Brazil is the biggest oil-producing country in South America. (Source: marchello74/Shutterstock.com)

Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

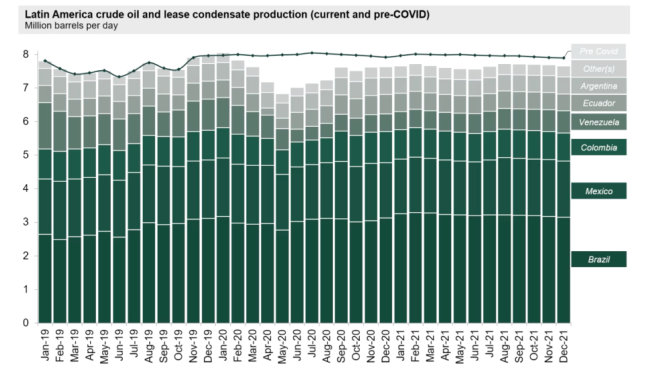

The effect of the coronavirus pandemic on Latin America’s oil market and a pullback in spending by oil companies prompted analysts to revise down expected 2020 oil production by about 550,000 bbl/d for the region.

The downward revision by Rystad Energy analysts came as both national oil companies (NOCs) and independents deferred some new development, exploration and brownfield activity.

“Now we expect 2020 production to average at about 7.4 to 7.5 million barrels a day,” Aditya Ravi, vice president of Rystad’s global E&P research team, said during a recent webinar. “And because of lack of investment, we’re also seeing that the overall decline rates on the legacy production has accelerated a bit, or at least in the past nine months.”

Data from Rystad shows oil production in the region fell by 1.2 MMbbl/d through September with Brazil, the biggest oil-producing country in South America, leading in cuts.

Brazilian state-owned oil company Petrobras cut its capex by 35%, mostly from brownfield projects. Meanwhile other NOCs—Colombia’s Ecopetrol SA and Argentina’s YPF SA—cut their investment levels by 40% and 30%, respectively.

Independents such as Frontera Energy Corp., Parex Resources Inc., GranTierra Energy Inc. and GeoPark Ltd. chopped capex by more than half or close to 70% in some cases, Ravi said. Canacol Energy Ltd.’s estimated capex was expected to fall by only about 5%, which he said was due to the company’s gas heavy portfolio and long-term contracts.

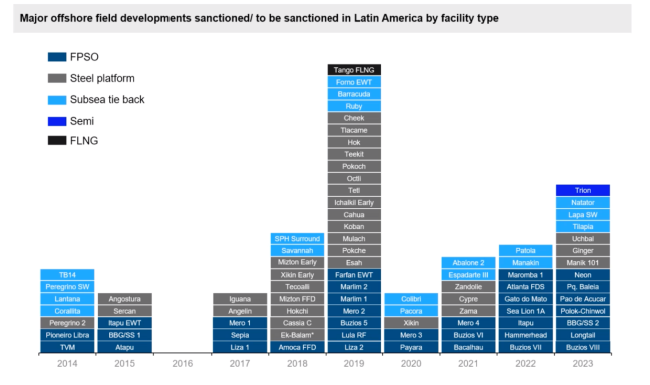

Among the project deferrals are Petrobras’ planned Parque das Baleia development targeting the Jubarte Field, sanctioning of the Talos Energy Inc.-operated Zama development and Brazilian independent Enauta Participacoes SA’s Atlanta heavy oil development to name a few.

The slowdown is also evident onshore, especially in the Vaca Muerta shale play. The number of horizontal wells put on production plummeted to five in the second quarter, down from 41 in the first quarter. Rystad estimates 12 horizontal wells in the Vaca Muerta Shale will start production in the third quarter.

“Activity for the remainder of the year is also expected to be grim,” Ravi said.

Hopes are for Latin American oil production to rise in 2021 to average about 7.65 MMbbl/d as upstream revenues rise on improved market conditions.

Deepwater developments are also expected to boost activity in the medium term, according to Ravi, who highlighted activity around Petrobras’ Mero and Buzios fields next year.

In 2022, “we expect close to about seven FPSOs being sanctioned for development in Brazil and Ghana with Petrobras is taking on two of them and the rest of them coming from other operators,” including ExxonMobil Corp.-led Hammerhead development offshore Guyana.

Just as many FPSOs are forecast for 2023.

Looking at cost of supply, developments nearing sanction within five years offshore Brazil and Guyana have competitive breakevens.

“What we see from Brazil is that about close to 1.4 million barrels [per day] of crude production … that is expected to be sanctioned has a breakeven of less than $40,” Ravi said. “And almost all of Guyana’s new production that is expected to be sanctioned in the next four to five years is also expected to have a breakeven of less than $40 a barrel.”

Recommended Reading

Tech Trends: AI Increasing Data Center Demand for Energy

2024-04-16 - In this month’s Tech Trends, new technologies equipped with artificial intelligence take the forefront, as they assist with safety and seismic fault detection. Also, independent contractor Stena Drilling begins upgrades for their Evolution drillship.

AVEVA: Immersive Tech, Augmented Reality and What’s New in the Cloud

2024-04-15 - Rob McGreevy, AVEVA’s chief product officer, talks about technology advancements that give employees on the job training without any of the risks.

AI Poised to Break Out of its Oilfield Niche

2024-04-11 - At the AI in Oil & Gas Conference in Houston, experts talked up the benefits artificial intelligence can provide to the downstream, midstream and upstream sectors, while assuring the audience humans will still run the show.

Haynesville’s Harsh Drilling Conditions Forge Tougher Tech

2024-04-10 - The Haynesville Shale’s high temperatures and tough rock have caused drillers to evolve, advancing technology that benefits the rest of the industry, experts said.