(Source: Shutterstock, Hart Energy)

Things calmed down on the 2019 Midstream 50. There were none of the gigantic zooms up and down that occurred in the prior year, with more typical shuffles by a few points up or down the rule this time around.

Compare those minor moves to last year’s rankings when Enbridge Inc. shot to the top of the list with its Spectra Energy Corp. megadeal. Calgary-based Enbridge rose to No. 1 from No. 4 with that acquisition. That’s a stupendous jump, given Enbridge lives up there in the list’s high-rent district, a neighborhood where a billion here or there can get lost in routine deals.

Even more impressive last year was a 30-point skyrocket, to No. 10 from No. 40, by Cheniere Energy Inc.—a 1,077% increase in EBITDA—as its long-promised LNG-export operation in Cameron Parish, La., started making cold. A steady stream of tankers dropped anchor to load at its dock on the Sabine River, with a concurrent new revenue stream.

Take A Look

Although overall trends this time around for the 50 largest publicly held firms were positive, not all enjoyed good news. The biggest challenge for all was how to get investors to look at midstream.

“Despite much better sector fundamentals in 2018 vs. the previous years, the midstream-sector stocks did not do great due to market skepticism on recovery, among other factors,” Sunil Sibal, senior analyst for energy infrastructure and MLPs at Seaport Global Securities LLC, told Midstream Business.

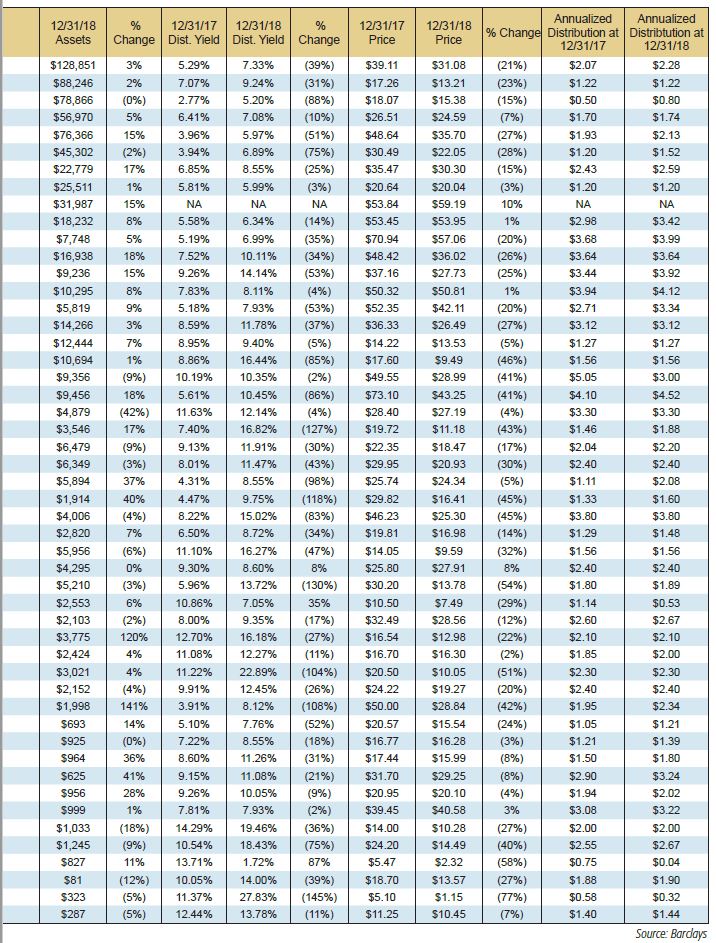

The Midstream 50 lists the top, publicly held midstream-sector players, whether MLPs or conventional corporations, by EBITDA, as compiled by Barclays. Interpretation of and reporting on the rankings is done by Midstream Business.

The 2019 rankings are based on 2018 full-year data, either fiscal or calendar, depending on which a company reports and which is deemed by Barclays to be most appropriate in comparison. Changes shown in the accompanying tables are against the 2018 Midstream 50 rankings, which were based on comparable 2017 financials.

All financials are in U.S. dollars.

Top 10

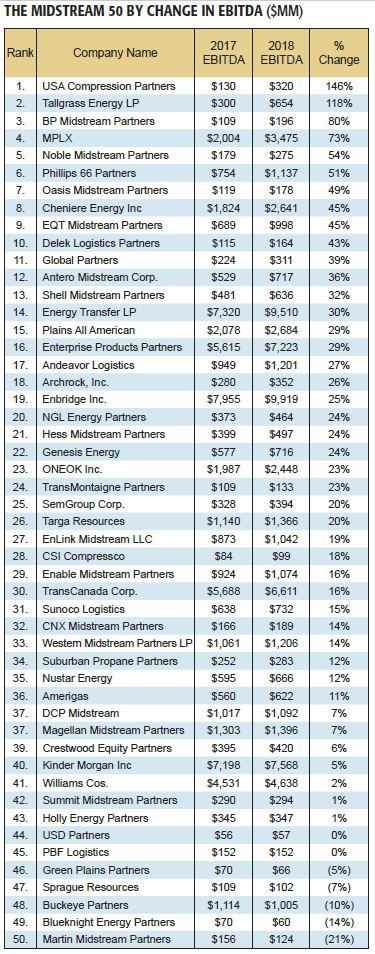

For the 2019 list, Enbridge remained at the top, with EBITDA of $9.92 billion, an impressive 25% rise. Energy Transfer LP continued at No. 2 at $9.5 billion, a 30% increase from the prior year. Perennial big player Kinder Morgan Inc. remained the show horse with EBITDA of $7.57 billion, a 5% increase.

Elsewhere at the top of the list, Enterprise Products Partners LP swapped places with TransCanada Corp. at Nos. 4 and 5 on the strength of a 29% increase in EBITDA. TransCanada’s EBITDA increased 16%.

Tulsa, Okla.-based Williams Cos. Inc. remained No. 6 with $4.64 billion in EBITDA, up 2%. Rounding out the Top 10, in order, were MPLX LP, Plains All American Pipeline LP, Cheniere Energy and ONEOK Inc.

The biggest percentage gains in EBITDA came from USA Compression Partners LP, ranked No. 34 overall. It saw cash flow rise 134% to $320 million for the year. Tallgrass Energy LP, No. 25, enjoyed an impressive 118% EBITDA increase. Another big mover was BP Midstream Partners LP, the sector player for supermajor BP Plc. Its EBITDA rose 80% as it climbed to No. 39 on the list from No. 47 in 2018, its debut on the Midstream 50.

Five firms on this year’s list recorded EBITDA declines: Green Plains Partners LP, Sprague Resources LP, Buckeye Partners LP, Blueknight Energy Partners LP and Martin Midstream Partners LP. PBF Logistics LP’s EBITDA remained flat, year over year.

For the entire field of 50, total EBITDA was $78.5 billion, a 25% increase from $62.7 billion from the previous list.

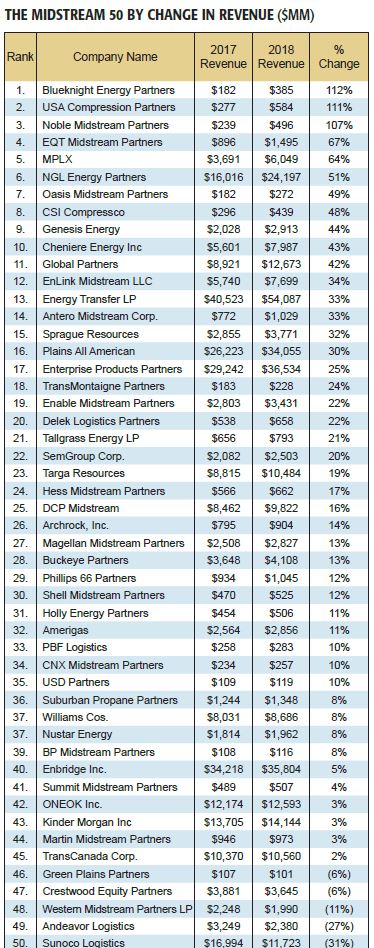

Revenue Rankings

Energy Transfer placed first in revenue at $54.1 billion, well ahead of Enterprise Products, reporting $36.5 billion, with Enbridge close behind Enterprise at $35.8 billion.

Blueknight Energy Partners had the biggest jump in revenue, a 112% increase to $385 million, placing No. 46 by revenue. Blueknight ranked No. 49 by EBITDA. Close behind, USA Compression, No. 37 by revenue, scored a 111% percent gain in revenues to $584 million. It ranked No. 34 by EBITDA.

Total revenue for the 50 firms on the list was $343.2 billion, a healthy 19% increase from $289.3 billion a year earlier.

Wall Street Yawns

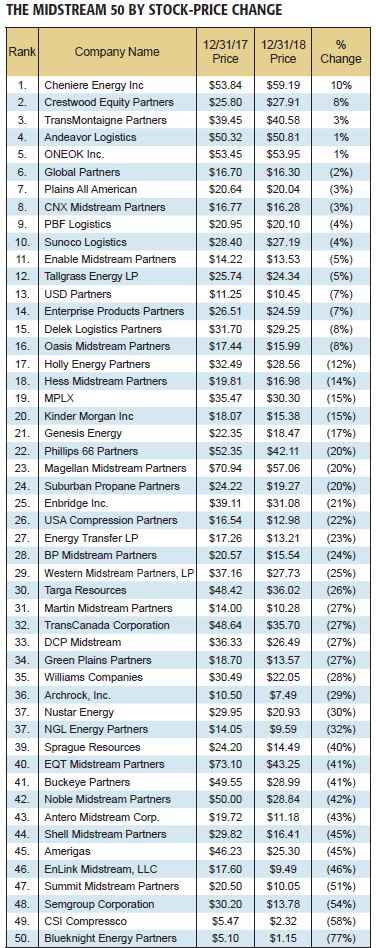

But if the sector’s financials looked acceptable last year—certainly better than the prior two years—it didn’t impress investors. The result showed in sagging share and unit prices. Only five of the 50 firms on the list managed to record year-over-year increases in stock price.

That compares with 13 increases the prior year, a mark most industry observers considered doleful.

Cheniere led with a 10% increase, closing out 2018 at $59.19 per unit, as its LNG sales continued to swell. Crestwood Equity Partners LP managed an 8% gain while TransMontaigne Partners LP ticked up a mere 3%. Andeavor Logistics LP and ONEOK were up 1%.

At the far end of the scale, Blueknight units plunged 77% and CSI Compressco LP, 58%.

The net result was a 20% drop in the index, weighted by market cap.

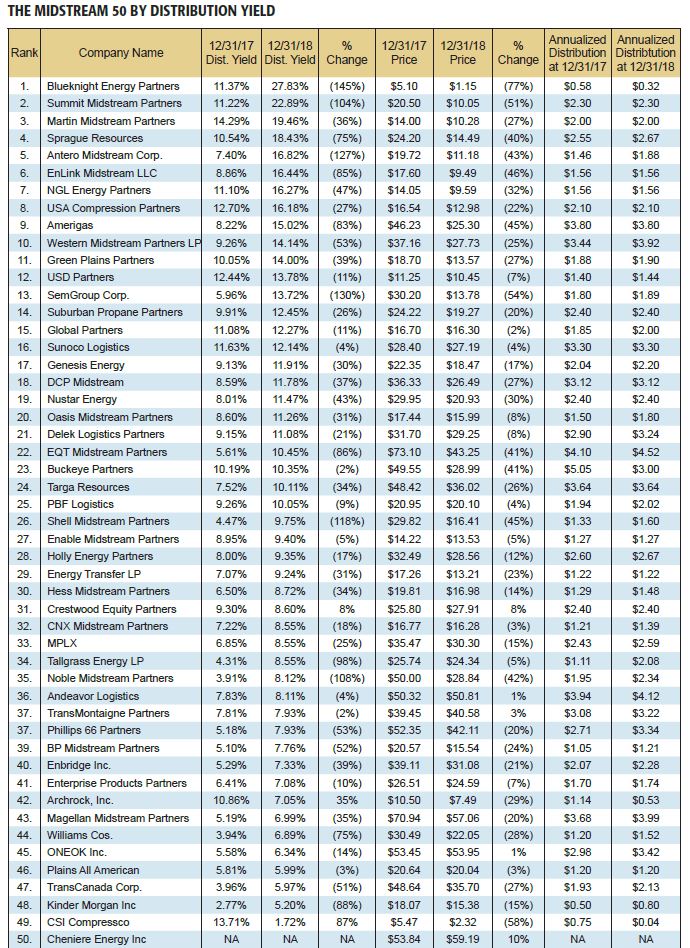

Sagging stock prices created some impressive yield distributions—if they can be maintained. Blueknight returned 27.83% last year as its unit price sagged to $1.15 from $5.10, while its annualized distribution stood at 32 cents, down from 58 cents.

Summit Midstream Partners LP fared little better with a 22.9% return. Its unit price sagged by half, to $10.05 from $20.50, while its annualized distribution remained unchanged at $2.30.

The equity-market problem proved a particular handicap for the smaller players.

“Big picture, our ratings are becoming more bifurcated as, increasingly, the space is shaking out the haves from the have nots,” U.S. Capital Advisors LLC reported in its summary of fourth-quarter midstream earnings.

Stifel Financial Corp.’s analysts sounded a similar theme in a report published as 2019’s second quarter began. “Smaller midstream entities will struggle to attract capital with management teams facing strategic alternatives, such as going private or cutting distributions,” they wrote in the April Energy Playbook.

“We prefer large-cap names, given diversified footprints, investment-grade balance sheets, robust distribution coverage and minimal, if any, external equity requirements.”

Arrivals and Departures

There were the usual comings and goings within the list, including some well-known names in the sector. The biggest name to disappear, Boardwalk Pipeline Partners LP—ranked No. 19 on last year’s list with EBITDA of $791 million—left as general partner Loews Corp. acquired the outstanding units in Boardwalk that it did not already hold.

Restructurings and mergers also claimed such well-known list participants at Valero Energy Partners LP, rolled into parent Valero Energy Corp., and Dominion Midstream Partners LP, merged into Dominion Energy Inc. as 2019 began.

ArcLight Energy Partners Fund VI LP announced as 2018 ended that it would acquire the remaining units in TransMontaigne Partners that it did not already hold and unitholders approved the deal early this year. The New York Stock Exchange delisted TransMontaigne in February.

ArcLight also announced a merger with American Midstream Partners LP, No. 39 on last year’s Midstream 50.

Petroleum products-focused Sunoco Logistics Partners LP earned its place in the sun, at No. 21, separate from its parent, No. 2 Energy Transfer.

Names that lingered on the new Midstream 50—but may not be around next time—are Andeavor Logistics (formerly San Antonio-based Tesoro Logistics), which merged along with its parent, Andeavor Corp., into Marathon Petroleum Corp. in 2018. Marathon also is the parent of MPLX, which moved up one notch in the list to No. 7 with a substantial 73% increase in EBITDA to $3.5 billion.

Andeavor operates west-of-the-Mississippi assets Marathon acquired in the deal, including gathering and processing operations in the Permian Basin and Bakken.

Newcomers on this year’s list include No. 27 Amerigas Partners LP, a major player in NGL and LP terminals. Philadelphia-based UGI Utilities Inc. is its general partner. Coming in at No. 37 was another familiar name in gas liquids, Suburban Propane Partners LP. Green Plains Partners, appearing at No. 48, focuses on motor fuels and ethanol storage and distribution.

Last but not least at No. 50, USD Partners LP rounded out this year’s list. USD specializes in midstream logistics assets, such as rail terminals.

Looking Ahead

Ethan Bellamy, managing director and senior research analyst at Robert W. Baird & Co. Inc., told Midstream Business he sees the positive trends that began in 2018 continuing this year and into the near future.

“The sector is in improving health,” Bellamy said. “If you look at the financial metrics of this group, on average they are better than in 2015, 2016 and 2017. Though the stock prices may not reflect it, leverage and payout metrics have improved meaningfully.”

The first numbers released on 2019 performance, for the first quarter, confirm that trend, according to a report published by Seaport Global.

“Midstream equities had a good start to this year with the Alerian Midstream Energy Select Index (AMEI) … outpacing the 15.9% gains in the broader S&P 500 Index and also the broader energy index (XLE) that gained 17.2%,” the Seaport analysts wrote.

They added, “Midstream equities have also seen some performance dispersion. Among names under our coverage, ONEOK and Williams have outperformed their peers while Plains All American has lagged a bit and Targa Resources [Corp.] significantly.”

Seaport’s Sibal emphasized last year’s dismal performance by midstream issues with more favorable results—so far—for 2019: The AMEI price was down 22.5% in 2018, “a move similar to the move from start of 2015 to the end of 2017.”

However, year-to-date in 2019 the AMEI price is up ~18%, “so things are looking much better,” he added.

With that backdrop, the Seaport report projected these themes for first-quarter earnings:

A quickening upstream pace and resulting midstream volume and cash-flow growth. “Advantage Permian. The commentary from the upstream community on capital discipline has brought increasing focus on slowing production growth and its impact on midstream volumes and cash flows.

“The well-completion data reported by the U.S. Energy Information Administration through March 2019, however, shows the U.S. shale basins continue to make strong progress on completions….”

Returning cash to shareholders vs. fortifying balance sheets. “We think this remains an open question as investors look to stability and sustainability of commodity prices and U.S. production growth. We think midstream players with a balanced approach are likely favored by investors as long as this does not lead to tapping equity markets to finance growth projects.”

A focus on operating costs. “In an environment where E&P customers are super-focused on margin improvement vs. growth, midstream-provider revenues are likely to come under increasing pressure. We think this could put pressure on midstream operators to reduce operating cost and G&A in order to improve profitability.”

NGL price weakness. “NGL prices have lagged crude prices, with ethane and propane leading the weakness.

“Weakness in end-use demand as demonstrated by weakness in ethylene and polymer-grade propylene prices—U.S. Gulf Coast prices down 26.5% and down 10.9%, respectively, year to date—has put pressure on petchem profitability, impacting demand as well as new-project start-up timing, while the growing NGL supply provides additional pressure.”

Potential risks to the midstream. “Despite the strong performance year to date, we believe sector valuations are supportive, devoid of a sharp downturn in commodity complex and upstream activity.

“With the U.S. becoming increasingly reliant on exporting hydrocarbon and, thus, building infrastructure to support that trade, a big slowdown in global demand and further flare-up in trade tensions likely pose the biggest risk to the U.S. midstream players in our view.”

New, Pricey

U.S. Capital Advisors analysts noted in its earnings summary that, although upstream players have “gotten a big dose of religion” about living within their means, the same can’t be said for the midstream as production continues to grow. That creates the need for new, pricey infrastructure.

“Despite the producer pullback in spending, oil and gas production is growing and needs infrastructure to accommodate that growth,” they added. “But that means higher capex and, thus, more financing, which investors are not particularly keen on.

“Aggregate expected capex spend for our midstream universe for 2019 is up 5%, or $1.6 billion, to $32.6 billion post-Q4 earnings calls.”

That will be tough “since equity funding is basically taboo,” so watch for midstream players to take on debt to get the job done, they added.

A Stifel report focused on four midstream trends, including the preference for large-cap players noted by U.S. Capital: An improving financial profile; tightness following by an unconstrained environment as significant new infrastructure goes on stream late this year and in 2020; returning capital next year, “either accelerating distribution growth or share buybacks to absorb excess cash flow; and the struggle of midstream operators to attract capital.

Structural shift

Another big shift Baird’s Bellamy sees is the midstream’s continuing move to a more traditional corporate structure and away from MLPs. He cited three reasons.

“If you tally the top 50, I think you’ll find a continued shift away from the partnership model and toward regular C-corporations,” Bellamy explained. “A few things have driven this. First, lower corporate tax rates suppress the partnership tax advantage.

“Second, the Federal Energy Regulatory Commission’s policy on natural gas pipeline tariffs makes the partnership structure less attractive for those assets. Third, the legacy incentive structures for partnerships can’t be justified by recent returns, and many sponsors have elected to do away with the partnership structure in concert with an elimination of those incentives.”

Seaport’s Sibal also commented on the trend toward C-corp structures, noting he uses the broader AMEI as a benchmark as, “considering the move from MLP to the C-corp structure, this has become more representative of midstream names in my view.”

So 2018 may have been pretty good for the sector. What will it take to make it very good—and get investors to start considering midstream issues again?

“Simplified structures and improved financial profiles create financial flexibility,” the Stifel analysts wrote. “Investment should moderate in 2020—confirmation needed—with either accelerating distribution growth or share buybacks absorbing excess cash flow, which should drive outperformance.”

Paul Hart can be reached at pdhart@hartenergy.com or 713-260-6427.

Recommended Reading

The OGInterview: Petrie Partners a Big Deal Among Investment Banks

2024-02-01 - In this OGInterview, Hart Energy's Chris Mathews sat down with Petrie Partners—perhaps not the biggest or flashiest investment bank around, but after over two decades, the firm has been around the block more than most.

Chesapeake Slashing Drilling Activity, Output Amid Low NatGas Prices

2024-02-20 - With natural gas markets still oversupplied and commodity prices low, gas producer Chesapeake Energy plans to start cutting rigs and frac crews in March.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

Will the Ends Justify the Means for W&T Offshore?

2024-03-11 - After several acquisitions toward the end of 2023, W&T Offshore executives say the offshore E&P is poised for a bounce-back year in 2024.

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.