Ameredev II’s well Red Bud State Com 115H, targeting the Wolfcamp A formation with a 9,674-foot lateral, flowed 2,813 boe/d (83% oil) on IP30. (Source: Ameredev II)

[Editor's note: A version of this story appears in the June 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

When Parker Reese was very young, he played on a giant sand pile deposited on the side of his grandparents’ house, the remains of a frack job performed by his grandfather’s operating company in Kansas. Reese is a third-generation oilman—his father also worked for a large oil company—so it is no surprise he followed in the family boot steps.

Parker Reese,

who launched

his first company

at age 30, was

first drawn to

the international

adventure oil

and gas offered.

Instead, “the

very best

opportunities

were right here in

the U.S.”

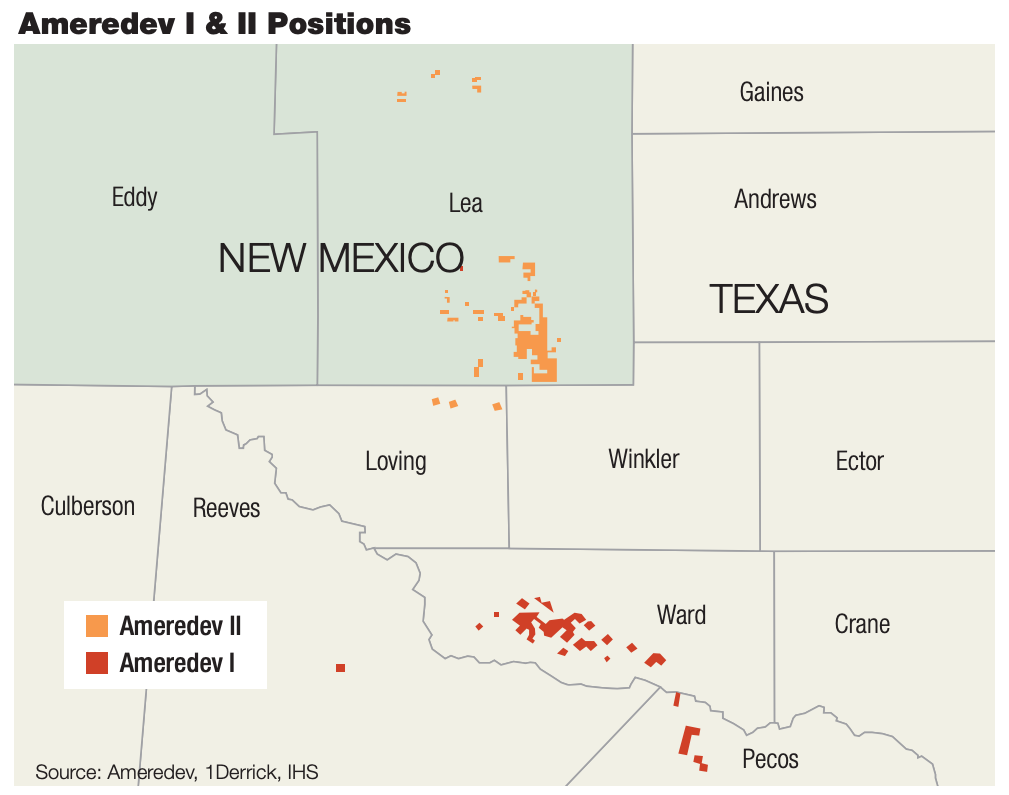

Today, at 35, he is the CEO of Ameredev II, an EnCap Investments-backed private company based in Austin and with a position in Lea County, N.M. Reese formed Ameredev II in March 2017 with a $400 million equity commitment from EnCap, which has since been upsized to $700 million.

Reese’s early allure to the oil and gas fields was derived from the critical need for energy around the world and visions of global megaprojects such as North Sea developments. Instead, his opportunity came in short-cycle unconventional projects in U.S. shales.

“Growing up around a major oil company, I was inspired by the scale and international nature of the projects those companies executed, but as I have moved into my own career, I have seen that the best work to do was drilling Wolfcamp Shale wells in the Permian Basin,” he said. “The very best opportunities were right here in the U.S.”

A petroleum engineer graduated from Texas A&M University, Reese’s first deployment out of college was with ConocoPhillips Co. and into the South Texas Lobo Wilcox Trend. He then spent time as a reservoir engineer with public midcap Cimarex Energy Co. and then with privately held Three Rivers Operating Co., or 3ROC, going smaller with each migration. Each taught him valuable lessons along his path to independence.

At ConocoPhillips, which was still a major at the time, he saw how the power of the balance sheet gave the company tremendous capacity to engineer every aspect of a problem and then to make huge projects happen. He identifies Cimarex as a technically excellent company with a laser focus on rates of return. “That is a company built to last, and something we want to emulate in a lot of ways at Ameredev.”

“My vintage of professionals had as much experience in the U.S. unconventional business as anyone. We’ve been there since the beginning of it.”

He characterizes 3ROC CEO Mike Wichterich as “a commercial genius” who takes a brute force approach in problem-solving, identifying every bottleneck and every solution to formulate a strategy. In putting together a position, Wichterich would analyze 100 deals, bidding on 20 to get to three transacted. “You have to have enough shots on goal to be successful. That’s what rubbed off on me at 3ROC.”

Reese formed Ameredev I in January 2015 and accrued 16,700 net acres in Ward County, Texas, before selling out to Callon Petroleum Co. for $633 million in February 2017, barely enough time to get two wells down.

Ameredev II is focused on the Delaware Basin’s eastern slope with a contiguous, 27,000-plus net acre position crafted through some 50 deals. It has drilled seven wells with five producing nearly 5,000 barrels of oil equivalent per day (boe/d) presently. The company is building its own infrastructure, including a crude gathering network, water gathering and treatment, and is contracted with Salt Creek Midstream for gas gathering and processing.

Reese chatted with Oil and Gas Investor about his entrepreneurial philosophies and his plans for Ameredev.

Investor: What motivated you to take an entrepreneurial tack?

Reese: Leading teams is just something that I’m passionate about. It’s challenging and rewarding to be able to build a company with a talented team. It’s taking all of those skills and putting them to the test in a competitive arena.

Investor: How old were you when you first did that?

Reese: I was 30 years old.

Investor: That’s a pretty bold move. What gave you that desire to take that chance?

Reese: I had the benefit of working closely with the management at Three Rivers and with Cimarex. I had the chance to do a lot of critical work at those two companies. Both of those companies are very lean and mean, and I got a lot of repetitions in.

And, my vintage of professionals, you know, we had as much experience in the U.S. unconventional business as anyone. We’ve been there since the beginning of it. It started in 2005 to 2007 in a serious way, so we’ve been there for the whole thing.

Also, 2015 was a great time to start a company. There was a lot of dry powder in the private-equity space, and it was a good time to have a new management team to offer up.

Investor: It was also a time of weeping and gnashing of teeth in the oil and gas space.

Reese: That’s right. And that was a challenge for us. It was easy to raise money, but it was hard to put it to work. If you remember, people didn’t want to sell at what they felt was a low oil price environment and low valuations.

That was the struggle, finding something to buy. In Ameredev I, we chased an incredible amount of leads. And after we looked at 150 deals, it was clear where we wanted to be investing to build a position where we thought we could achieve good returns for our equity.

Investor: Ameredev I was a very short cycle—what was the secret of your success there?

Reese: It was not the expected result. We were planning on going a lot further in development; we were building our back office and our operations team and our procedures, and the layout of the field to go longer. But public equity investors were just pushing these small and midcap independents to capture as much resource as they could, and we were getting inbounds from multiple guys that really wanted to buy it.

So we asked them for a number and the number was a good answer. Our technical perspective is to get the most value, but the commercial answer was that the quick exit was a unique opportunity at a unique moment in time. I’m glad that we exited when we did, because even if the asset, fundamentally, could be worth more, it would be harder for those same companies to buy it later. We felt like we made a good return.

Investor: How did you build your position in Ameredev II? Was it more difficult than the first time?

Reese: We looked at a wide area. We looked at the D-J Basin, Ark-La-Tex and the Powder River Basin. We looked at the Midcontinent. In each case, we did a regional analysis to understand the key drivers of the resource density, the productivity of the wells and the economics.

When that initial 12,000 acres in southern Lea County showed up as an opportunity, it was the clear leader from a life-cycle rate of return standpoint. So, we did 18 acquisitions in that one month to form that 12,000 acres. Over the next year and a half we did 24 more acquisitions for 13,000 more acres. Then we did several trades and some divestitures. We took scattered acres and put them into our main block where they’re a part of high working interest, long-lateral units.

We essentially upgraded the value of those acres to us. And what we’re left with is a little over 27,000 net acres with 96% working interest. All of these units are 2-mile laterals, except for right along the state line, where they’re 7,000 footers.

That really scrappy land and business development strategy—where we looked at all of these deals and worked them really fast—was a key part of making Ameredev II work in capturing this highly contiguous position in the Delaware Basin.

Investor: Can you tell me what an average price paid per acre is for your position?

Reese: That’s one of the few numbers we don’t talk about. But I would say there is plenty of value to be realized just by aggregating land, right? If you said it cost a dollar an acre to lease all this, then just by the fact that it’s put together, it’s worth a lot more than that, just by the fact the work is done and you have the certainty of getting one deal, versus all those little pieces.

Investor: Did you take a geological risk by being so far eastward in the basin? What gave you confidence this would work?

Reese: When we initially got into this, it was definitely viewed as risky—it was a step out. We were looking at the logs from old wells and saw that the key productive reservoirs continued across the position, and we had seismic that showed that the basin continued. We felt like it was a good risk.

And we’ve got some wells down now. Every modern log that we have has demonstrated a better reservoir than we had mapped before. We are ecstatic about our well results. Further seismic interpretation is showing this area as really special.

is being built for long-term development.

__________________________________________________________________________________________________

RELATED:

Ameredev’s Latest Drilling Activity Highlights – Two Wolfcamp Completions In Lea County, N.M.

__________________________________________________________________________________________________

Investor: Tell me about your program so far.

Reese: We’ve got five wells producing, we’ve got two that are completing right now, and one that’s drilling.

There are two 7,000-foot wells on the Azalea Pad; those are our first two. To the north, there are two wells on Red Bud. Those are stacked laterals; they’re actually pretty close. Those wells have all turned out phenomenal. Next, we have the Firethorn, and that was a 2-mile lateral. Unfortunately, we were only able to complete about 1,700 feet of it. It’s still a strong well on a per foot basis, and it demonstrates we’ve got a great reservoir there.

Next, we’ve got the Nandina and Golden Bell that we’ve drilled on a two-well pad. We are completing those as we speak. Then we’ve got the Magnolia that we are drilling right now.

Investor: Is this a one-rig program?

Reese: We’ve got one rig going right now, and we’re going to two rigs very soon.

Investor: What are you targeting?

Reese: Our existing wells are all in the Wolfcamp X, the A and the B. Basically, the program for this year stays in those zones. The First and Second Bone Spring look good, and we may add those on in the year, but that’s the next stuff we would test after that.

Investor: You’ve published results on four wells all above 2,000 boe/d on IP30. Are you pleased with the results?

Reese: They have exceeded all of our expectations so far.

As we climb updip from the deepest part of the basin, we’ve got a very low water cut in the reservoir. Our wells typically produce around 1-to-1, water to oil, whereas the Delaware Basin, on average, is 3-to-1, and some areas as high as 10-to-1. It’s a tremendous advantage.

“If we’re going to develop the asset, we’re going to end up wanting to keep it because the distributions we can spin off far exceed our cost of capital.”

Investor: Can you talk about what your drilling and completions look like?

Reese: We’re doing about 2,700 pounds per foot in a slickwater design. We have about a 125-foot stage length. We’re using 100 mesh in-basin sand and recycled water, which really reduces the cost of what we’re doing tremendously. Atlas Sand, specifically.

On the drilling side, we have a huge focus on safety. The eastern margin of the Delaware Basin has hydrogen sulfide in the gas. We’ve made a big investment in how the field is set up, in terms of having ambient air monitoring and automated shut-in valves. We designed the field to a very high standard for operational excellence.

Investor: Downspacing and concerns about parent-child well degradation have become prevalent in the basin. Are you concerned about that, or accounting for that in your projected development program?

Reese: So, there’s two things to separate. One is parent-child, and the other is just the actual spacing. The parent-child is where you go back and frack a well later, and I think that there’s a lot of progress being made in the industry now to mitigate the degradation of the child well. With re-pressurizing the parent well and modifying frack designs and positioning of the lateral vertically, there are a lot of things that are going to mitigate that problem.

But the other one is just interwell spacing. There is a demonstrated degradation in the ultimate recovery of the well with tighter spacing. It causes a trade-off between how many wells do you want to pack into a section vs. what is the incremental rate of return for each of those sticks you’re packing in.

As a private investor, our focus is to maximize the rate of return. I think the industry, in general, is going down that path. You see a lot of public operators upspacing their inventory to prioritize rate of return over just having absolutely the maximum number of locations.

We’re still not certain on what the ultimate spacing is on our position. One of the reasons we’re going to two rigs is we want to drill multiple spacing pilots.

The principle is we want to maximize rate of return, and I think that is going to lead us to larger, more intensive completions at a wider spacing, because we’re trying to make oil for the least amount of capital. We’re not trying to just maximize the amount of holes we can put in the ground.

Investor: As a small private, are you experiencing any challenges with takeaway capacity in the Delaware?

Reese: We’re really not. Last year, we had limited production and we took a big differential hit on most of the barrels we sold last year, but we didn’t lock ourselves into anything.

As we build the Trophy pipeline system, we’re going to have the freedom to market our barrels where and on the terms we want that are optimal for Ameredev. Ultimately, we feel like our best value risk proposition is having optionality in how we can market our crude.

Investor: How important is water infrastructure? How much are you investing into that?

Reese: It’s going to be critical as we go into the full development phase of the Permian Basin to have water infrastructure. Ameredev is unique in that we’ve got a concentrated, contiguous footprint. This allows us to take produced water from any battery in the field and bring it back to a couple of central storage tanks or pits. We can treat and we can push back recycled water to our fracks. We’re saving a tremendous amount of the cost, from $2.50 a barrel, full cycle, to something like 25 to 50 cents, full cycle.

The other piece that’s key here is the connectivity of the system; the network effect is really important. We’re connected to other outlets to where we can work with other water systems. This enables effective long-term development of the assets.

Investor: You’re investing a lot more capital into infrastructure than just drilling wells.

Reese: Right. There’s more than that, too. We’re putting in a cell tower out there.

We think the ability to move data from the field to headquarters is critical for long-term efficient development. There is cell service, but we want to have bandwidth to move telemetry and automation and real-time video data from the field to the office so that we can optimally manage the life cycle of the development and production of the field.

Our facilities are engineered for the long term because, ultimately, we’re designing this as if we have to live with it for a long time. We’re trying to develop a field such that we can provide the lowest cost, safest barrels anywhere in the world, because we want to compete with the rest of the Permian Basin and the rest of the world for the lowest cost of supply barrels. And that’s how we win and how we provide a service to the country and the world.

Investor: What about your private-equity investors? They typically like an exit to get cashed out. What is your exit strategy?

Reese: We’re shifting at this point. We have no idea what an exit would look like for Ameredev II.

The future development of this asset outpaces even our cost of capital for private equity. And so, if the capital markets are going to demand a return of capital from their investors and, thereby, push us to take this asset to being a free-cash-flow positive asset, then at that point our equity distributions are huge. So that can be a really good way for us to earn a return, also.

But if we’re going to develop the asset, we’re going to end up wanting to keep it because the distributions we can spin off far exceed our cost of capital. I think the private-equity investors can see the value in those long-term returns. That’s clear to them; the returns are there, and where there are good returns, capital finds a way to make it happen. Ultimately, if everyone’s making money, we’re going to find a solution to that question.

But there is still a lot of time. We’re going to get to free-cash-flow positive and to full return of capital early. I don’t think we’re going to have a tough time answering that question when we need to.

Investor: So is this a “yieldco” model?

Reese: Think about it this way: When a private-equity company exits, they just push cash back to the unit holders. We’re going to sell barrels instead of acres. We can distribute more cash that way.

“We want to maximize rate of return, and I think that is going to lead us to larger, more intensive completions at a wider spacing, because we’re trying to make oil for the least amount of capital.”

Investor: Do you perceive the private-equity model as changing?

Reese: Absolutely. I think you’re going to see more and more of these where the return comes from distributed cash flow to the equity holders as opposed to a full exit of the asset. For the past 10 years we were in this high growth cycle, but we’re in a more moderated cycle of restraint now, and the better returns are going to come from distribution of cash flow.

Investor: Do you think that’s a short-term cycle, or a longer-term paradigm shift?

Reese: It feels very long term right now. What would it take to change that? I think probably another supply crunch. That doesn’t feel like it’s on the horizon; it feels like we have ample sources of supply around the world and, in particular, U.S. growth.

Investor: What do you think the Permian will look like in three to five years?

Reese: We’re fortunate we already have our dance ticket. I think the majors and a handful of large independents are going to dominate the basin. They’re going to dominate infrastructure and services. They’re going to dominate in terms of the activity level that they bring. And it’s going to be their growth engine. For Permian assets to deliver meaningful growth to an Exxon or Chevron, they have to invest tremendously.

Investor: What’s Ameredev’s plan for 2019?

Reese: Continue to build the crude gathering system, continue to delineate all the way east and all the way to the north position, test spacing and multiple pilot projects, grow production and operate safely. And be best in class with operational excellence.

Investor: How many wells are you anticipating for the full year?

Reese: If we did 16, then that’s just the Wolfcamp X, A and B. But, we could add and test the First or Second Bone Spring, or the Avalon. The plan is very flexible.

Investor: Do you want to grow your position?

Reese: We’ve really slowed down. Our focus is moving into development of this asset. We want to maximize the life-cycle rate of return and return capital to our equity holders. It has influenced the way we put this position together in terms of the trades, and it’s guided our strategy in terms of where we’re putting wells in the infrastructure we’re building. So at the end of the day, we are a rate-of-return focused entity. And that is the answer.

But we’re deal junkies. If there is a strategic opportunity, we’re going to look at it.

Investor: What advice would you give to someone who might be considering breaking away to becoming independent themselves?

Reese: It’s a really tough time right now. With private equity having the flight to quality, with reduction in potentially the number of portfolio companies out there, and then even the number of firms out there, it is a very tough time to be entering this phase.

The key thing is this is a team sport, and you need to have the best team around you. A talented, multidiscipline team is what makes it work; it’s what makes it rewarding.

Investor: So is the opportunity for a start-up to come in to the Permian limited or nil?

Reese: The odds are against them, but I don’t want to bet against an entrepreneur who wants to commit capital on their idea in the Permian Basin. That seems like a bad bet. You don’t want to bet against the American entrepreneur.

Steve Toon can be reached at stoon@hartenergy.com.

Recommended Reading

Marketed: Confidential Seller Certain Mineral, Royalty Interests in Louisiana

2024-02-13 - A confidential seller retained RedOaks Energy Advisors for the sale of certain mineral and royalty interests in Louisiana.

Marketed: KJ Energy Operated Portfolio in East Texas

2024-04-16 - KJ Energy has retained TenOaks Energy Advisors for the sale of its operated portfolio located in East Texas.

Marketed: Stone Hill 41 Well Package in Howard County, Texas

2024-02-16 - Stone Hill Exploration and Production has retained EnergyNet for the sale of a Midland Basin 41 well package (11 PDP wells, 5 WIPs and 25 PUD locations) in Howard County, Texas.

EQT, Equitrans to Merge in $5.45B Deal, Continuing Industry Consolidation

2024-03-11 - The deal reunites Equitrans Midstream Corp. with EQT in an all-stock deal that pays a roughly 12% premium for the infrastructure company.

Marketed: Wasatch Energy Management Non-operated WI in Utah

2024-02-14 - Wasatch Energy Management has retained EnergyNet for the sale of non-operated working interest and royalty opportunities in Duchesne and Uintah counties, Utah.