(Source: Shutterstock.com)

Oil and gas producers often pursue M&A to create value for shareholders. But, a new report finds that a lot of upstream M&A is anything but accretive for investors.

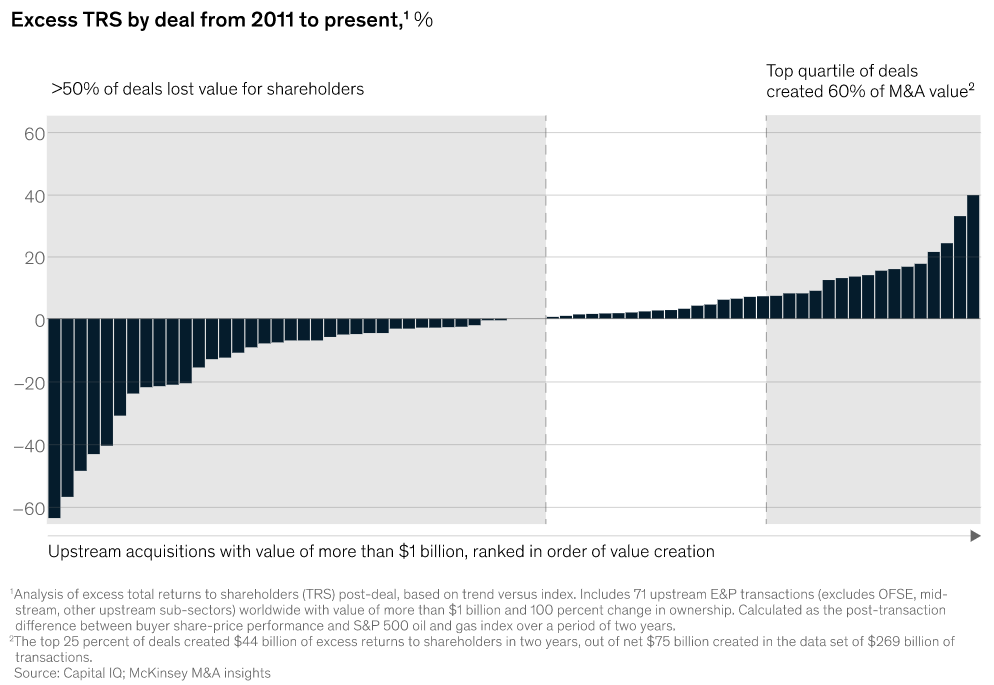

Since 2011, out of the 71 upstream oil and gas transactions totaling more than $1 billion, an analysis by McKinsey & Co. found that more than half of the deals did not create value for shareholders.

However, the April 18 report found that the top quartile of upstream E&P deals over the past 12 years generated outsized returns for shareholders. The top 25% of deals generated $44 billion in excess shareholder returns over two years, McKinsey found.

“Multiple components are at play, such as pre-deal diligence, asset-performance uncertainties, outlooks for oil and gas prices and transaction management,” McKinsey said in its report. “But in all cases, the ability to accrue differentiated value creation is a key factor determining merger success and may determine the winners in the next cycle.”

All too often, E&P companies targeting large-scale M&A are focused on the “low-hanging fruit” of reducing G&A costs, McKinsey found.

But, companies pursuing M&A for broader operational synergies often see greater cost savings than G&A savings through headcount reductions and eliminating other expenses.

“Upstream companies can open the aperture across revenue and production, operating costs and capital efficiency in addition to G&A, using the merger as a “moment in time” to catalyze performance improvement across both entities,” McKinsey said in the report.

Communicate goals

Planning for more accretive operational synergies around production, revenue and other metrics is a good start, McKinsey said. Making those needs known to the public is even better.

Announcing cost-synergy expectations may be tied to “significant long-term outperformance over peers,” according to an analysis of 776 deals across sectors. Total shareholder returns for companies that did announce synergy targets outperformed those that didn’t by an incremental 7% after a median of two years.

“Publicly announcing targets can contribute to putting healthy pressure on the executives and support teams who will have their compensation linked to meeting targets,” the company said in the report.

RELATED: Permian in Spotlight as Energy Dealmaking Gathers Steam

Cash-fueled M&A wave

Experts at McKinsey and beyond are expecting a new wave of oil and gas M&A driven by an influx of record cash flow into the E&P sector.

Going for greater capital discipline, upstream operators have been using their cash stockpiles to pay down debt and boost shareholder value through stock buybacks and dividends, KPMG’s Mike Harling, U.S. energy deal advisory and strategy leader, told Hart Energy.

But there’s still a lot of cash out there that E&P companies are looking to put to work, he said.

“That sets up an environment that is favorable for M&A,” Harling said.

In the Lower 48, the Permian Basin in West Texas and New Mexico continue to be a competitive market for upstream M&A.

Exxon Mobil has reportedly held discussions on potential M&A with Permian pure-player Pioneer Natural Resources as the oil and gas supermajor searches for more inventory runway.

Earlier this month, Ovintiv Inc. agreed to scoop up three EnCap-backed privates in the Northern Midland Basin in a cash-and-stock deal valued at $4.725 billion.

Within the past year, Matador Resources and Diamondback Energy also signed $1 billion-plus deals to acquire private E&Ps in the Permian.

RELATED: Shale M&A Opportunities Shrink After Ovintiv’s $4.2 Billion Permian Deal

Recommended Reading

NAPE: Turning Orphan Wells From a Hot Mess Into a Hot Opportunity

2024-02-09 - Certain orphaned wells across the U.S. could be plugged to earn carbon credits.

Exxon Versus Chevron: The Fight for Hess’ 30% Guyana Interest

2024-03-04 - Chevron's plan to buy Hess Corp. and assume a 30% foothold in Guyana has been complicated by Exxon Mobil and CNOOC's claims that they have the right of first refusal for the interest.

Petrobras to Step Up Exploration with $7.5B in Capex, CEO Says

2024-03-26 - Petrobras CEO Jean Paul Prates said the company is considering exploration opportunities from the Equatorial margin of South America to West Africa.

The OGInterview: How do Woodside's Growth Projects Fit into its Portfolio?

2024-04-01 - Woodside Energy CEO Meg O'Neill discusses the company's current growth projects across the globe and the impact they will have on the company's future with Hart Energy's Pietro Pitts.

Deepwater Roundup 2024: Offshore Australasia, Surrounding Areas

2024-04-09 - Projects in Australia and Asia are progressing in part two of Hart Energy's 2024 Deepwater Roundup. Deepwater projects in Vietnam and Australia look to yield high reserves, while a project offshore Malaysia looks to will be developed by an solar panel powered FPSO.