Presented by:

Joe, senior VP, drilling: “Siri, we’re ready to start the zipper, dual fuel e-frac in 45 minutes on Pad 12.”

Siri: “Okay. Sending group text to Pad 12 crew and Ricky at SchlumberHal.”

This year Oil and Gas Investor celebrates the fact that it made its first appearance in 1981. Forty years on, the independent E&P universe we cover has changed considerably. Now seemingly at a crossroads, what lies ahead for these companies in the next 10, 20, 30, (dare we say 40) years?

After we spoke to a variety of observers, two things became clear: All are concerned; all are optimistic. As they said in one voice, oil demand is not going away entirely. There are few viable substitutes of scale—yet.

Besides, they said, independents are fighters. They always have been, ever since the first entrepreneurs fought off the aggressive business tactics of John D. Rockefeller’s Standard Oil Trust. They have shown they are flexible, so they will adapt to new technologies and new regulations.

Their optimism shines whenever they make that phone call ordering a rig.

“I think the smaller independents will be around—they have always been the backbone of this industry,” said Harold Hamm, chairman of Continental Resources Inc., an independent in business for 54 years. “They are very tough. The industry will be around, but it will change.

“We know 85% of the oil is still left in the source beds, so everything we’ve used up in the last 150 years with our best technology is part of that 15%. So, there’s a lot of oil left to go.”

Still, independents face many new challenges today, from delivering ESG best practices to meeting heightened investor demands, managing limited capital availability and the whole energy transition theme, which raises plenty of questions about the future of the oil and gas industry itself.

“Oil and gas is going to be here for a long time—hydrocarbons are the lifeblood of the worldwide economy,” said EnCap Investments LP partner Kyle Kafka. “The U.S. in particular benefits immensely from the low cost of energy that our industry provides. It will remain a vital part of a growing energy need even as the energy transition continues to gain traction and realizes broader commercialization.

“Two driving themes over the last few years are an increased focus on ESG, and a move away from growth and a shift toward shareholder returns. We believe these will remain central tenants of the industry for the long term. To maximize returns and insulate from the next downturn, companies need to be nimble (low overhead and operating costs), avoid leverage, allocate capital to highest returning projects, use immense data set to make smart and predictive decisions, and proactively engage with stakeholders and incorporate ESG into the fabric of company decisions. We do believe the right teams and assets can generate extremely attractive returns following this playbook, and the returns of high performing companies (and the associated yield) will be tough to ignore in a yield starved world.”

“This is a cycle whose measuring tools have changed,” said Cameron Smith, principal, COSCO Consulting LLC, who has years of experience in private equity and running independent E&Ps.

“Value creation and market capture [during the shale boom] were good, but in terms of cash-on-cash returns, no. But there’s no way that 40 years from now, there would be no demand for petroleum-based products. My concerns are not about the industry’s ability to make money and ‘survive.’”

But he is concerned about the focus on ESG matters and wonders how that can be measured and if it will actually create any real value. “There’s so much money, time and talent being used in the energy transition; that money would have been used 10 years ago to find oil and gas, and now it’s not.”

His advice for the future? Go back to the basics and do what you have to do to attract the capital you need.

Analysts have noted that most public independents in the first quarter generally delivered the highest free cash flow in a decade, after a disastrous prior two decades, as far as investors are concerned. After 2020, one of their worst years ever, they are rallying.

“Public independent oil producers’ profits will set a record this year, surpassing the levels reached when crude oil hit an all-time high near $150 a barrel more than a decade ago,” according to Rystad Energy. “Combined free cash flow from the sector is expected to surge to $348 billion, beating the previous high of $311 billion in 2008,” Rystad said.

But indies are also being judged by new standards: not just production numbers, but financial metrics like costs per foot drilled and returns to shareholders. Not just reserves growth, but environmental metrics like emissions reductions or flaring as a percent of gas production.

“We’re in a period of real adaptation. I think there is some degree of alarm out there. The pressure for people to be sensitive to things like emissions is very high and probably not going away,” said Tom Petrie, chair and co-founder of Petrie Partners. He’s been involved in the industry as an award-winning equities analyst, M&A and corporate advisor and investment banker for about 40 years.

“I do believe the independent sector is in the process of quite a transition, but there’s a real good role for them. I do think there’s some question about what independents have to do to become viable and effective.

“Will the industry survive another 10 to 20 years, what with net zero? It will be a real test.”

Consolidation

Most experts foresee a lot of consolidation ahead. Even decades ago, think tanks were predicting the nature of the business would eventually change such that there would be only two or three large-scale operators per basin. It may not get to that, say sources we talked to.

“Post-shale, scale becomes very important. And there are too many competitors. Competition is a wonderful thing, but there needs to be a rebalancing of the number of players and their scale,” Petrie said.

“We’re in a contraction, but I don’t think there will be total elimination,” he said. “The advantages of scale will be very important, not least because of government policy issues, environmental compliance issues. The midsized company universe certainly shrinks, to my mind.”

“We think consolidation will continue, but we don’t expect to see only mega-independents dominating the core basins,” said EnCap Investments partner Brad Thielemann. “Basins like the Permian, Eagle Ford and Bakken have a significant number of years of very high-quality and high-returning inventory.”

“There will always be smaller, nimble operators seeking to unlock the absolute best way to develop each unique acre of a play in ways that a massive operator cannot,” added his colleague, EnCap partner Kafka. “This is currently evident in the market as we see larger operators selling acreage they view as noncore to smaller operators who are willing to spend the time and resources to maximize the value of the asset.”

Geoff Davis, who has 40 years in the business as an investment banker, now consulting for Morgan Stanley as needed, noted the need to consolidate will grow stronger in the future.

“When we [Morgan Stanley] go to the Middle East [to do business], we talk to one company in Qatar, one company in Saudi Arabia. We talk to five in Argentina. But when we do business in the U.S., we have to talk to a thousand companies? We’re an entrepreneurial society, but is this a sustainable business model? Are investors willing to invest in this model in 40 years?

“But for anything to happen, a thousand management teams have to blink, and CEOs don’t want to blink.”

OIL DEMANDThe future of the independent depends on what oil demand will be in the future. Jude Clemente, the Pittsburgh-based editor of RealClear Energy, clarified our thinking by writing this recently: “Let’s start with the obvious: Oil is the world’s most important fuel, supplying 35% of all energy and over 95% of transportation needs. “More than 6,000 everyday products contain oil as their core ingredient. Simply put, oil has no significant substitute, and it won’t for a long time. Massive amounts of wind and solar won’t displace ‘black gold’ because these sources compete only in the power-generating sector, where oil effectively plays no role.” Bernstein Research did a deep dive on the topic, looking at the data and projections of a handful of the usual suspects: the Energy Information Administration, the BP Annual Statistical Review and the International Energy Agency. In a business-as-usual scenario, oil demand will grow by 1% to 1.5% per year during the next 40 years. The analysts said this scenario is not the most likely one, however. The report said that if electric vehicles (EVs) were to reach half of all car sales by 2030, oil demand could plateau later in this decade, but then grow slowly with increasing petrochemical demand. “If EVs reach only 15% to 20% of sales in 2030, then total demand could still row by 1% per year.” The EIA’s startling report called for oil demand by 2050 to be only a fourth of what it was in 2019, before the pandemic. But many observers remain calm. “If you are worried about electric vehicles, don’t be!” said Thurmon Andress. “The upcoming motorization rate of China and India will dwarf the U.S. and Europe’s motorization. The number of electric vehicles will definitely grow in absolute numbers but as a percent of total vehicles the numbers are surprising. In 2020, EVs accounted for 3.25 million of the 77.5 million sold globally (4%). Currently, out of the total 1.4 billion vehicles there are 10.5 million EVs, or about 1% of all vehicles on the planet. No matter how many times you compound their growth, you will not even stay up with population growth.” A Cowen & Co. analysis in June looked at EV growth projections from 22 automakers and the current trajectory of EV adoption and how that may affect oil demand. “Transportation is the largest component of oil demand at about 60% of total demand; passenger demand accounts for about 40% of that 60%, the largest component and the one expected to transition to EVs the quickest. “We conclude oil demand is unlikely to peak by 2030 as a result of EV penetration, bringing into question the most aggressive strategic pivots from large hydrocarbon companies while seemingly justifying more balanced approaches.” The company concluded that oil demand may be reduced by about 2 million barrels a day by 2030. |

Resilience and changes

Oilmen like to joke that in good times the family eats steak and during the price busts, it’s back to cheap hamburgers. Twenty, 30 or 40 years from now, will they be eating fake meat grown in a lab somewhere?

Since 1859, they’ve ridden the ups and downs of the economic cycles that drive demand, endured the Depression, recessions, war, OPEC price shocks and more. They have adopted the splashy technical advances that drive oil supply, and they have managed around oil prices that ranged from nearly zero to $147/bbl, navigating geopolitical storms and everything in between.

There is no reason to assume they won’t continue in this vein, especially since the industry is populated by so many thousands of entrepreneurs with the dream of using oil and gas to accumulate wealth. Independents are not going away, but they may change.

The biggest ones are changing already, because when you’re big enough, you can command new things to happen. You’ve got the balance sheet; you’ve got the people; you’ve got the technology. You may even have international operations to supplement U.S. ones.

If you count all its predecessor companies, ConocoPhillips Co. is one of the oldest indies around, with a founding date of 1875. Recently, CEO Ryan Lance said on a conference call that it aims to be the premier indie. That means maintaining great, consistent financial returns, great ESG metrics, a net-zero emissions goal by some future date, maybe even a move into solar, wind, EV charging stations or other alternative business lines.

“We want to be the most relevant, sustainable E&P company in the business,” he said. “We believe there’s a valuable role for companies like Conoco in the energy transition.”

Similarly, many other public companies have made vows to reduce flaring, other emissions, and carbon footprint. Diamondback Energy Inc. has pledged to be a net-zero producer in Scope 1 emissions immediately; Devon Energy Corp. pledged to cut its emissions in half by 2030.

“Tackling methane represents an opportunity for the United States to develop increased global climate, geopolitical and economic influence, leveraging the technological skills and leadership of our industry to capture greater global LNG market share,” said Toby Rice, president and CEO of EQT Corp., the nation’s largest gas producer. EQT has joined an international group called the Oil & Gas Methane Partnership 2.0, which represents about 30% of global gas production, to help the industry achieve net-zero emissions.

It also announced targets to achieve net-zero Scope 1 and 2 greenhouse-gas (GHG) emissions in its production segment operations by or before 2025.

At some point in the next decade, carbon capture, storage and sequestration will become the norm and may not generate big headlines anymore. Commercial, large-scale hydrogen businesses will emerge, some based on natural gas. (For more on this, see Oil and Gas Investor’s July 2021 issue.). Renewable diesel and renewable, certified natural gas will be the norm. If new technologies enable it, even crude oil might become certified in some way.

“There are revolutionary but exciting changes going on. I do believe we have the talent in this industry to deal with all this,” said Dennis Petito, CEO, Montrose Energy Capital Advisors LLC. “The next five or 10 years will be extraordinarily challenging, and those that make it through will not resemble the current lot [of E&P companies].”

Carbon management

Petito told Oil and Gas Investor he thinks the industry may compartmentalize to the extent that an indie will find the hydrocarbons and then flip those to a much larger E&P or service company that will operate carbon capture and storage facilities and make a new business out of that. “I think carbon capture, utilization and sequestration (CCUS) will be a big factor ... and I think it will happen faster than we think. The era of poor stewardship is going to come to an end and do so very quickly.”

Another example of this came when Occidental Petroleum Corp. CEO Vicki Hollub spoke during a virtual IHS CERAWeek presentation in December 2020. She mentioned how the long-lasting company (founded in 1920) is changing to become, in her words, “a carbon management company.” Although it still has domestic and international E&P and marketing and chemical operations, new things are being added to the Occidental roster.

“Where we got the idea of ‘green oil’ was the fact that it takes more CO₂ injected into the reservoir than the barrel of oil that is produced from that CO₂ emits when burned. The fact that more injected and less burned means that you are either carbon neutral or negative. It depends on the reservoir as to how much CO₂ offset difference there is between the injection and the emission.

“Ultimately, I don’t know how many years from now Occidental becomes a carbon management company, and our oil and gas would be a support business unit for the management of that carbon. We would be not only using [CO₂] in oil reservoirs [but] capturing it for sequestration as well. I expect that in the not too distant future our OxyChem business will also be involved in some way to use CO₂ in products that they make. We’d have three ways to manage the CO₂ with both OxyChem and the oil and gas business being a support for that. I believe this industry is going to be huge,” Hollub said.

Does size matter?

A Goldilocks scenario is evolving where many people we spoke to think the very largest indies will change, diversify, survive and thrive, and the thousands of smaller ones, such as family-owned entities, will survive as they always have. The even smaller private mom and pops will survive, although probably fewer numbers. It’s the future of the public ones in the middle that are not too small, yet not big enough, that seems to be in question.

“I think the most uncertain part of the industry is the fate or role of the smaller E&Ps, public and private, although that could be helped by higher commodity prices that help the economics of having lesser-quality acreage,” said Tom Biracree, co-founder of Oil & Gas Financial Analytics LLC.

“The average size to be a survivor is moving up, but it’s hard to define it. It’s the companies in the middle that seem more at risk. I think the small or midsized public is most challenged and could find it harder to grow,” said Steve Hendrickson, president of Ralph E. Davis Associates, an Opportune LLP company, with a long history dating from 1924. He started his career at Shell Oil and worked at several independents as well, including Sonat (acquired by El Paso Production Co.) and Eagle Rock Energy Partners LP.

ESG matters

Stephens Inc. guru Jim Wicklund noted in his weekly newsletter that ESG topics are in the forefront at most conferences he attends and many headlines he reads, dominating the conversation. That will change, he said.

“I consider ESG somewhat akin to Sarbanes Oxley—something we questioned and complained about a lot, but today that rarely prompts a question. I fully expect that in three to five years, we won’t hear or read about ESG anymore than we talk about Sarbanes Oxley or 10-K disclosures. But it will be a key part of the industry ‘ratings’ for a long time.”

“There’s not been one drop of oil or one Mcf of gas that’s disappeared in the U.S. yet,” said Morgan Stanley’s Davis. “We all recognize the importance of being green, and carbon capture is something we need to do, but I think the rhetoric is going faster than the reality.”

COSCO’s Smith said that if you are a private company living off cash flow, you simply have to do less than a public firm regarding meeting ESG criteria, which he thinks will be very expensive for the larger public companies.

Other trends

A few recent news items illustrate how the upstream industry is changing and adapting to ensure its future. Intriguing deals, joint ventures (JV), carbon capture, emissions reduction—all are on the table.

This summer, Riley Exploration Permian Inc. said it will focus on EOR using CO₂ captured from power plants, in a pilot project in Yoakum County, Texas.

Priority Power Management LLC, an independent energy services provider, announced it will provide solar power via a solar development services agreement to FireBird Energy LLC, an E&P operating numerous properties in the Midland Basin.

Midstream giant Williams inked an upstream joint venture with privately held Crowheart Energy of Denver in the venerable Wamsutter Field of the Greater Green River Basin. The JV consolidates three legacy operating assets from BP Plc, Southland Royalty and Crowheart itself, totaling over 1.2 million net acres, over 3,500 operating wells and more than 3,000 potential development locations.

The deal creates a larger, contiguous footprint that enables the companies to deliver cost savings and synergies. Combining all the reserves will enhance the value of Williams’ midstream and downstream natural gas and NGL infrastructure in the field and give Crowheart plenty of running room as the operator, with a 25% stake. Williams, with 75%, will continue to operate and retain full ownership of its midstream assets. But, with such a huge portion of the JV, Williams retains significant governance rights, including control of the selection and pace of operations pursued by Crowheart and the ability to exit its upstream ownership position.

“I think the private independents are going to be OK. They are a different cluster—they have options that the publics do not, and they’ve always been so scrappy,” said Michelle Michot Foss, a fellow in energy, minerals and materials at Rice University’s Baker Institute.

Michot Foss is co-author of a new book released in May, “Monetizing Natural Gas in the ‘New Deal’ Economy,” which draws on her 40 years of experience analyzing national and global energy economics and trends. She believes natural gas will have a huge role in the energy transition, thereby assuring independents of a continuing business. After all, someone has to produce hydrocarbons to make the steel, metal and plastic found in wind farms or solar equipment and electric vehicles, she said.

She still sees an independent oil patch and one with somewhat better prospects for private firms than publics. Both will have to contend with public outcry if price hikes from undersupply become a problem in five or 10 years.

“The idea that people will stop using these hydrocarbons is nonsense.

“If I was a small public, I’d figure out how to go private because the publics are so much more exposed to the politics of energy and climate,” Foss said. “If you are a private indie, you can fly under the radar and get business done. They can move into new locations others have forgotten about. You have to pick your battles.”

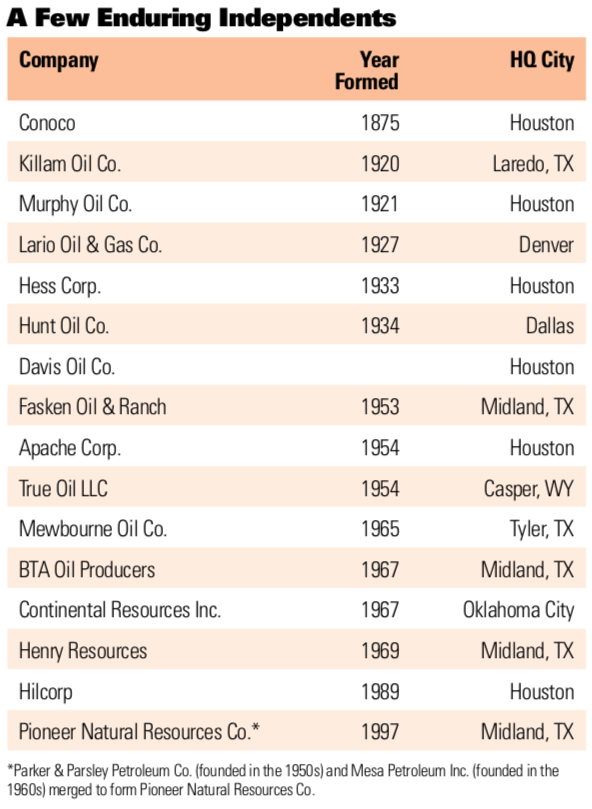

TWO INDIES SPEAKPatrick Noyes was present at the dawn of the Shale Age, lucky to be working for George Mitchell’s firm when the thought of shale was sketchy at best. Fast forward to 2021, when Noyes launched Grenadier Energy Partners III with a $400 million commitment from EnCap Investments L.P. He recently sold Grenadier II to Surge Energy US Holdings Co. for $420 million. Both companies are Permian Basin-focused. “In a perfect world, we’d be right back in the Permian,” he told Oil and Gas Investor. The NewCo will be buying PDP so it can immediately distribute cash flow back to investors. As for the industry’s future, and his place in it? At age 67, he has succession plans in place, and he’s been dealing with investor demands and ESG matters for years. Like many others, he thinks private equity-backed companies such as Grenadier will be few and far between compared to the past. “None of these issues are surprises to us. We’ve made changes to our operations to account for that and mitigate that. For example, we converted all our instruments from gas to air ... as we go forward, we’ll take [ESG matters] into account in whatever assets we buy.” As he started Grenadier III, he recognized going digital would be more important than ever, and he has hired accordingly. “It’s good to have a balance of people who’ve seen a lot, but I can’t manipulate that data like these young folks can.” Cliffe Killam is a partner in the business his great-grandfather started in 1920, Killam Oil, in Laredo, Texas. In 1924, he sold some production to Magnolia, a forerunner of Exxon Mobil Corp. With the latter company, in the 1950s he drilled what was the deepest gas well in the world at the time. “We have multigenerational thinking; I’m the fourth generation, so we don’t mind doing things where it’s OK if it doesn’t pay out in five years,” Killam said. “Maybe your grandchildren will benefit from it. One lesson we’ve learned is not everything pays off, but if you buy something right it can have a long duration. That’s part of our family culture.” Today the conservative company—built for longevity—operates out of cash flow with zero leverage, and it hedges. It’s all based on family money with no outside investors, which affects how it assesses risk. “During the good times we put away cash into stocks, bonds, ranches to diversify. We’re able to harvest these and redeploy that cash into oil and gas, so we can weather the storm,” Killam said. Nearly all its operations are in conventional plays, although it is looking at other opportunities, he said. It also buys minerals and makes acquisitions. For the future of independents, Killam is optimistic. “There is going to be a path for independents to be active and prosperous. There will always be a spectrum of different types of companies, whether they are private equity-backed or Exxon [Mobil]. I think there is room for everybody. The key to success is going to be how you adapt and manage risk. “And, the industry has a moral imperative to state its case.” |

Two business models

Nick Cacchione and Tom Biracree, analysts formerly with John S. Herold and other firms, have watched the independents for years, ranking them with numerous metrics. They have recently formed Oil & Gas Financial Analytics LLC to track 40 public E&Ps. They believe indies of the future have to do more of what they’ve just begun to do: get their balance sheets in order, target relatively low-growth production with cash flow, lower debt and deliver returns to shareholders.

“What they don’t want to do—and we have a perfect example in the coal industry—is never get off their tendency to overdevelop when prices are high and then end up with a surplus that tanks prices. For coal, their only business plan seems to be pleading with the government to save a dying industry,” said Biracree.

Two business models seem to be emerging, he said: larger companies such as ConocoPhillips or Pioneer Natural Resources Co. will continue to more responsibly develop the shales, observing ESG practices. Smaller E&Ps like Northern Oil & Gas or Diversified Gas & Oil will consolidate and act almost like a master limited partnership, to buy older producing properties.

“At $70 oil and rising gas prices, it can be lucrative to buy producing assets and manage them down to the end of their life, with minimal capital investment,” Biracree said.

It will be up to the larger indies to determine how much Tier 1 investing (drilling) is done and how to lengthen the time frame that the business lasts, added Cacchione. That search for inventory will drive M&A action. Examples include Pioneer’s purchase of DoublePoint Energy LLC or Southwestern Energy Co.’s acquisition of Indigo Natural Resources LLC—both deals meant to add inventory.

They’ll farm out their Tier 2 or 3 inventory to smaller entities as the properties become more mature. The one danger: getting bigger, but not getting better.

“I think renewable energy is not the focus of the small and mid-cap E&Ps,” said Biracree. “I think their response is to shore up their financial picture and produce more efficiently and maintain modest capex. I think if they do that, they’ll have tremendous cash flow and they’ll be investible.”

The future

We cannot presume to know what the world will look like in 40 years, but it will take some energy to keep things rolling. “The really big issue we will face is price shocks [from underinvestment] and the increased scrutiny that always brings,” said Foss.

We think the energy future could look pretty good in 10 or 20 years: There should be more widespread access to plentiful, affordable energy from oil, natural and renewable gas, sun, wind, water, hydrogen, nuclear and biomass. Probably not coal. Carbon capture, sequestration and storage will become a distinct industry sector with widespread use, whose growth trajectory and profits looks much like the advent of the midstream, water capture-recycling treatment and sand sectors that took place in the 2000s and 2010s.

Global oil demand may be lower than it is now, although we doubt it, but some level of demand will still be there, and especially if drilling underinvestment continues, not to mention the inevitable resource depletion that occurs in every producing field.

“The oil and gas industry has a future. Perhaps it will find a sweet spot—a level of production that’s neither high enough to destroy demand nor low enough to eliminate profits. But in that sweet spot, oil will be smaller, both as an energy source and as a raw material for industry. It will also be less relevant as a financial resource,” said Tom Sanzillo, director of financial analysis of the Institute for Energy Economics and Financial Analysis. (IEEFA is an organization dedicated to a profitable and sustainable energy transition.)

Thurmon Andress, president and CEO of Andress Oil & Gas, expressed the thought of many when he told Oil and Gas Investor that the independent will be the last man standing. With at least 45 years in the business, he should know. He founded, managed and sold several public and private E&Ps and was inducted into the All-American Wildcatters in 1996, among other honors.

“When you think about it, 40 years in the future would be the same as looking at the industry as someone would have in 1980 and trying to project where we would be today. In 1980, with many believing in M. King Hubbert’s peak oil projections, you might have thought there would not be any E&P business at all in 2060. But we did not know that George Mitchell would change the world,” Andress said.

“Technology has always saved our industry, and there is no reason to think it will be any different in the future. We probably have no concept of where it will take us by 2060. Can you imagine that technology might lead us to be able to recover 20% to 40% of the oil in place in shale plays instead of the current 10%?

“The data I have seen shows we will need to replace about 60% of our current production of oil and gas just to meet global demand by 2035.

“In short, I would not worry about the independents as they are the most resilient, entrepreneurial group in existence and will always be able to navigate the headwinds and the opportunities that come their way.”

Anti-fossil fuel thinking permeates headlines these days, but most oilmen are having none of it. “It’s very hard, difficult for me personally, to wake up every morning and see three articles about the death of your industry when you know it’s not the case,” Kaes Van’t Hof, Diamondback Energy CFO, told attendees of Hart Energy’s DUG Permian and Eagle Ford Conference and Exhibition in July.

“Diamondback and the industry, in general, are ready to fight this fight,” Van’t Hof said. “Where I come down in my final analysis is that in 40 years, the independent might just be the last man standing in our industry, especially when it comes to the United States.”

Recommended Reading

E&P Highlights: Feb. 12, 2024

2024-02-12 - Here’s a roundup of the latest E&P headlines, including more hydrocarbons found offshore Namibia near the Venus discovery and a host of new contract awards.

ChampionX to Acquire RMSpumptools, Expanding International Reach

2024-03-25 - ChampionX said it expects the deal to extend its reach in international markets including the Middle East, Latin America and other global offshore developments.

Triangle Energy, JV Set to Drill in North Perth Basin

2024-04-18 - The Booth-1 prospect is planned to be the first well in the joint venture’s —Triangle Energy, Strike Energy and New Zealand Oil and Gas — upcoming drilling campaign.

OEP Completes Acquisition of TechnipFMC’s Measurement Solutions Business

2024-03-27 - One Equity Partners said TechnipFMC’s measurement solutions business will be rebranded as Guidant and specialize in measurement technology, automation solutions and global systems.

Permian Activity in ‘Low-to-no-growth’ Mode for First Half

2024-02-22 - After multiple M&A moves in 2023 and continued E&P adherence to capital discipline, Permian Basin service company ProPetro sees the play holding steady.