[Editor's note: A version of this story appears in the December 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

There’s no sugar coating it: The U.S. LPG market is oversupplied. With nationwide propane inventories sitting just below record highs, prices at Mont Belvieu are seasonally at some of their lowest levels since 2015. But with gas plant NGL production growth slowing and LPG export capacity slated for another round of expansions next year, an easing of domestic oversupply conditions may soon be in the offing.

Enverus (formerly Drillinginfo Inc.) analyzed the causes of the slowing pace of gas plant NGL production growth as well as the midstream and downstream changes that will allow for higher U.S. exports of LPG in the year ahead. Enverus believes these trends point to a more constructive outlook for the domestic LPG market next year.

Slowdown in production growth

With oil and gas prices under pressure, E&P companies throughout the U.S. have been dialing back capex in order to focus on generating free cash flow. This trend is likely to continue into 2020. Since NGL is produced alongside crude oil and natural gas, any slowdown in drilling plans will certainly impact NGL production as well.

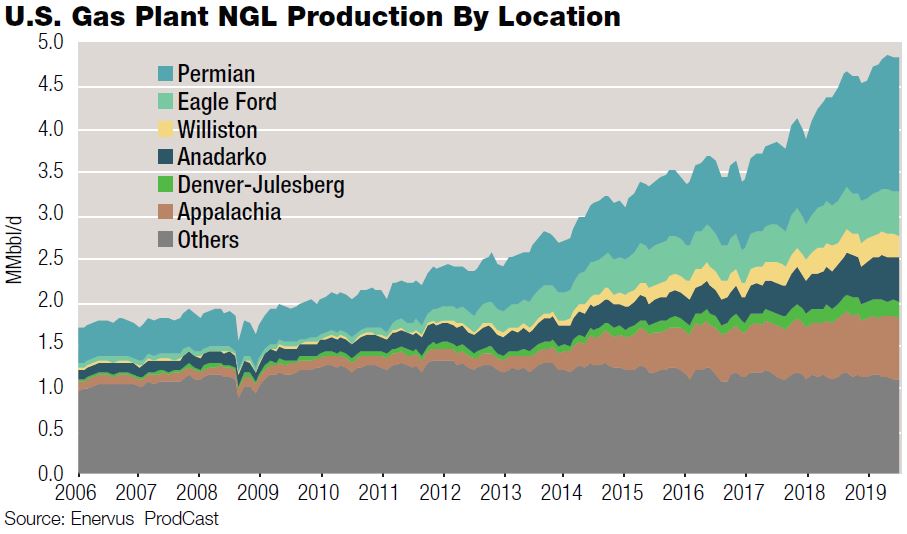

Approximately 30% to 35% of gross gas produced in the U.S. is associated gas, and the bulk of that associated gas is being produced in a handful of tight oil plays in the Permian, Williston, Anadarko and Denver-Julesburg basins, as well as the Eagle Ford play in southern Texas. As such, it should come as no surprise that the majority of NGL production growth in recent years has also been sourced from these locations.

The Permian Basin stands out as a major growth driver, making up nearly 40% of the expansion in total NGL production in the U.S. during the past 10 years. Superior economics are the main reason for this, with West Texas Intermediate (WTI)-equivalent half-cycle breakeven thresholds clustering in a range from the low $30s to high $40s per barrel (bbl) for the Delaware Basin and between $40 and $55 in the Midland Basin. Even as global crude prices soften due to a cooling global economic growth outlook, these low breakeven thresholds should keep upstream activity in the Permian moving forward. Although one can find a few exceptions, production economics are generally less advantageous in nearly every other tight oil play in the U.S., and rig counts have been trending downward.

This brings us to the topic of gas plant LPG production. Compared to 2017, growth was strong in 2018, clocking in at just under 250,000 bbl/d. This was roughly on par with the surge in production seen in 2015. It is worth noting that the average price of front-month WTI futures in 2018 was just under $65/bbl and touched intra-day highs of nearly $77/bbl. In short, the economics for drilling were good last year, at least until prices dropped into the low $40s in the fourth quarter. The price of WTI crude has since recovered to the mid-$50s but has struggled to gain much traction beyond that.

Thanks to the prior year’s drilling momentum, gas plant LPG production for the full year of 2019 is still expected to be up on average by 225,000 bbl/d vs. 2018. That momentum has since been spent though, leading to a slowing of production growth in the second half of the year. Total U.S. gas plant production of propane, normal butane and isobutane totaled 2.26 MMbbl/d in January 2019, up 330,000 bbl/d when compared to January 2018. In September, that annual rate of growth slipped to 139,000 bbl/d, according to preliminary data collected by Enverus.

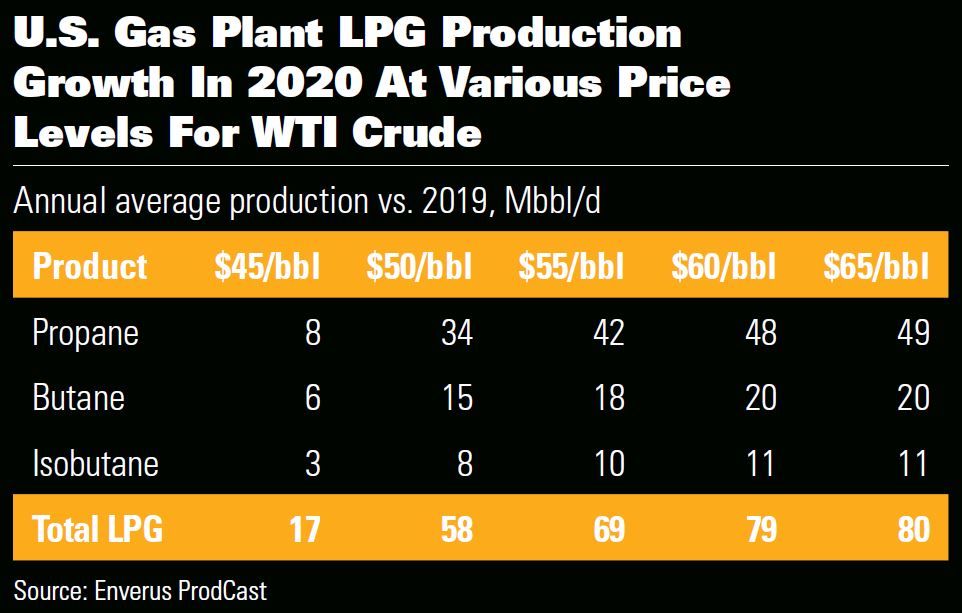

That growth rate is likely to slow even more in the months ahead. Figure 3 shows annual average increases in U.S. gas plant production of propane, normal butane and isobutane under various price scenarios for WTI crude in 2020. Front-month WTI futures have been trading between $51/bbl and $56/bbl in October, and market bias has been mostly to the downside. Even the surprise attack on Saudi oil facilities on Sept. 14 did not leave a lasting mark on oil prices. Since then, the market has shrugged off other geopolitical events as well, such as the purported missile attack on an Iranian oil tanker and the uprising in Ecuador that temporarily shut the Trans-Ecuadorean Pipeline.

All macro indicators point to a softening oil market, and that spells slower production growth for NGL in the U.S. tight oil patch as upstream capex is crimped.

LPG export capacity additions

Given domestic LPG demand averaging 1.4 MMbbl/d, the U.S. is on track for a 2019 average surplus of just over 1.6 MMbbl/d. With domestic markets well-supplied, these surplus barrels need to find a home in the international cargo market or else they will end up getting parked in storage.

Such is the rate of U.S. production growth during the past two years that both inventories and exports are trending up. Indeed, weekly propane inventories reported by the Energy Information Administration (EIA) are close to levels not seen since the record highs set in November 2015. According to the EIA, LPG exports hit a record 1.47 MMbbl/d in June. Arguably, LPG exports would have continued at or near those levels through the summer if not for Hurricane Barry and Tropical Storm Imelda.

Vessel tracking indicates total LPG exports averaged just under 1.3 MMbbl/d from July through September, and have averaged just more than 1.4 MMbbl/d in the first three weeks of October.

The October start-up of Enterprise Products Partners’ 175,000 bbl/d Houston Ship Channel expansion project helps explain part of the recent increase in export volumes. The facility, the largest in the U.S., already boasted a nameplate capacity of 660,000 bbl/d before the expansion. Enterprise’s LPG exports averaged just under 465,000 bbl/d out of the facility in September, ticking up to 580 MMbbl/d in the first three weeks of October this year.

Targa’s Galena Park export terminal may also see a boost in its effective capacity with the recent completion of the Dock 2 rebuild. Galena Park’s capacity was just over 230,000 bbl/d at the end of September, but Targa’s management believes that it could increase by 70,000 to 100,000 bbl/d before the end of the fourth quarter.

Further expansions are planned at Enterprise, bringing online another 260,000 bbl/d of export capacity in late 2020. This would boost total capacity at the facility to just under 1.1 MMbbl/d. Targa also aims to boost export capacity at Galena Park late in the third quarter of next year, with capacity potentially reaching 500,000 bbl/d, according to recent company statements. Not to be left out, Energy Transfer plans to increase capacity at its Port Arthur export terminal by around 200,000 bbl/d in the fourth quarter of 2020. Energy Transfer also aims to expand Marcus Hook by 40,000 bbl/d around the same time.

If all these projects are finished on time next year, total U.S. LPG export capacity could exit 2020 at just over 2.6 MMbbl/d, up from nearly 1.7 MMbbl/d at the end of September. Of course, none of this would amount to a hill of beans if fractionation capacity remains as tight as it is today. That, however, is set to change next year as well; indeed, 10 projects totaling 1.35 MMbbl/d of incremental fractionation capacity are planned to come online between March and December.

With export and fractionation capacity both looking unconstrained next year, inventories should end next year in a better place than they are today.

A tighter domestic supply/demand balance

From a purely market fundamentals standpoint, the combined effect of slowing production and increased export capacity should be constructive for markets.

Indeed, a significant amount of newly constructed export and fractionation capacity could even go unused in the first year of operation if production growth stagnates. This is a recipe for a tighter Gulf Coast spot market as larger volumes move across the dock inside of committed economic tranches.

However, this potential tightening in U.S. market fundamentals should be taken with some amount of caution amid worrying signs of a global macroeconomic slowdown. If global manufacturing slips into recession, petrochemical feedstock demand may come under additional pressure. If this happens, the increase in U.S. LPG export capacity risks transferring the domestic glut to the global cargo market.

Jesse Mercer is senior director of crude market analytics for Enverus’ strategy and analytics group. Prior to joining Enverus (formerly called Drillinginfo Inc.), Mercer was the crude oil trading strategist for the Americas at Phillips 66 Co.

Recommended Reading

US Drillers Add Oil, Gas Rigs for First Time in Five Weeks

2024-04-19 - The oil and gas rig count, an early indicator of future output, rose by two to 619 in the week to April 19.

Strike Energy Updates 3D Seismic Acquisition in Perth Basin

2024-04-19 - Strike Energy completed its 3D seismic acquisition of Ocean Hill on schedule and under budget, the company said.

Santos’ Pikka Phase 1 in Alaska to Deliver First Oil by 2026

2024-04-18 - Australia's Santos expects first oil to flow from the 80,000 bbl/d Pikka Phase 1 project in Alaska by 2026, diversifying Santos' portfolio and reducing geographic concentration risk.

Iraq to Seek Bids for Oil, Gas Contracts April 27

2024-04-18 - Iraq will auction 30 new oil and gas projects in two licensing rounds distributed across the country.

Vår Energi Hits Oil with Ringhorne North

2024-04-17 - Vår Energi’s North Sea discovery de-risks drilling prospects in the area and could be tied back to Balder area infrastructure.