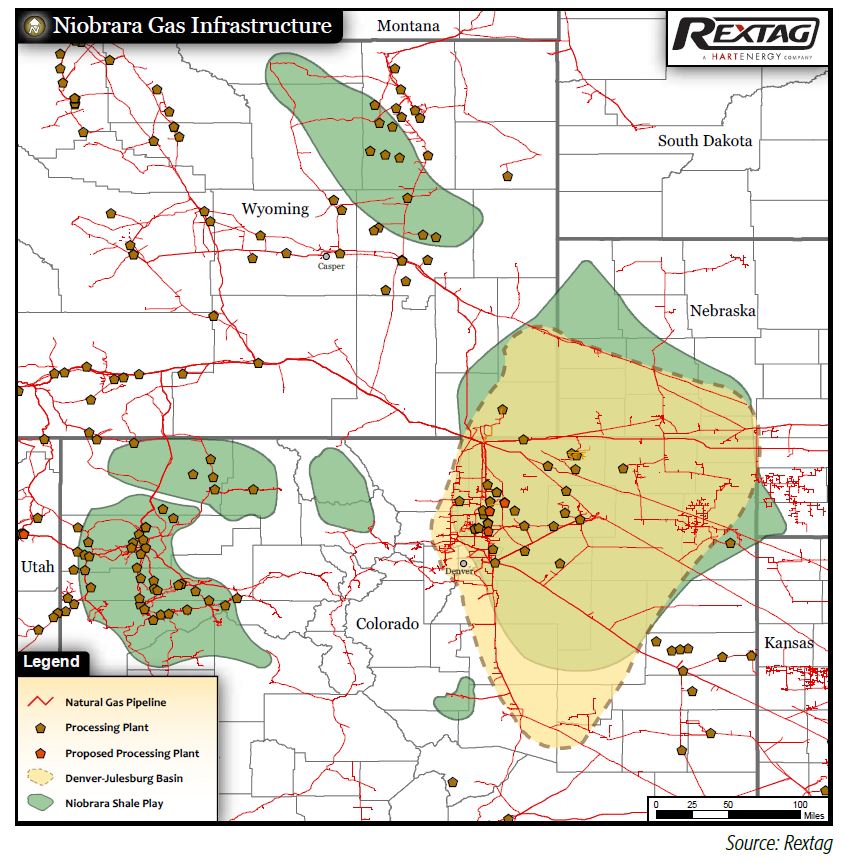

The big Rockies play has reawakened with a focus on the Denver-Julesburg Basin.

A snoozing energy executive stuck in a window seat, flying into Denver’s airport, might be forgiven if he or she suddenly jolts awake as a flight attendant starts the “place your seatbacks and tray tables in their full, upright and locked positions as we prepare to land” routine.

Huh? Who? What? Where are we?

A glance out the window: It’s open country down there, pool-table flat, a busy piece of the oil patch. Look! Lease roads to large well pads with nodding pumpjacks, tank batteries, compressor stations—and over there is a large gas plant with a lazy flare.

This must be West Texas! We made it to Midland!

A good guess for a sleep-fogged mind. But then the plane banks in for the final approach as the landing gear clunks into place: Oh, mountains.

That’s the Denver-Julesburg (D-J) Basin down there, not the Permian Basin.

The two basins rank among the biggest players in the industry’s shale revival and both are wide awake now, thank you, after a couple of sleepy years following the 2014 oil price crash. And much like its big brother far to the south, the D-J now faces midstream capacity challenges as things perk up.

Trends and changes

The D-J increasingly is a liquids play. The lines on the U.S. Energy Information Administration’s (EIA) production charts for Niobrara oil and gas were headed northeast as 2018 began. Estimated gas production for February was 4.88 billion cubic feet per day (Bcf/d), up nicely from four years ago but still shy of January 2012 when the Niobrara briefly topped 5 Bcf/d.

On the other hand, the EIA projected that oil would set a new record of 556,000 barrels per day (Mbbl/d) in February. Niobrara liquids output reached a 491 Mbbl/d pinnacle in 2015 before sliding back to a 402 Mbbl/d low in January 2017.

Hart Energy’s Stratas Advisors placed the Niobrara squarely in its list of “key contributors” to the nation’s climbing oil output in a January review of North America’s unconventional plays. It estimated that total Rockies production will rise to 1.489 million barrels of oil equivalent per day (MMboe/d) by the end of this year—a 17% increase from mid-2017 levels.

“There’s still a tremendous amount of gas coming out of the basin; it’s not one or the other,” Brian Frederick, president of asset operations for Denver-based DCP Midstream, told Midstream Business. “All of the associated gas coming off a well is where we focus our efforts. Yes, it is a big liquids play.”

Wells Fargo Senior Analyst Michael Blum’s “Basin Book,” released in February, had lots to say about midstream constraints in the Niobrara. The analysis noted existing NGL takeaway capacity should become full by the second half of 2018 and that the D-J may need as much as 200 Mbbl/d of additional gas liquids capacity in the near future.

For crude oil, “We estimate that the Niobrara has meaningful excess capacity through 2023; specifically, we project total crude supply of 1.14 [million barrels per day] MMbbl/d by 2023 (estimated), compared with existing takeaway of 1.33 MMbbl/d,” Blum said. “In the near term, excess takeaway capacity represents a risk to upcoming contract expirations in 2019-2020. This could be a negative for SemGroup Corp., as White Cliffs [Pipeline] contracts roll off in the next 18-24 months. However, given increasing production in the region (i.e., Platts has revised its projections by an average of 7%) and if White Cliffs repurposes 125 Mbbl/d of capacity, we believe takeaway could become constrained by 2021. This is a long-term potential positive for all midstream companies with pipeline assets.”

He listed NGL Energy Partners, Magellan Midstream, SemGroup, Spectra Energy and Tallgrass Energy as Niobrara “winners.”

Oil, sort of

“The Rocky Mountains region is a significant producer of natural gas, although natural gas production has been declining in recent years as high oil prices and recent drilling success in the Niobrara formation have steered producers toward oil production,” the EIA said in a recent study. “The distribution of Rocky Mountains crude oil production reflects this, showing a relatively stable percentage of API [gravity] 50+ production, where API 50+ production is commonly produced from wells targeting natural gas.”

That’s pretty light stuff. By comparison, the industry’s benchmark West Texas Intermediate has a standard API gravity of 39.6. So that means lots of condensate and NGL to pull out of very wet gas streams.

E&Ps plan to grow production in the D-J’s Wattenberg Field thanks to several recent transactions. Producers in northeastern Colorado’s Weld County are optimistic, citing high-return Niobrara and Codell formation wells supported by rising commodity prices and thus, they seek more of a good thing. Several companies have made bolt-on acquisitions and many are making acreage trades in the Wattenberg. Through these transactions that enable longer laterals or extended-reach wells (XRLs) to be drilled, they have positioned themselves for great production growth in 2018.

Since 2016, producers in the D-J have closed on nearly $2 billion of deals (not counting SandRidge Energy Inc.’s recently abandoned plan to merge with Denver-based Bonanza Creek Energy Inc. for $746 million).

Extraction Oil & Gas Inc. (XOG) has spent $333 million buying greater access to the D-J since the beginning of 2016. It has the best risk-reward in the basin, according to analysts at Tudor, Pickering, Holt & Co. “Beyond capex risk, XOG has successfully managed basin-wide themes that have kept D-J E&Ps at discounts: DCP Midstream LP (its diversified acreage position allows planning around DCP plant startups; it has just one DCP-exposed pad in each of 2018 and 2019), and regulatory risk (rhetoric is improving…),” the analysts said in a report.

For each of these buyers, XRLs of 7,500 feet (ft)-10,000 ft have become the norm.

Coupled with more intense fracking, they have led to a surge in production, but area gas processing and gathering line pressures cannot handle the incremental output—yet. Waiting on the midstream infrastructure to catch up is their biggest immediate hurdle. The greater Wattenberg Field yields anywhere from 35% -65% oil depending on location. NGL and natural gas are plentiful.

Processing capacity

D-J midstream operators are well aware of the needs and are moving rapidly to fill them, agreed Brandon Cowart, director of business development for SemGroup.

“The biggest need right now is to get gas processing capacity online in the near term, that’s the major near-term constraint,” Cowart said. Midstream operators have announced 1.2 Bcf/d of new processing capacity scheduled to come on in 2018 and 2019, he noted.

“Those projects should alleviate most, if not all, of those constraints. And of course, when you have that much new gas processing capacity the next constraint will be NGL takeaway. So we believe the D-J Basin could support several expansion opportunities.”

A drowsy D-J woke up to smell the coffee last year, he said.

“Recovery in the basin really started to show signs in 2017,” Cowart added. “D-J production, which we’re directly exposed to, was up approximately 23%, and we saw about a 20% increase out of [Wyoming’s] Powder River Basin, while the rest of the Niobrara region remained flat.

“We’re anticipating this trend to continue into 2018 when we’re expecting to see upper-single-digit to lower-double-digit growth in the basin,” he continued. “The timing of this growth may become constrained as gas processing and NGL takeaway capacity reach their limits in the latter half of 2018 and early 2019. However, we expect those capacity issues to be addressed by mid-2019 and anticipate production growth to continue to increase at a fairly good clip through 2023.”

Frederick sees the same challenge.

“The D-J Basin has seen tremendous activity; the producers have been really, really successful. The economics of the D-J stack up against almost any play in America. There are a lot of good things happening there; our systems are setting records almost every month; the volumes in the D-J just continue to grow.

“We are in a place where we are adding processing capacity,” he added. “We are currently constructing our Mewbourn 3 plant, which will be ready in third-quarter 2018 to be followed by our O’Connor 2 plant in mid-2019. Right now, [processing] is the biggest need in the basin. When you look at any overall play, you’ve got to have the gathering systems, the processing systems, and then the takeaway of the gas, the NGL and the oil. And now, it’s the processing that needs the most expansion.

“We are in discussions with our producers about adding additional processing capacity after that and what the timing should be. We are very much partners with the producers. All of their drilling plans and all of our buildout plans for the infrastructure are all very integrated together. We know their plans and they know our plans. The question is how to we build this out together?” Frederick said.

Combined, the plants will nearly double DCP’s current capacity of 850 MMcf/d in the Wattenberg and give the firm 11 processing plants in the basin.

Discovery Midstream, Rimrock Energy Partners, Cureton Midstream and Sterling Energy are also reportedly expanding midstream facilities or planning to get more active, Seaport Global Securities analyst Mike Kelly said. “Net-net, while infrastructure-related headwinds could remain pervasive in the short term, we see prospects improving materially for D-J players … starting in [third-quarter 2018] as various midstream projects start coming online.”

Anadarko Petroleum Corp.’s Western Gas Partners midstream unit is another big D-J player and has plans to grow its assets. It expects to put twin, 200 MMcf/d trains online at its Latham plant in 2019 to serve its parent’s production. An expanded gathering system will flow to the plant.

Anadarko and joint-venture (JV) partners DCP and Enterprise Products Partners LP seek to expand their Front Range Pipeline that moves NGL out of the D-J to the Skellytown, Texas, gas liquids hub. Current capacity of 150 Mbbl/d can be increased to 230 Mbbl/d. Also in consideration: A new residue gas line.

All of that new gathering and processing capacity could further reduce drilled but uncompleted (DUC) Niobrara wells. The EIA reported that producers worked off 23 DUC wells targeting the formation in the final month of 2017, but that still left 577 DUCs sitting on the Niobrara pond.

Regulatory questions

This is all good news for many people, but investors have been skittish about D-J operations due to Colorado’s underlying regulatory threats, which might dampen activity.

In February, the Colorado Supreme Court agreed to review an appeals court’s ruling on the role of the Colorado Oil & Gas Conservation Commission that regulates the basin. Meanwhile, municipalities and environmental groups along the populous Front Range continue to insist they can ban drilling within their borders and stop fracking activity altogether.

Despite these possible setbacks and delays, operators are pressing ahead, propped up by lower drilling and completion costs and the rich rewards found in the Niobrara, and the Codell, in the D-J. Estimates by Jefferies & Co. in an early 2018 report contend that internal rates of return (IRRs) in the Wattenberg Field range from 62% for Tier 1 wet gas in the Codell Formation and 51% in the wet gas of the Niobrara, to 47% for Codell in the oil core, to 35% in the oil core of the Niobrara.

PDC Energy Inc. is one of the more active D-J producers and it, too, has made acquisitions and acreage trades in the past two years, most recently closing a deal in January. But midstream limitations are a concern for it, too.

“We lowered our 2017 production guidance back in August 2017” due to gathering line pressure constraints, said Michael Edwards, PDC’s senior director of investor relations. The company was testing tighter frack spacing of 140 ft between stages, but it’s stopped those tests for now due to the midstream constraints, which could prevent the wells from being turned to sales in a timely manner, skewing data.

Think local

The Rockies present producers and their midstream counterparts with a problem: It’s a long ways to big markets. Major cities in the region include Denver, Salt Lake City—and, well, that’s it. But having the Niobrara in their backyard has been a boon for the region’s long-suffering refiners, who once had to ship imported crude feedstocks from faraway Canada and Gulf Coast ports. That’s not the case anymore.

“Refiners in the five Rocky Mountain states that make up the EIA’s Petroleum Administration for Defense District IV—or PADD IV—enjoy higher margins than their counterparts in every other part of the country except California,” RBN Energy noted in a recent analysis. “Quarterly crack spreads for domestic crude in PADD IV averaged $25/bbl between 2014 and 2017, while those for Canadian crude averaged $31/bbl.” Those “lofty cracks” reflect an abundance of nearby feedstock, coupled with traditionally higher-than-average gasoline and diesel prices at the pump, RBN added.

“With liquids prices increasing, I think that’s helping producers out on their returns,” Cowart said. “With crude prices returning into the 50s and the support that provides NGL prices, and with gas prices where they’re at, we’re seeing strong economics.”

“Currently, ethane in the basin is being reinjected back into the gas stream, where producers are realizing a natural gas price for that molecule,” he added. “Producers could see additional financial incentive if ethane prices strengthen and begin to be recovered in the basin.”

NGL capacity

ONEOK Inc. announced plans as 2018 began for the $1.2 billion Elk Creek Pipeline to haul NGL south to its extensive Midcontinent gas liquids facilities. The 900-mile, 20-inch line will start in the Williston Basin in Richland County, Mont.—serving Bakken producers—and extend through Wyoming and into Colorado where it will pick up Powder River and D-J production.

Capacity will be 240 Mbbl/d of Y-grade. Related infrastructure will cost an additional $200 million, with completion scheduled for the end of 2019.

“The existing Bakken NGL and Overland Pass Pipelines are operating at full capacity. Additional NGL takeaway capacity is critical to meeting the needs of producers who are increasing production and are required to meet natural gas capture targets in the Williston Basin," said Terry Spencer, ONEOK president and CEO. “The Elk Creek Pipeline will strengthen ONEOK’s position in the high-production areas of the Bakken, Powder River and Denver-Julesburg regions and also provide additional reliability and redundancy on our NGL system.”

Elk Creek is anchored by long-term contracts with terms ranging between 10 -15 years totaling about 100 Mbbl/d.

Gas capacity

Western Gas isn’t the only midstream player looking to handle the growing residue gas volumes. Tallgrass Energy recently announced a binding open season for its proposed Cheyenne Connector Pipeline that will move gas northward out of the D-J to the Cheyenne gas pipeline and storage hub in Weld County, Colo., just south of the Wyoming-Colorado border. The 70-mile pipeline will provide direct connections to Tallgrass’ Rockies Express (REX) system and other interstate gas transmission pipelines.

The project has an anticipated capacity of 600 MMcf/d or more. Tallgrass said two bidders already have committed for capacity. It will be operated as a separate interstate pipeline with its own tariff, Tallgrass said. The target in-service date is third-quarter 2019.

“Separately, REX is developing the Cheyenne Hub Enhancement Project to enhance the firm interconnectivity capability of the various pipelines and local distribution systems located in and around the Cheyenne Hub,” the company said in a statement. “The delivery to the REX Cheyenne Hub and the anticipated transformation of the REX hub facilities will provide customers significant diversity in terms of market access.”

Powder River

The Rockies sport multiple pays in addition to the Late Cretaceous Niobrara, which produces not only in northeastern Colorado’s D-J, but Wyoming’s Powder River and western Colorado’s Piceance. The other Niobrara hot spot is Wyoming’s Powder River Basin.

Crestwood Equity Partners told analysts at the recent UBS Midstream & MLP Conference that volumes flowing through its Powder River operations increased 43% in 2017, while customer Chesapeake Energy Corp. ran three rigs. Chesapeake expects to run four rigs most of this year to keep the growth momentum going, it added.

Crestwood and The Williams Cos. have a 50:50 JV in the Powder River Basin’s Jackalope system, which includes a 180 million-cubic-feet-per-day (MMcf/d) gas gathering system and a 120 MMcf/d processing plant in Converse County, Wyo. Crestwood told analysts there is the potential to grow production to more than 100 Mboe/d within five to seven years. Jackalope has 388,000 dedicated acres with 2,600 drilling locations targeting the Niobrara and four other zones.

Tallgrass also is active in the Powder River Basin. It and Silver Creek Midstream LLC announced plans to develop the Iron Horse Pipeline, a JV to transport crude from the Powder River to Guernsey, Wyo. Iron Horse will connect there with Silver Creek’s developing gathering system to the Tallgrass Guernsey Terminal, currently under construction, and then to Tallgrass’ Pony Express crude line and other oil pipes.

Iron Horse and Pony Express intend to create a joint tariff to offer producers and marketers a single rate and direct access to the multiple refineries on Pony Express and to Cushing, Okla. Iron Horse will likely enter service in first-quarter 2019 with an initial capacity of about 100 Mbbl/d “with significant available expansion capacity,” the firm said in a statement.

Let’s make a deal

It’s not a surprise that with an active basin like the D-J that midstream M&A deals are beginning to pop up, right along with the E&Ps’. At year-end 2017, Noble Midstream Partners and Greenfield Midstream announced a JV to acquire the basin’s Saddle Butte pipeline system for $625 million. Saddle Butte provides a variety of gathering services for oil, gas, NGL and produced water. That includes limited gas processing services to meet pipeline specifications.

Assets include about 160 miles of pipeline in operation, 300 Mbbl/d of delivery capacity and 210 Mbbl of crude storage. It serves 115,000 acres dedicated by six producers for fixed-fee services.

DCP’s Frederick discussed the firm’s sprawling operations—the firm is a perennial top performer in the annual Midstream Business survey of gas processors and NGL producers. And the D-J ranks right up there with the other big shale plays, in his opinion.

“We pay a lot of attention to how the plays stack up next to each other from an E&P standpoint. The best plays are where the drilling happens and where we need to focus our efforts. Clearly, the Permian, the D-J and the Scoop/Stack are the three premier basins in the country right now.”

SemGroup’s Cowart also is very positive about the D-J’s future. The basin has large producers and delineated areas “that can be exploited in a sustainable, manufacturing manner,” he said. “The D-J and Niobrara are key components in our overall strategy. We will continue to evaluate and chase incremental projects—opportunities that will allow us to extend our existing asset base.

“Activity in the D-J, where we have a lot of visibility, remains strong. We see producers able to achieve more with less. They have become very efficient with their drilling programs,” Cowart added. “It’s a strong basin with strong economics. We’re excited to be there.”

Paul Hart can be reached at pdhart@hartenergy.com or 713-260-6427. Leslie Haines can be reached at lhaines@hartenergy.com or 713-260-6428.

Recommended Reading

Marketed: BKV Chelsea 214 Well Package in Marcellus Shale

2024-04-18 - BKV Chelsea has retained EnergyNet for the sale of a 214 non-operated well package in Bradford, Lycoming, Sullivan, Susquehanna, Tioga and Wyoming counties, Pennsylvania.

Triangle Energy, JV Set to Drill in North Perth Basin

2024-04-18 - The Booth-1 prospect is planned to be the first well in the joint venture’s —Triangle Energy, Strike Energy and New Zealand Oil and Gas — upcoming drilling campaign.

PGS, TGS Merger Clears Norwegian Authorities, UK Still Reviewing

2024-04-17 - Energy data companies PGS and TGS said their merger has received approval by Norwegian authorities and remains under review by the U.K. Competition Market Authority.

Energy Systems Group, PacificWest Solutions to Merge

2024-04-17 - Energy Systems Group and PacificWest Solutions are expanding their infrastructure and energy services offerings with the merger of the two companies.

Chevron, Exxon in Dispute Over Hess Stake in Guyana Oil Block

2024-02-27 - Chevron’s $53 billion deal to buy Hess’ interests in the Stabroek Block offshore Guyana could be derailed as Exxon, CNOOC say they have first rights of refusal on the block’s interests.