M&A finds a way. Even in a year as ungainly and uncertain as 2022, dealmakers regained their balance despite war, rampant inflation, COVID and wild swings in commodity prices.

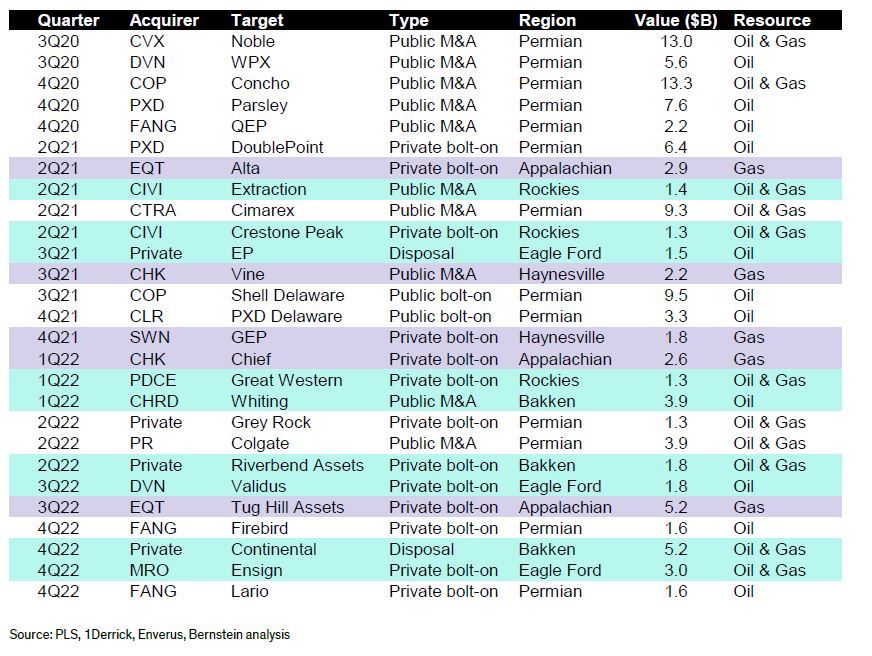

By the second half of the year, large public U.S. E&Ps struck six megadeals worth a combined $14.25 billion.

Bernstein analyst Bob Brackett sees a chance that M&A could “pivot from shale bolt-ons to something much grander.”

Independent shale E&Ps with high-quality inventory and operations are potential M&A targets for supermajors, Brackett said. Bernstein’s top E&Ps include Hess Corp., EOG Resources, ConocoPhillips, APA Corp., Devon Energy, Pioneer Natural Resources and Kosmos Energy.

With a lull in upstream deals in December amid a plunge in commodity prices, the question is whether 2023 will continue to be robust for M&A or another topsy-turvy year like 2022. In either event, public E&Ps will look for ways to replenish inventory through deals after largely turning away from investment in exploration, analysts said.

“This is a good time to actually think about, ‘hey are we getting the right value for the assets? Is the appreciation sufficient? Do we hold off for a little bit longer to expect that prices will go another $10 higher, another $2 more for gas?’ So, I think there's a lot of those unknowns that are occurring right now, and people are just definitely being a little cautious in terms of signing the deal.” – Seenu Akunuri, PwC

Seenu Akunuri, PricewaterhouseCoopers's (PwC) U.S. energy, utilities and resources deals leader, said dealmakers are likely taking a breather in December, particularly as the market’s volatility has seemingly little to do with supply and demand. Rather, macro events, including the Russia and Ukraine war, OPEC quotas, interest rate hikes and China’s COVID policies have buffeted prices.

“This is a time where people kind of reflect a little bit and take a little pause,” Akunuri told Hart Energy, noting that a deal he’s looking at currently could be announced in December but “they’re kind of dragging their feet a little bit.”

“This is a good time to actually think about, ‘hey are we getting the right value for the assets? Is the appreciation sufficient? Do we hold off for a little bit longer to expect that prices will go another $10 higher, another $2 more for gas?’”

“So, I think there's a lot of those unknowns that are occurring right now, and people are just definitely being a little cautious in terms of signing the deal.”

Typically, noise about the economy, inflation and interest rate increases wouldn’t impact commodity prices so dramatically. But recently, seemingly every news event causes prices to buckle, Akunuri said.

“My suspicion is, come January, we probably will start seeing deals,” he said.

Mike Scialla, managing director of energy equity research at Stephens, said the underlying pressure to get deals done persists, despite the drag of price volatility.

“Any deals that are free cash flow-accretive are going to be given some pretty serious consideration, especially if they come with operational synergies and lead to improved cost efficiency,” Scialla said. “The environment's still ripe for M&A, but you've got volatility on the price side that's just holding it back at the moment.”

For 2023, Scialla said he expects continued deals between publics and privates, “but I still think there’s some more mergers-of-equals that we’ll see. And maybe even some of the larger publics buying some of the smaller public companies as well.”

Supermajor shift in consolidation?

Bernstein’s view is that the very nature of shale consolidation is set to shift in a big way, according to a Dec. 12 report by Brackett and co-author Ian Moore.

“We believe shale E&P consolidation is once again logical and likely accretive at this point in the cycle,” they wrote.

The second-half of 2020 saw the creation of oil-focused giants via zero-premium public transactions. In 2021 and 2022, many larger operators such as Devon, Pioneer, EQT Corp., Civitas Resources, Southwestern Energy, Chesapeake Energy and others expanded sector discipline and extended inventory life through bolt-on acquisitions from private equity.

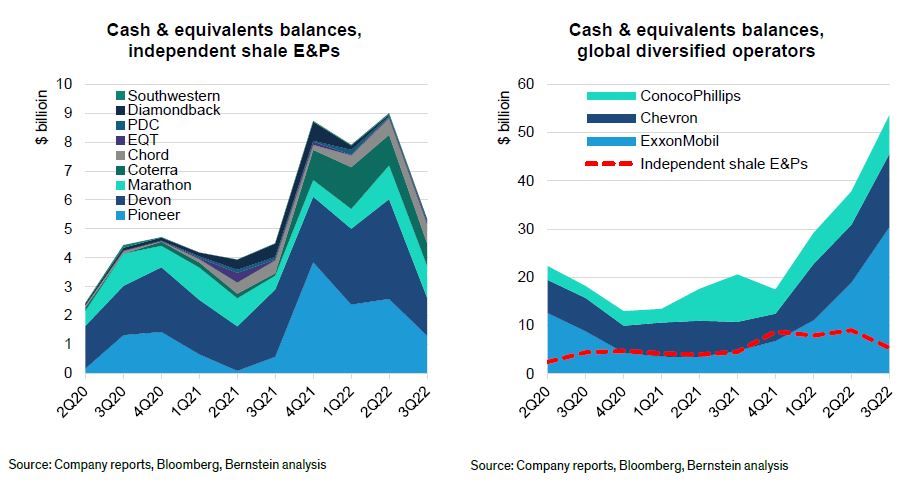

“Independent shale E&P balance sheets have shrunk to a point where pursuing bolt-on acquisitions from private equity is less likely,” Brackett said.

In the background, shale-focused global diversified operators ConocoPhillips, Chevron Corp. and Exxon Mobil have “built war chests over the past several quarters.”

And independent shale E&P company valuations have been either stagnant or contracting year-to-date, sitting near 10-year lows, Brackett said.

“We expect at least one large acquisition within the next 12 months, likely at a purchase price ~30% above market,” he said.

Three high-level market conditions were key to megadeal cycles in the past, Brackett said. They occur when:

- Organic growth and/or exploration prospects are nonexistent;

- Costs are rising and/or expected to rise further; and

- Valuations are modest, often with spot prices at or below marginal costs.

All of those conditions, Brackett said, are present today.

The largest oil-focused shale E&Ps have committed to low-single-digit organic volume growth “in perpetuity” as management teams focus on maximizing returns—“the sector that once spent ~$2/boe on exploration and has averaged just over ~25¢/boe in 2022,” Bracket said.

Costs are also up, along with supply chain constraints and a shortage of skilled oilfield labor, which are all driving up capital requirements for drilling and completions. Shale capex requirements rose about 20% to 25% in 2022 and could be up another 15% in 2023 based on third-quarter commentary from the operators.

And equities are trading at relatively modest valuations. “Crude is below marginal cost, and forward EBITDA multiples have not expanded year-to-date [and] are well below their pre-pandemic averages and … near 10-year lows,” Brackett said.

Shale E&Ps that acquired private equity-backed assets in 2021 and 2022 could now be viewed as potential takeout candidates for ConocoPhillips, Chevron and Exxon Mobil in 2023.

“For these three global operators, scaling U.S. shale operations (especially in the Permian) is core to their long-term strategy,” Brackett said. “Each has built a sizable war chest over the past several quarters. Cash positions among the independent shale operators, on the other hand, are beginning to dwindle as bolt-on acquisitions close and commodity prices taper.”

Notably, “two years have passed since the period of early-cycle, zero-premium Permian M&A, [and] Exxon Mobil has yet to make a sizeable acquisition,” Brackett said.

Private equity sets its sights on oil

PwC expects large oil and gas companies to continue divesting from oil and gas assets as they adjust their portfolios to meet growing ESG demands and satisfy policies that encourage green energy.

Private companies, in particular, are more likely to take the lead on domestic deals, especially for oil assets, the firm said.

In November, EnCap Investments was reportedly raising its first private equity oil and gas production fund in five years, according to Reuters. And in December, Kayne Anderson Capital Advisors was said to be creating a new investment vehicle dedicated to U.S. oil and gas production with a goal of raising $1.5 billion.

Akunuri said private capital will “definitely” look for opportunities to acquire resources and then exit.

EnCap, Kayne Anderson “and a whole host of others, they're constantly looking to buy assets,” he said.

In Texas and Oklahoma, many private companies and family businesses that own acreage are doing well. But the next generation may not want to manage those businesses.

Such companies are “perfect for private equity to buy, create a portfolio company and continue to buy other assets [and] create other portfolio companies, and when they're big enough, they can put them together, either go public or have an exit strategy in place,” he said. “Some of the deals that happened last year were very similar to that. Companies that were acquired over the past two, three years, and then they were monetized.”

In one private equity deal Akunuri saw to completion, a company purchased in 2021 was sold in early 2022 for a huge profit.

“Within a year they had a 300% return. So, they're always very opportunistic in looking to identify assets that make sense,” Akunuri said.

Private capital is also showing interest in midstream infrastructure, Akunuri said.

“They're also trying to make investments because they're looking to the future, and some of this infrastructure and [pipeline] systems could not only be utilized for oil and gas,” he said, “but they could potentially be utilized for wind and solar and other renewable energy as well.”

A different M&A cycle

Recession remains a major uncertainty in a year dominated by doubt.

In past years when recession loomed, M&A often meant fiscally stronger companies buying out distressed operators unable to survive low commodity prices.

That’s unlikely to be the case this time around.

The industry’s widespread adoption of fiscal discipline has strengthened most E&Ps’ balance sheets to withstand harsh economic conditions. As a result, M&A will likely take on a different character in the event of a severe recession or a dramatic plunge in commodity prices.

“I think that is going be different this time because the companies over the last two years have just taken advantage of the high prices to not only ramp up the free cash flow returns to investors, but they've really strengthened their balance sheets,” Scialla said. “I don't think many [operators] are going to be distressed, even if we have a period of sub $50 oil or even $40 oil.”

Nor would most companies be willing to sell assets in such a price environment.

“Most prognosticators now are anticipating a recession, which I think is fine given where we've been the last few years and makes sense. You've had free money; at some point you’ve got to pay for it.” – Mike Scialla, Stephens

“That would definitely, this cycle, slow things down,” he said. “If it's going to be a deep recession that causes price retrenchment to that extent, then I think M&A does slam on the brakes.”

Scialla said he envisions a scenario in which the economy is sluggish but not “too terrible.” But dealmakers still want clarity on macro issues, including interest rates, the Russia-Ukraine war and a better idea of how China is wrestling with a COVID resurgence.

“Most prognosticators now are anticipating a recession, which I think is fine given where we've been the last few years and makes sense. You've had free money; at some point you’ve got to pay for it,” Scialla said.

What matters is the degree, depth and breadth of the recession.

“We’ve just got to get more clarity on that,” Scialla said.

With a clearer view of the market, “you could see more deals getting done in the first quarter next year,” he said. And even in severe recessions, such as 2008, deal activity dipped and then bounced back dramatically.

Regardless of macroeconomics, deals are likely to get done so long as public companies are able to offer cash while the bridging bid-ask spreads with equity, Akunuri said.

And with free cash flow still foremost on the minds of management teams, Scialla said most companies are “probably agnostic” about the basins where they will buy.

“I think that is going to promote consolidation all over the country,” he said.

In 2022, companies felt confident using their excess cash and highly valued stock to make large-scale deals outside of the Permian. Devon Energy, for instance, closed two bolt-on deals valued at $2.66 billion in cash that left some analysts surprised. Devon’s acquisitions included the purchase of Bakken operator RimRock Oil and Gas LP in July and Eagle Ford E&P Validus Energy in September.

Likewise, in early November, Marathon Oil Corp. agreed to acquire Ensign Natural Resources in a $3 billion cash deal that almost doubled the company’s position in the Eagle Ford Shale.

Consolidation seems likely to continue, particularly for companies that have a footprint in an area where a free-cashflow-accretive deal is available and synergies are possible, Scialla said.

“I would still say the Permian's still the biggest, probably the most fragmented of all the basins that would still need to have the most consolidation,” he said. “But I don't think it's necessarily going to dominate like it did for a while.”

Recommended Reading

Air Products Sees $15B Hydrogen, Energy Transition Project Backlog

2024-02-07 - Pennsylvania-headquartered Air Products has eight hydrogen projects underway and is targeting an IRR of more than 10%.

Air Liquide Eyes More Investments as Backlog Grows to $4.8B

2024-02-22 - Air Liquide reported a net profit of €3.08 billion ($US3.33 billion) for 2023, up more than 11% compared to 2022.

Some Payne, But Mostly Gain for H&P in Q4 2023

2024-01-31 - Helmerich & Payne’s revenue grew internationally and in North America but declined in the Gulf of Mexico compared to the previous quarter.

Uinta Basin: 50% More Oil for Twice the Proppant

2024-03-06 - The higher-intensity completions are costing an average of 35% fewer dollars spent per barrel of oil equivalent of output, Crescent Energy told investors and analysts on March 5.

In Shooting for the Stars, Kosmos’ Production Soars

2024-02-28 - Kosmos Energy’s fourth quarter continued the operational success seen in its third quarter earnings 2023 report.