(Source: NASA, Shutterstock)

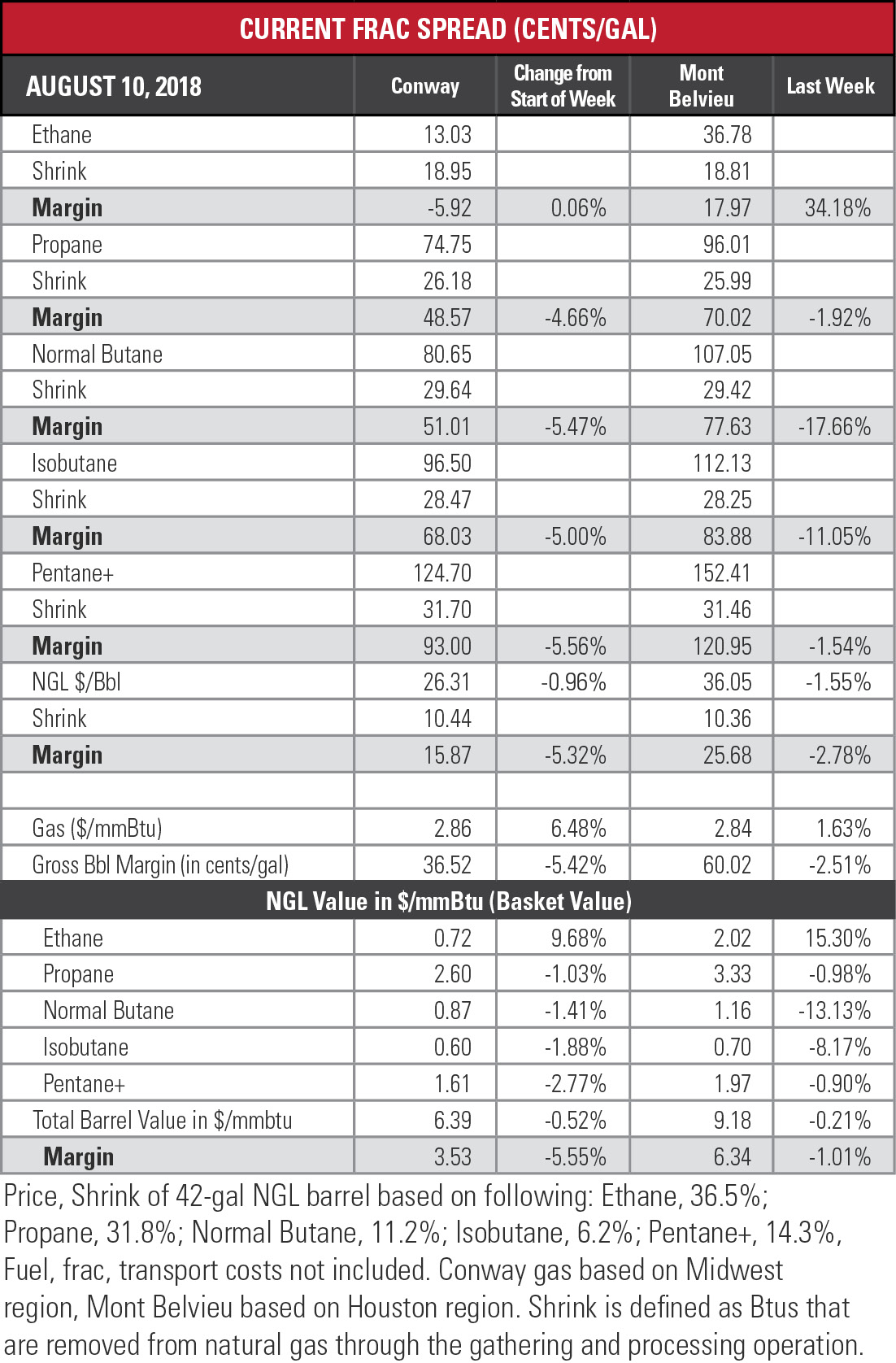

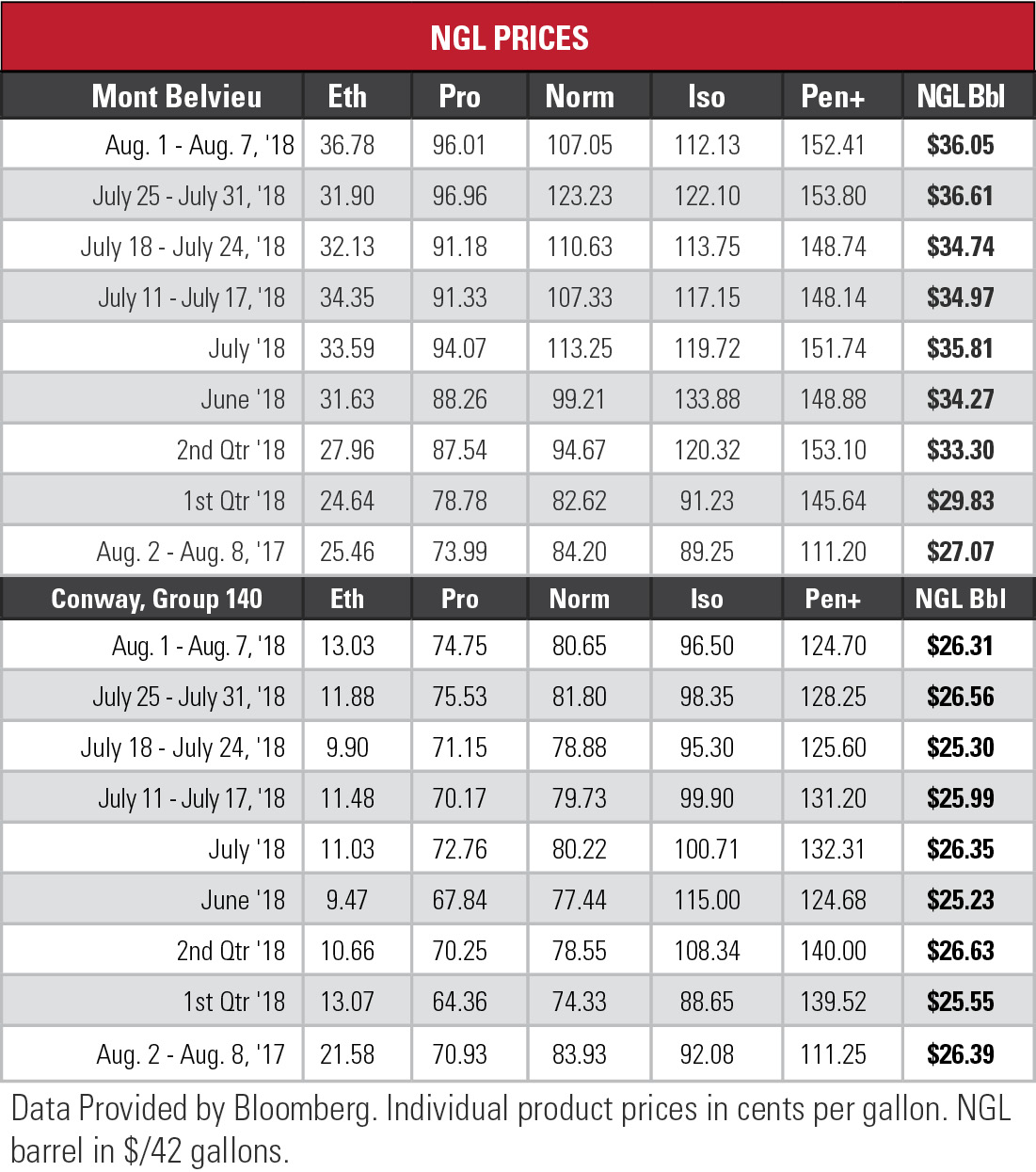

Ethane reached another high for the year at Mont Belvieu, Texas, last week as it lurched toward 37 cents per gallon (gal) into its loftiest territory since February 2014, or 227 weeks.

The 15.3% weekly jump erased the declines of the past three weeks and widened the margin by 34.2% to about 18 cents/gal. The rest of the NGL at both Mont Belvieu and Conway, Kan., slipped in price, with the hypothetical barrel taking a 1.5% hit at Mont Belvieu and Conway’s remaining static.

The Mont Belvieu barrel was still 33.2% higher than it was a year ago, and the price of ethane was 44.5% above the average of the same week in 2017.

The Mont Belvieu barrel was still 33.2% higher than it was a year ago, and the price of ethane was 44.5% above the average of the same week in 2017.

The industry could be forgiven for a case of nerves recently, with China’s threat of imposing a 25% tariff on U.S. LNG and Sinopec citing trade tensions for its decision to cut off U.S. crude oil imports.

“One knee-jerk reaction that is almost certainly wrong is that China’s rejection of U.S. imports poses a significant challenge to U.S. exports,” Citigroup analysts wrote in a report. “Whether in the long- or short-run, China’s potential imposition of tariffs or quotas on U.S. exports is a tax on Chinese consumers rather than an obstacle to U.S exports.”

Short-term implications of the loss of a market that had diminished 70% from April to June are fairly limited. It’s the long-term prospect of losing a foothold in the world’s fastest-growing economy that is of concern, but shouldn’t be.

China has long maintained that it will not be beholden to any single source of energy, so the celebratory smirks emanating from Australia following the recent Chinese tariff threat can be discounted.

China has long maintained that it will not be beholden to any single source of energy, so the celebratory smirks emanating from Australia following the recent Chinese tariff threat can be discounted.

After all, Australian energy executives, enjoying a huge geographical advantage compared to other LNG producers, would not worry at all were it not for the remarkable ability of the U.S. energy sector to be able to sell products in far-flung markets at competitive prices.

So are “billions at risk” for Gulf Coast investment in terminals? Sure. Risk is the essence of investment. That is why big bucks are paid to analysts who pore over pricing data and develop supply/demand scenarios to fashion a forecast.

The consensus forecast is that demand for natural gas will experience strong growth worldwide over the next decade or so because of the need for accessible, affordable energy. Fret over the Chinese market if you must, but know that the real risk is coming short of export capacity to meet demand.

In the week ended Aug. 3, storage of natural gas in the Lower 48 experienced an increase of 46 billion cubic feet (Bcf), the U.S. Energy Information Administration reported. The figure, below the Bloomberg survey’s consensus of 48 Bcf, resulted in a total of 2.354 trillion cubic feet (Tcf). That is 22.2% below the 3.025 Tcf figure at the same time in 2017 and 19.5% below the five-year average of 2.926 Tcf.

Joseph Markman can be reached at jmarkman@hartenergy.com or @JHMarkman.

Joseph Markman can be reached at jmarkman@hartenergy.com or @JHMarkman.

Recommended Reading

Chesapeake-Southwestern Deal Delayed Amid Feds Scrutiny of E&P M&A

2024-04-05 - The Federal Trade Commission asked Chesapeake and Southwestern for more information about their $7.4 billion merger — triggering an automatic 30-day waiting period as the agency intensifies scrutiny of E&P deals.

EQT, Equitrans to Merge in $5.45B Deal, Continuing Industry Consolidation

2024-03-11 - The deal reunites Equitrans Midstream Corp. with EQT in an all-stock deal that pays a roughly 12% premium for the infrastructure company.

Chord, Enerplus’ $4B Deal Clears Antitrust Hurdle Amid FTC Scrutiny

2024-04-08 - Chord Energy and Enerplus Corp.’s $4 billion deal is moving forward as deals by Chesapeake, Exxon Mobil and Chevron experience delays from the Federal Trade Commission’s requests for more information.

Talos Energy Sells CCS Business to TotalEnergies

2024-03-18 - TotalEnergies’ acquisition targets Talos Energy’s Bayou Bend project, and the French company plans to sell off the remainder of Talos’ carbon capture and sequestration portfolio in Texas and Louisiana.

NOG Closes Utica Shale, Delaware Basin Acquisitions

2024-02-05 - Northern Oil and Gas’ Utica deal marks the entry of the non-op E&P in the shale play while it’s Delaware Basin acquisition extends its footprint in the Permian.