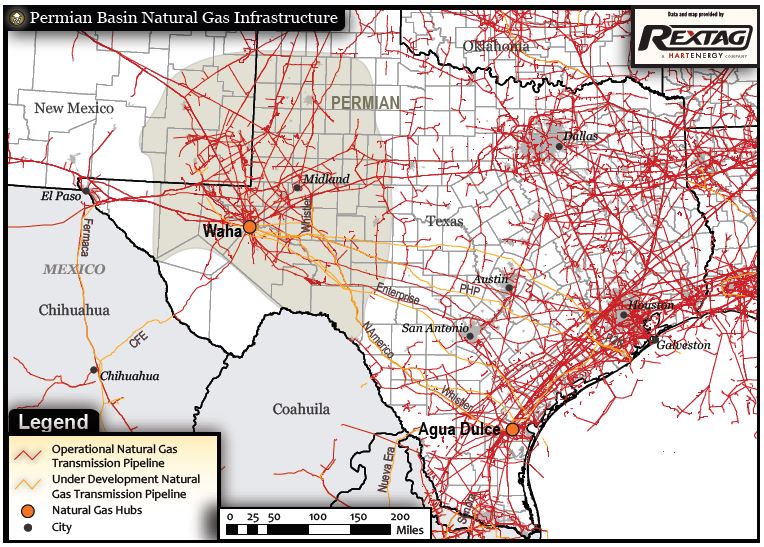

As the fourth quarter began, Kinder Morgan launched full commercial service along its joint-venture Gulf Coast Express (GCX) gas pipeline ahead of schedule. The line runs from the Permian Basin’s Waha gas pipeline to the Agua Dulce hub near the Texas Gulf Coast. Fully subscribed under long-term contracts, GCX provides 2 billion cubic feet per day (Bcf/d) of incremental gas capacity, which will help relieve existing Permian gas takeaway constraints and reduce flaring.

“We had more than 3,000 contractors deployed at times and more than 6 million contractor hours worked, all without a major safety incident during the construction phases of the project,” said Sital Mody, Kinder’s president of natural gas midstream. Kinder Morgan owns a 34% interest in GCX and is the operator of the pipeline. Other equity holders include Altus Midstream, DCP Midstream and an affiliate of Targa Resources.

Gulf Coast Express is the first of the three Permian pipelines planned by Kinder Morgan. The Permian Highway Pipeline will add another 2 Bcf/d of capacity by the end of next year. And still to come is the Permian Pass, which has yet to reach final investment decision. The decision will be contingent on demand from producers, but Kinder management has indicated that the project is moving along.

Production progress

The Permian’s August gas production of 14.7 Bcf/d is nearly twice that of production just three years ago. Natural gas prices at Waha have traded at an average discount of $1.81/MMBtu to the industry-standard Henry Hub in Louisiana this year and even fell into negative territory, signaling a need for additional takeaway capacity, according to energy infrastructure analyst firm Alerian.

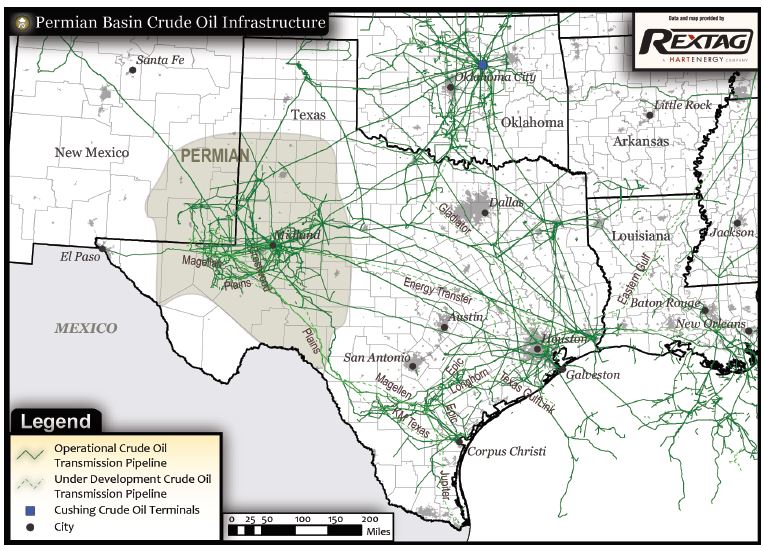

Crude production in the Permian has more than quadrupled since 2011, and the basin is now, on its own, the fifth-largest producer of crude in the world, according to a recent report from Alerian. Total Permian crude production was over 4.3 million barrels per day (MMbbl/d) in August, a nearly 20% increase from just a year ago, and production growth is expected to continue.

Before recent pipeline additions, estimated Permian takeaway capacity was roughly 3.6 MMbbl/d.

“The Permian has long faced a lack of takeaway capacity due to its rapid growth, but new long-haul pipelines are finally coming online to provide an outlet for crude production,” wrote Bryce Bingham, Alerian research analyst. “While these capacity additions helped ease the Permian bottleneck, additional takeaway capacity was, and still is, required to meet rapid production growth.”

Two major Permian pipeline projects began service in August, helping to ease the basin’s takeaway constraints and providing further sources of stable cash flows for midstream companies. Crude oil shipments began just days apart on Plains All-American’s 670,000 bbl/day (Mbbl/d) Cactus II line and on Epic Midstream’s Y-grade (mixed NGL) pipe.

Together they added more than a million barrels a day from the Permian to the Gulf Coast. Another 2 MMbbl/d planned to be added by 2022. (See adjoining chart.)

Everyone in the pool

Technically, the Epic Y-grade line has only been temporarily converted to crude service. It will revert to NGL in January after Epic puts into service a dedicated 600 Mbbl/d line. That is scheduled to take place just a little after Enbridge and Phillips 66 Partners put into service the 900 Mbbl/d Gray Oak Pipeline.

At the other end of the line, NuStar Energy loaded the first shipment of Permian crude for export from its Corpus Christi, Texas, terminal in the third quarter. NuStar had only recently completed a project connecting a pipeline in South Texas to Cactus II.

U.S. crude exports have surged to a monthly record of greater than 3 MMbbl/d.

NuStar also said it was nearing completion of connections between its South Texas Pipeline System to two other long-haul pipelines that would also move barrels from the Permian to South Texas. The company said it was in discussions with both Epic and Phillips 66 Partners regarding connections to those lines.

Phillips 66 ranks No. 15 on this publication’s Midstream 50 of the sector’s largest publicly held firms.

The beat goes on with the Wink to Webster Pipeline, a group effort that is slated to add a further million barrels a day of transportation in 2021. The partners in that line read like a Who’s Who of upstream, midstream and downstream: ExxonMobil, Plains All American, MPLX, Delek, Lotus Midstream and Rattler Midstream.

“Not only does additional infrastructure coming online benefit midstream companies, it has supported crude prices at Midland,” wrote Bingham. “Crude spreads widened significantly last year as a result of inadequate pipeline capacity and rapidly growing production but have since narrowed significantly.”

Crude at Midland was trading at a $0.35/bbl premium to West Texas Intermediate at the Cushing, Okla., pipeline and trading hub at the end of the third quarter.

“That is a dramatic shift from a nearly $18/bbl discount in August 2018,” noted Bingham. “Houston-to-Midland differentials have also narrowed to $3.45/ bbl after blowing out to nearly $24/bbl last summer.”

In April, EagleClaw Midstream, a portfolio company of Blackstone Energy Partners and I Squared Capital, made the final investment decision on its proposed Delaware Link pipeline to transport residue natural gas from the Permian’s Delaware Basin to Waha, with access to further downstream takeaway connections. I Squared Capital is an independent global infrastructure investment manager focusing on energy, utilities, telecommunications and transport in the Americas, Europe and Asia. The firm has offices around the world.

Delaware Link is expected to be anchored by residue volumes from EagleClaw’s processing facilities, as well as third-party customers. The approximately 1.2 Bcf/d, 40 mile, 30-inch diameter pipeline will originate at EagleClaw’s three existing natural gas processing complexes in Reeves County, Texas—East Toyah, Pecos and Pecos Bend. Even as the decision was made to proceed, Blackstone noted the level of producer inquiry and is already considering increasing the pipeline’s diameter and capacity.

Planned interconnections include direct access to the Permian Highway Pipeline, a planned 2.1 Bcf/d gas line from Waha to the Gulf Coast and other markets. Permian Highway is a joint venture of Kinder Morgan, EagleClaw, Apache and another undisclosed anchor shipper. It is expected to be in service in the second half of 2020.

EagleClaw claims primacy as “the largest natural gas gatherer and processor in the southern Delaware Basin.” EagleClaw is a partner with Targa on the Grand Prix Pipeline Project and with Kinder Morgan on the Permian Highway Pipeline Project. EagleClaw has long-term dedications for gas, crude and water midstream services in place over half a million acres from more than 25 successful and active producers in the Delaware Basin.

Flare for the dramatic

The Gulf Coast Express announcement by Kinder Morgan was as notable for what it mentioned as what it did not.

Kinder Morgan is one of the big dogs of midstream—ranked No. 3 on the Midstream 50—and its push to get gas transportation into service signals that the sector is serious about getting all Permian molecules to market, not just oil.

It is also notable that Mody stressed the importance of the new pipe as part of the effort to reduce gas flaring. It would have been easy to stick with banalities about export opportunities, especially given the number of liquefied natural gas (LNG) terminals being built and expanded along the Gulf Coast. Indeed, Kinder Morgan is leading one itself.

The Federal Energy Regulatory Commission (FERC) approved Kinder Morgan’s request to start commercial operations at Train 1 of the company’s Elba Island LNG complex in Georgia as the fourth quarter began. FERC approved the request to “commence service for liquefaction and export activities.” Elba Island won’t directly impact the Permian, of course, but is another example of the boom in U.S. LNG exports.

The facility experienced start-up problems that led to periodic delays since late last year as it tweaked the setup of its 10 trains. In total, they will produce around 3 million tonnes per year when up and running. The U.S. had exported 26 million tonnes of LNG through September, exceeding its 2018 total of 22 million tonnes with the fourth quarter to go.

That puts the U.S. into a tie with Malaysia for third place among global LNG exporters—quite a change from zero LNG exports less than a decade ago.

The blight

Flaring of associated gas has been the blight on the escutcheon of the Permian success story for years. In recent months, the pressure to address that has been increased as some upstream leaders have spoken publicly about it. The pivot point on the issue may have been a recent decision by the Texas Railroad Commission.

Ironically, the commission ruled 2-1 that a producer could flare and did not have to put associated gas into a nearby gathering system. Still, the split decision was made on narrow grounds in favor of a struggling producer and against a large national midstream operator.

Arguments in the case clearly showed regulators’ patience is running out for flagrant flaring. Though natural gas pipelines providing additional takeaway capacity are welcomed, low natural gas prices, pipeline takeaway commitments and other economic factors remain an issue when it comes to flaring of gas, according to Scott Sheffield, Pioneer Natural Resources president and CEO.

“That’s the biggest issue we have to solve with the producers and with the pipeline companies,” Sheffield said during a recent Permian-focused event hosted by the Center for Strategic & International Studies. “And the states probably need to do a better job of putting more pressure on both groups of people, in my opinion, to solve that problem. We should be adding 21 Bcf/d of natural gas lines. We’re only adding six, so this flaring issue is not going away with these three new pipelines.”

Chevron has had a no-flaring company policy since 2008, according to another panelist, Stephen Green, president of Chevron North America E&P.

“That doesn’t mean you won’t ever see a Chevron facility that has a flare. We do have to use them for safety and operational issues,” Green said. “But we don’t bring on production with flaring as a routine part of the operations.”

Both Green and Sheffield acknowledged economic challenges surrounding the flaring issue and how it impacts operators in different ways.

“But as an industry this is an issue that we have to come to grips with and figure out how to address for the long term,” Green said.

Produced water

One of the ironies of prodigious Permian production is that it generates both fire and water at the same time: too much associated gas that ends up going up in smoke, as well as vast seas of produced water.

As producers, midstream operators and regulators struggle to reduce flaring, there is a broad effort to expand and integrate water-gathering systems.

At present most are focused on disposal wells, but there is progress on reuse and recycling. Both of the Permian’s cities, Midland and Odessa, have struck deals to treat produced water as a way of tying the resources of the region to its population centers.

NGL Energy (NGLEP) closed an equity deal to acquire Hillstone Environmental Partners, a water midstream company, from Golden Gate Capital for about $600 million at the end of the third quarter. Hillstone operates water-pipeline and -disposal infrastructure to producers in the Delaware, with a core operational focus in the stateline area of southern Eddy and Lea counties, N.M., and northern Loving County, Texas. NGLEP acquired another water midstream firm, Mesquite, in July.

Hillstone has a fully interconnected, produced-water pipeline transportation and disposal system. It comprises 19 saltwater disposal wells with total permitted disposal capacity of 580 Mbbl/day. The newly built network of produced-water lines has a transportation capacity of about 680 Mbbl/day. NGLEP owns and operates a vertically integrated energy business with four primary businesses: crude logistics, water and liquids, as well as refined products and renewables.

Hillstone also has an additional 22 permits to develop another 660 Mbbl/ day of disposal capacity. NGLEP expects to integrate the Hillstone system into its existing Delaware Basin operations. All of the water on Hillstone’s Northern Delaware Basin system is delivered via multiple pipes. Hillstone also has an aggregate of more than 110,000 acres contracted under long-term dedications with priority disposal rights or minimum volume commitments.

“This transaction is highly complementary to our Delaware Basin operations,” said Mike Krimbill, CEO of NGLEP. “It not only adds a redundant, interconnected produced-water pipeline system with significant permitted disposal capacity that fits perfectly within our existing footprint, but importantly, it also supports our ongoing strategy of increasing our cash flow predictability.”

Doug White, the firm’s executive vice president of water, added, “The integration of the Mesquite assets is fully underway and providing immediate benefit. The certainty of off-take and reliability of our integrated system of large-diameter pipelines will provide approximately 2.7 million barrels per day of operational disposal capacity in the Delaware Basin, including the addition of Hillstone. The Hillstone assets include long-term contracts with investment-grade producers. The contracts have an average remaining term of greater than 10 years, minimum volume commitments and first-call priority volume commitments that minimize impacts of timing related to recycle and reuse activities.”

Down Mexico way

NuStar is not only active in moving crude out of the Permian but in creating new markets for the basin’s vast production, too. It also is building 600 Mbbl additional tankage at its Corpus Christi terminal. That will take total storage to 3.9 MMbbl completed by the end of the year.

NuStar also recently began moving refined fuels through its expanded Valley Pipeline System in South Texas after another expansion. That line runs from Corpus Christi to the Rio Grande Valley and across the frontier into parts of northern Mexico.

NuStar began moving diesel in particular into Mexico by reactivating its 11-mile, 8-inch refined fuels pipeline from its Laredo, Texas, terminal, crossing the short hop under the Rio Grande (Rio Bravo) to its Nuevo Laredo terminal in Mexico. That is all part of an initiative with Valero to move fuels from Valero’s refineries in Corpus Christi and Three Rivers, Texas.

NuStar ranks No. 24 on the Midstream 50.

Under the sweeping reforms to nearly a century of state control of the petroleum industry in Mexico, many segments of the country have opened to foreign investment. The retail sector has seen the fastest and most extensive participation. In contrast, pipelines and refining have seen little investment.

“Refineries in Texas and California have been targeting northern Mexico for fuels by rail,” said Luis F. Delgado, director of Mexico business development at Delek US, speaking at the Petrochemical and Refining Summit in New Orleans.

“Barges are not considered viable because there are no real navigable rivers, and pipelines are subject to sabotage and theft. The government recently turned off the pipelines to discourage the rampant illegal tapping, but the distribution system only has a two-day supply,” Delgado told Midstream Business.

Until 2014, the six aging refineries operated by state energy company Petroleos Mexicanos (Pemex) were able to produce about half the fuels and other refined products that the country needed. At that point, inefficiency and years of deferred maintenance caught up with Pemex. Today, Mexico imports 70% of its fuels because the refineries are operating at an aggregate 40% of nameplate capacity.

That might seem like an opportunity for North American midstream operators, but they have been reluctant to invest.

In contrast, there are now more than two dozen companies with retail stations in Mexico in direct competition with Pemex at the fuel pump, according to Delgado. They have more than 1,700 stations and represent about 15% of the market. That penetration only took four years.

Mexican president Andrés Manuel López Obrador, universally known by his acronym, AMLO, opposed the petroleum reform laws, but they took effect before he assumed office. His main initiative has been to push a plan for a greenfield refinery, estimated to cost US$8 billion, in Paraíso, Tabasco.

As reported in October by the Financial Times, the planned refinery, beside the Dos Bocas port, is much more than just a prestige project. It is a powerful symbol of the new economy López Obrador wants to build: state-directed, centrally driven, reliant on national production and free of foreign influence.

However, “many businesspeople, former senior government officials, ex-Pemex executives and investors believe the rescue strategy for the oil company is deeply flawed,” the newspaper reported. “The likely outcome of the plan, they say, will be missed targets and wasted resources. That could lead to downgrades of both the company’s and Mexico’s sovereign debt and risk further economic stagnation.”

Pemex is Mexico’s biggest company by revenue and Latin America’s second largest, according to the story. But it is also a record-breaker for the wrong reasons: Its $104 billion of loans makes it the world’s most indebted oil company, while its workforce of 125,000 is more than double that of Petrobras, its Brazilian state-controlled rival, whose revenues are 10% higher.

“A lot of that labor force is more of a burden than an asset,” said Valérie Marcel, an expert on national oil companies at Chatham House in London. “The lack of investment in skills is a big issue.”

Mexico also provides an important gas market for the Permian—although growth has not come as quickly as many expected. Platts noted recently that gas exports across the border had ticked up to just less than 6 Bcf/d.

The longer view

The current relief over new transportation capacity is very much a short term view, said John Coleman, Wood Mackenzie’s principal analyst of North American crude.

“There will be excess capacity. But looking beyond the next five years, we expect growth to continue, driving the need for either one new [line] from the Permian to the Gulf Coast or expansion, probably across multiple systems.”

Coleman noted that between now and then, the Permian Basin is likely to see a moderate overbuilding in the early 2020s as the current wave of pipeline investments is completed.

Crude capacity from the Permian to the U.S. Gulf Coast is likely to tighten as production growth expands well into the 2030s, and Coleman suggested that if new pipe is not added in the Permian by the mid-2030s, takeaway will become a major concern again. Without more investment, the Permian-to-Gulf Coast pipelines could surpass 92% of capacity.

That eventuality would all but force pipeline expansions or greenfield capacity, he added.

Wood Mackenzie forecasts production in the Permian to peak at around 7.1 MMbbl/d by the late 2020s or early 2030s. Although, the firm’s outlook differs with predictions from another analyst with the Bank of America Merrill Lynch, who predicts that production will triple to 9 MMbbl/d in the next three years and sees the current substantial infrastructure investment to raise concern of overbuilding.

Recommended Reading

Rhino Taps Halliburton for Namibia Well Work

2024-04-24 - Halliburton’s deepwater integrated multi-well construction contract for a block in the Orange Basin starts later this year.

Halliburton’s Low-key M&A Strategy Remains Unchanged

2024-04-23 - Halliburton CEO Jeff Miller says expected organic growth generates more shareholder value than following consolidation trends, such as chief rival SLB’s plans to buy ChampionX.

Deepwater Roundup 2024: Americas

2024-04-23 - The final part of Hart Energy E&P’s Deepwater Roundup focuses on projects coming online in the Americas from 2023 until the end of the decade.

Ohio Utica’s Ascent Resources Credit Rep Rises on Production, Cash Flow

2024-04-23 - Ascent Resources received a positive outlook from Fitch Ratings as the company has grown into Ohio’s No. 1 gas and No. 2 Utica oil producer, according to state data.

E&P Highlights: April 22, 2024

2024-04-22 - Here’s a roundup of the latest E&P headlines, including a standardization MoU and new contract awards.