Militant attacks that ignited fires at two Libyan crude oil export terminals stymied market bears this week. The bruins had been feasting on rising U.S. production and an anticipated increase in production from OPEC.

Now it appears OPEC members, meeting this week, may choose a more modest increase than Saudi Arabia has sought. But that does not erase recent warnings from the International Energy Agency (IEA).

“Higher flows from Saudi Arabia, Iraq and Algeria offset a fall in Nigeria and further declines in Venezuela,” IEA said in its June 13 Oil Market Report. “While the call on OPEC is set to ease in 2019, potential losses from Venezuela and Iran could require others to produce more.”

“Higher flows from Saudi Arabia, Iraq and Algeria offset a fall in Nigeria and further declines in Venezuela,” IEA said in its June 13 Oil Market Report. “While the call on OPEC is set to ease in 2019, potential losses from Venezuela and Iran could require others to produce more.”

The agency sees that extra production coming from the U.S., but with a caveat.

“The United States shows by far the biggest gain (about 75% of the total across 2018 and 2019), but recently this expansion has not been without stress,” said IEA. “The discount for WTI vs. Brent has blown out to $10/bbl, amidst signs that takeaway capacity is lagging behind output growth.”

Full disclosure: I’ve put a jar on my desk that requires contributions every time someone mentions takeaway constraints.

The list of bullish factors is growing:

- OECD stocks are at a three-year low;

- Venezuelan production could tumble to just 800,000 barrels per day (bbl/d) next year from May 2018’s 1.36 million bbl/d average;

- Falling U.S. crude oil inventories; and

- Increased U.S. output is more than matched by higher exports and increased refinery inputs.

“We are still in the camp that there is limited downside for crude prices as the global fundamentals along with geopolitical risks to crude production vastly outweigh any increase that could come from Saudi Arabia and Russia, if the increase comes at all,” said Envantage Inc. “It still appears to us that upside risks are building.”

“We are still in the camp that there is limited downside for crude prices as the global fundamentals along with geopolitical risks to crude production vastly outweigh any increase that could come from Saudi Arabia and Russia, if the increase comes at all,” said Envantage Inc. “It still appears to us that upside risks are building.”

Envantage sees upside for natural gas prices as well. Benchmark Henry Hub cracked $3 per million Btu (MMbtu) on June 15 for the first time since the end of January.

The National Oceanic and Atmospheric Administration (NOAA) gauges the chances of an El Niño developing in the fall at 50% and winter at 65%.

“The forecaster consensus favors the onset of El Niño during the Northern Hemisphere fall, which would then continue through winter,” reads the forecast. “These forecasts are supported by the ongoing build-up of heat within the tropical Pacific Ocean.”

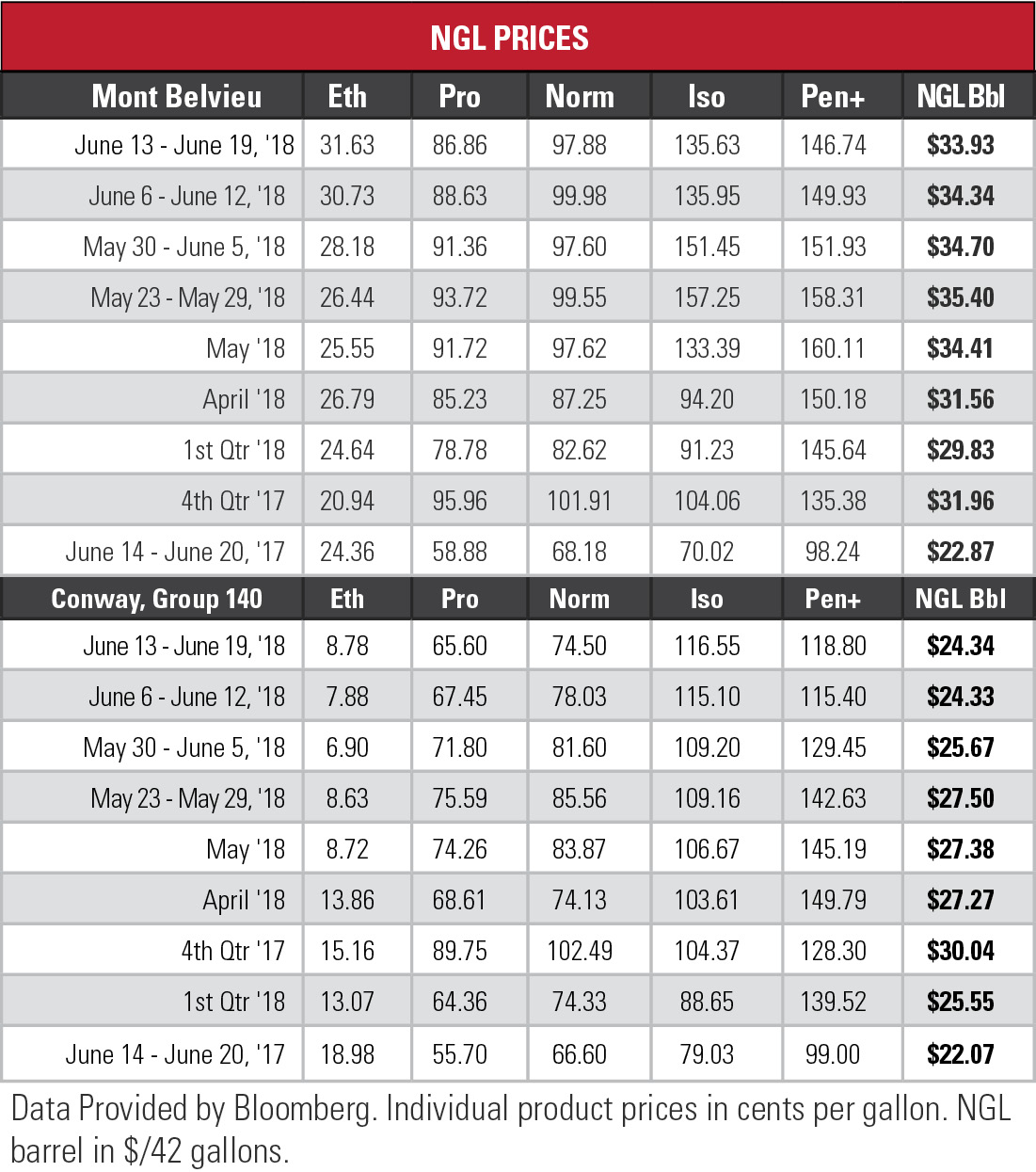

The Mont Belvieu, Texas, ethane price rose for the fifth straight week, rising above 31 cents per gallon (gal) for the first time since March 2014. The spread expanded by 5.62% over the previous week to 12 cents/gal.

Propane continued its four-week slide to its lowest price in eight weeks. The U.S. Energy Information Administration (EIA) reported another strong boost of 3.23 million barrels to propane inventories for the week ending June 15. Propane storage has increased 34% in the most recent five-week period.

Propane continued its four-week slide to its lowest price in eight weeks. The U.S. Energy Information Administration (EIA) reported another strong boost of 3.23 million barrels to propane inventories for the week ending June 15. Propane storage has increased 34% in the most recent five-week period.

Envantage speculates that traders share its skepticism concerning the EIA’s propane export data. Its analysts track exports regularly and estimate a weekly average that is about 169,000 barrels higher than the what the government agency is showing.

Joseph Markman can be reached at jmarkman@hartenergy.com and @JHMarkman.

Recommended Reading

For Sale? Trans Mountain Pipeline Tentatively on the Market

2024-04-22 - Politics and tariffs may delay ownership transfer of the Trans Mountain Pipeline, which the Canadian government spent CA$34 billion to build.

Energy Transfer Announces Cash Distribution on Series I Units

2024-04-22 - Energy Transfer’s distribution will be payable May 15 to Series I unitholders of record by May 1.

Balticconnector Gas Pipeline Back in Operation After Damage

2024-04-22 - The Balticconnector subsea gas link between Estonia and Finland was severely damaged in October, hurting energy security and raising alarm bells in the wider region.

Wayangankar: Golden Era for US Natural Gas Storage – Version 2.0

2024-04-19 - While the current resurgence in gas storage is reminiscent of the 2000s —an era that saw ~400 Bcf of storage capacity additions — the market drivers providing the tailwinds today are drastically different from that cycle.