RED President Steve Hendrickson looks at the recent volatility in natural gas prices and what the future might hold for the commodity. (Source: Shutterstock.com)

This is an excerpt from the Ralph E. Davis Associates (RED) Weekly E&P Update Newsletter.

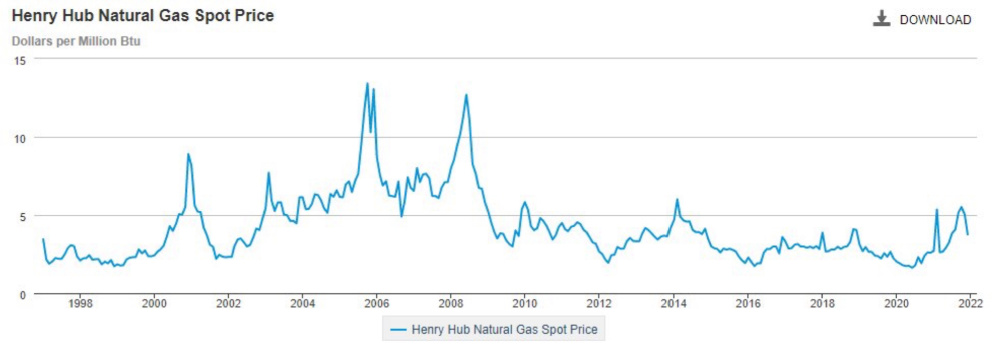

Just over two months ago we were entering the winter heating season enjoying the highest U.S. natural gas prices in almost eight years. Demand was strengthening as the economy continued to recover, exports were humming and although rig counts were higher, natural gas producers had, for the most part, maintained capital discipline and resisted the urge to overdrill.

By the end of the year, however, natural gas spot and futures prices had fallen significantly. What happened?

Overproduction doesn’t seem to be the culprit. Although U.S. natural gas production has increased steadily since the demand drop at the start of the pandemic, the annual average has been consistent over the last three years.

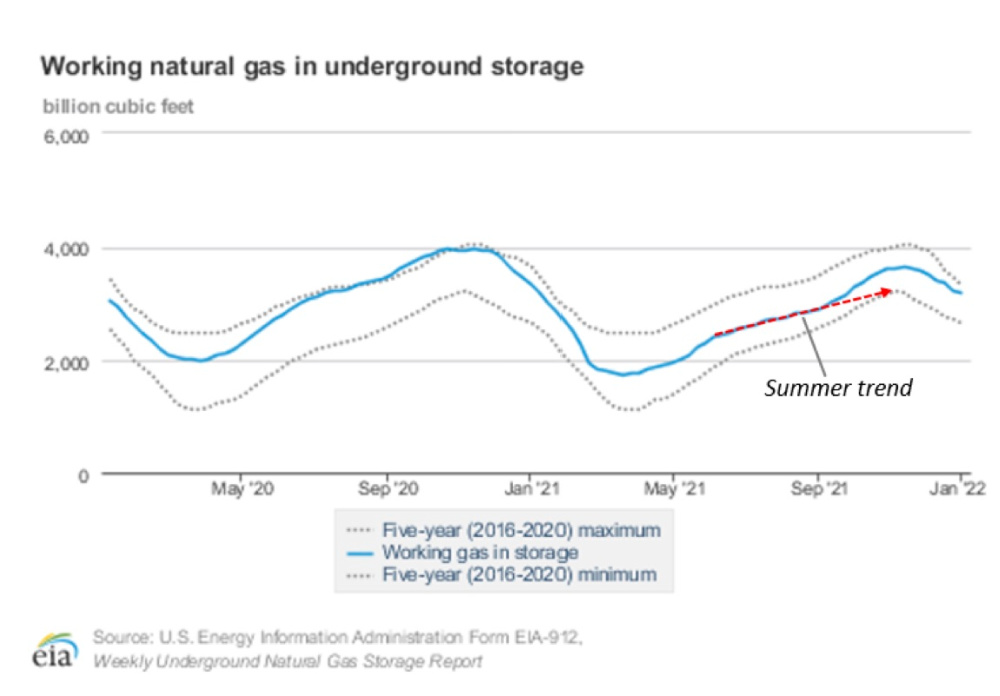

Looking back at working gas in storage, we can see that we were on a trajectory to enter the heating season near the five-year low. In October, the trend changed, however. Production did increase slightly during this period, but the big story was the surprisingly mild weather we experienced in the last three months of the year. If you live in Texas, you know exactly what I’m talking about. According to the Texas State Climatologist, in 2021, we experienced what was probably the warmest December since at least 1989.

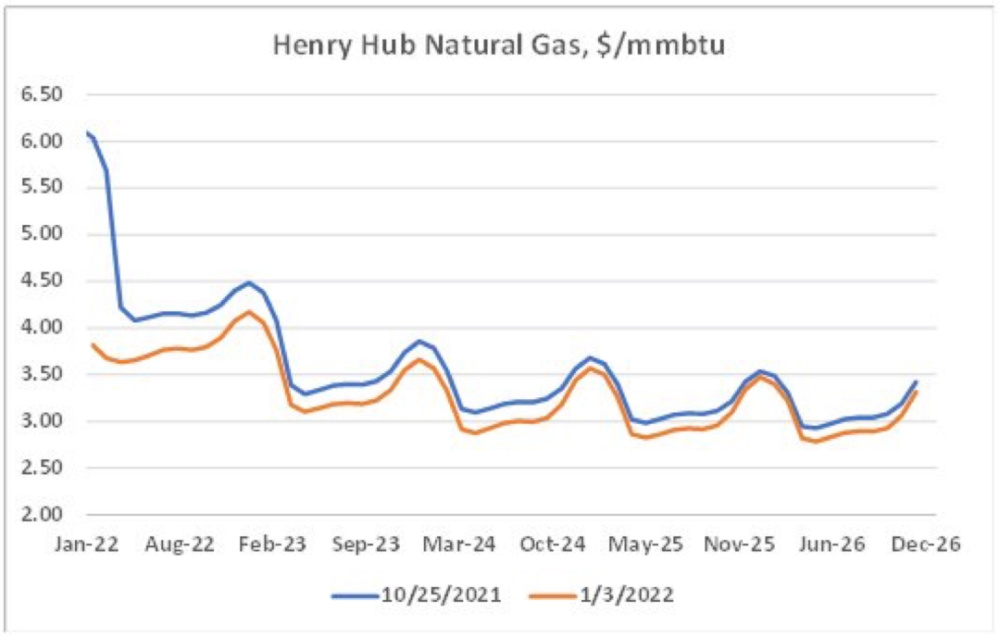

On the bright side, Natural Gas Intelligence reported this week that factors may be lining up for higher prices before the winter is over. Production has dipped recently, and the latest weather models indicate the U.S. may get a cold blast of Canadian air near the end of the month (hopefully not as cold as last year!). February future prices closed above $4/MMBtu on Jan. 10 (about 8% higher than where we were a week ago), and there’s a good chance that we’ll exit the heating season with storage near the five-year average rather than the five-year high.

About the Author:

Steve Hendrickson is the president of Ralph E. Davis Associates, an Opportune LLP company. Hendrickson has over 30 years of professional leadership experience in the energy industry with a proven track record of adding value through acquisitions, development and operations. In addition, he possesses extensive knowledge of petroleum economics, energy finance, reserves reporting and data management, and has deep expertise in reservoir engineering, production engineering and technical evaluations. Hendrickson is a licensed professional engineer in the state of Texas and holds an M.S. in Finance from the University of Houston and a B.S. in Chemical Engineering from The University of Texas at Austin. He recently served as a board member of the Society of Petroleum Evaluation Engineers and is a registered FINRA representative.

Recommended Reading

US Interior Department Releases Offshore Wind Lease Schedule

2024-04-24 - The U.S. Interior Department’s schedule includes up to a dozen lease sales through 2028 for offshore wind, compared to three for oil and gas lease sales through 2029.

Utah’s Ute Tribe Demands FTC Allow XCL-Altamont Deal

2024-04-24 - More than 90% of the Utah Ute tribe’s income is from energy development on its 4.5-million-acre reservation and the tribe says XCL Resources’ bid to buy Altamont Energy shouldn’t be blocked.

Mexico Presidential Hopeful Sheinbaum Emphasizes Energy Sovereignty

2024-04-24 - Claudia Sheinbaum, vying to becoming Mexico’s next president this summer, says she isn’t in favor of an absolute privatization of the energy sector but she isn’t against private investments either.

Venture Global Gets FERC Nod to Process Gas for LNG

2024-04-23 - Venture Global’s massive export terminal will change natural gas flows across the Gulf of Mexico but its Plaquemines LNG export terminal may still be years away from delivering LNG to long-term customers.

US EPA Expected to Drop Hydrogen from Power Plant Rule, Sources Say

2024-04-22 - The move reflects skepticism within the U.S. government that the technology will develop quickly enough to become a significant tool to decarbonize the electricity industry.