(Source: Shutterstock)

How will the U.S. natural gas market change in the coming decades? There are two likely options.

Last year, the INGAA Foundation commissioned a thorough flagship study—“The Role of Natural Gas in the Transition to a Lower-Carbon Economy”—prepared by Black & Veatch Management Consulting LLC. The recently published review outlines what could happen to the natural gas market and what the industry—particularly the midstream—can do to prepare now for an uncertain future.

A 12-member steering committee, led by Dan Santa, INGAA Foundation president and CEO, and Deepa Poduval, Black & Veatch associate vice president and oil and gas industry executive, coordinated the project. These are the study’s key findings. Copies of the full report are available online at ingaa.org/foundation.aspx.—Paul Hart

The evolving role of natural gas continues to be at the forefront of U.S. energy industry developments.

This evolution to a lower-carbon economy, including how growing renewable power generation and battery storage will affect gas-fired power generation—and the resulting effect on the utilization of midstream natural gas infrastructure—is an important consideration for natural gas midstream operators and the value chain supporting the construction and operation of midstream infrastructure.

This study on the role of natural gas in the transition to a lower-carbon economy was undertaken to examine trends affecting energy use in the United States over a 20-year horizon, from 2020 to 2040, with a focus on understanding how natural gas complements a lower-carbon economy while identifying potential challenges and opportunities for the natural gas pipeline industry.

This report presents a comprehensive strategic and analytical study to help educate key stakeholders, including energy consumers, infrastructure investors and policy makers, about how natural gas and natural gas infrastructure will be needed and utilized in a lower-carbon economy.

Breakthroughs

Over the last decade, spectacular breakthroughs in exploration and production technology have transformed the natural gas industry. Producers have dramatically reduced the time required to drill and complete wells through increased efficiency in their multistage hydraulic fracture stimulations.

Increased use of data analytics continues to improve well completion designs and the ultimate recovery from each well. Shale gas production has grown almost 20% per year over the last 10 years. Low and stable gas prices have allowed natural gas to become the primary fuel for power generation. The combination of increased production and growing domestic markets created the need for new and reconfigured natural gas pipeline infrastructure.

Increasing global consumption of natural gas is also driving infrastructure needs in North America to serve newly-constructed and planned liquefied natural gas (LNG) export terminals along the U.S. Gulf and East coasts and pipeline expansions to deliver natural gas to Mexico.

Simultaneously, the impetus to reduce greenhouse gas (GHG) emissions has triggered state and regional mandates to reduce carbon emissions across all sectors. Some suggest that GHG emissions from natural gas combustion and distribution system methane leaks could be reduced by electrifying residential and commercial energy applications that historically have been met with natural gas.

Advances in solar and wind generation power generation technology, combined with the extension of the production and investment tax credits, have spurred significant renewable generation capacity additions over the past decade.

The study examines how these key drivers could affect the role of natural gas and the utilization of gas infrastructure over the next two decades. Our extensive analysis, supported by detailed modeling and industry subject matter expertise, centers around future scenarios that model different levels of renewable penetration and examine the effect on natural gas demand.

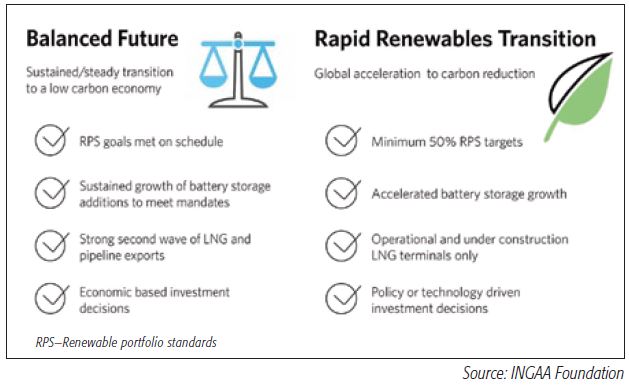

These scenarios focus on two possible paths toward an energy portfolio that relies increasingly on renewable energy:

- One path reflects a result driven by a balance of policy initiatives and market economics—a balanced future; and

- An alternative path is driven heavily by policy initiatives intended to accelerate the penetration of renewables in power generation—a rapid renewables transition.

Key findings are:

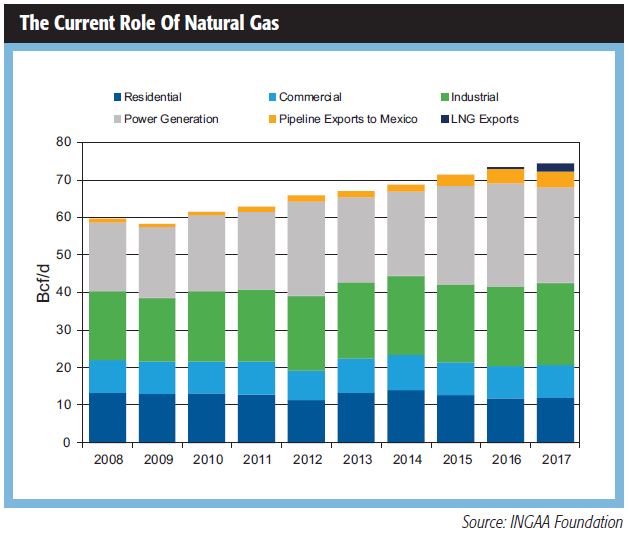

Natural gas will remain a significant contributor to the energy portfolio and economic growth in the United States.—Over the next 20 years, the current U.S. natural gas pipeline infrastructure will continue serving both traditional end-use sectors, namely those that are residential, commercial, and industrial, as well as emerging sectors, such as pipeline exports to Mexico and LNG exports to the global market.

Rising gas demand and production levels could spur the need for up to 21 billion cubic feet per day of new gas pipeline infrastructure to support the shift in demand and supply driven by global LNG demand growth, booming pipeline exports to Mexico and continued demand growth from the petrochemical sector, or to enhance the reliability of the power generation sector.

Natural gas-fired power generation will continue to play a key role in meeting low-carbon initiatives. —The variability of renewable generation, especially solar and wind generation, will require flexible, fast-ramping generation or energy storage. Natural gas-fired generation will allow an increasing amount of renewable energy in the electric generation portfolio by providing electric grid reliability in the form of load and generation profile following, backup power, frequency regulation and spinning reserves.

Battery storage at scale will be able to provide some of these services; current battery technologies, however, do not support the full range of flexibility needed, including for seasonal and daily variations, and therefore cannot displace natural gas-fired generation, which is uniquely suited to mitigate this variability. Even assuming technological advancements, declining life-cycle costs and solutions for disposal issues, battery storage may become economically comparable to gas-fired generation only toward the end of the analysis period.

Therefore, regardless of any assumptions about increasing renewable generation, natural gas-fired generation will continue to play a crucial role in ensuring that peak electric demand is met reliably.

Demand for non-ratable flow interstate natural gas transmission services and hourly nominations will increase.—The continued evolution of the gas transmission industry to support a lower-carbon economy over the next two decades will alter shippers’ requirements for natural gas pipeline services. Renewable integration will require quick-ramping, gas-fired generation during specific hours of the day.

Increased integration of intelligent metering will allow local distribution companies that serve traditional residential and commercial sectors to predict and respond to peak hourly need and to offer demand-response programs that can reduce overall design day needs.

If natural gas-fired generators are expected to serve as the backup when renewable generation is unavailable, these shippers may require pipeline services that allow them to nominate on the pipeline with little-to-no notice and grant them the ability to consume gas non-ratably. In such cases, pipelines must have the capacity to offer such services, and if they do not, pipelines must be sized to do so. In cases where existing capacity is insufficient to support such services, the shippers demanding such services must be willing to pay for the needed capacity.

Market uncertainty

Uncertainty about the energy future is nothing new for natural gas or any other energy source.

Market dynamics can change because of any number of factors, including a sudden technological breakthrough or federal or state energy policy decisions.

Over the next two decades, global market forces and regional U.S. policy initiatives may change the way we think about the role of natural gas. In the mid-2000s, the U.S. was positioning itself to import LNG from around the globe and perhaps pipeline gas from the Arctic, as domestic conventional natural gas supplies were steadily declining. This changed rapidly when the shale revolution made domestic natural gas abundant and affordable.

Today, we know that there is both a domestic and a global impetus for reducing carbon emissions and transitioning to a lower-carbon economy. Natural gas will play a key role in supporting this initiative by providing a safe, reliable and affordable source of energy.

Opposition to gas

Natural gas transmission infrastructure is built to serve the economic needs of the market and is

supported by shippers willing to commit to long-term firm transportation contracts to use the capacity. Despite the steadily increasing consumption of natural gas, opponents of natural gas infrastructure projects argue that increased renewable penetration will decrease the demand for natural gas-fired generation, thereby leaving gas transmission assets stranded.

Demand for gas transportation services from the power sector, however, has not been the primary driver for recently proposed pipeline projects.

Rather, other sectors have been the primary drivers of new pipeline infrastructure investments and utilize the majority of existing gas pipeline capacity. These shippers will continue to rely on natural gas and natural gas infrastructure, even as demand for renewable energy increases.

Natural gas usage trends in traditional end-use sectors (residential, commercial and industrial) and nontraditional sectors (LNG exports and pipeline exports to Mexico) will also significantly affect how the natural gas infrastructure will be utilized to meet the needs of all energy consumers in a safe and reliable manner. The INGAA Foundation is seeking to understand the future roles of natural gas and natural gas infrastructure in a lower-carbon economy for a 20-year analysis period, as well as the challenges and opportunities for the natural gas industry as it fulfills these roles.

Ramp up-ramp down

The continued development of renewable resources across the country, coupled with slower than

expected electric load growth, has dampened the need for new baseload generation capacity. Concurrently, the need for dispatchable generation that can quickly ramp up and down has grown.

In California, for example, the continued addition of solar resources has significantly changed the typical daily net load profile, with a deep midday drop and steep ramp rates in later afternoon and early evening hours. In West Texas, the significant amount of wind capacity has frequently driven electricity prices into the negative during the off-peak hours. The duration and magnitude of this kind of shift across the country will affect the amount, timing and duration of demand for natural gas to support the power generation sector and how pipelines and storage facilities will be utilized to facilitate renewable energy growth.

Global and U.S. initiatives to create a lower carbon economy will also impact traditional and non-traditional demand sectors. North America’s entrance into the global LNG market will provide Asian and European consumers with the benefits of competition that includes a low-cost supplier. U.S. LNG exports are expected to continue to grow over the analysis period and are expected to have a sustained impact on the need for natural gas infrastructure.

Conclusions

Across both scenarios examined, natural gas will continue to serve both traditional (residential, commercial and industrial) and emerging sectors (e.g., LNG exports and pipeline exports to Mexico) while playing a greater role in complementing renewable generation growth.

Gas-fired generators, with the help of pipeline and electric grid operators, have been able to ensure a stable and balanced electric grid. Higher levels of renewable generation over the next two decades will create new challenges in the electric transmission sector that the natural gas industry can help overcome.

Also, gas-fired generation will require additional flexible transmission services to balance the growth in renewable generation and support electric grid reliability.

LNG exports and pipeline exports to Mexico support the U.S. trade balance and work to reduce global emissions by replacing coal and other fossil fuels with clean-burning natural gas. With renewable generation growth in emerging markets, natural gas in the form of LNG will be needed to mitigate hourly and seasonal renewable variation. In both scenarios, U.S. LNG export terminals will be utilized at high capacity factors because U.S. gas supplies will remain competitive with global LNG alternatives.

Existing and new natural gas infrastructure will continue to play a critical role in facilitating future natural gas consumption.

Across both scenarios, natural gas infrastructure allows reliable, low-cost gas supplies to be produced and transported to meet critical needs and to support the transition to a lower-carbon economy.

Recommended Reading

Talos Energy Sells CCS Business to TotalEnergies

2024-03-18 - TotalEnergies’ acquisition targets Talos Energy’s Bayou Bend project, and the French company plans to sell off the remainder of Talos’ carbon capture and sequestration portfolio in Texas and Louisiana.

Enbridge Closes First Utility Transaction with Dominion for $6.6B

2024-03-07 - Enbridge’s purchase of The East Ohio Gas Co. from Dominion is part of $14 billion in M&A the companies announced in September.

SCF Acquires Flowchem, Val-Tex and Sealweld

2024-03-04 - Flowchem, Val-Tex and Sealweld were formerly part of Entegris Inc.

Pembina Cleared to Buy Enbridge's Pipeline, NGL JV Interests for $2.2B

2024-03-19 - Pembina Pipeline received a no-action letter from the Canadian Competition Bureau, meaning that the government will not challenge the company’s acquisition of Enbridge’s interest in a joint venture with the Alliance Pipeline and Aux Sable NGL fractionation facilities.

Global Partners Buys Four Liquid Energy Terminals from Gulf Oil

2024-04-10 - Global Partners initially set out to buy five terminals from Gulf Oil but the purchase of a terminal in Portland was abandoned after antitrust concerns were raised by the FTC and the Maine attorney general.