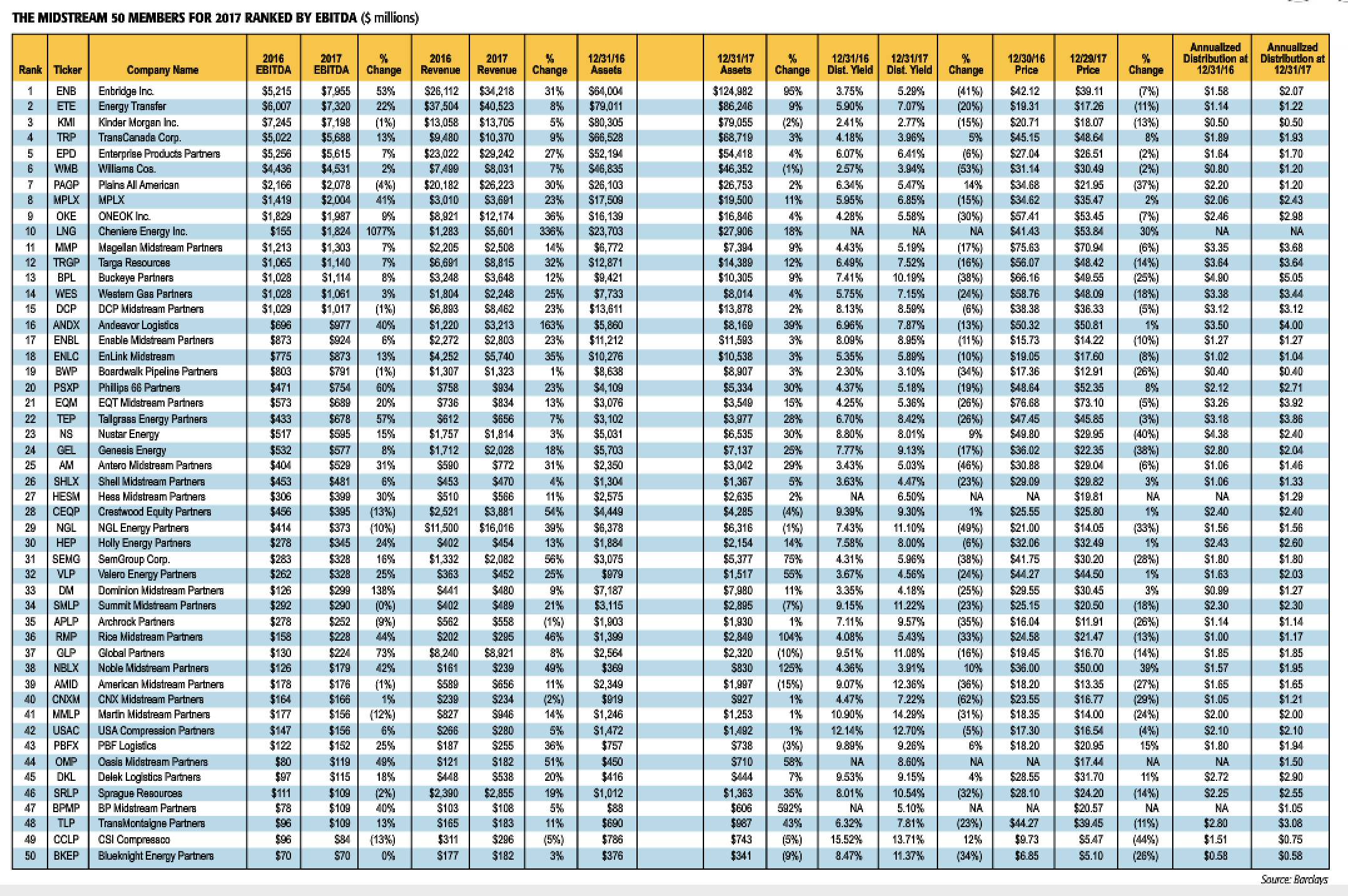

After its combination with Spectra Energy Corp., Enbridge Inc. sprinted to the top of this magazine’s 3rd third annual Midstream 50 list of the sector’s largest publicly held firms in 2017. The Calgary-based company held the show place in last year’s survey but jumped over perennial Nos. 1 and 2, Kinder Morgan and Energy Transfer.

It bears mentioning that even as the future of the North American Free Trade Agreement has been cast into some doubt by protectionist sentiments in Washington, the combination is technically a Canadian company acquiring an American one.

Big mover

Several other business combinations tweaked the charts but the biggest move was purely organic—fueled by LNG. Cheniere Energy, operator of the first mega-LNG export terminal in the U.S., made a lightspeed move higher by 30 places to crack the top 10.

Midstream operators are ranked by EBITDA as compiled by Barclay’s. Interpretation of and reporting on the rankings is done by Midstream Business.

The 2018 rankings are based on 2017 full-year data, fiscal or calendar, depending on which the company reports and which is deemed to be most appropriate in comparison. Changes in the league tables are against the 2017 rankings, which were based on 2016 financials.

There were four debuts on the charts, one merger and three newly autonomous midstream ventures spun out of upstream producers. San Antonio-based Tesoro Logistics, a substantial No. 18 on last year’s list, and Western Refining Logistics, No. 44 last year, were combined into the renamed Andeavor Logistics when their parent refining and marketing firms merged. The combined entity made its entrance at No. 16. It also came in at No. 2 on the list based on changes in revenue, with a pro forma gain of 163%.

The other three debuts were an interesting group: one from a global major, one from a large and formerly integrated producer, and one from a Bakken independent. Hess Midstream Partners made the highest debut, entering at No. 26. Oasis Midstream Partners entered the list at No. 43. And BP Midstream Partners made its appearance at No. 46.

Lost to the list

A few other names also disappeared from the charts. Spectra, as noted, became part of new top-dog Enbridge. At the end of February, 2017, Enbridge and Spectra Energy closed their merger. The transaction created a global energy infrastructure operation with an enterprise value of about $126 billion.

Separately, VTTI Energy Partners, a terminal operator, was merged back into parent company VTTI BV. As a result, VTTI Energy Partners ceased to be a publicly-traded partnership and its common units are no longer traded on the New York Stock Exchange.

In contrast to the 2017 rankings where there was quite a bit of jockeying around from the 2016 standings, this year there were not too many major moves. Other than the noted warp-drive jump by Cheniere, there were no shifts up or down greater than seven places this year.

American Midstream Partners, No. 39, moved higher by seven places from its 2017 standings. Noble Midstream Partners, No. 38, moved higher by five notches. Meanwhile, DCP Midstream, No. 15, and Phillips 66 Partners, No. 20, both moved higher by four places.

Slipping spots

Among companies slipping lower, the biggest decline was CSI Compressco, which fell seven places to No. 49. Archrock Partners, in 35th place, slipped six places from its 2017 ranking. Two companies, Crestwood Equity Partners and Martin Midstream Partners, fell five spots.

All of the other moves higher or lower were three spots or fewer.

Strictly speaking, there were no actual promotions or relegations in the traditional sense of companies moving up into the Top 50 or being displaced out of it. All four of the names out of the list are gone as independent operations, and all of the new names added are new entries.

There were eight companies that held steady positions.

Overall, companies reported relatively steady business, which jibes with prevailing sentiment in the midstream sector that operators are sticking to their knitting. The notable changes were due to business consolidation, and the one standout by the full force of a new market segment: LNG exports. It will be interesting to see in the next few years if the four or five new LNG trains that are due to come into service will work equally substantial changes in those rankings to Cheniere’s performance.

Enbridge endeavors

“This has been a transformational year for our company,” said Al Monaco, president and CEO of Enbridge, in commenting on the company’s 2017 results. “With the Spectra Energy assets now in the fold, we have successfully delivered on our strategy to re-balance our business mix with best-in-class natural gas transmission assets, and further enhance and extend our growth potential. We’ve substantially integrated the two companies and are slightly ahead of target for capturing cost synergies as we streamline operations and create an even more effective and efficient organization.”

In addition to the merger, Monaco noted that Enbridge, “significantly added to our leading infrastructure footprint, bringing a total of $12 billion of new assets into service, substantially on-time and on-budget. This marks the single largest year for project completion in our history and these assets will provide growing and predictable cash flows to support our premium dividend growth.”

Dawn of LNG exports

There is an old expression that there is no resisting an idea whose time has come. And Cheniere’s rocket ride from No. 40 last year to No. 10 this year is proof that is true for U.S. LNG exports. There was no merger or acquisition, no Deus ex machina drop of assets from a parent C corp. There was simply the release of long-pent supply into a global market eager for both raw volumes and for a trading partner committed to commercial reliability and the rule of law.

“2017 was a breakthrough year for Cheniere, with milestone achievements throughout the company, and with 2018 off to a robust start, we are raising our full year guidance,” said Jack Fusco, Cheniere’s president and CEO in his discussion of the company’s 2017 results. “In 2017, we [brought] the third and fourth trains at Sabine Pass online ahead of schedule and on-budget, fulfilling our obligations to our foundation customers, and successfully marketing and delivering portfolio LNG volumes.”

Strategically, Cheniere made significant recent progress toward a final investment decision for Train 3 at its new Corpus Christi, Texas, plant by entering three long-term supply agreements, two with China National Petroleum Corp. and one with Singapore commodity trading house Trafigura.

Cheniere also issued to engineering and construction firm Bechtel a limited notice to proceed under the contract for Train 3.

Further, Fusco said that “As we begin 2018, we are committed to capitalizing on these successes by continuing to supply LNG, progressing construction on Train 5 at

Setting a mark that is likely to stand for a long time, Cheniere’s increase in EBITDA was 1077% in one year.

Leaders in EBITDA

Among mere mortals, Dominion Midstream achieved an increase in EBITDA of 138% year on year. But in an indication of how competitive the midstream has become, that was only good for 33rd place in the league table. That was actually a decline of three places from last year.

Global Partners was next best in boosting EBITDA, with a healthy improvement of 73%. In contrast to most other operators on the charts, Global is integrated downstream in distribution, including wholesale and retail fuel operations. Management discussions of results focused on those operations rather than on traditional midstream business.

The Sand Hills Pipeline, a joint venture (JV) in which Phillips 66 Partners has a one-third interest, exceeded 300,000 barrels a day (Mbbl/d) throughput in fourth-quarter 2017 and was expected to reach 365 Mbbl/d in the first quarter. Further expansion of the line to 450 Mbbl/d is expected to be completed by midyear.

Sand Hills transports NGL from the Permian Basin to the Texas Gulf Coast. Enbridge, now No. 1 on the table, owns one-third through its acquisition of Spectra, and DCP Midstream Partners, No. 15, owns the other third.

The STACK Pipeline LLC JV expansion to loop an existing pipeline and to extend further into the big Midcontinent play was completed late in 2017. The loop increased capacity by 150 Mbbl/d. It is a 50:50 venture between Phillips 66 Partners and Plains All American Pipeline, No. 7 on this year’s table.

Looking ahead, permitting is complete and construction has begun on the Bayou Bridge Pipeline extension from Lake Charles to St. James, La. The pipeline is currently operating from

The Sacagawea Pipeline venture is building a 24-mile raw natural gas system linking production in Mountrail County, N.D., to gathering and processing capacity in McKenzie County, N.D. The project is anticipated to be completed in the second half of 2018.

The Sacagawea Pipeline and Palermo Rail Terminal are designed to enhance logistical options for crude transportation in the Bakken region. Phillips 66 Partners owns half of the pipe JV and 70% of the rail JV. Paradigm Energy Partners owns the balance of each. Paradigm is not on the list.

Assets drove growth

Among increases in assets, the standout was BP Midstream Partners, new to the Midstream 50 this year. According to the company, the main reason for the increase in total assets is due to the assets contributed to the partnership at the time of the IPO in October 2017.

In response to an inquiry from Midstream Business, BP Midstream [BPMP] provided this detail: “The assets [composing] our predecessor operations are a subset of the post-IPO-period asset portfolio—the assets of our predecessor only included the BP2, River Rouge and Diamondback pipeline systems; they do not include our interests in the Mars and Mardi Gras pipeline systems ... Additionally, cash held by BPMP at Dec. 31, 2017, was approximately $33 million; cash was not reported against our predecessor operations at Dec. 31, 2016.”

BP is the second supermajor energy company to spin out a midstream MLP, following the lead of Shell’s creation of Shell Midstream in late 2014. Shell Midstream moved up two notches in the new rankings, to No. 26 from No. 28.

Revenue increases

Not surprisingly, Cheniere also led the table for raw revenue increase, at a lofty 336%. The newly formed Andeavor combination was second at 163%.

Among companies making organic increases to top-line money, SemGroup, at 56%, edged out a tight cluster of Crestwood, 54%; Oasis, 51%; and Noble, 49%.

Tulsa, Okla.-based SemGroup’s higher 2017 results were driven by cash flow contributions from two new Gulf Coast assets in addition to strong results from its Canadian business. In the summer of 2017, Sem acquired Houston Fuel Oil Terminal Co. (HFOTCO) for $2.1 billion. Also during the summer, it completed the Maurepas Pipeline on the Gulf Coast, which began contributing cash flows.

“Our higher fourth-quarter results include a full quarter of secure cash-flow contributions from our new Gulf Coast assets in addition to strong results from our Canadian business,” said SemGroup President and CEO Carlin Conner. “We have raised nearly $800 million in the last few months with announced sales of non-core businesses and a preferred equity transaction, the proceeds of which we plan to use to fully pay the second HFOTCO payment by the end of the first quarter and to fund future growth.”

In February of this year, SemGroup announced that it had reached an agreement to sell its SemLogistics business unit, a petroleum storage facility in the U.K., to Valero Logistics UK, a subsidiary of San Antonio refiner and marketer Valero Energy. In addition to the sale price, the agreement provides for potential earnout payments to be made to SemGroup if certain revenue targets are met in the four years following close of the transaction.

SemGroup intends to use proceeds from the sale toward its plan to raise capital and to “pre-fund capital growth projects.” The SemLogistics sale is expected to close by the end of the third quarter of 2018, subject to the receipt of governmental approvals and the satisfaction of other customary closing conditions.

Index performance

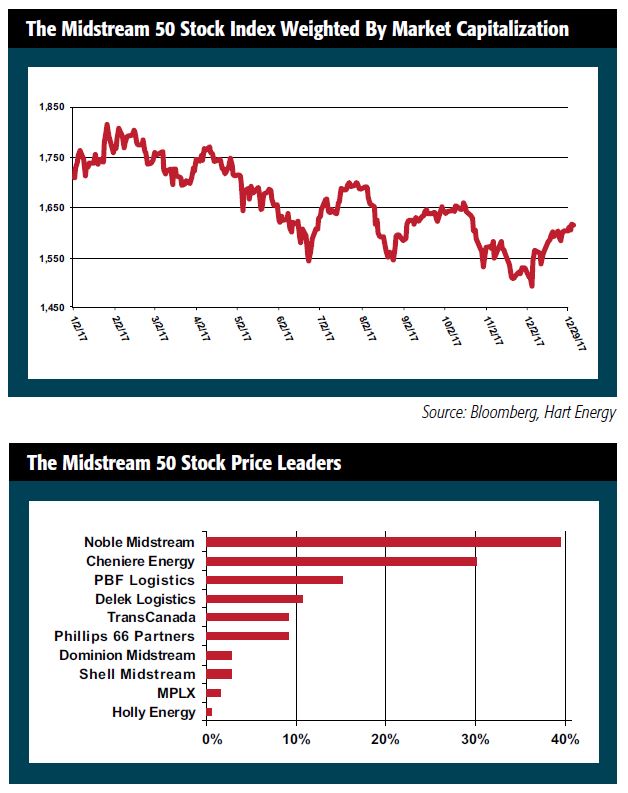

Despite improving business performance, the midstream remained out of favor with many investors on Wall Street and that showed in index stock price performance.

The average stock price among the 50 members of the listing was down 10% for the year, even though the 50 firms saw EBITDA climb 38%, on average, and both revenues and assets rose by 28%.

Noble Midstream had the best unit price performance, up 39%, and to no one’s surprise Cheniere’s unit price was up sharply at 30%. But of the 47 firms that returned to the list from the prior year, only 13 managed to show an increase in stock price for 2017.

Recommended Reading

From Restructuring to Reinvention, Weatherford Upbeat on Upcycle

2024-02-11 - Weatherford CEO Girish Saligram charts course for growth as the company looks to enter the third year of what appears to be a long upcycle.

TechnipFMC Eyes $30B in Subsea Orders by 2025

2024-02-23 - TechnipFMC is capitalizing on an industry shift in spending to offshore projects from land projects.

NOV's AI, Edge Offerings Find Traction—Despite Crowded Field

2024-02-02 - NOV’s CEO Clay Williams is bullish on the company’s digital future, highlighting value-driven adoption of tech by customers.

Patterson-UTI Braces for Activity ‘Pause’ After E&P Consolidations

2024-02-19 - Patterson-UTI saw net income rebound from 2022 and CEO Andy Hendricks says the company is well positioned following a wave of E&P consolidations that may slow activity.

ProPetro Reports Material Weakness in Financial Reporting Controls

2024-03-14 - ProPetro identified a material weakness in internal controls over financial reporting, the oilfield services firm said in a filing.