Presented by:

[Editor's note: A version of this story appears in the January 2021 issue of Oil and Gas Investor magazine. Subscribe to the magazine here.]

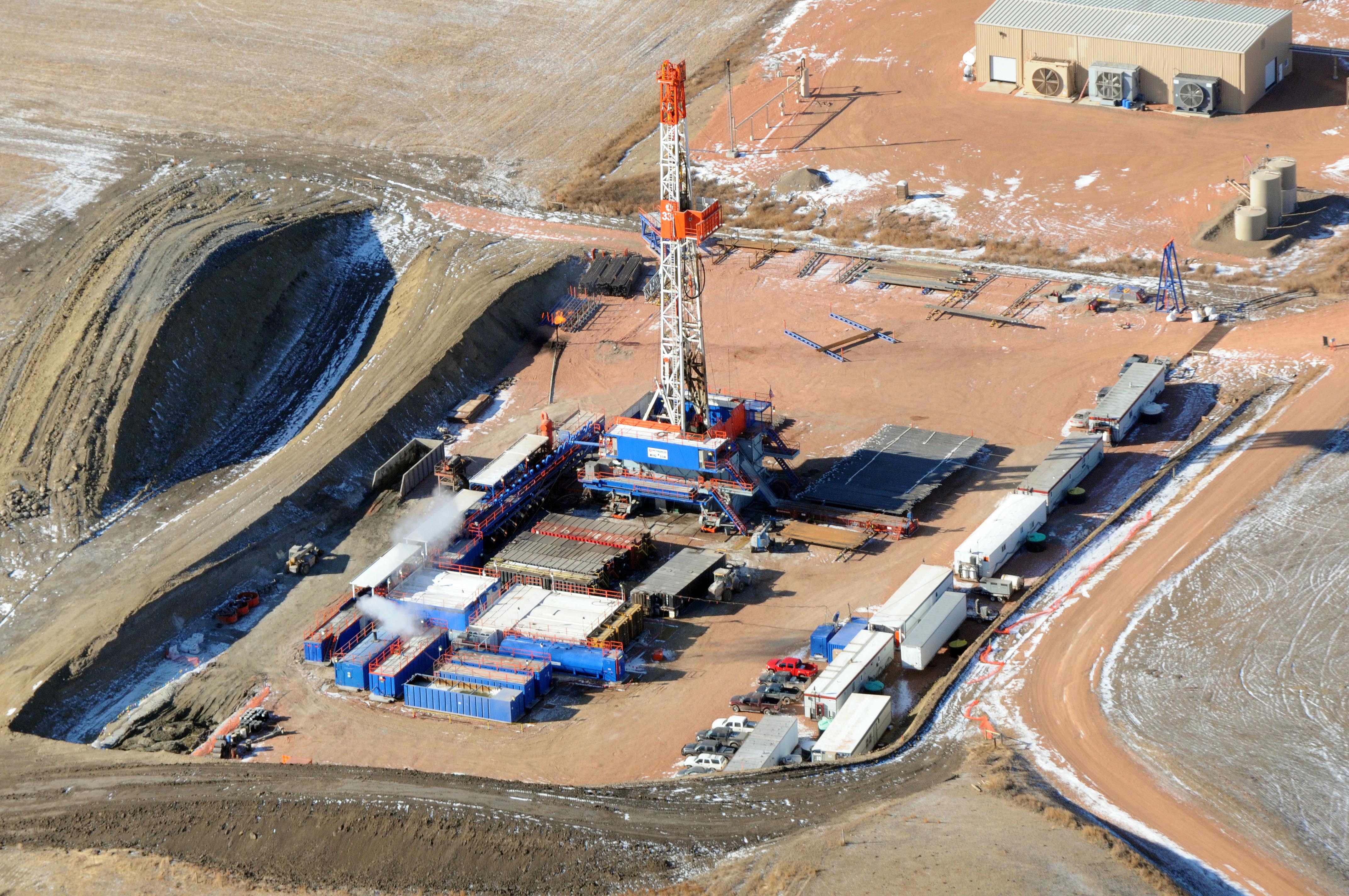

In New Mexico this summer, EOG Resources Inc. debuted a new technology to capture natural gas that sometimes flows back due to third-party midstream companies. EOG engineers in Midland, Texas, were pleased but not satisfied with the company’s 99.5% gas capture rate. But the culture at EOG bends toward perfectionism.

In the company’s Permian Basin division, in what might have been a hallway conversation between an engineer and a geologist, the question, relentlessly, was how to do it better. In this case, capture emissions.

One area that EOG cannot control is its third-party midstream disruptions. A disruption downstream limits takeaway capacity. Even with redundancies, there are times when companies have no choice but to flare the gas. Out of that occasional uncertainty came EOG’s June test of a closed-loop gas capture system, which automatically re-routes natural gas back into existing wells. “We had a team of technical and operational specialists get together to brainstorm the idea,” said Gordon Goodman, EOG’s director of sustainability. “They came up with the concept and then followed through with a successful test.”

investors after the 10-K.

The closed-loop gas capture technology will not only reduce the need to flare gas, but the system will pay for itself by conserving resources that can be sold.

The atmosphere around ESG began to change in relation to the oil and gas industry in 2020. Like the air itself, the ambiance among bankers, insurers, investors and institutional funds was invisible, but unmistakably pushed and shoved about by high- and low-pressure areas. Those stakeholders wanted assurances, or at least the veneer of assurance, that oil and gas companies are taking ESG seriously.

The environmental, or the E, has taken on an outsized significance as global capital providers have largely fallen in line with the Paris Accord climate goals to reduce carbon emissions.

Subash Chandra, managing director and senior analyst at Northland Capital Markets, said companies lately have hyperfocused on environmental topics while looking to overachieve state or federal regulations.

“At this point, you’re seeing everyone take it seriously because they have to,” he said.

That’s created the need for spending, the hiring of staff and further innovation, a paperchase of sustainability reports. E&Ps, many for the first time, began publishing principles for an effective ESG policy that broadly hits categories such as greenhouse gases, diversity and societal engagement.

Most companies have made the case that sustainability and tighter emission controls result in higher profitability—in general meaning they can sell what would otherwise be lost to the atmosphere.

CEOs, private equity firms and analysts all expect companies to continue to make progress, despite suffering under a relentlessly bad commodity environment.

Lenders such as JPMorgan Chase & Co. have made clear that ESG will be a factor in which businesses get money. Insurers and institutional investors are also beginning to ask questions about oil and gas companies’ environmental stewardship, with some E&P executives fielding calls on what they’re doing to report, and eventually, mitigate emissions.

New York capital provider Kimmeridge Energy Management Co. has been at the forefront of such efforts, including publication of its principles for an effective ESG policy that generates economic returns while committing to reducing methane emissions.

Ben Dell, a managing partner at Kimmeridge, said that the industry has a standing problem with reacting to problems and challenges rather than leading the way.

“I think the environmental discussion is a great, great example of that, where E&Ps have tended to have the view that they will do the minimum required based on what they’re told to do, rather than actually thinking about what the best practice is, what’s in the best interest” of stakeholders, he said.

Ultimately what’s forcing the industry to change now is that capital markets won’t give them any more money, Dell said. “That cost of capital will in the end force them to change or force them out of business. In that respect, the market is arguably doing its job.”

at Kimmeridge Energy

Management Co., said ultimately E&Ps will have

no choice but to conform to ESG requirements, regardless of their perception of the matter.

“The cost of capital will in the end force them to change or force them out of

business.”

Dell said that reclaiming investors may not be as big a chore as it first seems considering the state of the industry.

“First, all these companies are being priced as if they’re going out of business. So, your starting point is extremely low. It’s not a high hurdle to actually start attracting investments again,” he said.

Companies also need to make money, which Dell said is “not a big ask.” The industry, he argues, hasn’t had a problem generating cash flow but rather in spending that cashflow on drilling instead of returning money to investors.

In the past two quarters, Dell said he’s seen teams aggressively crack down on costs, capex and maintenance spending.

“They’ve been able to do it even with the trough of the commodity,” he said.

To win the ESG crowd on environmental concerns, Dell sees a relatively quick fix: Don’t flare.

“We don’t flare as a business, unless there’s an emergency use situation where it’s a real safety issue,” he said. “And all it requires is better planning, getting pipeline companies to buildout to your well locations ahead of your drilling… so that they can be turned inline to sales.”

For most companies, halting flaring has no economic downside.

“Burning your product and venting it to the atmosphere is not an economically rational thing to do,” he said. “It’s more profitable to put it in the pipeline and see that product come to fruition.”

EOG’s ESG efforts

Following the first test in New Mexico, in cooperation with the state’s Energy, Minerals and Natural Resources Department, EOG plans to consider additional sites to deploy the technology.

While 2020 saw an influx of sustainability reports, EOG has been one of perhaps a handful of independent E&Ps to produce such reports. EOG first published their report in2017. The company has shown improvements on emissions, flaring, water use and safety. For the second year in a row, EOG reduced its methane intensity rate by 45% through a mix of retrofitting and removing pneumatic controllers and field pumps.

COO Lloyd W. “Billy” Helms Jr. said that a growing interest in ESG has provided the company with an opportunity to engage with a broader audience to share the “innovative technology we have developed to reduce emissions, minimize flaring and increase water reuse.”

Growing interest in ESG has led to more transparency by E&Ps of industry operations as a whole, and environmental practices and performance in particular, which drives the dual benefit of educating more stakeholders and highlighting the benefits of responsible oil and gas development to local communities,” he said.

As various stakeholders make increasing demands for ESG, and environmental stewardship in particular, in the oil and gas industrious has responded by producing low-cost energy while also finding ways to reduce emissions and the overall footprint of its operations, he said.

“We believe investor interest will follow the demand for barrels as it gravitates toward the most efficient producers—the most efficient from a capital perspective and the most efficient from an emissions perspective,” he said.

Goodman said EOG’s approach to reporting its environmental statistics is geared toward showing its performance. In developing disclosures for the company’s sustainability report, he said EOG has tailored its metrics to be relevant to operations and as comprehensive as possible.

The company bases its metrics, where feasible, on publicly available information to aid in comparability among peers.

“While we are committed to enhancing disclosure of our policies and metrics that are important to our operations, we evaluate the success of our ESG efforts by performance and performance improvement, and just like every other area of our operations, we drive performance improvement through innovation,” he said.

Continental’s perspective

It’s clear that some companies are getting new questions, which has kicked off a mountain of new sustainability reports that highlight air, water, diversity, social engagement and other ways oil and gas communities act as stewards of their resources.

Continental Resources Inc. CEO William Berry said that some parties involved in the ESG discussion clearly want to see the petroleum industry disappear, however unworkable that might be. But various stakeholders are increasingly asking what companies are doing on the ESG front.

“What you’re seeing out there is that a lot of the banks, insurance companies—their investors are putting pressure on them to say, ‘Okay, what’s your policy around ESG,’” Berry said. “They’re wanting to make sure that that’s being considered and so … we have had conversations with those guys where they are saying, ‘This is part of the dialogue that we’re having to have with our investors.’

founder and chairman Harold

Hamm said the company, which

produced its first sustainability

report this year, has been

striving to make the company an

environmental steward for more

than 50 years.

“What I think everyone is struggling with is that ‘investors’ is a wide swath,” he said.

Continental founder and chairman Harold Hamm said much of the tumult in the oil and gas industry is due to the fluctuations in oil and gas commodity prices. And while Hamm believes ESG is largely good for the industry and Continental, he’s also wary of it being used as a weapon by investors and activists.

Continental, which produced its first sustainability report this year, has been striving to make the company an environmental steward for more than 50 years, Hamm said. For instance, decades ago the company created ECO-Pad technology that allowed for drilling multiple wells from a single site, minimizing the production profile for multiple wells. And though ESG concerns are important, price will be the ultimate determinant for investment, he said.

“Everybody wants to press ESG, and a lot more, perhaps, than it should be [pushed],” Hamm said. “Rather than [catering] to these activist groups trying to set some arbitrary goals or metrics, we believe [in] demonstrating very clearly that we’re a part and a driver of the solution, not the problem, and as such the larger issues around climate management can be achieved.”

Of its own volition, Continental Resources has already found ways to limit methane and volatile organic compounds from escaping to the atmosphere. In 2016, for instance, the company began installation of new controllers for natural gas at well facilities. Since then, the company’s greenhouse gas and methane intensity rates have fallen by at least 22% while production has increased by about 44%.

Escape the echo

The determinant factor for oil and gas companies, and other industries, is public sentiment, Chandra said. And the public’s sentiment is that climate is real. That, he said, drives everything else.

“Global capital has led the way, and that is because global capital is concerned about climate change,” he said. “Global capital is composed of the bank accounts of the global population.

“Within the past year, Chandra recalled visiting oil and gas companies to talk about environmental concerns. A few companies were talking about it but, “I didn’t get the sense [that the] rank and file felt that strongly about it.”

Instead, he got the sense they were seeing it as a political issue and that if the right people were elected it would go away.

“What really scared me about that kind of opinion is that the E&P sector has had enough issues. They haven’t gotten in front of many of them, and here’s one more issue that they are not anticipating,” he said.

Then, beginning in March, “You’ve just seen this topic be topic No. 1, and there’s no going back.”

Chandra said companies are faced with a stark choice: If they can run their businesses without public financing, they’re free to run their business as they choose, but for the others that need financial backing, companies need to be aware that climate change is driving investor decision-making.

“And so, you saw things like BlackRock and [others] adopt climate change and ESG and the Paris Agreement,” he said.

Chandra said he watched ESG approach like it was an incoming shelling dropping on an unsuspecting target and that the industry needs to lean into the ESG movement.

What it doesn’t need is to engage in long debates on climate change, he noted. It may well be that other factors cause global warming, but the prevailing sentiment is that manmade emissions are responsible. The other factor is that global temperatures are breaking records, glaciers are melting and storm activity in 2020 was at a record levels.

“If weather wasn’t so screwy, this would not be a big topic,” he said. “My point to the companies was, ‘Guys, get out of that echo chamber. It’s not going to help you.’”

Dell said there’s a misconception that to be a leader or thoughtful on environmental matters requires abandonment of economic rationales. Good environmental performance, like good safety performance, pays off, he said.

“Over a period of time, you benefit from doing it. If you have good locations and you don’t have spills, over time, you’ll benefit because the cleanup cost is lower. If you don’t flare gas wells, you also benefit over time because you can sell that product.”

SIDEBAR

PDC's Sustainability Focus

In September, PDC Energy Inc. published the company’s first sustainability report. But the company has long been at work to exceed its own expectations as well as the onerous regulations imposed by the Colorado Oil and Gas Conservation Commission.

Still, President and CEO Bart Brookman said he saw the end product as the result of building momentum around ESG and questions from a variety of shareholders.

Partly, that began in March 2020, as private equity firm BlackRock Inc. became one of the most prominent investor groups—and PDC’s largest investor—to make sustainability a focus for its investments. Banks, particularly European lenders such as Credit Suisse and Deutsche Bank, have led the way.

sustainability report has helped

to clarify that PDC’s actions align with what it’s saying.

Brookman said investors want to see a commitment to ESG and a “good summary of the progress we’re making.”

The sustainability report has also helped to clarify that PDC’s actions align with what it’s saying. Toward that end, PDC’s team assembled what the company was already doing, Brookman said, into a single cohesive report.

“I think there’s a lot of aspects of, culturally, who we are as a company,” he said, as well as the way the company has been shaped by Colorado state regulations over the past five years.

Brookman sees such reports as what the industry needs to be doing to become more transparent, more accountable environmentally and to demonstrate how E&Ps are following tightening regulations.

“We are early in our journey,” he said. “This is our first year. We plan on setting goals to make better and better progress on the E,S and G areas as we go forward. On the environmental side, we definitely have plans to improve, to get cleaner and cleaner.”

“The big thing with the sustainability report this year is that it gets all the information out there and the ratings agency scores catch up and accurately portray what we’ve been doing for years as a company,” said Kyle Sourk, senior manager of corporate finance and investor relations.

The sustainability report includes data from various company departments and then presents it in a way that the average person or state officials can easily digest.

“The sustainability report involves going out and gathering all the data, putting it into one concise report where the investment community, the banks, the board of directors and any of other stakeholders can go and look,” Brookman said.

The report also has an authenticity to it that cannot be spontaneously created. Many of the conversations and snippets of conversations quoted in the document happened over years.

“They don’t just happen when we’re putting together a report,” said Courtney Loper, senior manager for stakeholder relations, who helped create the sustainability report. “The testimonials in the report are things that we already had in our files, because that was the feedback we got in real time from some of those events and some of those partnerships.”

Through the need for innovation or at the behest of the state, PDC has also been exploring cleaner technology that it’s implemented in the past10 years, including vapor recovery units, tank pressure monitoring and loadout control among others.

“We have dramatically changed the engineering of our facilities,” Brookman said. “We have that 80% to 85% reduction in CO2 and methane emissions. And that is a collaborative effort of our field operations, engineers, regulations, and the state of Colorado saying, ‘We want you to do this,’ and we go find a way to get it done.”

That said, Colorado’s regulations can be onerous and even illogical.

“I have to shoot straight with you on it,” Brookman said. “There are times that proposed regulations have us holding our head. But I am proud of the progress we have made in these areas.”

And even without the changes in regulations, Brookman said he believes the company would still have done a phenomenal job to get cleaner.

Brookman notes that he joined PDC 15 years ago. Two years later, he hired his first safety employee. In November the company had 25 environmental, health, and safety employees working fulltime.

Advantage gas?

EQT’s new management team has been in a “fixer-up mode,” setting standards and listening to stakeholders.

While the company hasn’t felt pressure to adopt any standards yet, EQT CFO David Khani said, “We know from our conversations with investors, with banks and a whole host of what we’ll call ‘capital providers’ that the goal here is to set very tangible metrics,” he said.

“The goal would be to get to net-zero in scope one and probably scope two and think about the right timing and approach for scope three emissions,” Khani said. Pressure would come if EQT were to set standards or targets that they fail to achieve.

bifurcation between oil-based and natural gas-focused companies for these banks/capital providers, driving their investment standards to the lower emission entities over time,” said David Khani, CFO with EQT Corp.

Companies that don’t go down a path of reducing emissions will see their ability to attract capital erode.

“We see lending standards on oil and gas companies ratcheting up, and after the first conversation we had with one bank, more conversations have been occurring recently on this topic with multiple banks,” he said.

Insurers are also asking similar questions, he said. “They’re very long-term providers of capital. Their renewals might be annual, but they’re expecting to be with us for many years,” Khani said. “They’re asking us about our current ESG focus, so they understand these are rising risk determinants on capital… we’re providing transparency into our ESG practices, which goes beyond the standard environmental focus.”

These sorts of conversations have picked up in the past two or three years from typical conversations regarding property and surety lines and now translate over to areas such as casualty insurance.

Khani expects the industry to find itself sundered into more distinct camps of oil and natural gas. He expects pure natural gas producers such as EQT to have a sizeable advantage over coal and oil companies.

“I would say there’s going to be a major bifurcation between oil-based and natural gas-focused companies for these banks/capital providers, driving their investment standards to the lower emission entities over time. It’s not like they’re not going to lend or invest in an oil company, but if you don’t have a much more rapid reduction in emissions, their ability to lend or invest with them over time will erode.

“I haven’t seen that yet, but it’s probably coming. So, there will be bifurcation from the investment community on a gas versus oil. It’s going to come,” he said.

The same is true for “dirty” natural gas providers.

E&Ps will first face a profitability hurdle before banks and institutional investors back and trust them due to the poor investment performance of the group. Then they will choose the companies they want to work alongside.

“If you have two companies with the same economic profile, but one is a better steward of the ‘E’, lenders will gravitate to that company. In essence, they will use that as a second filter for sure,” Khani said. “And in our conversations with different institutional investors, they are ranking companies from an ESG perspective.”

Some have simple “one to five” rankings. Others use different ranking mechanisms. But again, a second filter on picking and choosing winners and losers.

“I have not seen that extreme yet, but it’swhere it’s the broader market is heading becauseyou’re seeing this occur from the more sophisticated, larger investors now,” Khani said.

A complicated picture

Not everyone is convinced that oil and gas companies will need to meet ESG criteria to find investors.

Hamm said the American model of production, which is highly regulated and controlled, has already reduced emissions. The U.S. saw emissions drop by 77% since 1970, including during a recent ramp up period in which production rose by 2.5x.

Continental’s Berry said the world needs multiple forms of energy and it has for quite some time. But managing carbon dioxide would be far easier if the world switched from coal to natural gas.

“You’d probably see a 20% reduction from fossil fuels just by switching to natural gas. That’s what happened in the United States. That’s why we’ve been able to meet part of the Paris Accord today. We achieved that because of natural gas.”

Berry said that ESG has become far more visible of late, though like Hamm he said that ESG has long been one of the fundamentals driving the industry.

“It’s a continuous drive for improvement,” he said. “We don’t see this as a static environment.”

Berry also said separating the need to reduce emissions from energy poverty throughout the world is short-sighted, since some nations may rely on coal rather than natural gas for their power generation needs.

“There’s 10% of the population that is European and North American that are trying to drive the narrative for 100% of the population of the world,” he said.

The company also exceeds flaring requirements in the Bakken and captures 99.5% of its emissions, Berry said. North Dakota’s overall gas capture target was 93% in September 2020.

“We’ve helped the states try to drive their requirements to higher and higher levels to appropriately reflect what needs to be done,” Berry said. “For that gas capture, we’re 99.5% and we’re still looking at opportunities to go even further.”

While commodity prices may rise in some unforeseeable way, Kimmeridge tends not to be swept up in the euphoria of the industry’ speaks and valleys.

“We are able to sit back a little bit more and look at the overall market and say, ‘Listen, if you’re competing for capital in this market, you have to be relevant. You have to be investable,’” he said. “And that isn’t just about being investable within the energy space; it’s about being investable for everyone. It’s about competing for capital across the stock market against other companies.”

To do that, Dell said a more forward-thinking view of the industry in the next one or two decades is required.

Dell notes that oil and gas companies have lagged behind in diversity—and not just in terms of ethnicity or gender. Industry boards are dominated by other energy company executives. He sees this as a pitfall that leads to group thinking about what a company should do.

“At the end of the day, if you look at where we are today, we’ve had this herd mentality about ‘What is the right business model for the industry?’ and ‘How should we run our companies?’ And as a result, the industry’s driven itself into the ground over the last decade.”

SIDEBAR

A Model for Mitigating Emissions

While many institutional investors are running away from oil and gas on the premise of ESG concerns, Kimmeridge Energy Management Co. is running toward them. Kimmeridge, which makes both public and private investments in the oil and gas space and whose principals are rooted in the oil and gas industry, believes it can effect environmental change better from the inside out.

In February last year it published a white paper, titled “Charting A Path To Net Zero Emissions For Oil & Gas Production,” on how E&Ps big and small can and should do their parts in mitigating greenhouse gas emissions.

“Kimmeridge intends to advocate for change in the sector through its investments,” the report stated. It believes that companies it invests in should adopt the following five key principles:

1) Eliminate routine flaring by 2025

2) Reduce U.S. methane intensity below 0.2% of gas production by 2023

3) Reduce total upstream GHG intensity by 50% by 2030

4) Pursue routine monitoring and independent verification of emission levels

5) Align reporting with SASB standards and adopt all 11 TCFD recommended disclosures by 2022

Specific steps should include:

1) Disclose the specific actions being taken to meet intensity reduction targets (scope and frequency of leak detection and repair (LDAR) program, replacement of pneumatic devices, installation of vapor recovery units (VRUs), use of plunger lift, field electrification, etc.)

2) Outline the steps being taken to monitor the effectiveness of flare units and ensure zero flaring by 2025

3) Increase independent monitoring and verification of atmospheric readings with transparency into how it correlates to internal calculations

4) Provide independent certification of emission intensity (i.e., Intertek’s CarbonClear), especially if linked to executive compensation

5) Aspire for continuous on-site emissions monitoring as the technology improves and costs are reduced

Good environmental performance is also good business, the report promotes, and the New York investment house intends to advocate for improvements in environmental performance, disclosure, verification and target setting for the E&P sector that are measurable and impactful via its capital placements.

“As the world transitions to a low carbon future, the upstream oil and gas business must evolve and address its own environmental deficiencies. The leading E&P companies of tomorrow will adopt a business model that is aligned with the energy transition through lower reinvestment rates while charting a path toward net zero emissions in their direct operations. This is critical for attracting investors back to the sector.”

Next ESG steps, and beyond

EQT itself is starting in a good position on emissions, Khani said, and focusing on becoming cleaner. The company is starting to track emissions on, for instance, water trucks and has implemented measures to electrify parts of its operations and increase its monitoring for leaks in real-time.

EQT, which has published sustainability data since 2012, reported zero flaring of natural gas in the past two years. Last year, the company also reduced fugitive emissions of carbon dioxide equivalents by more than70%, to 6,816 metric tons compared to 23,200 metric tons in 2018.

“One bank said to us that we’re at such a low level of emissions right now that there’ll be a whole host of companies that could spend 10 years and never get to the same spot where we’re starting at,” he said.

The company is also looking at renewable technology, though “It’s not a sunny place in Pittsburgh, so we can’t always rely on solar,” said Charity Fleenor, EQT’s environmental affairs director.

In one project, EQT has looked at more closely monitoring methane leaks from pneumatics. The Environmental Protection Agency (EPA) typically identifies gas pneumatics as a primary source of emissions and accounts for about 60% of what is reported to the agency, Fleenor said.

“We’ve looked at different ways to capture that information and recently presented that to EPA,” she said. Moving forward with such practices is a “matter of constantly keeping on top of the technology, understanding how and if the technology works for us. That’s really what we’re targeting right now,” she said.

EQT recently presented an alternative method to calculate emissions from pneumatics to the EPA.

Fleenor said EQT looked at emissions actually generated from equipment compared to a blanket emissions calculation that EPA utilizes. Fleenor said EQT presented all of the data, good and bad, and the EPA was receptive of the thought process and appreciated the transparency. While it is uncertain if the agency will approve the alternate calculation methodology, EQT still considers this a win.

“I’ve been working in this industry and the environmental space for almost 24 years,” she said. “And I’ve never had an agency give us a thumbs up on something we’ve done like that.”

For E&P companies, beginning to compile a report can be onerous. However, many companies and analysts pointed to the Sustainability Accounting Standards Board (SASB), which provides a template for reporting carbon emissions and other ESG measures. SASB provides standards for 77 industries.

Swapnil Karnik, Columbia Threadneedle Investments’ research analyst for oil and gas, said ESG has triggered tangible impacts across several different fronts. More assets under management are starting to incorporate ESG perspectives into their portfolio construction process. That usually has an impact for how much capital it is willing to invest in companies, which don’t necessarily score as high on some of the ESG factors.

From a financing perspective, banks are increasingly measuring their impact on climate and climate risks while limiting their exposure to fossil fuel companies. Even Federal Reserve Chairman Jerome Powell has said it will look into how to incorporate climate change and risk into what they do, with the potential to affect monetary policy, bank regulation and financial stability.

gas, Columbia Threadneedle, said, “Once you start measuring [ESG] and reporting it, people want to get better at it. So maybe the first reduction

that happens is all the easy

things that you do. But even that is a good thing.”

“We haven’t necessarily seen a big shift yet in my opinion, but you’re starting to see more pressure on banks starting to carve from investors in terms of their own company disclosures,” Karnik said.

E&Ps may not have seen a “deep impact” yet from a bank-financing standpoint, “but in the changing environment, I think we’re probably going to see some impact from available key lender, credit facility issues,” Karnik said. Those may apply to certain debt refinancings that might include higher scrutiny on ESG matters.

So far, however, banks with direct exposure to fossil fuel companies haven’t made any significant changes from the recent past.

“There has been no meaningful impact in terms of banks limiting their exposure to fossil fuel companies because of ESG matters; though, that might change given the changing environment,” he said.

But ESG questions are more likely starting to be asked now.

“If your credit facility is coming up for a refinancing, you’re probably going to get more questions on how you think of ESG issues than the last time you refinanced,” he said.

“We do encourage our companies to focus on the standards and try to improve their disclosure on those fronts,” Karnik said.

While oil and gas companies are regulated by a number of state and federal agencies, some data are self-reported. The initial accuracy of the reports is not necessarily as important as simply making an initial disclosure, he said.

“We are not necessarily making an argument for methodology behind the data that’s being captured,” he said. “That is an issue that’s clearly there within the industry, and I think those discussions are going to evolve.

“What we like about SASB is they have identified the critical ESG issues and, based on those issues, what factors should be disclosed by the company. That’s the first step we would like the industry to wholeheartedly adopt.”

Beyond an initial report, emphasis shifts from what is initially reported to improvement.

“I think our focus more is more about showing progress, year after year, setting targets and tying those targets to compensation and that’s what we focus on in our engagements,” he said. “Obviously, then you’d start on a new objective.

“Once you start measuring it and reporting it, people want to get better at it. So maybe the first reduction that happens is all the easy things that you do. But even that is a good thing.”

In 2020, there were perhaps dozens of inaugural sustainability reports published. Chandra said he mainly looks at greenhouse gases, total emissions, carbon and methane.

He believes that the corporate sustainability report will ultimately be the most important document a company publishes after the 10-K for investors. The reports also provide a way to begin ranking companies based on their emissions. The question now is whether the rest of the industry will follow suit.

“So, you either are part of the solution, or you’re the villain,” he said. “Why play up to the role of the villain when they already think you’re one?”

Recommended Reading

Santos’ Pikka Phase 1 in Alaska to Deliver First Oil by 2026

2024-04-18 - Australia's Santos expects first oil to flow from the 80,000 bbl/d Pikka Phase 1 project in Alaska by 2026, diversifying Santos' portfolio and reducing geographic concentration risk.

Iraq to Seek Bids for Oil, Gas Contracts April 27

2024-04-18 - Iraq will auction 30 new oil and gas projects in two licensing rounds distributed across the country.

Vår Energi Hits Oil with Ringhorne North

2024-04-17 - Vår Energi’s North Sea discovery de-risks drilling prospects in the area and could be tied back to Balder area infrastructure.

Tethys Oil Releases March Production Results

2024-04-17 - Tethys Oil said the official selling price of its Oman Export Blend oil was $78.75/bbl.

Exxon Mobil Guyana Awards Two Contracts for its Whiptail Project

2024-04-16 - Exxon Mobil Guyana awarded Strohm and TechnipFMC with contracts for its Whiptail Project located offshore in Guyana’s Stabroek Block.