What’s gone largely unnoticed in the recent angst over global recessionary fears are some of the very positive changes undertaken by the sector to make midstream players more attractive to investors, including those looking for yield. (Source: Hart Energy/Shutterstock.com)

[Editor's note: A version of this story appears in the October 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The recent stock market disdain for seemingly all things energy has left midstream securities less scarred than their E&P cousins, but, nonetheless, badly bruised. However, what’s gone largely unnoticed in the recent angst over global recessionary fears are some of the very positive changes undertaken by the sector to make midstream players more attractive to investors, including those looking for yield.

Confusing corporate structures and incentives that did little to align the interests of managements and investors, such as incentive distribution rights, have gone out the door. Instead, midstream strategies aim to be self-funding, with reduced capex and little or no equity issuance and management incentives based on returns rather than growth, said Pearce Hammond, senior research analyst with Simmons Energy.

The result has been that, “overall, the midstream companies have better distribution coverage, lower leverage and less reliance on equity markets than they did a few years ago,” he observed.

midstream

companies have

better distribution

coverage, lower

leverage and less

reliance on equity

markets than they

did a few years

ago,” observed

Pearce Hammond,

senior research

analyst with

Simmons Energy.

In addition, in the event that construction of new energy infrastructure faces ongoing obstacles, due to “keep it in the ground” opposition, those midstream companies that already have large established infrastructure should see their assets grow in value, said Hammond. Recreating large legacy assets positions would be “very difficult” given what are “essentially closed” capital markets, he added.

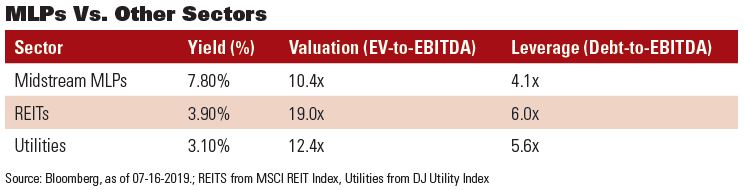

For those looking for income, there is a yawning gap between yields offered by the midstream sector and competing sectors, notably real estate investment trusts (REIT) and utilities, Hammond pointed out. For example, the midstream MLP group offers yields averaging 7.8% as compared to 3.9% and 3.1%, respectively, for REITs and utilities on average.

Midstream metrics

Moreover, midstream sector participants tend to trade at lower valuations and carry less leverage than REITs and utilities. The midstream sector trades at an enterprise value-to-EBITDA (EV-to-EBITDA) of 10.4 times, on average, with debt-to-EBITDA of 4.1 times. This compares to EV-to-EBITDA valuations of 19 times and 12.4 times for REITs and utilities, respectively, with debt-to-EBITDA of 6 times and 5.6 times.

If investors “dispassionately examined the quality and consistency of midstream cash flows,” without focusing on cash flows coming from the energy sector, “investors might be willing to pay up for the higher yields,” offered Hammond. Over time, the discounted valuations, return of cash to investors and attractive risk-reward proposition should help drive interest in the sector, he said.

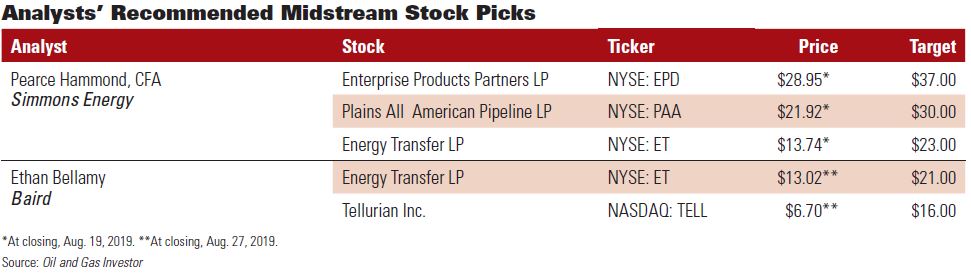

Against an energy tape that has been less than friendly—to say the least—Hammond pointed to three midstream names he believed would run ahead of the pack and make money for investors.

At the top of his list is Enterprise Products Partners LP, followed by Plains All American Pipeline LP and Energy Transfer LP. If the first two recommended stocks hit their target prices, they would both offer over 30% returns, before dividends. The third, Energy Transfer, has been trading cheap to its peers on valuation and, with a rerating, would offer upside of well over 50% if it reached its target.

All three recommendations by Hammond have continued to operate as MLPs rather then switch to become C corps, as, for example, Kinder Morgan Inc. and several others have elected to do.

Hammond has a target price for Enterprise Products Partners of $37 per share. This compares to a price of $27.92 per share when he initiated coverage of the midstream sector. Hammond is quick to emphasize that Enterprise is his top recommendation.

Wellhead to water

“I really think it’s the top company I cover,” he said. “Enterprise has a very advantageous position. They have a great set of assets. They touch the molecules from wellhead to water. They’re a first mover on this VLCC offshore terminal to be built off Freeport. There’s a real advantage if they can be the first, because there is a number of proposals, and they won’t all get built. The trick is to get there first.”

The series of assets built by Enterprise exemplifies a “classic toll road mentality,” observed Hammond. “We like the toll road approach whereby a midstream company collects a fee at each stage of the process” of its operations, he continued. “Enterprise can essentially offer a solution from wellhead to the water. The end-to-end solution is critical in maximizing producer netbacks.”

“We like the toll road approach whereby a midstream company collects a fee at each stage of the process of its operations.”

—Pearce Hammond, Simmons Energy

As an example, Hammond pointed to the ability of Enterprise to collect fees at each of these steps: gathering the gas; processing the gas; transporting the NGL Y-grade stream to Mont Belvieu; fractionating Y-grade into purity products; and storing the purity product. If export markets are involved, fees can then also be collected for transporting to a dock and shipping overseas.

Leader in exports

Enterprise is a leader in the export market, holding “the No. 1 position in oil and No. 1 in liquefied petroleum gas [LPG] exports,” according to Hammond. The company is estimated to handle through its terminals about half of all LPG exported from the U.S. Compared to the earlier stages in midstream operations, it “wants to play where there is less competition,” he commented.

The Sea Port Oil Terminal, called SPOT, is one such project likely to enjoy an advantage due to few competing offshore terminals. The facility is designed to load one very large crude carrier per day. Plans call for constructing a 50-mile pipeline from the company’s ECHO storage facility south of Houston to Freeport, with two 36-inch diameter lines then extending offshore to the SPOT terminal.

“You’ll probably get better rates [from SPOT], because there’s likely less competition,” said Hammond.

The company already has existing export capacity amounting to about 5 million barrels per day (MMbbl/d). This breaks down to about 1.4 MMbbl/d for crude exports and 3.3. MMbbl/d for crude or LPG, with the balance used for ethane. It has 18 deepwater docks spread between the Houston Ship Channel, Beaumont, Freeport/Texas City and Morgan’s Point.

Enterprise has a record of 10 consecutive years of distribution growth. Distribution coverage is a solid 1.7 times, as of the first quarter, with a 6% distribution yield and projected growth in the distribution of 2.3% this year. The free-cash-flow yield is estimated at 4.3% in 2019 and 5.2% in 2020, according to Hammond, while return on invested capital is estimated at 15% this year.

‘Superb’ management team

The Enterprise management team is described by Hammond as “superb.” The chairman of the board is a member of the Duncan family, which collectively owns roughly 30% of the units. The $37 target price is based on a “premium” multiple of 13 times 2020 EBITDA, which Hammond said is justified by “the quality of Enterprise’s businesses and management.”

Hammond has a target price for Plains All American LP of $30 per share, which is based on a 12 multiple of 2020 EBITDA. Plains is well-positioned in the Permian Basin, which is “the primary growth engine for U.S. hydrocarbons,” noted Hammond. Not surprisingly, Plains is a sponsor of several key Permian projects, including the Cactus II and Wink-to-Webster pipelines.

As of its second-quarter results, Plains indicated Cactus II was mechanically complete from Wink to Ingleside, with partial service that was due to begin in mid-August and full service in the first quarter of 2020. The Wink-to-Webster project is targeting an in-service date of early 2021. Capacity is put at 1 to 1.5 MMbbl/d. Other sponsors are Exxon Mobil Corp., MPLX LP, Delek US Holdings Inc. and Rattler Midstream LP.

Plains provides access to multiple end markets for its customers, including St. James, La., and Nederland, Houston and Corpus Christi in Texas. As an example, the Cactus II pipeline is designed to connect to docks in Corpus Christi used by Buckeye Partners LP and physical commodity trader Trafigura, as well as NuStar Energy LP. The Wink-to-Webster project will be able to connect to docks in Beaumont.

valuation for

Energy Transfer

does not

adequately reflect

the fact that it

has eliminated

its incentive

distribution rights

that benefited the

general partner,”

said Ethan

Bellamy, senior

research analyst

with Baird. “The

stock looks like

it is still being

valued with a

Kelcy discount.”

Positives on the financial side are that Plains has eliminated incentive distribution rights, is generally self-funding and is targeting lower leverage. Plains is aiming at long-term distribution coverage in a range between 130% and 190%. It expects to exit 2019 with distribution coverage of more than 190%. Plains is targeting distribution growth of 5% per annum.

‘Compelling upside’

Energy Transfer has tended to trade at a lower multiple than its peers, providing investors with an opportunity to buy a midstream security that is “deeply undervalued with compelling upside,” according to Hammond. Plains has recently been trading at a multiple of 8.8 times EV-to-EBITDA, based on 2020 metrics, vs. an average 10.4 times multiple for its large-cap peers.

Hammond’s target price of $23 per share is based on 10.5 times multiple applied to 2020 EBITDA, essentially rerating the stock in line with its peers. Factors that may have held back Energy Transfer to date include somewhat higher leverage, although debt-to-EBITDA has come down to 4.4 times from 6.1 times at 2017 year-end, said Hammond. The company also has greater exposure to natural gas in the Marcellus, he added.

However, Energy Transfer’s assets do not differ that much from Enterprise in terms of quality, according to Hammond, and the distribution yield of over 8% is “extremely attractive.” Long-term distribution coverage is solid at 1.7 to 1.9 times and exceeded 2 times in the first quarter. Hammond projects a free-cash-flow yield of 5.2% for 2019 and 4.9% in 2020.

Energy Transfer also earns an outperform rating from Baird’s senior research analyst, Ethan Bellamy. Bellamy’s target price for the stock is $21 per share, which is calculated using four components. These are an EV-to-EBITDA multiple; a price-to-discretionary cash-flow multiple; a dividend discount model; and the yield spread-to-U.S. Treasuries.

“Energy Transfer is a massive, diversified logistics conglomerate,” said Bellamy. “Historically, it has been one of the most active—if not the most active—in midstream M&A. Its CEO, Kelcy Warren, has built an empire. It’s highly diversified, and its stock is very cheap. And it’s cheap because of a legacy of prioritizing the general partner first and the limited partner second.”

The reference to a legacy practice of prioritizing the general partner relates to an industry trend—now largely dropped—involving incentive distributions rights. These rewarded the general partner largely on the basis of growth in units outstanding, rather than returns flowing to unit holders, and have been eliminated by Energy Transfer and many other midstream MLPs.

Now pari passu

According to Bellamy, “the current valuation for Energy Transfer does not adequately reflect the fact that it has eliminated its incentive distribution rights that benefited the general partner. As a result, Kelcy Warren is now pari passu with the limited partners for the first time. But the stock looks like it is still being valued with a Kelcy discount. I think that that’s no longer valid.”

While Energy Transfer “is almost universally viewed as being cheap in midstream circles, one of the challenges it faces is that it will need new money to move it higher,” said Bellamy. “Most key investors in infrastructure already have a full position. But that can be solved, in my view, if they execute on their plan and are rewarded for their performance.

“Overall, I’m very positive on the stock,” he continued. “In 2020, we have Energy Transfer generating free cash flow after distributions, which is a fairly compelling milestone and ought to screen well versus competitors. They’re on track to de-lever, produce more free cash flow and reap the benefits of all the capex they’re spent. Now they’re in a good position to capture all the volume growth.”

Whether the market will recognize Energy Transfer’s good metrics and “relatively cheap” multiple in 2019 is “tough to say,” commented Bellamy. “But between now and 2020, the data will clearly show fundamental improvement. Determining when the market will respond to that is always difficult. But the performance should be self-evident.”

In terms of valuation, Bellamy said Energy Transfer trades at a multiple of EV-to-EBITDA of roughly 8.5 times, based on 2020 estimates. This is cheap to Williams Cos. Inc., at 10.2 times; Kinder Morgan Inc., at 10.4 times; and ONEOK Inc., at 12.2 times. Leverage stands at about 4.4 times trailing EBITDA for Energy Transfer, compared to an average of 4.6 times for the sector as a whole, he noted.

Due to the “bad taste” of the earlier era, when incentive distribution rights encouraged acquisitions, “there may be some folks who still refuse to own Energy Transfer stock,” commented Bellamy. “But, over time, I believe the value proposition will ultimately win out.”

For those investors comfortable investing in a sometimes volatile small-cap name, Bellamy pointed to Tellurian Inc. Tellurian is developing an LNG production and export terminal, called Driftwood LNG, in south Lake Charles, La. The Tellurian management team, led by Charif Souki and Martin Houston, formerly worked at Cheniere Energy Inc.

Telluride’s ‘partner model’

Using experience gained at Cheniere, the Tellurian management has developed a “partner model” in response to LNG customer requests. The customers provide upfront capital for the construction of the terminal and associated pipelines. In exchange, customers have offtake agreements which give them a pro-rata stake in the LNG cargoes, which they will “effectively get at cost,” said Bellamy.

“In theory, if you have a stake in Driftwood, you should always have the lowest cost gas going forward,” according to Bellamy.

Tellurian took a step toward taking a final investment decision (FID) on the Driftwood LNG project when it finalized an agreement with French integrated producer Total SA to buy 1 million tonnes of LNG and to invest $500 million in Driftwood Holdings LP. The two parties also entered into a sales and purchase agreement covering an additional 1.5 million tonnes from Tellurian’s offtake volumes.

“In theory, if you have a stake in Driftwood, you should always have the lowest cost gas going forward.”

—Ethan Bellamy, Baird

Bechtel, the engineering and construction company in charge of the project under a turnkey contract, has an equity stake in the project in lieu of some of their fees, noted Bellamy. “That demonstrates their commitment to the project,” he observed.

“We’re very positive on Tellurian because of the management team and their track record of execution and expertise, the commitment to the project made by Total, and the relationship with Bechtel,” said Bellamy. “All of which has led to a model agreement that Total has approved, which will allow other potential buyers to take a stake in the project.”

Bellamy projected a FID may take place late this year or, more likely, in the first half of 2020. This assumes a half-dozen or so additional LNG customers come into the project under the “partner model.” Possible new partners to participate in the project include Petronet LNG, based in India, Saudi Arabia’s Saudi Aramco and Middle Eastern and Asian buyers.

Bellamy’s target for Tellurian is $16 per share, but the reality is that—depending on the level of success of the project—the stock price is likely to be either much lower or much, much higher. “I want to stress that it is speculative. The project will either be well underway, with $8 per share of cash flow in sight, or it won’t.”

Recommended Reading

Eni, Vår Energi Wrap Up Acquisition of Neptune Energy Assets

2024-01-31 - Neptune retains its German operations, Vår takes over the Norwegian portfolio and Eni scoops up the rest of the assets under the $4.9 billion deal.

NOG Closes Utica Shale, Delaware Basin Acquisitions

2024-02-05 - Northern Oil and Gas’ Utica deal marks the entry of the non-op E&P in the shale play while it’s Delaware Basin acquisition extends its footprint in the Permian.

California Resources Corp., Aera Energy to Combine in $2.1B Merger

2024-02-07 - The announced combination between California Resources and Aera Energy comes one year after Exxon and Shell closed the sale of Aera to a German asset manager for $4 billion.

DXP Enterprises Buys Water Service Company Kappe Associates

2024-02-06 - DXP Enterprise’s purchase of Kappe, a water and wastewater company, adds scale to DXP’s national water management profile.

Pioneer Natural Resources Shareholders Approve $60B Exxon Merger

2024-02-07 - Pioneer Natural Resources shareholders voted at a special meeting to approve a merger with Exxon Mobil, although the deal remains under federal scrutiny.