Liberty Oilfield Services developed its Quiet Fleet during the downturn to serve customers, particularly in Colorado, that conduct operation near expanding population centers. (Source: Liberty Oilfield Services Inc.)

[Editor's note: A version of this story appears in the November 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Oilfield service companies are perhaps faster, leaner and more efficient than they’ve ever been—and it’s killing them.

Veteran executives and observers don’t mince words. Debt-laden service companies are “holding ticking time bombs.” Some are adopting capital austerity budgets. In a crowded group of companies, most don’t have the leverage to negotiate good rates with their upstream customers.

And time is slipping away.

“There are a number of players in our space with a lot of debt, probably not great prospects. I do think you will see more restructuring,” Liberty Oilfield Services CEO Chris Wright told Oil and Gas Investor.

The services industry is a world turned upside down. That some companies won’t survive may be a given. But the sentiment among industry leaders is that for the sector to thrive, the best-case isn’t whether companies will fail—but if enough will.

Jim Wicklund, managing director at private-investment bank Stephens Inc., said there are roughly 100 public oilfield service companies globally, about 80% of which are microcaps worth less than $1.5 billion.

Wicklund sees a need to radically thin the herd to about 25 or 30 companies.

“There are sub-sectors inside of service, and that’s why I’m saying it’d be 30. You need three to five players, big players, in every sub-sector,” he said.

The service industry’s oversupply takes place against the backdrop of a relentlessly dropping total U.S. rig count. In the first nine months of the year, an average 5.6 rigs were taken off the field each week. The week of Jan. 4, the rig count stood at 1,075. The week of Sept. 27, the count had fallen to 855, according to Baker Hughes. For land rigs alone, the past 12 months ended in September saw nearly one in five taken offline.

If the oil rig count seems to be on a familiar angle of descent, it’s because horizontal gas rigs have already skidded over the same runway.

In 2008, the gas rig count peaked at about 1,600. By January 2016, it fell to 148 gas-directed rigs, a 90% drop, according to Jeffries.

Yet, gas production “went up every year,” Wicklund said.

Three years later, Wicklund sees the same pattern. The rig count drops, but “we’re still expected to be a million barrels a day oversupplied in 2020,” he said. “This could be the market we’re in for the next couple of years.”

of companies out

there are for sale,”

said Chris Wright,

CEO of Liberty

Oilfield Services.

“There’s a desire

in the industry [to

consolidate].”

With too much equipment and too many companies, nearly all are suffering. The OSX index of publicly traded oilfield service companies shed about 20% of its value from January to September.

“Collapsing earnings combined with banks that are generally unwilling to refinance debt mean rafts of service companies may end up in the hands of their lenders,” said Richard Spears, vice president and co-founder of Tulsa, Okla.-based market research firm Spears & Associates Inc. “That rarely works out well for employees or customers.”

Next year, Spears told Investor, “will be the battle of the balance sheets.”

That battle has begun. Companies that cut deeply during the downturn are now starting to saw past the bone and into the marrow.

National Oilwell Varco (NOV), for instance, slashed $3 billion in personnel costs and $1 billion in overhead during the three years of the downturn. In first-quarter 2019, the company began hunting for another $120 million in annualized cost savings.

In the second quarter, the company enacted a voluntary, early retirement plan and embarked upon the redesign of several administrative functions to move closer to a shared services model, NOV CEO Clay Williams said on a July 30 earnings call.

With E&Ps living under a mandate to live within cash flow, an oversupplied service market allows E&Ps to gravitate toward the cheapest bidders.

“If that means screwing your service customers for right now, so be it,” he said. “So, right now the lowest [priced] job wins.”

The squeeze

In August, Key Energy Services president and CEO Rob Saltiel told analysts listening in on an earnings call that the road so far in 2019 had been uneven.

Upstream companies no longer plan their budgets on an annual basis. “The fact is that our clients now manage their budgets on a quarterly, if not monthly basis,” he said. Key Energy did not respond to requests for additional comment.

To their credit, many oilfield service companies continue to drive improvements in efficiency, which allow upstream companies to realize better returns even as oil prices rarely stray above $65 per barrel. In the first six months of 2019, the median price of oil was $56.60, according to U.S. Energy Information Administration data.

Spears said E&Ps are taking advantage of service-sector weakness and the lengths to which the industry will go to get business.

“This is an excellent time to be an oil company and a terrible time to be a service company,” Spears told Investor. “Service firms have almost no ability to negotiate favorable contract terms because the competitor down the street will work for a dollar less.”

He added that 2020 is already shaping up as a battle of the balance sheets. As the new decade begins, service company prices could increase within six months of a climb in drilling activity—but, Spears said, “is that a 2020 event?” Service companies have become, in a sense, “fairly commoditized” and, as a result, are stretched thin, Wicklund said.

“Unless you’re very special in some way, you’re just being buffeted by whoever bids the lowest.”

That sets up a near-impossible challenge for services companies that, just like E&Ps, are being judged on their ability to return capital to investors.

The squeeze on oilfield service companies has a crucial flaw, Wicklund argued. Service companies need to reinvest in equipment.

“Eventually, it will come back to bite E&P companies, because the service companies won’t have had the capital to reinvest in new equipment,” he said.

At some point, upstream companies will put out a request for proposal and no one will bid because they won’t have the equipment for the job.

“But, as with most things in life, we don’t deal with an issue until it hits us in the face,” Wicklund said.

In a cutthroat environment, Saltiel said the obvious way out of the industry’s labyrinth is consolidation. Mergers, he said, are the most efficient way to increase scale, reduce costs and create value for investors.

“Every business line we compete in is very price sensitive,” he said. “Only the lowest-cost players can thrive through the cycle.”

But, he added: “It takes two willing boards and shareholder bases to make consolidation happen.”

The industry, he said, continues to wait on the sidelines and hope.

The A&D snag

In June, C&J Energy Services and Keane Group Inc. announced a combination hailed by analysts as a merger of equals. Pro forma, the new company would be worth about $1.8 billion with $255 million in net debt.

“Consolidation always occurs at this point in the cycle,” Spears said. “The valuations of companies being bought are typically quite low, and the acquirer doesn’t always survive, but if they do survive, the following upturn in business creates enormous wealth for shareholders and launches a bunch of great opportunities for employees.”

Why aren’t there more? The holdup, industry professionals say, is competing interests among companies.

“More than half of companies out there are for sale,” Wright told Investor. “There’s a desire in the industry [to consolidate]. It’s sort of a theoretical desire. Making it happen—it’s happened slower than I would have guessed,” he said.

Consolidation has stalled, in part, because some companies have “misaligned incentives to get deals done. I hear plenty of stories that are preventing deals from happening,” he said.

Wicklund offered a more blunt assessment: The sticking point isn’t whether financial benefits or potential synergies will arise.

The obstacle is “what we are euphemistically calling ‘social issues,’” he said.

A consolidation means some workers may lose their jobs. But in a merger, at least one CEO is “definitely going to lose their job.”

Consider two midsized companies in which both CEOs earn $4 million annually, Wicklund said.

“Which one of us is going to lose our job? And whoever loses their job, where are they going to go out and find another $4 million a year position in the current market?

“I only want to combine if I’m the one who keeps my job,” Wicklund said. “And if everybody says that, who combines?”

Wicklund said the C&J-Keane transaction succeeded because C&J CEO Don Gawick agreed to walk away.

The service industry also lacks a large-scale aggregator of service businesses. Among the sub-sectors in the service space, there aren’t any easily identifiable consolidators in sand, pressure pumping or drilling.

“Pick a sub-sector of the market and there’s nobody,” Wicklund said. “Who’s going to consolidate the pressure pumping market?”

With consolidation largely stalled, Wicklund said service companies will continue to scrape by and be shut out of badly needed capital. Private-equity and institutional investors aren’t interested in investing in the smaller companies, Wicklund said.

“The oilfield service industry arguably has six investable names,” such as Halliburton Co., Schlumberger Ltd. and NOV, he said.

For companies unable to serve E&P giants such as Exxon Mobil Corp., “the concern is you’re going to end up with a significantly bifurcated market where the big service companies work for the big oil companies and everybody else fights it out at the bottom.

“So it’s not consolidation for consolidation’s sake,” Wicklund added. “It’s a whole bunch of different issues driving the need for scale.”

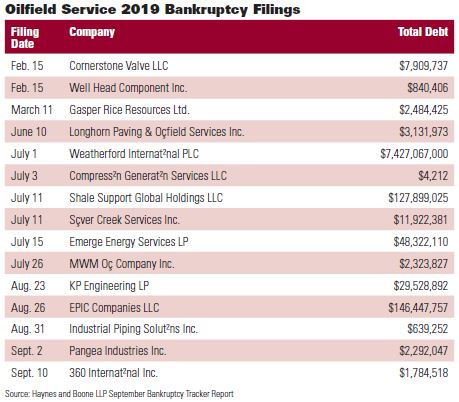

The bankruptcy edge

In 1987, as Ratliff Drilling Co. started to unravel financially, the company surrendered 13 rigs to two Oklahoma banks and prepared to liquidate.

But some banks today, fearing a repeat of the 1980s, don’t want to own rigs. As lenders move away from ruinous liquidation to converting debt to equity, bankruptcy has become a competitive advantage for some companies.

“Collapsing earnings combined with banks that are generally unwilling to refinance debt means rafts of service companies may end up in the hands of their lenders,” he said.

“Nobody has to sell anything,” Wicklund said. “Nobody quits operating. There were no repercussions.”

Wicklund calls it the American Airlines problem. At a time when other major carriers were filing bankruptcy, American Airlines stayed out of the courthouse. Then they found out they couldn’t compete.

“Everybody else had written down their debts to zero, and their returns were significantly better,” he said. “So, American Airlines had to declare bankruptcy just to play on a level playing field with the other airlines. And so now if your competitor goes bankrupt, he is now a stronger competitor than he was before. Not a weaker one.”

For oilfield service companies, bankruptcy doesn’t result in vanishing assets, he said.

“Every company that’s gone through bankruptcy—Key [Energy Services], Basic [Energy Services]—they didn’t have to sell a single workover rig. All their debt turned into equity, and they never missed a beat,” he said.

Jr., a bankruptcy

attorney at Haynes

and Boone, said

some oilfield

service companies

appear to be

“hanging on by

their fingernails,

trying to maintain

market share.”

Charles Beckham Jr., a bankruptcy attorney at Haynes and Boone, said some oilfield service companies appear to be “hanging on by their fingernails, trying to maintain market share.”

He said more bankruptcies may be filed.

“The fewer rigs that people have working out there means they’re all competing against each other in the different segments in the oilfield industry,” Beckham said. “So, there’s over capacity.”

While companies will promote their safety and quality to customers, their true leverage may be in pricing.

They are continuing to chase the work. And the easiest way to get a new contract is to bid less than their competitor, he said. “And if you’re losing money on each job bid, it’s impossible to make it up on volume.”

Self-fulfilling profits

Like their upstream counterparts, service companies are intent on being disciplined stewards of capital. But there’s a paradox worthy of Socrates’ “all I know is I know nothing” at the heart of the services industry.

“You actually have to have some capital to spend before you spend it in a disciplined manner,” Wicklund said.

Service companies are caught in multiple catch-22s, none perhaps as self-defeating as their relentless drive to create more efficient services—which leads to greater obsolescence of their fleets.

“If you’re 10% more efficient, than I effectively have 10% more capacity than I needed before,” Wicklund said. “So until some of this equipment starts to wear out, we’re going to be an oversupplied market.”

Technology has been both a saving grace and an Achilles’ heel for some companies.

“We’re victims of our own supply,” Wright said. “What fixes oversupply? Two things: disciplined investing and time.”

Liberty, which Wright describes as a company of self-described “tech nerds,” focuses solely on hydraulic fracturing. The company runs 23 frack fleets, including 14 in the Rockies and nine in Texas’ Permian Basin and Eagle Ford Shale.

Wright pointed to Liberty’s cash returned on the capital invested, which only dipped into negative territory in 2016, at the height of the downturn. The company saw 44% returns on investments in 2017 and 43% in 2018.

Wright recognizes that the industry’s improvements in drilling rates have buoyed the overall oil and gas industry. And that advances create “downward pressure on prices of services that are getting much more efficient.”

But Liberty said more sophisticated companies look at total costs. E&Ps may spend about $30,000 a day for equipment and manpower at a drilling location. Competitors may charge lower rates, but take 45 days to do a job Liberty can finish in 30.

“That saves them $400,000. With Liberty moving faster, you also get oil on 15 days sooner. So you get revenues earlier,” Wright said.

Liberty intends to stick to its strategy during the downturn: meet customer demand. The company began to develop its quiet fracturing fleet in the summer of 2014 and continued to work on the fleet during the downturn, rolling it out in the summer of 2016 “when things were awful.”

The company could have shut down the research or laid off employees as other companies did. Instead, “we played the long game,” Wright said.

Once again, however, the industry is in an inhospitable environment. Service companies are chasing technological advancements, especially in machine learning and automation.

But technology may yet aid service companies by turning focus inward, into how it can benefit their businesses.

“The industry has really not spent a whole lot of capital on the technology of running a business. They spend all their money on technology for their downhole tools or whatever their product is,” Wicklund said. “So, this cycle you’re seeing companies start running their businesses better.”

Still, the industry sees technology as leading the way in the field as well.

“This is what brought the shale revolution,” he said. “This is what will distinguish the winners and losers: differential technology.”

The number of companies will still need to shrink as market conditions tighten even more.

“That process from where we were five years ago to where we’ll be in two or three years is indeed painful,” Wright said.

Recommended Reading

NOG Closes Utica Shale, Delaware Basin Acquisitions

2024-02-05 - Northern Oil and Gas’ Utica deal marks the entry of the non-op E&P in the shale play while it’s Delaware Basin acquisition extends its footprint in the Permian.

Vital Energy Again Ups Interest in Acquired Permian Assets

2024-02-06 - Vital Energy added even more working interests in Permian Basin assets acquired from Henry Energy LP last year at a purchase price discounted versus recent deals, an analyst said.

California Resources Corp., Aera Energy to Combine in $2.1B Merger

2024-02-07 - The announced combination between California Resources and Aera Energy comes one year after Exxon and Shell closed the sale of Aera to a German asset manager for $4 billion.

DXP Enterprises Buys Water Service Company Kappe Associates

2024-02-06 - DXP Enterprise’s purchase of Kappe, a water and wastewater company, adds scale to DXP’s national water management profile.

Tellurian Exploring Sale of Upstream Haynesville Shale Assets

2024-02-06 - Tellurian, which in November raised doubts about its ability to continue as a going concern, said cash from a divestiture would be used to pay off debt and finance the company’s Driftwood LNG project.