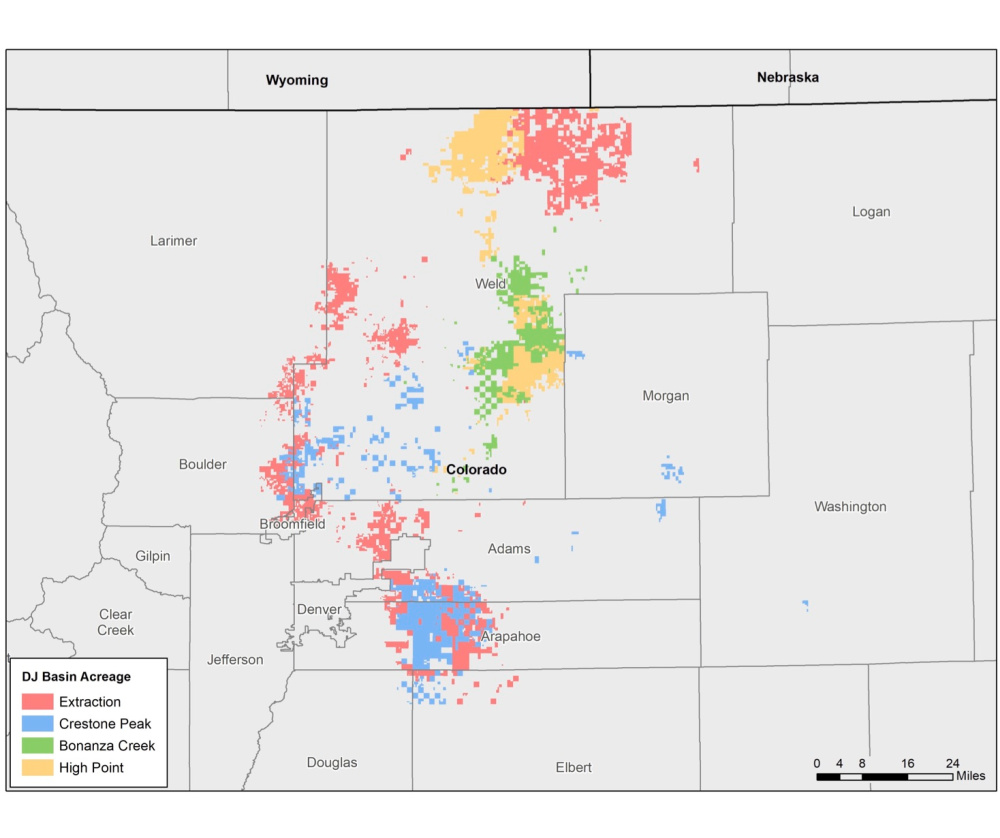

The recently announced transactions between Bonanza Creek Energy, HighPoint Resources, Extraction Oil & Gas and now Crestone Peak suggest that the sort of regional consolidation we’ve been predicting may be gaining steam. The map (below) shows what the combined position of the various companies would look like after the deals close later this year.

A fair question is whether these transactions indicate that the governance issues mentioned above have been overcome and the expected wave of consolidations are upon us. A closer look at this situation, however, probably wouldn’t lead you to that conclusion. Bonanza Creek, HighPoint and Extraction were all publicly traded, which makes valuation issues less subjective; and often, change-of-control provisions in public company management agreements (as opposed to cash-on-cash management incentives in private equity-sponsored companies) make it easier for management teams to support consolidation deals. Crestone Peak is a private company, but its primary shareholder is the Canada Pension Plan Investment Board, which may view its diminished level of control over the combined entities differently than a traditional private equity fund would. Another unique aspect of this combination is that HighPoint and Extraction recently exited bankruptcy proceedings with cleaned-up balance sheets.

RELATED:

Bonanza Creek Continues D-J Basin Consolidation with Crestone Peak Deal

Taking it all in, I’m not ready to say the “wave” of consolidations is finally here, but there seems to be a good rationale for continued combinations of single-basin public companies with improved balance sheets. To the degree that recently increased commodity prices have reduced balance sheet pressure on many companies, that can only help, and although a “wave” seems premature, I do expect we’ll see more consolidation deals announced this summer.

About the Author:

Steve Hendrickson is the president of Ralph E. Davis Associates, an Opportune LLP company. Hendrickson has over 30 years of professional leadership experience in the energy industry with a proven track record of adding value through acquisitions, development and operations. In addition, he possesses extensive knowledge of petroleum economics, energy finance, reserves reporting and data management, and has deep expertise in reservoir engineering, production engineering and technical evaluations. Hendrickson is a licensed professional engineer in the state of Texas and holds an M.S. in Finance from the University of Houston and a B.S. in Chemical Engineering from The University of Texas at Austin. He recently served as a board member of the Society of Petroleum Evaluation Engineers and is a registered FINRA representative.

Recommended Reading

Kimmeridge Fast Forwards on SilverBow with Takeover Bid

2024-03-13 - Investment firm Kimmeridge Energy Management, which first asked for additional SilverBow Resources board seats, has followed up with a buyout offer. A deal would make a nearly 1 Bcfe/d Eagle Ford pureplay.

Hess Corp. Boosts Bakken Output, Drilling Ahead of Chevron Merger

2024-01-31 - Hess Corp. increased its drilling activity and output from the Bakken play of North Dakota during the fourth quarter, the E&P reported in its latest earnings.

Petrie Partners: A Small Wonder

2024-02-01 - Petrie Partners may not be the biggest or flashiest investment bank on the block, but after over two decades, its executives have been around the block more than most.

CEO: Coterra ‘Deeply Curious’ on M&A Amid E&P Consolidation Wave

2024-02-26 - Coterra Energy has yet to get in on the large-scale M&A wave sweeping across the Lower 48—but CEO Tom Jorden said Coterra is keeping an eye on acquisition opportunities.

CEO: Magnolia Hunting Giddings Bolt-ons that ‘Pack a Punch’ in ‘24

2024-02-16 - Magnolia Oil & Gas plans to boost production volumes in the single digits this year, with the majority of the growth coming from the Giddings Field.