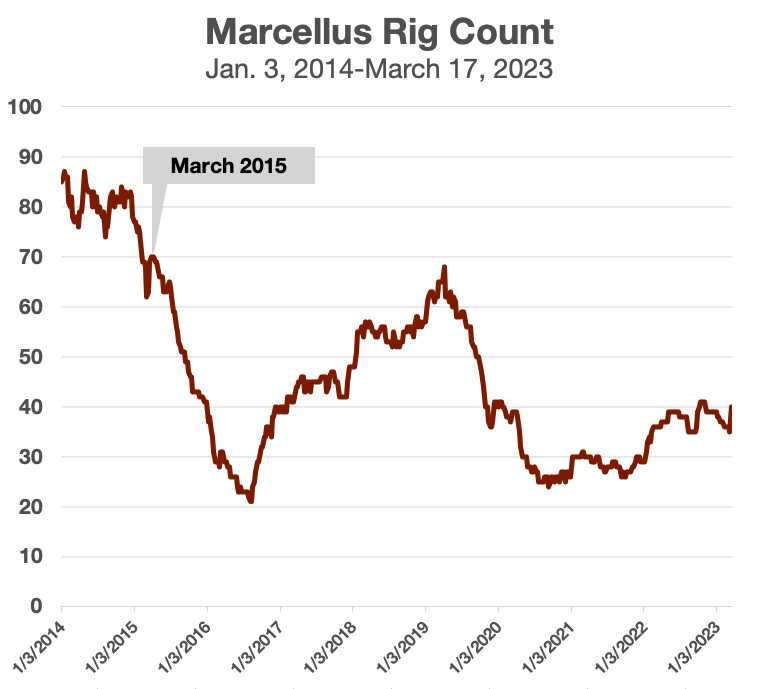

Gas-directed rig activity was led by the Marcellus Shale, where drillers added five gas rigs over the past week – the most gas rigs added in the region since March 2015. (Source: Shutterstock)

Rig activity in key U.S. basins is up, despite volatility in commodity prices, according to data from Baker Hughes.

The oil and gas rig count, a barometer for the drilling sector and industry suppliers, grew by eight to 754 total rigs during the week ended on March 17.

While the number of net oil rigs fell by one to 589, U.S. drillers added nine natural gas rigs over the week. It was the largest single-week increase in gas rigs since December 2018, Baker Hughes data shows.

Faced with warmer weather and weaker-than-expected demand so far this year, U.S. gas demand has struggled to keep up with supply, Rystad Energy Analyst Ade Allen said.

“Last week was a relatively tepid week for the U.S. gas markets as prompt-month Henry Hub prices traded sideways and end[ed] up settling relatively flat for the week at $2.33/MMBtu [million Btu],” Allen said in a March 21 research note. “As winter draws to a close and the market moves into the shoulder season, limp demand is not enough to keep up with growing supply, and the chances of that balance finding equilibrium is minimal at best.”

Gas rigs on the move

Gas-directed rig activity was led by the Marcellus Shale, where drillers added five gas rigs over the past week – the most gas rigs added in the region since March 2015, according to Baker Hughes data.

A total of 40 rigs were deployed in the Marcellus as of March 17.

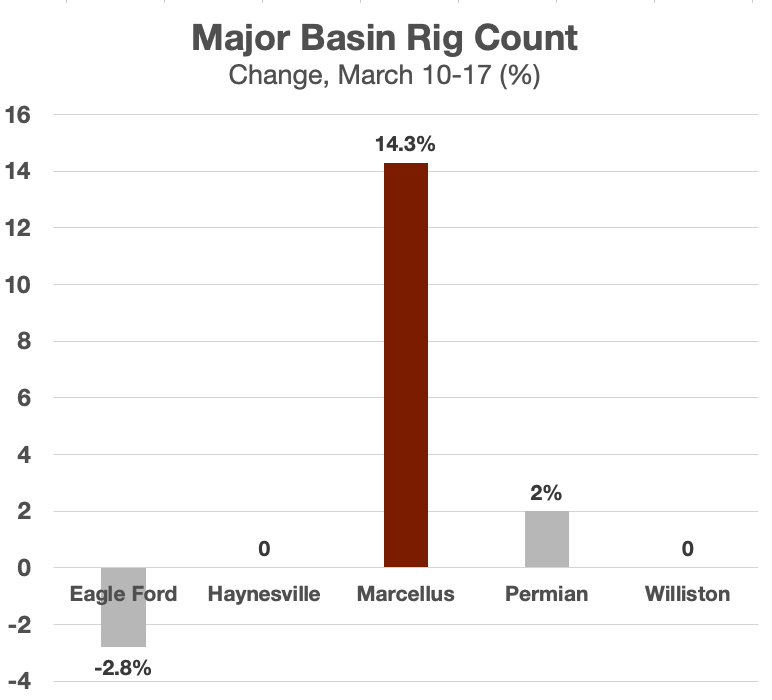

Operators in the Eagle Ford Shale in South Texas added four gas rigs during the week, while the Permian Basin in West Texas and New Mexico added a single gas rig.

Meanwhile, four gas rigs exited the Utica Shale play over the past week.

Rig activity in the gassy Haynesville Shale region held steady at 67.

RELATED

Haynesville, Permian to Lead Natural Gas Production Growth in April

As the natural gas sector continues to face price pressure, analysts at Tudor, Pickering, Holt & Co. (TPH) expect gas rigs will be cut in the Haynesville, the Eagle Ford and the Anadarko Basin during the second quarter and in the second half of 2023.

However, TPH analysts said it is time to begin accumulating gas stock exposure for eventual upside recovery in 2025 and beyond, with possible estimates ranging between $6/MMBtu and $7/MMBtu during tighter years.

RELATED

U.S. NatGas Price Volatility? ‘No Sympathy’ From Europe, Says Tellurian’s Simões

After averaging $6.42/MMBtu in 2022, Henry Hub gas prices are expected to average around $3/MMBtu this year before rising to an average of $3.89/MMBtu in 2024, according to the latest U.S. Energy Information Administration forecasts.

Oil rigs trend down

The total oil rig count decreased, continuing a downward trend seen for the past five weeks.

Energy companies in the prolific Permian region added six oil rigs during the week ended March 17.

The Denver-Julesburg Basin (D-J Basin) and Niobrara Basin in Colorado and Wyoming added a single oil rig.

The oil rig count in the Eagle Ford fell by six over the week.

Bank failures in the U.S. and uncertainty about a broader banking contagion have pushed down commodity futures and energy stocks in recent days.

On March 17, WTI's spot price closed out trading at $66.61/bbl while Brent ended the day at $71.03/bbl. It was WTI’s lowest point since December 2021, per EIA data.

Oil prices have rebounded some this week: WTI rose to $69.53/bbl and Brent rose to $75.25/bbl on March 21.

Recommended Reading

Santos’ Pikka Phase 1 in Alaska to Deliver First Oil by 2026

2024-04-18 - Australia's Santos expects first oil to flow from the 80,000 bbl/d Pikka Phase 1 project in Alaska by 2026, diversifying Santos' portfolio and reducing geographic concentration risk.

Iraq to Seek Bids for Oil, Gas Contracts April 27

2024-04-18 - Iraq will auction 30 new oil and gas projects in two licensing rounds distributed across the country.

Vår Energi Hits Oil with Ringhorne North

2024-04-17 - Vår Energi’s North Sea discovery de-risks drilling prospects in the area and could be tied back to Balder area infrastructure.

Tethys Oil Releases March Production Results

2024-04-17 - Tethys Oil said the official selling price of its Oman Export Blend oil was $78.75/bbl.

Exxon Mobil Guyana Awards Two Contracts for its Whiptail Project

2024-04-16 - Exxon Mobil Guyana awarded Strohm and TechnipFMC with contracts for its Whiptail Project located offshore in Guyana’s Stabroek Block.