(Source: Hart Energy; Shutterstock.com)

[Editor's note: A version of this story appears in the June 2020 edition of Midstream Business. Subscribe to the magazine here. It was originally published June 1, 2020.]

Environmental, social and governance (ESG) factors comprise the criteria used by investors in a holistic approach to analyze an investment. Formerly a niche concept, ESG has moved toward the mainstream of finance in recent years as a result of investor demand, regulatory influence and demographics.

As ESG has gained traction broadly among the investment community, the midstream space has discussed ESG considerations with more regularity and depth. The concept has received increased attention at recent industry conferences, and several companies have released sustainability reports highlighting ESG initiatives.

ESG can be evaluated using a number of metrics, which can vary widely by industry and degree of disclosure. This analysis is tailored specifically to midstream and the top 30 companies by weighting in the Alerian Midstream Energy Index (AMNA), excluding Plains GP Holdings to avoid redundancy given the inclusion of Plains All American Pipeline LP.

Intangibles

ESG’s role in financial analysis has become more pronounced in recent years. ESG investing has grown significantly in assets under management (AUM) since 2005, when a frequently cited United Nations report suggested that companies that manage ESG factors can potentially perform better by mitigating risks, anticipating and responding effectively to regulations and operating sustainably. ESG issues can also impact intangibles like reputation and branding, which matter for risk management and, increasingly, in the analysis of a potential investment.

In general, the inclusion of ESG factors into the investment process has grown significantly in the past decade and is being driven by younger investors. The Global Sustainable Investment Alliance said in a 2018 report that ESG integration accounted for $17.5 trillion of investment dollars globally in 2018, up 69% from 2016. In the U.S., sustainable investing accounts for just over one-fourth of total managed assets.

In addition to growing AUM dedicated to ESG, demographics and increased regulations have played a part in the ESG space. In Europe, there has been a significant commitment to sustainable finance and ESG, with a push toward including ESG in multiple parts of the investment process through regulations. Both international investors and younger investors alike are increasingly interested in ESG investing and see it as a way to express values, which is a shift from how other generations have viewed investing. MSCI Inc. projected that millennials could invest $15 to $20 trillion in U.S. ESG investments over the next 20 to 30 years.

Even if investors merely incorporate ESG issues into a traditional investment analysis to provide a more holistic view of a company and assess certain risk factors, ESG and related areas such as sustainable investing will likely continue to grow.

Midstream introduction

Although not typically considered an ESG investment, the oil and gas industry is not immune to the shift toward ESG. As a vital piece of both the U.S. and global economies, the energy sector cannot be ignored by investors, but energy companies, including midstream names, must also adapt to address the priorities of shareholders. Investors’ interest in ESG plus its inclusion in presentations shows that management teams recognize the increasing relevance of ESG. Finally, the general increase in data disclosures by companies on ESG issues has made more in-depth analysis possible.

ESG considerations for midstream are generally evaluated on metrics that are most applicable to midstream operations and investment considerations. When considering the environmental category, midstream is primarily concerned with land management, biodiversity, limiting spills, investing in clean technology and other ways of limiting its environmental impact. Social factors are those that impact stakeholders, namely issues such as workplace safety, diversity and community engagement. Finally, governance issues encompass the rights and responsibilities of a company and its shareholders and the alignment between shareholders, the board of directors and management.

In general, the amount of disclosure on ESG issues by midstream companies is bifurcated between companies that have provided detailed reports on the topic and companies that have hardly acknowledged ESG concerns. The varied degree of transparency and relative lack of uniformity prevalent with the sector’s ESG disclosures make comparison among companies more difficult.

However, several companies have taken steps to release an annual sustainability report containing information on how companies monitor and integrate ESG issues into their operations as well as long-term initiatives and goals. These reports also contain detailed data that was previously only tracked internally and not commonly disclosed. For example, companies may report greenhouse gas and carbon emissions from assets, total recordable incident rates and detailed employee diversity data. In 2019, Crestwood Equity Partners LP, Targa Resources Corp. and Williams Cos. Inc. released their inaugural sustainability reports. Other companies have not released full sustainability reports but have engaged with investors on ESG topics during investor days and have increased the amount of disclosures on their websites.

Inclusion in broader indexes is another potential benefit to ESG efforts. For example, ONEOK Inc. announced that it has been included for the first time in the Dow Jones Sustainability North America Index.

Alerian compiled and analyzed government data and company disclosures in U.S. Securities and Exchange Commission (SEC) filings and company websites. For the more granular ESG disclosures, the data presented by midstream companies varied significantly. Some companies, especially those that have published sustainability reports, offered details including emissions data that are difficult or impossible to track without company disclosure.

|

Alerian Midstream Energy Index ESG First Steps |

|||||

|

Company |

Ability to Vote on Board Members |

Skin in the Game* |

IDRs |

Board Independence |

Sustainability Report |

|

Cheniere Energy |

Yes |

0.6% |

No |

55% |

No |

|

Crestwood Equity Partners |

No |

6.3% |

No |

67% |

Yes |

|

DCP Midstream |

No |

0.1% |

Yes |

80% |

No |

|

Enbridge |

Yes |

0.2% |

No |

73% |

Yes |

|

Energy Transfer |

No |

13.8% |

No |

30% |

No |

|

EnLink Midstream |

No |

0.7% |

No |

33% |

No |

|

Enterprise Products Partners |

No |

0.3% |

No |

56% |

No |

|

EQM Midstream Partners |

No |

0.0% |

No |

43% |

No |

|

Equitrans Midstream |

Yes |

0.0% |

No |

71% |

No |

|

Genesis Energy |

No |

8.9% |

No |

100% |

No |

|

Gibson Energy |

Yes |

0.3% |

No |

88% |

No |

|

Inter Pipeline |

Yes |

0.3% |

No |

90% |

Yes |

|

Keyera |

Yes |

1.1% |

No |

78% |

No |

|

Kinder Morgan |

Yes |

14.0% |

No |

75% |

Yes |

|

Macquarie Infrastructure |

Yes |

0.2% |

No |

78% |

Yes |

|

Magellan Midstream Partners |

Yes |

0.3% |

No |

89% |

No |

|

MPLX |

No |

0.2% |

No |

57% |

No |

|

NuStar Energy |

Yes |

7.4% |

No |

89% |

No |

|

ONEOK |

Yes |

0.6% |

No |

64% |

Yes |

|

Pembina Pipeline |

Yes |

0.2% |

No |

82% |

Yes |

|

Phillips 66 Partners |

No |

0.1% |

No |

43% |

No |

|

Plains All American Partners |

Mixed |

0.6% |

No |

69% |

No |

|

Shell Midstream Partners |

No |

0.0% |

Yes |

33% |

No |

|

Tallgrass Energy |

No |

2.0% |

No |

44% |

No |

|

Targa Resources |

Yes |

1.9% |

No |

70% |

Yes |

|

TC Energy |

Yes |

0.1% |

No |

92% |

No |

|

TC Pipelines |

No |

0.1% |

Yes |

43% |

No |

|

The Williams Cos. |

Yes |

0.1% |

No |

92% |

Yes |

|

Western Midstream Partners |

No |

0.1% |

No |

75% |

No |

|

*Measure of insider ownership of common units as a percentage of total shares outstanding. (Source: Company reports, Alerian) |

|||||

The degree of transparency with ESG metrics is one area for improvement among midstream companies, especially in the MLP space. MLP investors would benefit from greater transparency with ESG data and in other areas, like project-level details, that could be used to evaluate returns, for example.

Over the past year, a portion of midstream has moved in the right direction to improve the availability of ESG data, but further participation is necessary.

Environmental impact

While climate change may be the first environmental issue that comes to mind when ESG is mentioned, the environmental category comprises more than just greenhouse gas or carbon emissions. It includes operating effectively and encouraging best practices to minimize the impact on the environment. In general, carbon and greenhouse gas emissions issues are relatively less significant for midstream compared to other energy sectors, given the containment of hydrocarbons within assets, with the exception being natural gas processing and fractionation of natural gas liquids.

Instead, midstream companies are more concerned with preventing spills and addressing pipeline routing and land usage. Pipelines have been criticized by opposition groups as unsafe and hazardous to the environment, but extensive research has found the opposite to be true—pipelines are the safest mode of transportation for oil and natural gas.

One study determined that crude transportation by rail was 4.5 times more likely to result in an accident than pipelines, and the majority of pipeline accidents occurred in facilities with secondary containment measures. Pipeline spills are expensive from a cleanup and regulatory standpoint and can cause significant damage to a company’s reputation. As a result, companies have incentive to mitigate any spills through active monitoring of their assets and investment in technology that reduces risk.

In general, environmental data are not commonly reported by companies without a sustainability report, and there is little uniformity among the companies that do disclose environmental metrics. As a result, environmental metrics are mostly sourced from government data, such as U.S. Environmental Protection Agency (EPA) violations and related fines and U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA) enforcement actions.

Within sustainability reports, some companies highlighted qualitative issues like biodiversity. Midstream operations teams plan pipeline routes to mitigate risks to conservation projects or endangered species, working with government agencies and local communities to meet or exceed regulatory expectations. There is not a set industry benchmark for EPA violations or PHMSA enforcement actions, but these should be as close to zero as possible given the paramount importance of safety and environmental stewardship.

PHMSA notices range from warning letter cases that do not result in actual violations to corrective action orders requiring immediate action by the company. The average number of probable violations cases for the companies included was slightly over two per company in the study period from January 2015 through August 2019.

In general, one would expect companies with a more extensive asset base to have greater enforcement actions than smaller companies. Separately, for crude and refined products pipelines in general, the 5-year average accident rate per 1,000 miles was 0.72 according to PHMSA data. Despite an increase in pipeline miles, liquids pipeline incidents impacting people and the environment fell by 20% from 2014 and late 2019.

Social relationships

The social category of ESG refers to how a company manages its relationships with its employees and the community it operates within. Social includes issues such as diversity, workplace safety, community engagement and the pay gap within a company.

Across energy, safety has been and will remain a priority for every company. Many midstream companies begin every meeting with a safety-related discussion, which could cover anything from a review of procedures to a talk on how to prepare for contingency events. These safety discussions provide an opportunity for every employee to get into the mindset of operating safely, which is paramount when handling and processing hydrocarbons.

Companies also constantly review safety training and drills for the sake of their employees and to ensure compliance with regulations. Companies disclosed varying metrics for safety, including safety training hours and the number of safety courses, exercises and drills undertaken by employees during a given year. Notably, several Canadian companies were among a small group that disclosed the number of safety exercises and drills performed each year. In addition to safety, the social category also encompasses metrics like board diversity and the intracorporate pay gap. These two metrics that have drawn greater interest in recent years. In 2015, the U.S. Securities and Exchange Commission implemented a rule requiring most public companies meeting certain size and other requirements to disclose the ratio of CEO pay to the pay of the median employee, with companies allowed some flexibility in determining how the ratio is calculated.

The mandated disclosure of pay ratios has increased transparency in executive compensation and reveals what the median employee is paid at each company. Among the companies analyzed that reported their pay ratio, the median salary of the median employee was $111,341.

At a glance, pay ratios for the midstream space compare favorably on a relative basis to other industries. Per a 2018 report, the midstream would rank among the industries with the lowest pay gaps, with a median of approximately 67:1, and slightly below the broader energy industry at 72:1. For context, sectors such as health care and financial services typically have ratios of 150:1, given the high number of low- paid employees.

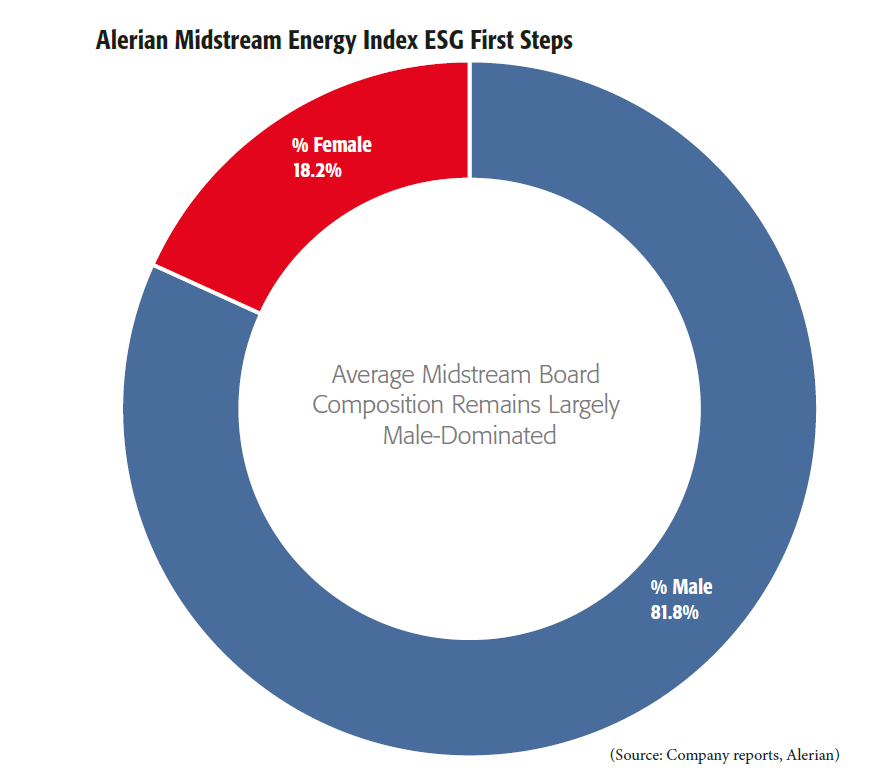

Board diversity and independence is another social issue that has been in focus. Board diversity refers to the composition of the board by gender (although other factors can be considered), and independent board members are defined as those that do not have a position within the company. Midstream boards of directors are mostly composed of male members, with 81.8% of midstream boards represented by the AMNA top 30 being male. All six Canadian companies finished in the top 10 of the analysis in terms of gender diversity on their boards, with each company having at least 25% female members. Enbridge Inc. led the constituents with a nearly even split of male and female members.

For many midstream companies, community engagement is an important piece of company culture, and most companies touted accomplishments related to charitable work and monetary donations. Given the public nature of some energy infrastructure projects, community engagement also includes how companies communicate with landowners, local governments, native people groups and the general public. While these elements of the social category are difficult to quantify, they remain an important part of the outreach performed by midstream companies.

Governance issues

Governance is defined as the actions taken by management and the board of directors to ensure accountability, fairness and transparency in a company’s relationship with its stakeholders. Rather than simply meeting regulatory or stock exchange requirements, effective corporate governance involves taking active steps to align executive and shareholder interests through consideration of economic interests, board independence and shareholder voting rights.

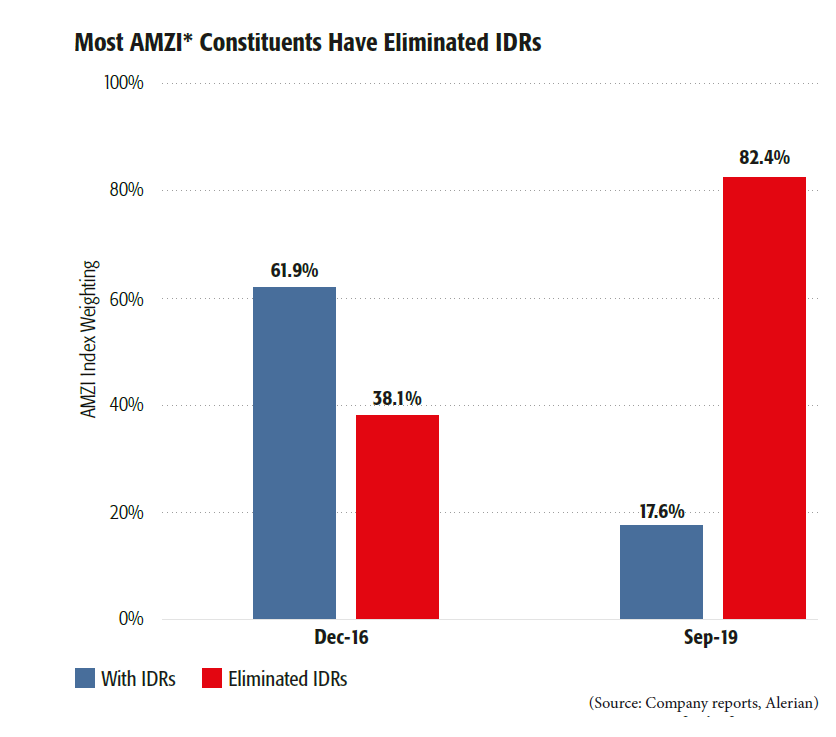

Historically for MLPs, incentive distribution rights (IDRs) have been detrimental to governance and therefore a concern for investors. Although the initial goal of IDRs was to align the interests of the MLP and its general partner (GP) early in the life of the partnership, the structure lacks sustainability as an MLP matures, and IDRs become a burden on cost of equity. Additionally, the elimination of IDRs can better align the financial interests of the GP and individual unitholders by increasing the parent’s ownership in the MLP and by putting the two groups on equal footing regarding distributions.

After IDR eliminations were recently announced by Shell Midstream Partners LP and DCP Midstream LLC, only two of the top 30 AMNA constituents, Cheniere Energy Partners LP and TC PipeLines LP still possess IDRs. The widespread elimination of IDRs is the clearest example of improving corporate governance in the MLP space.

Governance metrics

While MLP unitholders typically do not have the right to vote in board elections, there are a few exceptions to the rule. Common unitholders of Magellan Midstream Partners LP and NuStar Energy LP are allowed to vote for members of the board. Plains All American unitholders can also vote for seven members of the board, but the remaining six are designated or appointed by the GP.

A board of directors with a high percentage of independent directors is positive for corporate governance; recent research suggests that board diversity and independence can improve governance by providing different viewpoints and expertise to key decisions. The average midstream board of directors based on the top 30 AMNA constituents is made up of nearly 70% independent directors. Out of the 30 boards, seven MLP boards consist of less than 50% independent directors.

In addition to unitholder voting rights and board independence, a “skin in the game” metric within governance focuses on alignment between executives and equity owners. It measures insider ownership of common units as a percentage of total shares outstanding. Average insider ownership is a low 2.1% for the top 30 AMNA constituents, but insiders of two midstream operators—Energy Transfer LP and Kinder Morgan Inc.—own more than 10% of outstanding units/shares.

Executive compensation is often discussed in tandem with skin in the game. Executive compensation should align the interests of company management with those of shareholders. Additionally, executive compensation should not be tied too much to a single metric such as distribution growth.

What’s next?

As generalists and international investors alike continue to show further interest in ESG, the onus will be on midstream management teams to increase the information provided to allow for thoughtful decisions by investors. In many cases, midstream companies may already have extensive ESG data available as a result of risk management and monitoring practices, and the burden rests mostly in packaging these data into a report.

For companies that have already released sustainability reports, one challenge for investor analysis has been the variety of metrics used by each company. Because not every aspect of ESG is quantifiable, one management team may prefer to measure a factor a certain way, while a different management team prefers another standard. Eventually, the ideal would be a midstream space with uniform metrics that allow for efficient comparability between companies, but investors would likely settle for simply having more data available in any form.

In a review of the data available from companies, significant gaps and inconsistencies exist in what was disclosed. For example, in the environment category, disclosure of environmental metrics by companies varies between limited

or no information to granular data in sustainability reports that include details on emissions profiles, spills and other environmental compliance information.

Sustainability reports included additional commentary on biodiversity, pipeline routing and water management, among other topics.

The difference is clear for companies that currently lag on ESG reporting, and those companies should make a conscious effort to make more data and information available as a next step

ESG and beyond

Energy infrastructure companies should report any metrics that would give investors a clearer picture of how the entity operates. It is also important to note that ESG goes beyond environmental, safety and social reporting. Governance issues are just as important as environmental and social issues, if not more so as far as shareholders are concerned. Bringing these issues into focus could also help bring about an improvement in how investors view the industry in general.

The growing investor interest in ESG is an opportunity for midstream companies to highlight some of the risk management and safety practices that have long been a priority in the space. The indirect benefits of ESG are plentiful, including greater anticipation of risks, increased investor engagement and transparency and a public emphasis on important priorities like safety, which have typically been a more internal focus. Greater transparency and engagement on ESG issues may increase investor comfort that management is considering risks and opportunities appropriately.

Going forward, the first steps for midstream companies should be to make an effort to listen and engage on issues important to investors; increase disclosure of ESG metrics, including releasing a sustainability report; and promote uniformity and transparency on ESG data.

The authors are with Alerian. Bryce Bingham and Michael Laitkep are research analysts, Caroline Mahavier is a data analyst and Stacey Morris is director of research.

Recommended Reading

Wayangankar: Golden Era for US Natural Gas Storage – Version 2.0

2024-04-19 - While the current resurgence in gas storage is reminiscent of the 2000s —an era that saw ~400 Bcf of storage capacity additions — the market drivers providing the tailwinds today are drastically different from that cycle.

Biden Administration Criticized for Limits to Arctic Oil, Gas Drilling

2024-04-19 - The Bureau of Land Management is limiting new oil and gas leasing in the Arctic and also shut down a road proposal for industrial mining purposes.

PHX Minerals’ Borrowing Base Reaffirmed

2024-04-19 - PHX Minerals said the company’s credit facility was extended through Sept. 1, 2028.

SLB’s ChampionX Acquisition Key to Production Recovery Market

2024-04-19 - During a quarterly earnings call, SLB CEO Olivier Le Peuch highlighted the production recovery market as a key part of the company’s growth strategy.

Exclusive: The Politics, Realities and Benefits of Natural Gas

2024-04-19 - Replacing just 5% of coal-fired power plants with U.S. LNG — even at average methane and greenhouse-gas emissions intensity — could reduce energy sector emissions by 30% globally, says Chris Treanor, PAGE Coalition executive director.