(Source: Shutterstock)

Crude oil prices continue to slowly increase due to the continued trade impasse with China and a supply overhang. Despite these headwinds prices are trending upward and are trading around the $60 per barrel mark.

The good news is that OPEC+ announced plans to cut back crude production by a further 500,000 barrels per day (bbl/d) through March 2020 to help support price increases. Unfortunately, the market was slow to respond to this news due to uncertainty over whether members would actually abide by the terms.

However, OPEC+ production cuts haven’t had much of an impact on global prices in recent years due to huge increases in crude production out of North America.

En*Vantage Inc.’s Weekly Energy Report for the week of Nov. 28 was released before the OPEC+ announcement but noted that the market is much improved from last year. While crude prices have been slow to climb this year, they are in stark contrast to last year when the West Texas Intermediate (WTI) price tumbled from $75/bbl in early October to $42/bbl in late December.

“Last year at this time, the market was fearing rising U.S. production, an intensifying trade war between the U.S. and China, and the inability of OPEC+ to maintain production discipline. After a year of fretting, traders are becoming cautiously optimistic that the crude markets can work through these issues,” the report said.

It appears that trade talks between the U.S. and China are progressing, albeit at a slow pace. En*Vantage also noted that the global economy seems to be stabilizing and the U.S. economy is still strong.

En*Vantage said it’s likely WTI stock levels will decrease in the coming weeks as refinery turnarounds are completed. The company is forecasting crude runs to increase and stock levels to decrease at similar levels, which will cause WTI prices to remain stable or increase slightly. Other hydrocarbon prices are following similar trends to crude with slow improvements despite solid tailwinds. Natural gas prices have been were slow to ramp up despite colder temperatures until this past week when they saw a 5% increase to $2.44 per Btu. However, this market has been topsy-turvy and likely requires sustained cold temperatures to really have a notable impact on prices for very long.

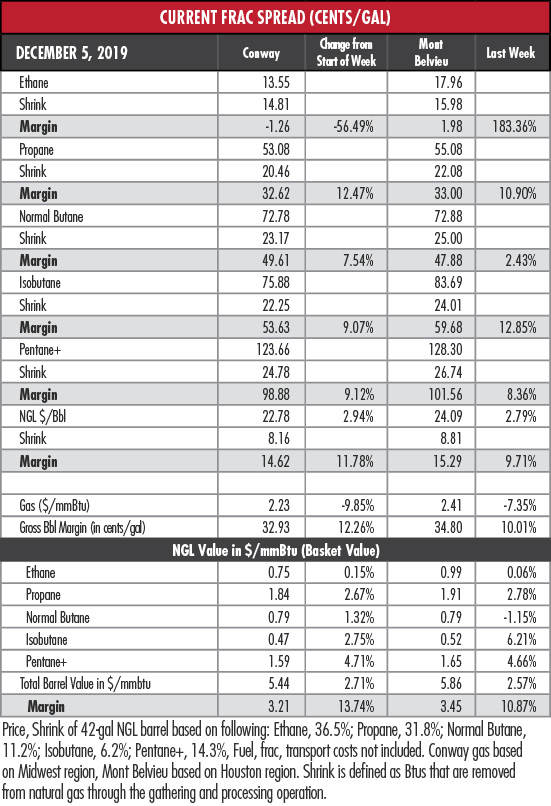

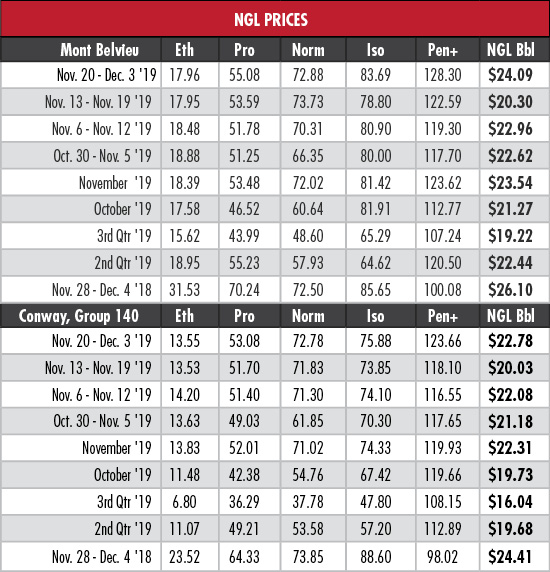

Despite being the preferred ethylene feedstock, ethane prices remained flat at both the Mont Belvieu, Texas, and Conway, Kan., hubs the week of Dec. 3. Storage levels are at high levels while unplanned ethane cracker outages are further hurting demand. Relief is coming in the form of 230,000 bbl/d of new cracker capacity, but it won’t be online until sometime in first-quarter 2020.

“[E]thane is currently in a vaccum driven largely by the up and down movements in natural gas prices. This past week was a good illustration of how ethane prices are captive to gas price movements. When Henry Hub prices dropped [the week of Nov. 28], ethane prices followed. Expect this trend to continue for at least the next couple of months,” En*Vantage said.

Butane had been the most preferred ethylene feedstock, but price increases from gasoline blending and export demand have seen that designation slip away. Prices were largely flat at both hubs this week. Another heavy NGL, natural gasoline has been the strongest NGL for much of this past month due to facility outages in Canada, Europe and Asia. Prices rose 5% at both Mont Belvieu and Conway, but they should start to level off as these fractionators and naphtha crackers come back online.

The propane market should start to tail off a bit soon, but prices remained pretty solid with 3% gains at both Mont Belvieu and Conway this week. Propane has been supported by higher demand levels for this time of year due to a lengthier and stronger crop drying season and colder temperatures last month.

However, crop drying season is just about over and temperatures are normalizing in much of the country. A further sign that prices are likely to begin to fall comes from increasing stock levels. According to the U.S. Energy Information Administration (EIA), propane stocks increased incrementally along the Gulf Coast and remain much higher than normal along the East Coast. On the bright side, they have been dropping in the Midcontinent.

The most profitable NGL to make at both hubs was natural gasoline at 99 cents per gallon (gal) at Conway and $1.02/gal at Mont Belvieu. This was followed, in order, by isobutane at 54 cents/gal at Conway and 60 cents/gal at Mont Belvieu; butane at 50 cents/gal at Conway and 48 cents/gal at Mont Belvieu; propane at 33 cents/gal at both hubs; and ethane at negative 1 cent/gal at Conway and 2 cents/gal at Mont Belvieu.

According to the EIA, natural gas in storage for the week of Nov. 29 was down 19 billion cubic feet to 3.591 trillion cubic feet (Tcf) from 3.61 Tcf the previous week. This is up 20% from the same time last year when it was 3 Tcf. This week’s storage level is about the same as the five-year average.

Heating demand should be typical for this time of year based on the National Weather Service’s forecast for the coming week as the service anticipates normal temperatures across much of the country.

Recommended Reading

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.

SLB’s ChampionX Acquisition Key to Production Recovery Market

2024-04-21 - During a quarterly earnings call, SLB CEO Olivier Le Peuch highlighted the production recovery market as a key part of the company’s growth strategy.

PHX Minerals’ Borrowing Base Reaffirmed

2024-04-19 - PHX Minerals said the company’s credit facility was extended through Sept. 1, 2028.