The third quarter was another high-producing three months, which saw companies making moves and deals to get more product—crude oil and natural gas—to market. The trend has rolled on into the fourth quarter.

In some cases, there were strategic partnerships, expansion and construction all taking place with a common goal. Here’s a quick review of selected midstream projects, by the major plays:

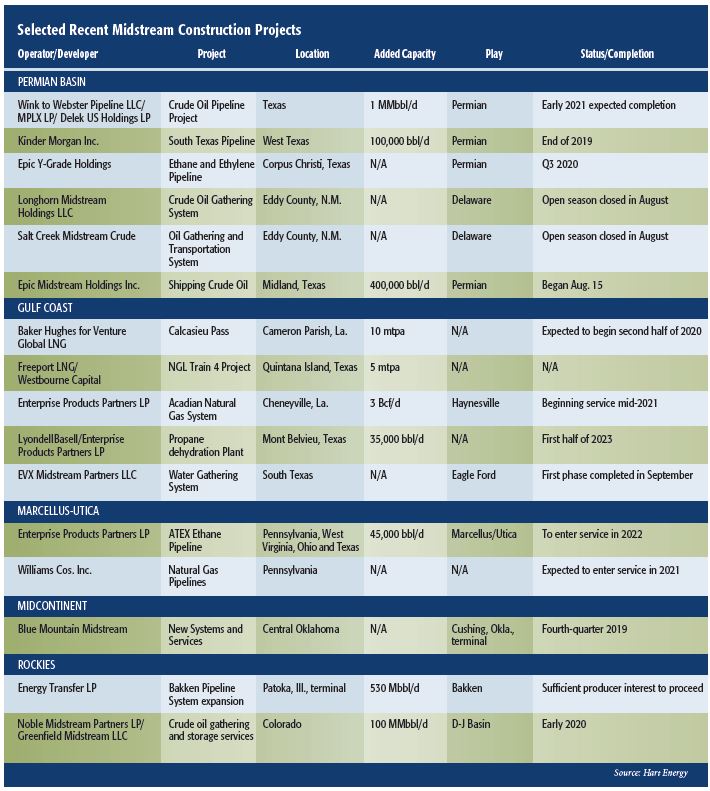

Permian Basin

The name of the game in the Permian Basin remains increasing the flow of product to market. To do so effectively, there is more construction coming online now and in the future.

One of the biggest projects, set to begin operation in early 2021, is the Wink to Webster Pipeline project. The pipeline, which will have 1 million barrels per day (MMbbl/d) of takeaway capacity from the Permian Basin, will see Wink to Webster Pipeline LLC affiliates MPLX LP, Delek US Holdings LP and Rattler Midstream LP joining ExxonMobil Corp., Plains All American Pipeline LP and Lotus Midstream LLC as partners.

Kinder Morgan Inc. is also moving forward with its South Texas pipeline connection that will transport crude from Phillips 66’s 900,000 barrels per day (Mbbl/d) Gray Oak pipeline in the Permian Basin to delivery points on the Houston Ship Channel.

Kinder Morgan expects service to begin by the end of 2019 and carry 100 Mbbl/d.

Epic Midstream Holdings Inc. began shipping crude on its 400 Mbbl/d pipeline from the Permian Basin to the U.S. Gulf Coast during the third quarter, which had the positive impact producers wanted: Midland crude prices climbed higher.

Rockies

A Noble Midstream Partners LP and Greenfield Midstream LLC collaboration is making progress and is on schedule to have a new liquids-focused system in operation for producers in early 2020.

Their Black Diamond Gathering LLC joint venture will provide crude oil gathering and storage services to producers in the Denver-Julesburg (D-J) Basin.

As part of the strategic relationship, Black Diamond and Noble Energy Inc. made commitments during Saddlehorn Pipeline’s recent open season. Black Diamond’s investment option expires in April 2020. The Saddlehorn Pipeline is jointly owned by affiliates of Magellan Midstream Partners LP, Plains All American Pipeline LP and Western Midstream Partners LP, and it is currently capable of transporting about 190 Mbbl/d of crude oil and condensate from the D-J and Powder River basins to storage facilities at the Cushing, Okla., facilities owned by Magellan and Plains All American. With the recent successful open season, the Saddlehorn Pipeline will be expanded by 100 Mbbl/d, to a new total capacity of 290 Mbbl/d.

To the north, an Energy Transfer LP executive said in September the firm received sufficient producer interest during a third-quarter open season to move ahead with an expansion of its Bakken Pipeline System. The project would nearly double capacity to 1.1 MMbbl/d. The Dallas-based firm did not provide a construction schedule.

Gulf Coast

Freeport LNG isn’t allowing a glut of natural gas supply to slow its business plan. In fact, the company has gone full steam ahead by shipping its first commissioned cargo of LNG from its Quintana Island location in Freeport, Texas. About 150,000 cubic meters of the super-chilled fuel was loaded on board the Bahamas-flagged LNG Jurojin and shipped from the Freeport LNG terminal in September. Ship tracking found that the tanker stopped in Jebel Ali, United Arab Emirates.

The start-up of Freeport LNG is expected to add to a supply glut that has been weighing on spot LNG prices in Asia. Industry observers speculate weak LNG prices could delay work on additional liquefaction capacity as the new year begins.

“The start-up of Freeport LNG contributes to even more supply growth at a time when the market is already oversupplied,” FGE LNG analyst Edmund Siau said in a Reuters report.

Baker Hughes is at the helm of Calcasieu Pass LNG project construction and was granted a final notice to proceed (FNTP) in the third quarter by Venture Global. The project, which is expected to begin in the second half of 2020, will add 10 million tonnes per annum (mtpa) to domestic LNG capacity.

Under the contract, Baker Hughes will provide an LNG liquefaction train with 18 modularized compression trains across nine blocks. The modularized system is said to offer a “plug-and-play” approach that allows for faster installation and lower construction and operational costs.

Meanwhile, Enterprise Products Partners LP has established plans to expand and extend its Acadian natural gas system, which will deliver volumes of natural gas from the Haynesville Shale to the LNG market in South Louisiana. This project, which is set to begin service in mid-2021, will feature construction of about 80 miles of pipeline around Cheneyville, La., to third-party interconnects near Gillis, La., and will include multiple pipelines that will serve LNG export facilities in Louisiana and Texas.

Marcellus-Utica

Noteworthy—but far afield from other midstream projects—Kinder Morgan announced early in the fourth quarter the commercial start-up of the first train at its Elba Island, Ga., LNG operation, outside Savannah. Trains 2 and 3 were expected to start up in the fourth quarter. The plant will have 10 trains when completed with a capacity of 2.5 mtpa.

It’s the nation’s second Atlantic-facing LNG plant, in addition to Dominion’s Cove Point, Md., plant on Chesapeake Bay and will provide another, badly needed market for natural gas coming out of the Appalachian Basin, which faces continuing constraints on pipeline capacity.

It has taken longer than expected, but it appears Williams Cos. Inc.’s Constitution Pipeline from Pennsylvania to New York could start moving again. A breakthrough came when the Federal Energy Regulatory Commission (FERC) voted that New York State took too long to deny a water permit. There still is a chance of a permit reversal in the courts, and other permit issues loom. But the project could enter into service in 2021, if all goes well.

FERC ordered that the New York State Department of Environmental Conservation (NYSDEC) waive the water quality certification required under the federal Clean Water Act for the New York portion of the pipe. FERC approved construction of Constitution in December 2014, but the project has been at a standstill since 2016 due to permitting questions.

Enterprise Products Partners announced it will proceed with an expansion of its Appalachia-to- Texas (ATEX) ethane line following a successful open season. The system could be expanded by as much as 45 Mbbl/d to 190 Mbbl/d in 2022.

The 1,200-mile ATEX pipeline transports ethane from the Marcellus and Utica in Pennsylvania, West Virginia and Ohio to the NGL storage and trading hub at Mont Belvieu, Texas, which features pipeline access to multiple petrochemical plants along the Gulf Coast.

Enterprise could add up to 50 Mbbl/d of incremental capacity through a combination of pipeline looping and modifications to already existing infrastructure. The expansion could be in service by 2022.

Gas producers in Pennsylvania, Ohio and West Virginia need all they help they can get from new pipeline capacity. Appalachia, much like the Permian, has continuing “basis” problems, or the price difference in what producers realize there vs. gas produced in other basins.

And new capacity doesn’t always have the desired effect.

The Rockies Express Pipeline, or REX Pipeline, was designed to improve Rockies gas prices by selling to the Northeast—until the vast reserves of gas from the Marcellus and Utica emerged. And, with that rapidly growing glut of gas in Appalachia, traditional long-haul pipelines serving Northeast markets ended up being reversed.

Recommended Reading

JMR Services, A-Plus P&A to Merge Companies

2024-03-05 - The combined organization will operate under JMR Services and aims to become the largest pure-play plug and abandonment company in the nation.

Humble Midstream II, Quantum Capital Form Partnership for Infrastructure Projects

2024-01-30 - Humble Midstream II Partners and Quantum Capital Group’s partnership will promote a focus on energy transition infrastructure.

Petrie Partners: A Small Wonder

2024-02-01 - Petrie Partners may not be the biggest or flashiest investment bank on the block, but after over two decades, its executives have been around the block more than most.

Hess Corp. Boosts Bakken Output, Drilling Ahead of Chevron Merger

2024-01-31 - Hess Corp. increased its drilling activity and output from the Bakken play of North Dakota during the fourth quarter, the E&P reported in its latest earnings.

Exxon, Chevron Tapping Permian for Output Growth in ‘24

2024-02-02 - Exxon Mobil and Chevron plan to tap West Texas and New Mexico for oil and gas production growth in 2024, the U.S. majors reported in their latest earnings.