At the manmade Island D hub at the Kashagan Field in the Caspian Sea, liquids and gas will be initially separated for piping onto the shore facility. (Source: Eni)

Kazakhstan marked long-awaited milestones in October at the gigantic Kashagan oil field in the Caspian Sea, starting production from Phase One of the offshore development and shipping the first batch of crude for export from its onshore processing plant.

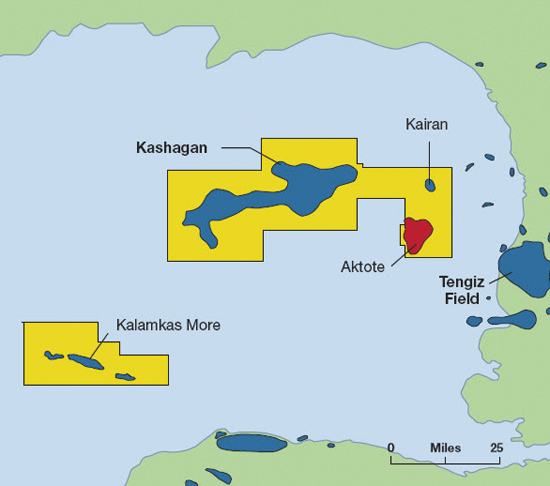

But the feat, part of efforts to develop between 7 billion barrels (Bbbl) and 9 Bbbl of reserves from the Kashagan, Kashagan Southwest, Kalamkas, Aktote and Kairan fields, has not come without challenges. The discovery was made more than 16 years ago, but developers had to overcome technical difficulties associated with:

- High-pressure reservoirs with high sour gas content;

- Freezing weather conditions including pack ice that created logistical obstacles, which led to construction of artificial islands to house drilling equipment, processing facilities and staff; and

- Pipeline leaks that brought production to a halt in 2013. The culprit was apparently corrosion from high sulfur. Pipe replacement made way for the production restart.

Costs for the development have swelled to about $50 billion as the oil and gas industry copes with lower commodity prices, leaving analysts to ponder the chances for capex recovery for project partners.

Operated by the North Caspian Operating Co. (NCOC), partners in the consortium developing the field include KazMunayGas with 16.88%; Eni, ExxonMobil Corp. (NYSE: XOM), Royal Dutch Shell Plc (NYSE: RDS.A) and Total, each with 16.81%; CNPC with 8.33%; and Inpex with 7.56%.

While recent developments are seen as positives for Kazakhstan—boosting its economy, raising production tallies and fattening up oil supplies that potentially will be exported to Europe and China—the same remains to be seen for investors.

RELATED LINK: A Different Kind Of Pressure

“It will be a challenge for partners to recover their investment in the project under our oil price projections, making an expansion of the project unlikely given other risks,” Fitch Ratings said in a report Oct. 21. “As for many other mega- oil- and-gas projects launched over the last couple of years, it will be difficult for Kashagan to recover its [US$50 billion-plus] capex based on our long-term Brent price assumption of [US$65/bbl], despite the weak tenge [Kazakhstan currency].”

Fitch said it is possible that the consortium will delay making decisions on potential expansions. Or, the project may not go forward at all “if oil prices do not rebound more strongly from current levels, given the project complexity and the more conservative approach to mega-projects by the majors.”

Future phases of the project are still under concept selection, NCOC has said.

However, the speed of production growth will be a factor due to the added challenge of the world’s hydrocarbon glut.

“With all gathering and processing infrastructure in place for a 2013 start, including 20 predrilled production wells, Kashagan could have captured the upside of record high oil prices if production continued as planned,” Anna Belova, oil and gas senior analyst for GlobalData, said in a statement.

“Instead, the project restarted in today’s oversupplied market. And while prices rebounded, they would not justify Kashagan’s full-cycle capex, which exceeds US$47 billion to date. … The key to realizing favorable present value metrics for Kashagan centers on the project’s ability to quickly build up production.”

Work continues toward increasing production to a targeted 370 Mbbl/d by year-end 2017, according to the operator. During Phase One, about half of the gas produced will be reinjected into the reservoir. The rest will transported via pipeline to the Bolashak onshore processing plant where oil will be produced, the company has said, noting some of the gas will also be used to power the processing plant.

However, “upstream developments recognize two limiting factors to production,” Belova said. “Processing and export capacities often dictate hydrocarbon quantities that reach markets from a given asset. Production well performance and drilling campaign execution similarly provide an upper limit for production.”

Citing the Kazakh Energy Ministry, Belova said about 90 Mbbl/d are being produced from four reactivated wells at Kashagan. If the performance of 16 more production wells, which have been awaiting the start of production since 2012, equals that of the first four wells, the 495 Mbbl/d processing capacity will not be a constraining factor, she said.

“With a large number of predrilled wells and a multistage processing buildup, Kashagan is well positioned to reach its targeted capacity for Phase One by 2018,” Belova said. “This paves the way for negotiations on full-field development that has a potential to bring over 1.1 [MMbbl/d] to global crude markets.”

Velda Addison can be reached at vaddison@hartenergy.com.

Recommended Reading

NAPE: Turning Orphan Wells From a Hot Mess Into a Hot Opportunity

2024-02-09 - Certain orphaned wells across the U.S. could be plugged to earn carbon credits.

Exxon Versus Chevron: The Fight for Hess’ 30% Guyana Interest

2024-03-04 - Chevron's plan to buy Hess Corp. and assume a 30% foothold in Guyana has been complicated by Exxon Mobil and CNOOC's claims that they have the right of first refusal for the interest.

Petrobras to Step Up Exploration with $7.5B in Capex, CEO Says

2024-03-26 - Petrobras CEO Jean Paul Prates said the company is considering exploration opportunities from the Equatorial margin of South America to West Africa.

The OGInterview: How do Woodside's Growth Projects Fit into its Portfolio?

2024-04-01 - Woodside Energy CEO Meg O'Neill discusses the company's current growth projects across the globe and the impact they will have on the company's future with Hart Energy's Pietro Pitts.

Deepwater Roundup 2024: Offshore Australasia, Surrounding Areas

2024-04-09 - Projects in Australia and Asia are progressing in part two of Hart Energy's 2024 Deepwater Roundup. Deepwater projects in Vietnam and Australia look to yield high reserves, while a project offshore Malaysia looks to will be developed by an solar panel powered FPSO.