[Editor's note: A version of this story appears in the March 2020 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Getting your arms around environmental, social and governance (ESG) issues can be quite some task. As one observer noted, current criteria used to evaluate ESG issues are “highly diverse on a massively complex subject.”

ESG issues have never before claimed such importance. Public companies, no matter in what sector they may operate, “ignore this at their peril,” according to Pavel Molchanov, an energy research analyst at Raymond James & Associates Inc.

On the environmental issue alone, the divide is wide—very wide—in terms of opinions. As one industry magnate summed up, there are two sets of people: one that denies climate change is occurring and another that “thinks it will be easy to solve.”

With some $7.43 trillion in assets under management, BlackRock hit the headlines when CEO Larry Fink touched the subject of “sustainability-related risk” in fossil fuel stocks. Action has to be taken now, he urged, but the issue is not going away anytime soon.

“We’re not running away from all hydrocarbons, because we do believe they play a role,” said Fink in a CNBC interview. “The climate change is going to require a huge energy transition. It’s going to be 40 or 50 years. So we’re not running away. We need to have an organized plan.”

European political leaders have led the charge but not without ESG issues on their doorstop. Germany still relied on lignite coal—a coal with higher carbon emissions—to generate 22.5% of its electricity in 2018. Some $45 billion of government funds have been earmarked to phase out coal by 2038.

In January, world leaders gathered at the World Economic Forum in Davos, Switzerland, where ESG issues were one of the more frequently addressed topics. The “No. 1 hypocrisy,” one commentator noted, was that such a large number of world leaders arrived by private jet.

In the U.S., the active part played by consumers of energy was similarly highlighted by David Swensen, Yale University’s chief investment officer, in a publicized speech.

Divesting energy holdings, he argued, unfairly targets producers rather than consumers. “The real problem is the consumption of fossil fuels. And every one of us in the room is a consumer. And I guess it’s a little harder to look in the mirror and say ‘I’m part of the problem.’”

All things considered, where do the chips fall for energy firms trying to navigate around ESG issues?

Like it or not, ESG-related issues are now front and center among investors, particularly those that view energy as having entered an era of “abundance” from a previous one marked by energy scarcity.

Subash Chandra, senior equity analyst covering the E&P sector at Guggenheim Securities, is adamant that ESG issues are here to stay. If anything, investors are prone to treat ESG issues as a read-through to the quality of overall management performance. “If a company decides to do one thing well, it will tend to do all things well,” he observed.

It’s in the interest of the E&P sector to “be a good neighbor,” said Chandra. It will only benefit the sector if it maintains standards that are higher than regulations in force at the federal, state or local level. If E&Ps hold themselves to a higher level, it reflects a sign of “leadership,” he added.

Chandra noted that 2018 and 2019 had seen significant changes in terms of proxy voting on various ESG-related issues by investors. And, of course, everyone wants a “safe workplace environment” from a health, safety and environmental viewpoint.

“But the train bearing down on us is decarbonization,” he observed. “It’s a global phenomenon.”

Decarbonization in Europe

In Europe, where the decarbonization trend is typically strongest, some European banks have pulled back from providing finance to certain energy sub-sectors, noted Chandra.

“The number of interested parties is large enough to disrupt capital flows,” according to Chandra. “It’s the money that greases the wheels. If you don’t need the money, you may not need to worry about it. You may have the luxury of saying, ‘I don’t need capital throughout the organization.’ But even some smaller areas, like business insurance, are involved.”

In a recent report on greenhouse-gas (GHG) emissions, Chandra noted that the U.S. accounted for 11% of global GHG emissions, based on 2018 data from several sources, including CAIT Climate Data Explorer. Over the past decade, GHG emissions in U.S. and Europe have trended downward, while those for India have moved higher, and emissions for China have risen sharply but show signs of leveling out of late.

The oil and gas sector is mainly associated with methane and CO2 emissions, with the former known for having markedly higher heat-trapping potential than CO2, noted Subash.

Power generation and transportation are the two largest sources of GHG emissions in the U.S. It is fossil fuel consumption—rather than fossil fuel production—that is the “overwhelming driver behind CO2 emissions,” according to Chandra. Combustion of fossil fuels accounts for 93% of emissions, with power generation and transportation making up 73%, between them, split almost evenly.

“The battle to contain CO2 emissions will have to occur mainly with cars, trucks and power plants,” said Chandra, while oil and gas producers are “bit players in the CO2 debate,” he commented. However, they could be impacted by decarbonization of the global economy, or they could play a role in helping attain GHG goals through use of carbon sequestration techniques.

As for methane, the energy sector has a larger hand in its emissions, with upstream and midstream sectors accounting for roughly 30% of methane emissions as compared to only 1% of CO2 emissions, according to Chandra. However, while less prevalent than CO2, methane is some 25 times more potent than CO2 in trapping heat, he noted.

In a binary decision as to either flare natural gas or vent it, the choice of flaring—so as to produce less heat-trapping CO2 emissions—does less harm from an environmental viewpoint. However, both of the above options fall short, from both an environmental and a commercial perspective, of a more optimum practice of avoiding leaks and fully capturing natural gas volumes to take to market.

As one analyst observed, capturing the above emissions is in essence “a win-win.”

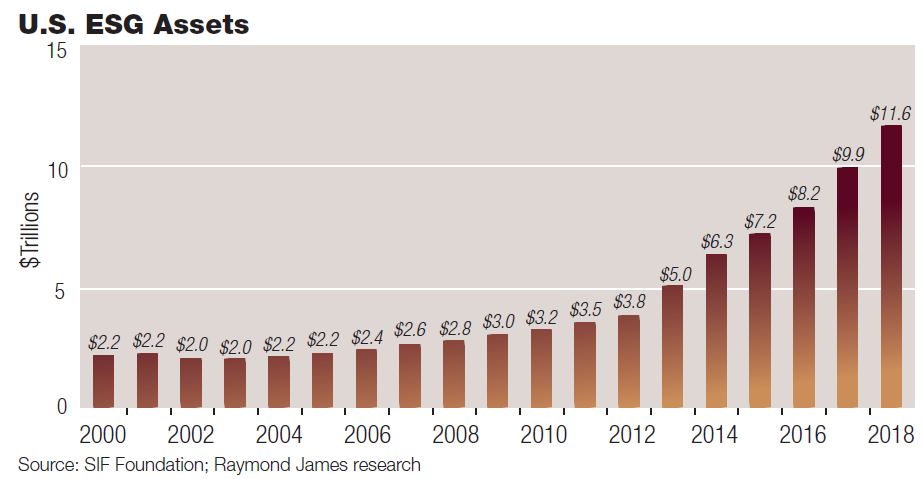

$11 trillion ‘off limits’

Molchanov described the trajectory of ESG investing as being “firmly upward and onward.” Professionally managed funds in the U.S. that are subject to some form of ESG criteria have tripled in size since 2012, reaching over $11 trillion, he noted. This represents roughly 26% of professionally managed (versus passive or index) equity and fixed income funds.

If public companies want to maximize their access to capital markets, attracting institutional investors is likely to be hampered by the absence of appropriate ESG credentials, said Molchanov. And with 26% of actively managed assets already “off limits” of late, the headwinds will only stiffen if the trajectory of ESG-oriented funds continues on a path of further market share gains.

Rather like rating agencies that deal with a company’s financial standing, a number of rating agencies—some say 50 or more—have sprung up to provide an evaluation of a company’s ESG metrics. However, unlike the more precise analysis possible in the credit sector, the ESG sector finds itself in the midst of a growing number of rating agencies using confusingly differentiated criteria.

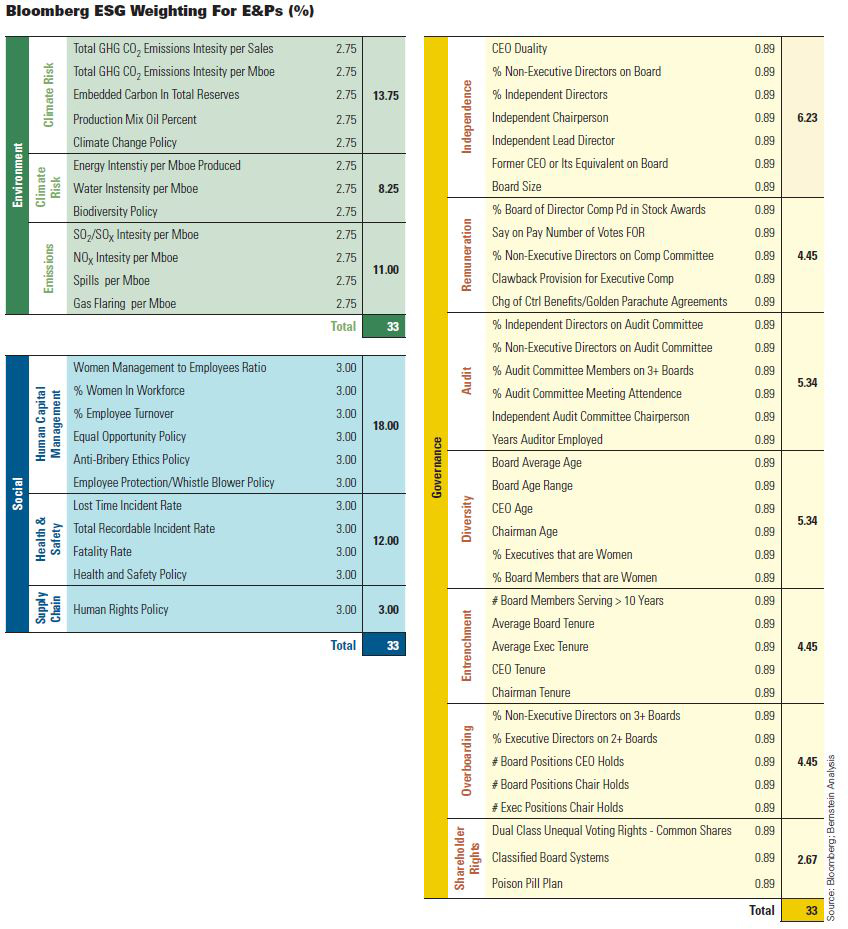

Molchanov offered a review of typical ESG sub-categories around which E&Ps must now navigate.

“As a rule of thumb, roughly half of the ESG score for an oil and gas producer pertains to environmental metrics,” said Molchanov. “The highest-weighted component in this category is the carbon intensity of its operations, followed closely by other types of emissions and waste. Other factors include impacts on water, land use or any use of toxic materials, etc.”

The other half of the score, in rough terms, is made up by the social and the governance weightings. These are more directly comparable to industries other than energy. For example, health and safety falls under the social heading, while community relations and board independence fall under governance. Here is a breakdown of the average weightings for E&Ps rated by Sustainalytics:

- Environmental: 51.5%, comprised of carbon—own operations at 16.5%; emissions, effluents and waste at 15%; carbon—products and services at 13.9%; land use and biodiversity at 3.2%; resource use at 2.9%;

- Social: 12.4%, comprised of solely occupational health and safety; and

- Governance: 36.1%, comprised of community relations at 11.4%; corporate governance at 7.9%; bribery and corruption at 7.2%; human capital at 6.9%; business ethics at 2.7%.

“If management takes the time to publish a sustainability report, that will help the ESG score but not by much,” said Molchanov. “The way the score can be improved significantly is when companies are taking genuine steps to improve their operations. Publishing a sustainability report with an ESG strategy and some targets spelled out in it will tell ESG analysts that you’re getting serious.”

This sends a “positive message,” he added. “But management ultimately has to deliver on the strategy.”

In general, an ESG score is assigned based on a company’s performance relative to other companies in the same or a similar industry. For example, said Molchanov, an E&P is typically compared to another E&P, or possibly, say, a pipeline company. Ultimately, however, the score will reflect a degree of discretion on the part of the ESG analyst, he observed. “A lot of it is more art than science.”

In addition, the score will to some degree reflect the hydrocarbon mix of a company’s production and reserves. As is well-known, “gas has a lower carbon footprint than oil,” he noted. “So a company producing predominately gas will get a better score, other things being equal, than a company that produces predominately oil. That’s the nature of the asset and the geology.”

A higher score may depend more on actions that a company can do on the operating front. Positive moves may include the use of electric fracturing in place of traditional diesel fracturing,” he continued. “Or companies can replace diesel generators with solar generators and batteries. In addition, they can opt to minimize flaring, which reduces CO2 emissions into the atmosphere.”

These measures are not without cost, but over time they will tend to pay for themselves with lower operating costs, according to Molchanov. For example, a company may use an existing diesel generator—viewed as a sunk cost—to provide electricity, but it has to buy diesel regularly to run it. By contrast, with a solar system and battery, there is an upfront cost, but operating costs are nearly zero “as sunlight is free.”

Not losing money

A policy of “having good ESG practices does not have to mean losing money,” said Molchanov. “These cash outlays aren’t made just out of the goodness of somebody’s heart. There are ways to implement ESG strategies that are profitable. And a better ESG score has the potential to broaden the scope of investors and, in turn, enable the company’s stock to trade at a higher valuation.”

A similar viewpoint was put forth by Molchanov for costs of training, etc., in the social aspect of ESG.

“If people are better trained, they will make fewer mistakes, and there will be fewer accidents,” he said. “And a better trained workforce is generally a happier workforce, which means they will likely stay longer at a company instead of jumping ship. That reduces turnover, which saves money in the long run. It’s another example of how an upfront investment can deliver dividends over time.”

Bill Thomas, CEO of EOG Resources Inc., makes it clear that sustainability is a top priority for his company.

“Being a good corporate citizen goes hand in hand with delivering long-term value to our shareholders,” said Thomas. “Responsible stewardship of our resources is essential to our long-term sustainability. Put simply, to create long-term value for our shareholders, we must be good stewards of all our resources: our assets, the environment, our people and the communities where we live and work.”

Moreover, EOG’s sustainability strategy is designed to improve key metrics across all three ESG fields.

“EOG’s culture is our sustainable competitive advantage. Our culture is one of continuous improvement throughout all aspects of our operations,” said Thomas, noting EOG’s drive to innovate, improve efficiencies and reduce costs. “That same focus extends to our environmental stewardship, fostering diversity of thought, experience and background at all levels of our organization, and making a positive community impact on a local, national and global scale.”

EOG’s sustainability report for 2019 will be its third. Previously, much of the information in the report was disclosed on the company’s website and is updated annually. The company noted that, in response to stakeholder interest in greater disclosure of EOG’s climate-related risk assessment and management, it integrated in 2018 with recommendations by the Task Force on Climate-related Financial Disclosures organization.

Reducing methane emissions

One of the first items addressed in EOG’s 2018 sustainability report focuses on methane emissions. While methane made up less than one-eighth of EOG’s total GHG emissions—12.25% versus 87.68% for CO2—its potential heat-trapping effect makes reducing methane emissions a priority. EOG set for itself a “qualitative goal for 2019 to reduce our methane emissions intensity rate below 2018 levels.”

EOG was able to report a reduction in its methane emissions intensity rate of more than 45% in 2018. This stemmed from an initiative to retrofit or, where feasible, remove high-bleed pneumatic controllers from operations. Pneumatic controllers are used in energy production to regulate equipment pressures, temperatures and liquid levels, typically utilizing pressurized natural gas to open and shut valves.

“We’re optimistic we’ve reduced our methane emissions intensity rate further in 2019,” said Creighton Welch, manager of government relations and communication for EOG. “Retrofitting a controller from high-bleed to low-bleed results in an approximate 96% reduction in methane emissions,” Welch noted, citing Environmental Protection Agency data. High-bleed designs still made up 62% of controller methane emissions in 2018.

A GHG emission intensity rate is measured by comparing the tons of methane (or CO2 equivalent if a conversion rate for methane is used) that are emitted for every thousand barrels of oil equivalent.

Water recycling and reuse

A water intensity rate is also calculated to assess improvements in recycling and the reuse of water by EOG. The intensity rate measures barrels of water used for each barrel of equivalent produced in the U.S.

“To accelerate implementation of best practices in water management, EOG has formed a strategic water resources team with representatives from each of our operating area offices,” said Welch. “The team evaluates the life cycle of water used in our operations, from acquisition through transportation, storage, production, treatment, reuse and disposal.”

The focus of the team is to determine water quality needs, develop multiple alternative water source options and maximize recycling and reuse options. Reuse is a term used by EOG to categorize treated fluid and/or produced water that is generated by the company’s operated oil and natural gas wells.

“We expanded our water reuse operations, increasing our percentage of reuse water to more than 20% and to much higher levels in the Delaware Basin,” noted Welch. “On a combined basis, reuse and non-fresh water provided nearly two-thirds of our water needs in 2018, consistent with our efforts to minimize fresh water use.”

The team also focuses on water transportation infrastructure to maximize water moved on pipelines and to reduce truck traffic. In 2018, EOG transported 99% of its Permian Basin water by pipeline.

EOG is also far from timid in terms of innovation. Following the oilfield service sector’s development of “e-frac” equipment, “EOG is a first mover in, and we believe the largest user of, electric-powered hydraulic fracturing,” observed Welch. In a different area, for example, EOG is experimenting with drones in efforts to monitor leak detection more efficiently.

On governance issues, EOG can point to independent directors making up 88% of its board members. In January of last year, Julie Robertson joined the board of directors, 25% of which comprises women, and in April, she was named chairperson of the nominating, governance and sustainability committee. In August, Gordon Goodman was also named as the first director of sustainability.

Transparency for stakeholders

Southwestern Energy Co. is quick to emphasize the importance of looking at all three ESG components.

“With respect to the environment, being a good steward of our natural resources and environment is vital to being a responsible operator,” said Jim Schwartz, director of corporate communications. “But you also have to keep a perspective on social and governance issues. Fund managers are spending greater efforts on all three issues, as investor focus has widened, especially among pension funds and endowments.”

Southwestern has seen investor interest move in a number of areas over time. On environmental issues, for example, a focus mainly on liability exposure has transitioned to the long-term sustainability of the business. Governance issues, once centered on Sarbanes-Oxley compliance, have shifted to focus more on appropriate management incentives and actions to benefit shareholders and other stakeholders.

“Southwestern endeavors to be transparent to all stakeholders: shareholders, employees, contractors, neighbors, government officials,” said Schwartz. “By focusing on performance and engaging stakeholders on ESG matters, an operator like Southwestern can demonstrate that we understand our responsibility to do business the right way.”

Southwestern published its first corporate responsibility report in 2015 and has continued with a report each year since then. In addition, the company files a report with the Global Reporting Initiative. This allows Southwestern to provide information to rating agencies that the agencies may have missed. Among rating agencies, MSCI, ISS and Sustainalytics are cited as being “highly impactful.”

Reducing methane emissions is a key goal for Southwestern. Methane performance metrics are on the scorecard used to evaluate senior operating executives at the firm, and the board of directors regularly reviews the subject. In 2018, Southwestern achieved a leak/loss rate 0.056%, which was 96% below the industry average of 1.62%, based on a National Energy Technology Laboratory report.

In overall GHG emissions, Southwestern saw a 39% improvement on a year-over-year basis in 2018. The company said its leak detection and repair program exceeds the standards of many of its peers by covering all operational facilities, equipment and components. Southwestern said it has no high-bleed controllers in its current facilities and does not use them in new facility design or installation.

Freshwater neutrality

In terms of a water resource strategy, “the company’s commitment to freshwater neutrality is unprecedented in the oil and gas industry,” according to Southwestern. Its commitment to being freshwater neutral is “a key part of meeting our goal to be a model operator and lead the way on responsible unconventional energy development,” it said.

“While we seek to minimize our use of fresh water as much as possible, primarily through water reuse and recycling, we know our operations will continue to need fresh water,” said Southwestern. “That is why we have committed ourselves to achieve and maintain fresh water neutral operations. We attained this goal in 2016, 2017 and 2018, and we believe we are the only oil and gas operator to achieve this benchmark.”

The Southwestern formula for fresh water neutrality is when “total water used in its operations is less than, or equal to, the sum of alternative and reuse water, operation offsets and conservation offsets for each of its operating areas.”

Last October, Southwestern announced it had returned more than 10 billion gallons of freshwater to the environment through “its comprehensive approach to optimizing water usage and 10 innovative, company-sponsored water conservation projects.” Its commitment to freshwater neutrality meant that “each gallon of freshwater used is replenished or offset,” it added.

Ashley McNamee, director of communications and corporate responsibility with Whiting Petroleum Corp., cited several reasons why investor focus on ESG issues has been gaining momentum.

“If you’re a company approaching sustainability in a productive way, you have the ability to add value to your company,” said McNamee. “Sustainability practices and some of the metrics within a sustainability framework offer ways to achieve efficiencies and to create and drive long-term value, which of course makes a company more sustainable—hence the term.”

“The other perspective relates to the investment audience. We’d heard several years ago that European investors were reluctant to invest in our stock because our disclosure was not robust enough. That isn’t why we started an ESG program, but it’s something we’ve watched over the years. Now, investors like BlackRock have made it clear they expect companies to report on sustainability.”

[SIDEBAR]

Quantum's ESG Strategy

Quantum Energy Partners has been a long-time advocate of environment, social and governance (ESG) principles, according to managing director, Sean O’Donnell. As a private-equity sponsor, he sees the firm having greater scope and flexibility for ESG to contribute to the “business case” of energy investing rather than a short-term “check the box” role played in some parts of the public sector.

“There is a business case for ESG,” affirmed O’Donnell. “Being private, you can be inwardly focused on developing your own business case with your key stakeholders, such as limited partners (LPs), management teams and lenders,” he noted. “That’s where private-equity sponsors have an advantage over our publicly traded peers.”

“The dialogue with our stakeholders around ESG has evolved to now include a consistent theme about value creation and retention around ESG,” said O’Donnell. “Key issues are: What is the business case that we’re developing around the ESG data? How is it going to make our assets better? And how is it going to make our investment more valuable?”

Putting ESG protocols on paper is nothing new to Quantum, whose funds have numerous overseas investors, including sovereign wealth funds, major public pension funds, etc.

“We’ve done it for years,” said O’Donnell. “We write it into our governance documents. For each of our portfolio companies, we do ESG diligence screens and establish protocols before we engage with a company. It is part of our due diligence, and it’s a closely monitored element of the business as every program requires a degree of customization.”

As examples, said O’Donnell, “water issues in New Mexico are different from water issues in West Virginia. And worker safety programs and community relations on our drilling sites are different from our various solar construction sites.”

With European investors typically in the forefront of ESG, Quantum is well aware of rising ESG priorities. As the universe of LPs interested in energy investing is getting smaller in size and smarter on ESG, the bar is rising in terms of the level of the ESG dialogue, he observed.

“Some of our largest investors are in Europe, and they have sophisticated ESG programs,” O’Donnell commented. “We mutually share best practices, mistakes and successes with their ESG investments in order to continuously improve and benchmark our programs. We have the benefit of a private, direct dialogue with our investor base about what our ESG business case should be in various business lines.”

For example, the days of slide decks showing ESG criteria in meetings are long gone, said O’Donnell. “Investors say: ‘Don’t give me PowerPoints; show me how it’s actually being implemented,’” he said.

The returns on investment from ESG measures provide “a fundamental litmus test,” even though “not all the benefits are numerically available today,” according to O’Donnell.

“If I have a robust ESG program for the next five years of operations, what is that worth to a potential buyer?” he asked. “I may not have an exact answer to that today, but it’s certainly worth something. It’s costly, if not impossible, to retrofit an asset after years of lost time to bring it up to best-in-class ESG standards. Doing anything late and in a hurry is expensive, and astute buyers should see it from a mile away. So there is value there.”

Also, when the A&D market reopens, a priority will be to have portfolio assets in shape for a potential sale after an extended hold period by private-equity sponsors.

“The large majority of private-equity exits are ultimately to public companies,” said O’Donnell. “Hold periods have been longer, and our portfolio companies will be larger at the time of exit. Our counterparties will be the larger surviving public companies whose ESG standards are going to be rising. And so we need to be keeping up, if not staying ahead, on key ESG topics.”

The point is “you’ve got to give the public companies reasons to say ‘yes’ across a number of deal metrics, including ESG, to make the transactions go smoothly, especially where you’ve got multibillion portfolio companies,” said O’Donnell.

How is Quantum changing its strategy, if at all, to the rising tide of ESG and climate change concerns that are absorbing much of the conversation among major investors?

“Our conversation with them is: ‘We are a private-equity firm that invests broadly across the energy value chain. We are not going to change what we do—investing in energy,’” said O’Donnell. “But we are committed to continuously improving how we do it. And that’s where our strategy includes an ESG lens. How can we become better energy investors and producers by involving ESG more in our business case.”

ESG: A metric for doing business

“We believe that the investment community cares substantially about sustainability,” she continued. “It wants to be sure it’s investing in companies that are sustainable and operating through that ESG lens. Going forward, it’s increasing likely that ESG factors are going to be a metric for doing business.”

Whiting began putting sustainability-related data on its website in 2016 and, later that year, brought in a consulting firm “who formalized the process and provided a very robust reporting program.”

“Reducing flaring is a challenging issue for the industry and has been a significant focus for Whiting. The Williston [Basin] has grown at a pace that the midstream providers and the E&P sector itself didn’t anticipate,” said McNamee. “We became so efficient as an industry that everything just became more productive in the same timeframe.”

Whiting has been a leader in ongoing discussions aimed at reaching a consensus on how best the sector can reduce flaring and GHG emissions in North Dakota, according to McNamee.

“We really try to lead by example,” she said. “We will not sacrifice our environmental responsibility for production. That’s our promise, and we will follow it. If you look at publicly available data, you’ll see we’ve consistently satisfied the regulations and captured a higher proportion of our gas than industry. We view the ESG program as a means to focus awareness across the company on key nonfinancial metrics.”

McNamee acknowledged it may at times “seem counterintuitive to release data that the industry hasn’t done historically, and which may not cast the industry in the best light. However, it’s important to create a baseline and then to drive improvements year-over-year thereafter. The key to sustainability is to make improvements.”

Elsewhere, Whiting has had continued success in its long-standing leak detection and repair program. The company reported in 2018 a 90% reduction in issues discovered during inspections. In addition, it said it saw nearly a 200% improvement in the number of inspections that found no issue as well as a greater than 400% increase in the time between issues being detected on tank batteries.

On governance issues in ESG, the feedback from major shareholders is that governance remains a “significant component,” said McNamee. “If your governance is sound, and your board is engaged, it improves the function of your business. Governance provides the oversight.”

Return of obstetric services

On social issues, Whiting has had a solid history of engagement with local communities, according to McNamee. “We’ve always practiced community relations, but in a very proactive way,” she said. “When Whiting went into North Dakota, we hired local people, and the benefit of that is that they know those communities and care more about them than anyone else.”

An example of Whiting’s support is when in 2017 it joined with the McKenzie County Healthcare System in helping build a hospital wing to bring back obstetric services.

“The oil patch tends to be boom and bust, and over time, labor and delivery services had been eliminated,” she noted. “The majority of our labor force in the area is under the age of 40, and so it has affected our employees who are living there, working for us and having children. We really wanted to do something to make that opportunity available to them again.”

“Whiting partnered with the hospital to underwrite the labor and delivery wings, and this summer they will be able to deliver babies in Watford City again,” said McNamee. “Up until then, in winter, they had been driving hours to reach a hospital to deliver babies, sometimes delivering on the side of the road, or in someone’s home, instead of safely in a medical institution.”

“We thought Whiting’s ability to provide that service again would have a meaningful impact to the community and their wellbeing going forward.”

From niche to mainstream

“Momentum on ESG is definitely accelerating; it’s going from niche to mainstream,” observed Joanne Howard, vice president of sustainability and corporate communications at Crestwood Equity Partners LP. “The driver is multifaceted; it’s not just one thing. The investment community is the most important driver, but we’re also seeing pressure from a confluence of other stakeholders.”

As for the outlook, “I only see this continuing,” she added. “It’s just going to get bigger and bigger.”

Crestwood, based in Houston, is a midstream services provider operating in multiple areas of the U.S. The company’s more gas-oriented gathering and processing activities are in the Marcellus, Fayetteville and Barnett shale plays, while its more crude-oriented midstream assets are in the Bakken Shale, Powder River Basin and the Delaware side of the Permian Basin.

Crestwood is notable for its attention to ESG issues in that it is an MLP. Unlike a C corp, which at times can come under pressure applied by shareholder activity, investors in an MLP are unable to file a shareholder resolution. However, MLP investor demands have changed and are continuing to evolve.

“As generalist investors are entering our stock, they are increasingly demanding transparency on ESG,” said Howard. “Therefore, Crestwood is taking a proactive and strategic approach in navigating the rising tide of ESG.”

While environmental issues typically hold the headlines, social issues have also grown in importance in ESG for midstream companies, according to Howard.

“As infrastructure in the midstream sector is becoming more crucial to the energy sector, with midstream companies developing infrastructure across the U.S., pipelines are sometimes coming in close proximity to communities,” she noted. “So now, more than ever, it’s important to maintain your social license to operate when you’re working in these communities. Being able to have long-term community relations is vital.”

Also in the social field, “it is paramount to develop meaningful relationships founded in respect when working with indigenous communities,” said Howard. Crestwood has experience in this area through its operations on the Fort Berthold Indian Reservation in North Dakota, where the company has “tribal relations specialists who are themselves Native Americans and integral members of the community.”

Crestwood was one of the first midstream MLPs to issue a sustainability report in 2018 and to create a Sustainability Board Committee that oversees ESG issues. In addition to conducting a materiality assessment, in which it identified 12 material ESG topics for Crestwood, Howard went on to create a three-year sustainability strategy to further integrate sustainability into the company.

This involved selecting five key areas where the company “can really make some traction” and will seek to further advance each of the goals. The five components of the three-year plan were: supply chain management, ESG investor strategy and disclosure, environmental stewardship, diversity and inclusion, and social investment.

“People ask me if sustainability costs a lot of money, and it’s the wrong way to think about ESG,” commented Howard. “If you’re operating in a sustainability friendly way, you think of it more as a way of cost avoidance over the long term by doing the correct measures and responsible measures now.”

In Howard’s view, the energy sector has historically not played as strong a hand as it could in terms of winning over the public on issues relating to the many benefits that energy delivers.

“But I see the rise of sustainability reports as an impactful tool for the energy industry to tell its story and to demonstrate all the important and valuable things it is doing. It’s a call to action for everyone.”

Recommended Reading

Subsea Tieback Round-Up, 2026 and Beyond

2024-02-13 - The second in a two-part series, this report on subsea tiebacks looks at some of the projects around the world scheduled to come online in 2026 or later.

PGS Wins 3D Contract Offshore South Atlantic Margin

2024-04-08 - PGS said a Ramform Titan-class vessel is scheduled to commence mobilization in June.

2023-2025 Subsea Tieback Round-Up

2024-02-06 - Here's a look at subsea tieback projects across the globe. The first in a two-part series, this report highlights some of the subsea tiebacks scheduled to be online by 2025.

Sapura Acquires Exail Rovins’ Nano Inertial Navigation System

2024-02-01 - Exail Rovins’ Nano Inertial Navigation System is designed to enhance Sapura’s subsea installment capabilities.

TGS Commences Multiclient 3D Seismic Project Offshore Malaysia

2024-04-03 - TGS said the Ramform Sovereign survey vessel was dispatched to the Penyu Basin in March.