Depressed equity prices may inhibit future distribution growth.

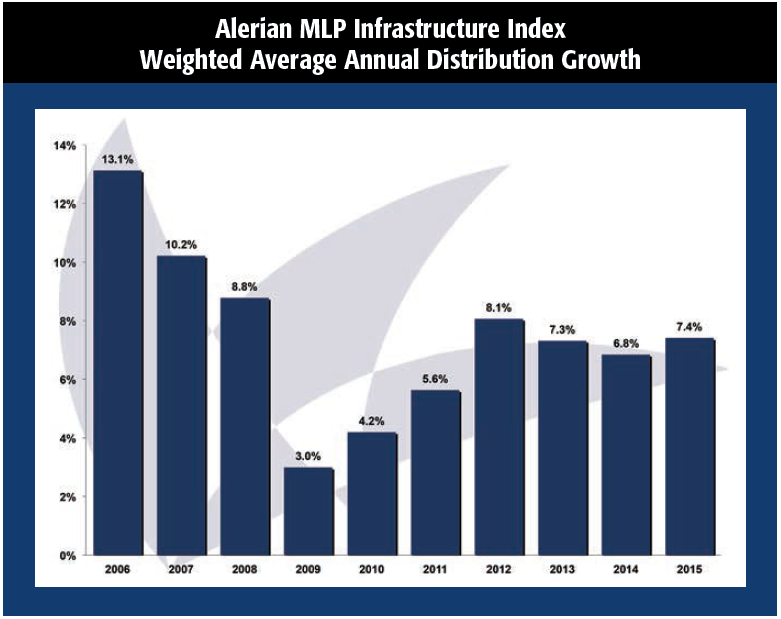

No one reading this magazine will be surprised to learn that the Alerian MLP Infrastructure Index (AMZI) fell 56.4% peak-to-trough over the past 18 months. The investors who traded MLPs in that fashion may or may not have realized that in 2014, midstream MLPs raised distributions 6.8%, and in 2015, distributions grew 7.4%.ribution growth.

Since MLPs pay out nearly all cash flow to investors, to grow they need alternative sources of capital. With unit prices cut in half, funding growth projects with equity is prohibitively expensive. While 82% of the companies in the AMZI (by weight) are investment grade, debt financing is still open to them, although only so much debt can be used before leverage ratios begin to worry ratings agencies.

Those midstream MLPs with volumetric exposure may see their EBITDA levels falling, impacting leverage ratios even before using additional debt. And there are many smaller midstream companies without investment-grade ratings that are not tracked by the AMZI—the debt markets may be closed to these companies entirely.

Still, thanks to projects begun in the past few years and coming online now, midstream companies in the AMZI were able to maintain distribution growth.

Moving forward, they’ll have to get creative. Plains All American Pipeline LP used a convertible preferred equity offering to satisfy capital needs in 2016 (and part of 2017). Williams Partners LP decided to sell assets to the tune of $1 billion in the first half of the year. Energy Transfer Partners LP has followed the most popular route: reducing growth capital spending. By eliminating $750 million of spending, it reduced 2016 growth capex requirements by 15%. Enable Midstream Partners LP has also delayed projects, allowing it to reduce growth spending by 66%.

The MLPs that have announced distribution growth for 2016 or further have been able to do so for one of two reasons:

• Historically high coverage ratios enable them to grow with retained cash flow, examples include Enterprise Products Partners LP and Magellan Midstream Partners LP; or

• A supportive general partner, examples include MPLX LP and EQT Midstream Partners LP.

For the rest of the midstream universe, this may be the start of a harsh cycle. Investors trade down the stocks despite distribution increases. Then, midstream MLPs must cut back on growth spending. Less growth spending means many companies need to maintain their distributions, instead of growing them.

After a period of keeping distributions fl at, midstream companies may be able to grow based on retained earnings. Or they may wait for the capital markets to reopen. In either situation, distribution growth is likely to remain low or fl at for the near and medium term.

Recommended Reading

Report: Freeport LNG Hits Sixth Day of Dwindling Gas Consumption

2024-04-17 - With Freeport LNG operating at a fraction of its full capacity, natural gas futures have fallen following a short rally the week before.

Permian NatGas Hits 15-month Low as Negative Prices Linger

2024-04-16 - Prices at the Waha Hub in West Texas closed at negative $2.99/MMBtu on April 15, its lowest since December 2022.

BP Starts Oil Production at New Offshore Platform in Azerbaijan

2024-04-16 - Azeri Central East offshore platform is the seventh oil platform installed in the Azeri-Chirag-Gunashli field in the Caspian Sea.

US Could Release More SPR Oil to Keep Gas Prices Low, Senior White House Adviser Says

2024-04-16 - White House senior adviser John Podesta stopped short of saying there would be a release from the Strategic Petroleum Reserve any time soon at an industry conference on April 16.

Core Scientific to Expand its Texas Bitcoin Mining Center

2024-04-16 - Core Scientific said its Denton, Texas, data center currently operates 125 megawatts of bitcoin mining with total contracted power of approximately 300 MW.