Along with a significant acreage position, the Mach Resources-Alta Mesa deal provided Mach with control over Kingfisher Midsteam’s gathering and processing infrastructure. (SOURCE: MACH RESOURCES)

[Editor's note: A version of this story appears in the October 2020 issue of Oil and Gas Investor magazine. Subscribe to the magazine here.]

April 2020 came and went, but there was something familiar about the times, something anachronistic about Mach Resources LLC’s purchase of Alta Mesa Resources. It was déjà vu all over again for an industry stuck on repeat.

At least, that’s how it felt for Tom L. Ward.

Alta Mesa was once expected to have a market capitalization of $3.8 billion. The company’s worth never approached half that amount. It ended its public run with a value, as adjudged by Wall Street, of just under $27 million.

In the spring, Alta Mesa signed away its Midcontinent leases and midstream infrastructure for $220 million, ending the company’s brief rise and tortured fall through bankruptcy.

Mach Resources was the only serious bidder likely because it’s one of the few companies with the capital and the appetite to take on the Oklahoma assets. But this is a scenario made by design. Ward’s game plan, hatched two years ago, was to make Mach Resources an acquirer of distressed and overlooked assets.

Ward doesn’t fault Alta Mesa’s management team for its financial woes. The company had been run by the highly respected CEO Jim Hackett, who previously headed Anadarko Petroleum Corp. Alta Mesa’s troubles are part of a larger, universal ailment afflicting the industry, Ward said.

For the last decade or perhaps two, oil and gas companies have consistently lost money and, as an industry, “We’ve tended to over promise and under deliver,” he said.

Ward’s been talking about the gap in returns since 2015. In a May 2016 interview on CNBC’s Squawk on the Street, Ward was already convinced the industry model was off kilter, saying the industry’s “dirty little secret is you can’t really spend within cash flow and grow production.”

“I don’t necessarily think there’s anything that the [Alta Mesa] management team did wrong as much as that there’s been capital fleeing the industry for the last year or so,” he said. “And it’s getting more difficult to raise capital. That was pre-pandemic and price war, post-pandemic it became nearly impossible.”

Industry commentators often compare today’s COVID ravaged market to the disastrous oil glut of the 1980s, particularly 1987. Ward sees it more as a reflection of the oil and gas industry when he and Aubrey McClendon, who co-founded Chesapeake Energy Corp. on a handshake, began making deals in the 1990s.

Those times were filled with heartbreak but also rife with opportunity.

“And I think this is similar to 1998 when we were at Chesapeake and we were starting a growth,” Ward said. “What we’re doing today is very motivating to me. We are trying to thrive at a time when the industry is collapsing all around us.”

In 1998, the collision of several events sent oil and gas prices into a tailspin. Warmer than expected weather, an increase in OPEC oil quotas and a financial crisis in Asian markets sent oil prices to lows of about $10/bbl, according to the Dallas Federal Reserve Bank. Worldwide, planned engineering and industrial construction projects were canceled.

“Chesapeake at that time had raised some capital, and we were able to go buy some properties,” Ward said. “We had an idea that future prices couldn’t stay as low as they were because nobody had any money to drill. We also had a firm belief that natural gas prices could not stay at those prices because of new demand. This is very close to the way we see the industry today.”

Two decades later, the world has changed, but the strategy remains sound. Ward has capital with his partners at Bayou City Energy. And he has long rejected the idea of building new companies focused on growth.

“I’ve been very hesitant to invest capital into a growth through the drill bit company. That’s why we never competed really in the STACK or SCOOP or Permian or any of the highly competitive locations as other companies were doing,” he said. “This was not because there weren’t good places to drill. However, the cost of entry was too high.”

William McMullen, Bayou City Energy’s founder and managing partner, said Ward’s philosophical approach meshed well with Bayou City’s objective to put economics first ahead of the rock.

“Good rocks do not necessarily make for good investments,” he said.

Since 2018, the Houston private-equity firm and partner Mach Resources have set out to consolidate.

“There are too many E&P companies, and Tom and I have really set out to roll up the Anadarko Basin. That consolidation is our focus. We are big believers in scale in this market.”

Mach Resources isn’t running many rigs, instead operating “as cheaply as possible” by purchasing leasehold and infrastructure along with the reserves at significant discounts.

“I think at most we ran two or three rigs across half a million acres that we control in Oklahoma now,” he said.

Mach Resources instead operates owned compression and saltwater disposal systems as well as a power grid.

“That allows us to produce oil and gas as low-cost as we possibly can,” he said.

Ward believes that within the next few years, prices will begin to adjust. Even if that does not happen, Ward is making deals that he believes are profitable enough they will ensure investors, capital providers and Mach Resources will earn returns.

“That’s my goal, to make sure that we do our job so that other capital providers who have trusted us will make exceptional returns.”

It’s a tall order for any company to make such assurances. But Ward set out, far before the pandemic, to capitalize on opportunities within the upstream space.

It was a journey that began in Oklahoma, of course, where Ward was born and helped usher three previous companies into existence. By a quirk of the calendar, Mach Resources made its first Midcontinent acquisition in 2018. Within months, Alta Mesa would write down its own assets by $2 billion.

Midcon recon

After 40 years in the oil and gas industry, Ward has witnessed some wild cycles.

“The entire energy complex is going through a very difficult period of time, and the Midcontinent region is more challenged than others,” Ward said.

It’s also the sort of era that Mach Resources was built for. The company was designed to acquire distressed assets in the Midcontinent, to run lean and deliver free cash flow. The pandemic has only aggravated the symptoms that companies there have been struggling with for years.

“We find ourselves in a niche position to offer something that others really can’t provide right now,” he said. “The basic fact is there has to be a fundamental shift in how our industry operates and manages cash flow.

“Outside of large public companies, there’s little access to capital, widening debt to EBITDA ratios and a banking industry that wants out of the business.

“All of those things added together signal that there has to be a change. And that’s what we bring. We focus on being efficient.”

Ward wanted to create a company that would roll out cash while remaining ultra-efficient. Mach Resources employs what Ward calls his “SWAT team” of personnel who oversee 2,500 operated wells and interests in 5,500 wells.

“We oversee our business with 90 corporate employees and $18 million in G&A,” Ward said. With each acquisition, whether its 100 wells or 300, the goal is to hold overhead steady.

Alta Mesa’s G&A costs were roughly $40 million when Mach Resources purchased the company in April and more than $55 million in 2019.

Alta Mesa’s G&A costs were roughly $40 million when Mach Resources purchased the company in April and more than $55 million in 2019.

“That has been reduced by basically 10 times just by moving [it] into our organization,” Ward said. “By operating on a large scale we are able to reach our goal of making distributions, paying down debt and maintaining positive cash flow.”

It’s part of the reason the company stays in the Midcontinent. It’s also where Ward has maintained a presence. He knows the towns, the land and the geology. He knows Oklahoma, where he grew up in the small town of Seiling, went to college, met his wife and built billion-dollar companies.

A lifetime of insider knowledge was put to bear in Mach Resources’ first acquisition—a deal that closed in April 2018 with Ward’s former company, Chesapeake Energy.

Most of the leases Mach purchased from Chesapeake were acquired after he had left the company to start SandRidge Energy and later Tapstone Energy. Ward was with Chesapeake when the company began buying in parts of Woods, Woodward and Major counties in the Chester Formation from 1998 through 2006.

“The Miss Lime basically was developed after I left Chesapeake because the formation has a much higher water content,” Ward said. “And so really the idea around the Miss Lime was to develop that high water cut well at a time when energy prices were much higher. And so that’s what we did at SandRidge and what Chesapeake did.”

Ward said he’s comfortable with the oil play, which stretches from northern Oklahoma into Kansas and was present at the inception of horizontal drilling there.

Part of the allure of acquiring Chesapeake’s Mississippi Lime position in 2018, however, came from its readymade infrastructure.

“You have the infrastructure in place with the Chesapeake assets we were able to acquire,” Ward said. That included 500,000 bbl/d of disposal capacity.

“We don’t use all of that, even today,” he said.

Mach also hasn’t had to drill any new disposal wells and was able to put rigs to work in the play.

“It’s been a very efficient use of capital for us, to own not only the Chesapeake asset but also a couple of other assets that we purchased after that, in the Miss Lime,” he said.

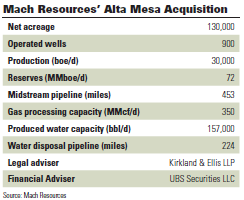

Six acquisitions later, Alta Mesa offered a similar bounty. Amid bankruptcy, Alta Mesa produced 30,000 boe/d, of which 67% was liquids. Alta Mesa also controlled 900 operated wells and 130,000 net acres, with about 90% HPB.

A price drop due to falling oil prices amid a pandemic and oil price war was a bonus. Initially, Mach Resources bid $320 million for Alta Mesa’s assets. After prices dropped, Mach walked away with the company for $100 million less.

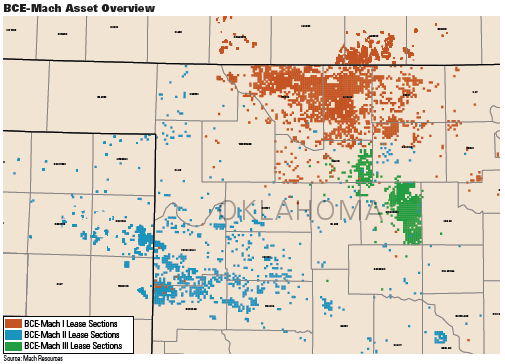

Including Alta Mesa’s acreage tucked into Mach Resources, the company has built a 500,000 net acre Midcontinent position in two years, through seven acquisitions.

More significantly, the Alta Mesa deal gave Mach Resources control of Kingfisher Midstream’s (KFM) sprawling infrastructure, including 453 miles of gas gathering pipeline, 108 miles of oil pipeline and gas processing capacity of 350 MMcf/d.

“That gives us a leg up on competition,” Ward said. “The Alta Mesa acquisition was a very efficient use of capital, and the KFM midstream system was a giant windfall for us. Much like the use of the water disposal system in our first acquisition, the midstream system allows us to minimize our expenses to create value.”

McMullen also views the Alta Mesa deal as a bargain, though the purchase was negotiated at a difficult time for WTI. A week and a half after closing the deal, oil prices sank into negative territory at about negative-$37/bbl.

“There was certainly some anxiety on our part,” McMullen said. “Our bet was simply that at $30 to $40 oil [prices], you can [generate] free cash flow … of close to $10 million a month because of the integration of the upstream and the midstream we purchased.”

Invisible upside

For all the deals Mach Resources has made, the company sticks to some basic rules of thumb. Chief among them is that assets must be purchased for a price that allows the company to make decent rates of return off production—without upside.

Cash has to roll off and back to the company and the investor.

McMullen said Mach Resources and Bayou City have been disciplined deal makers for roughly three years, carefully underwriting acquisitions to capitalize on new assets.

“We have very low leverage across our assets,” McMullen said, adding he expects to have net zero debt by the end of the year on the recently purchased AMR assets.

“There are a lot of distressed operators out there, and we want to be nimble and move quickly on those opportunities,” McMullen said.

Disregarding future growth forces the company to game out how deals will pay for themselves.

“We have always had a model of making distributions. We have cash on cash returns after debt service after capex, and we make distributions to our investor,” Ward said. “But the only way to do that is to buy at a price that only values the reserves that are producing.”

Drilling isn’t out of the question, if it can be done at a discount. Alta Mesa’s assets include what Ward described as a large area that hasn’t been depleted. The company had two rigs running consistently until February, when prices dropped.

Significant well results aren’t the company’s aim, however. The company instead touts the 40% reduction in drilling and completion costs from early 2019 to early 2020.

Mach has completed two DUCs and has a few more in its inventory it may experiment with. But for now, the company has paused further drilling to focus on expansion through acquisition.

At higher prices, Mach Resources might put out a rig, but it will be stingy with any capex. The company may put one or two rigs back to work next year. But Ward reiterates that growth is not the answer to the industry’s current misery.

“We’ll be working in very highly selective areas that we don’t feel will have the competition or depletion from other areas,” he said.

Ward does see an eventual rebalancing of the oil and gas markets. While he believes the industry needs $50 oil to survive, he doubts investors will return until prices rise substantially. However, factoring in OPEC, world demand and other areas makes the calculation difficult. An easier equation is to solve for natural gas.

Ward has previously been critical of moves made by Chesapeake into the Haynesville Shale. And the commodity has been the bane of many producers. But the numbers are hard to ignore.

In 2010, the U.S. produced 55 Bcf/d of natural gas. Today, natural gas production is down slightly to 89 Bcf/d after peaking last year at 92.21 Bcf/d, according to the U.S. Energy Information Administration (EIA). EIA projects that in 2021, production will fall to 86.59 Bcf/d.

“Gas has been a hated asset for more than a decade,” Ward said. But over the next five years, demand for natural gas will rise somewhere between 10 Bcf/d and 15 Bcf/d.

“We’re really losing about a Bcf a day per month, and our demand continues to move up,” Ward said.

Even adding 200 more rigs in the Permian, a doubling of Haynesville rigs and a doubling of the Northeast rigs by 2021, Ward said the U.S. might maintain production in the 80 Bcf/d to 83 Bcf/d range.

“I don’t know how and where you are going to find that capital today,” he said. “It’s just a very interesting time to be looking at natural gas.”

Mach Resources commodity of choice remains oil. But the company’s Midcontinent assets necessarily mean a lot of gas production. The company averages 58,000 boe/d of production, including roughly 30% oil and 30% natural gas.

Ward also expects Mach Resources to continue to acquire assets largely by searching for the best pieces among the wreckage of the oil and gas industry.

“Ultimately what you’re seeing is that in each deal that we’ve looked at, there’s been billions of dollars [in value] wiped away,” Ward said. “The equity is obviously gone. The second liens are basically gone. The companies are moving toward bankruptcy, and there has to be some type of consolidation or sale.”

For Mach Resources, each deal is examined through in the same strategic light: that the company will operate them “as if it will be the last owner.”

“I do believe good can come out of this. New investors can come,” he said. “We’re in a time period that you need to be prepared to own these assets. And own them through depletion.”

SIDEBAR:

ROAD OF HUMILITY

Whether he would consciously admit it or not, Ward is, and remains, a pioneer of the Oklahoma oil and gas story and the shale revolution.

Ward said he started out just wanting a job. In 1982, Ward was unemployed for a couple of months and did farm work for a family outside of Clinton, Okla., working in the fields.

“I really didn’t care to cut wheat the rest of my life,” Ward said.

With help from investors, he started an oil and gas business in 1982 to buy distressed assets. His premise: In a time of no capital, a little bit of money and an idea can be a powerful combination.

“You can make a way. You can make a living. That’s all I was trying to do, was make a living,” he said.

Ward said he never anticipated doing any of the things he’s accomplished.

“There’s nothing really special about me. Other than I associate myself with very smart, good people,” he said.

About that time, he met a man named Aubrey McClendon, who had hit upon the same strategy of buying distressed oil and gas assets inexpensively.

“We were the only two at our age group … and we were competing with each other,” he said.

So the two decided to team up, later forming Chesapeake Energy Corp.

More than four years after McClendon’s death, Ward sees his friend as a visionary that has been wrongly vilified, particularly in the press.

“I don’t think he gets enough credit for leaving a company that had $35 billion worth of enterprise value when he left. And we started it with a meager amount,” Ward said. “He did more things for our industry than anyone else in history, that I know of.”

Ward’s assessment of his own legacy is free of any superlatives.

“I have never really dwelt on legacy. If the company continues to operate on what we call the ‘road of humility,’ where we put the good of one another ahead of self-interest, commit to making things better than the day before, learn to be content in all situations and serve those that are less fortunate we can look back at what we have accomplished and be pleased.”

Recommended Reading

Chevron Hunts Upside for Oil Recovery, D&C Savings with Permian Pilots

2024-02-06 - New techniques and technologies being piloted by Chevron in the Permian Basin are improving drilling and completed cycle times. Executives at the California-based major hope to eventually improve overall resource recovery from its shale portfolio.

Pitts: Heavyweight Battle Brewing Between US Supermajors in South America

2024-04-09 - Exxon Mobil took the first swing in defense of its right of first refusal for Hess' interest in Guyana's Stabroek Block, but Chevron isn't backing down.

Exxon Versus Chevron: The Fight for Hess’ 30% Guyana Interest

2024-03-04 - Chevron's plan to buy Hess Corp. and assume a 30% foothold in Guyana has been complicated by Exxon Mobil and CNOOC's claims that they have the right of first refusal for the interest.

NAPE: Chevron’s Chris Powers Talks Traditional Oil, Gas Role in CCUS

2024-02-12 - Policy, innovation and partnership are among the areas needed to help grow the emerging CCUS sector, a Chevron executive said.

Exxon Ups Mammoth Offshore Guyana Production by Another 100,000 bbl/d

2024-04-15 - Exxon Mobil, which took a final investment decision on its Whiptail development on April 12, now estimates its six offshore Guyana projects will average gross production of 1.3 MMbbl/d by 2027.