(Source: HartEnergy.com, Shutterstock)

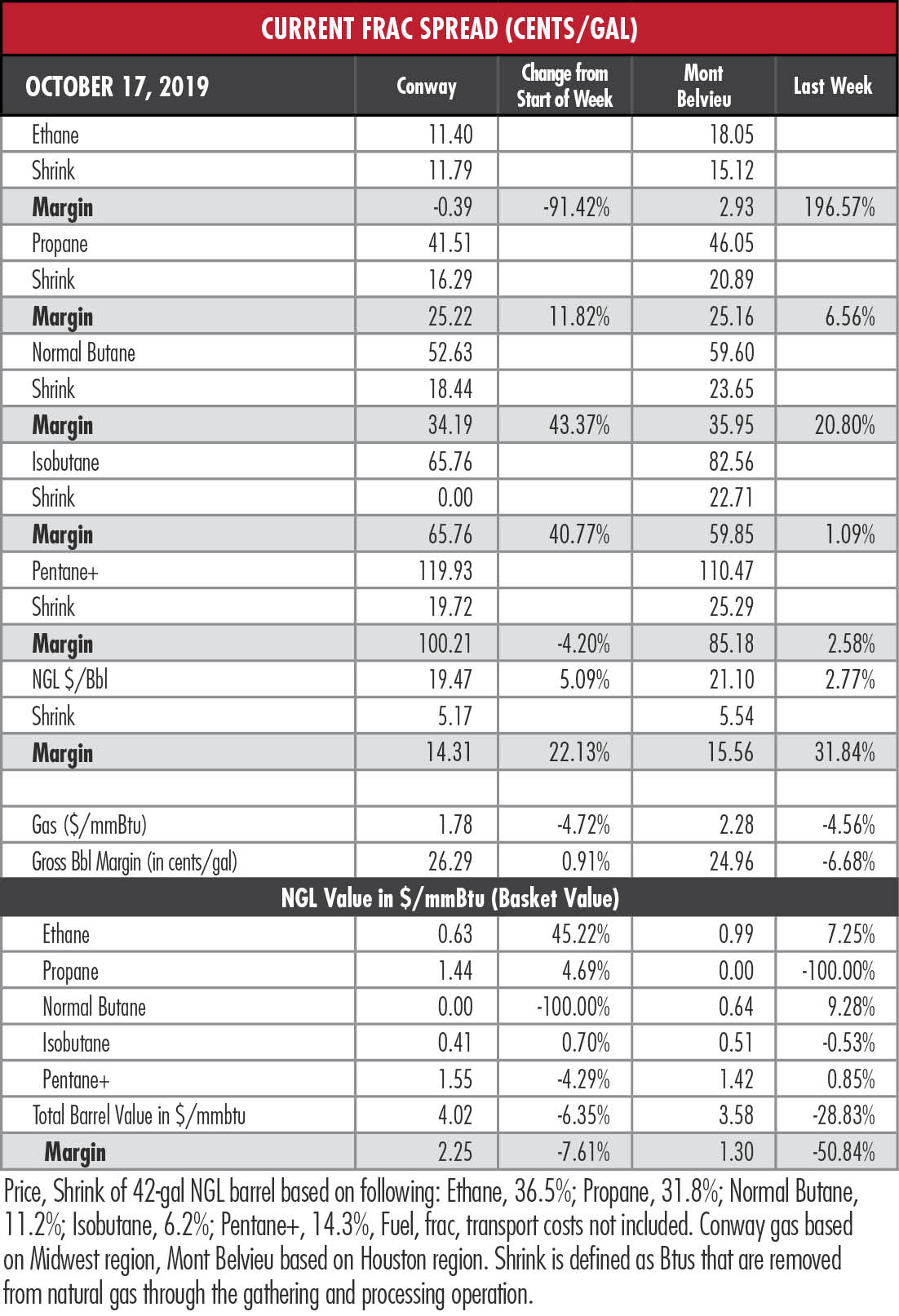

Prices for the hypothetical NGL barrels were their highest since late May at both Mont Belvieu, Texas, and Conway, Kan., over the past two weeks.

The rally, which has kept the Mont Belvieu barrel above $20 since the start of September, was led by a 7.2% rise in the price of ethane and a 9.3% increase in normal butane. Ethane’s margin almost tripled since the five-day period ending Oct. 1 to just under 3 cents per gallon (gal) and butane’s margin widened by about 21% to almost 36 cents/gal.

Ethane rose 45% at Conway to return to a double-digit price although its margin remained in the negative. Butane shot up 22% since Oct. 1 to surpass 50 cents/gal for the first time in 20 weeks. Its margin rose 43%.

Still, the recent price jolt only disguised continued sluggishness. Mont Belvieu ethane is less than half of its price at this time in 2018 and the Mont Belvieu “barrel” is off 43%. And while the 10-day average price showed a strong upturn, the daily price peaked on Oct. 8 and has been drifting lower since.

What will it take to lift ethane from its doldrums? EnVantage Inc. estimates that around 250,000 barrels a day (bbl/d) of increased demand is possible when current outages are resolved, new crackers are fully online and new crackers operated by Formosa Plastics Corp. and Dow Inc. are completed. Then, as the analysts have stressed, ethylene plants need to avoid unscheduled outages.

Of course, the high level of ethane in inventory—EnVantage estimates around 40 million barrels on the Gulf Coast—is a drag on prices and the analysts suspect that petrochemical operators purchased considerable volumes in late July when the price sunk to around 10 cents/gal. That means that about 100,000 bbl/d of incremental demand can be met by commercial and private stocks for several months.

EnVantage also notes that major Permian Basin players such as Enterprise Products Partners LP, Energy Transfer LP, Targa Resources Corp. and DCP Midstream LP can recover a significant amount of rejected ethane.

“The bottom line is that the combination of high ethane storage levels and the integration of certain midstream companies can distort ethane’s economic dispatch curve,” EnVantage wrote. “In other words, as ethane demand increases and inventories decrease, more ethane supplies can be delivered to the market at lower prices by the integrated midstream players. We believe this is happening now, which is resulting in a very slow grind upward for ethane prices.”

In the week ended Oct. 11, storage of natural gas in the Lower 48 experienced an increase of 104 billion cubic feet (Bcf), the Energy Information Administration (EIA) reported. That compared to the Stratas Advisors expectation of a 116 Bcf build and the Bloomberg consensus of a 108 Bcf build. The EIA figure resulted in a total of 3.519 trillion cubic feet (Tcf). That is 16.3% above the 3.025 Tcf figure at the same time in 2018 and 0.4% above the five-year average of 3.505 Tcf.

Recommended Reading

Humble Midstream II, Quantum Capital Form Partnership for Infrastructure Projects

2024-01-30 - Humble Midstream II Partners and Quantum Capital Group’s partnership will promote a focus on energy transition infrastructure.

Air Products Sees $15B Hydrogen, Energy Transition Project Backlog

2024-02-07 - Pennsylvania-headquartered Air Products has eight hydrogen projects underway and is targeting an IRR of more than 10%.

First Solar’s 14 GW of Operational Capacity to Support 30,000 Jobs by 2026

2024-02-26 - First Solar commissioned a study to analyze the economic impact of its vertically integrated solar manufacturing value chain.

TechnipFMC Eyes $30B in Subsea Orders by 2025

2024-02-23 - TechnipFMC is capitalizing on an industry shift in spending to offshore projects from land projects.

SunPower Begins Search for New CEO

2024-02-27 - Former CEO Peter Faricy departed SunPower Corp. on Feb. 26, according to the company.