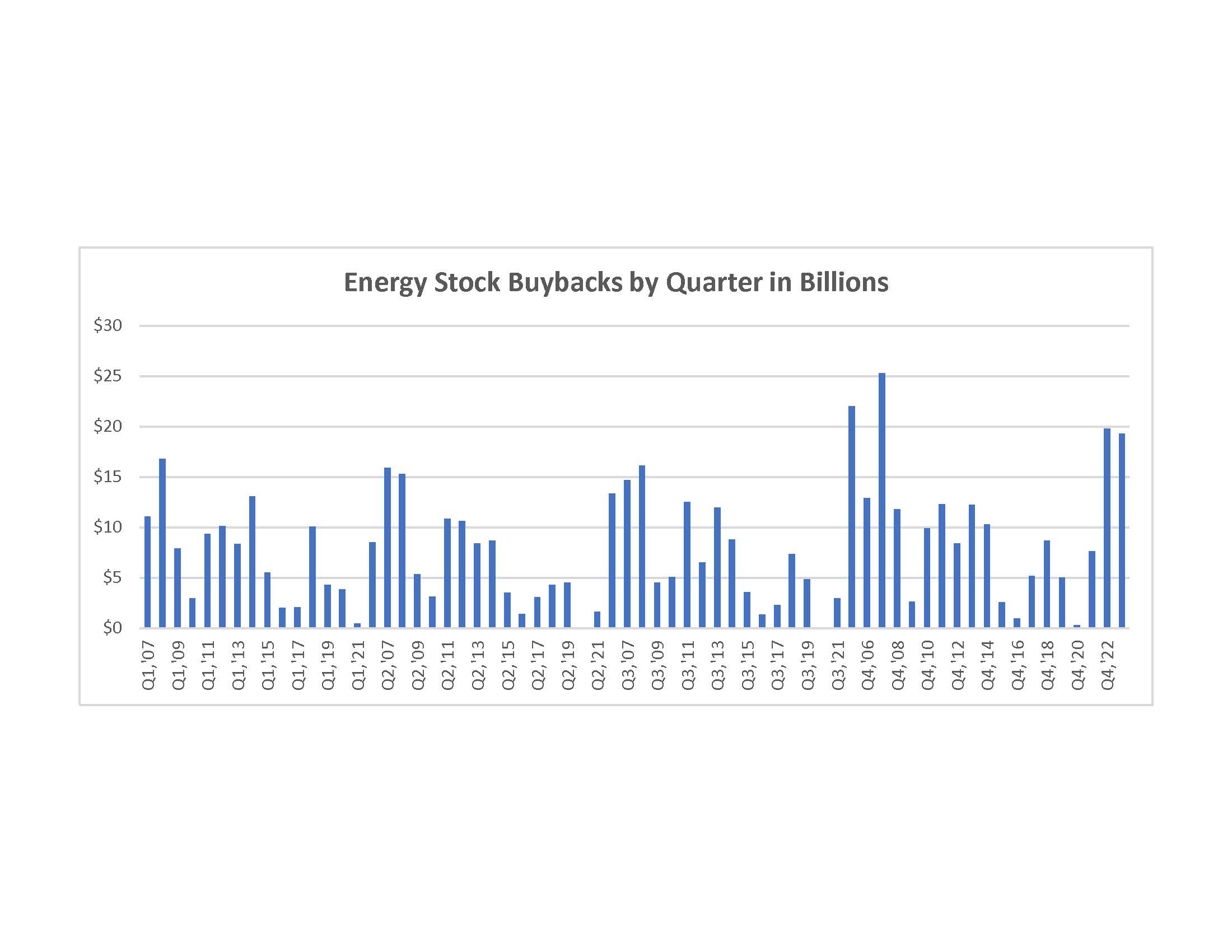

Despite fizzling oil and gas prices, E&Ps continue to push ahead with robust stock buyback plans that have the sector outperforming the commodity. The trend highlights oil and gas companies’ rigid adherence to capital returns as the industry continues to make its growth and capex overspend days a distant memory.

In the first quarter, large independents were aggressive in buying back stock and even upsizing repurchases. Devon Energy reported in early May that its board had approved a 50% increase in buybacks to $3 billion. The Oklahoma City-based company repurchased $692 million of its shares in the last year. Diamondback Energy, based in Midland, Texas, told its investors it is committed to returning at least 75% of its free cash flow to investors on a quarterly basis. The company repurchased $332 million worth of stock in first-quarter 2023. And Occidental repurchased $752 million of common stock, accounting for more than 25% of its $3 billion repurchase program.

Restoring investor confidence

Other industries, particularly tech, are also ramping up buybacks but experts said they are especially the right decision for the energy industry. The buybacks show investors the sector has learned its lesson from the recklessness of the “drill-baby-drill” era and that they are going to insulate investors for the industry’s boom and bust cycles, analysts said.

Subash Chandra, an equity research analyst at Benchmark, said investors would not believe the energy sector was more stable and responsible until the sector outperformed the commodity.

“We just passed that test resoundingly,” Chandra said. “Oil went from $120 to a low $68 … The correction in the stocks were just not as deep.”

He described oil and gas as a mature industry with few growth cycles ahead of it.

“We have to figure out how to sunset this thing profitably for everyone,” Chandra said.

David Deckelbaum, a managing director at TD Cowen, said energy companies’ implied payoff ratios are triple that of the average S&P 500 company.

“I think that the sustainability of those payouts is extremely long, five to 10 years, if not longer, because you're not really looking at capex changing year over year. Your asset base isn't really changing, and then over time especially if you're employing things like buybacks, you could end up retiring a decent portion of your market cap over time,” he said.

Mark Cieciura, head of corporate and venture services at Piper Sandler, pointed out that most companies that buy back their own shares outperform stocks that do not have high buyback yields.

“It’s the best use of cash on their balance sheet. It shows they have faith in their own company because they’re out buying themselves, they’re investing in themselves,” Cieciura said.

Another advantage: energy stocks are undervalued. With a large amount of cash on hand, E&Ps would be foolish not to buy them at low prices, said Xavier Tison, director of energy innovation at the Maguire Energy Institute at Southern Methodist University (SMU).

“Why would you not do that? To me, it seems like the very simple, logical way to go,” Tison said.

Tison’s colleague, Bruce Bullock, director of the Maguire Energy Institute, said companies that don’t repurchase their shares may leave themselves open to an activist investor making a run at them and replacing board members. He added that higher interest rates are making other investment opportunities attractive, and energy companies need to compete with that.

Buyback fallout

While most energy finance experts see buybacks as the right move for the energy sector, William Lazonick, professor emeritus of economics at the University of Massachusetts, said buybacks have always been a terrible idea and should be banned.

“They are done to manipulate the stock price. Nothing more, nothing less,” he said. “In my view, if they decide just to use it for buybacks, they’re basically saying there’s nothing better they can do with the money, and they’re not doing their job.”

Lazonick, who has crusaded for decades against stock buybacks with critical academic studies, said buybacks are self-serving because executive pay is tied to stock performance. He said dividends should be used to return capital to investors. That’s what they are for.

But SMU finance professor Don Shelly said dividends are unsustainable. Investors expect them to be paid every quarter – and to go up. GE paid dividends for decades, then shocked investors when its capital return model was no longer sustainable and had to abruptly halt, he said. Complaints about stock buybacks over dividends from some members of Congress need to be taken with a grain of salt, Shelly said.

“For some reason, the politicians in Washington have gotten this bee in their bonnet where they're saying, ‘Buybacks, bad. Dividends, good.’ It's kind of ridiculous because they're the same thing — they’re returning capital to shareholders,” he said.

One of those Washington critics sits in the White House. President Joe Biden lambasted buybacks in his February State of the Union address and singled out “Big Oil” for investing too little in domestic production.

“Corporations ought to do the right thing,” the president said. “That’s why I propose we quadruple the tax on corporate buybacks and encourage long-term investment.”

Buybacks are currently taxed at only 1%. Legislation by Democrats to quadruple that is stalled by Republican opposition. In early May, the Securities and Exchange Commission announced new regulations to make buybacks more transparent, and the move was quickly met with a lawsuit from U.S. Chamber of Commerce and several other business groups.

Recommended Reading

California Resources Corp., Aera Energy to Combine in $2.1B Merger

2024-02-07 - The announced combination between California Resources and Aera Energy comes one year after Exxon and Shell closed the sale of Aera to a German asset manager for $4 billion.

Equinor Brings Solar Plant Online in Brazil

2024-03-08 - Equinor says the Mendubim solar plant will produce 1.2 terawatt hours of power annually.

Select Water Solutions Bolts On Haynesville, Rockies Assets for $90MM

2024-01-31 - Select Water Solutions Inc. added disposal and recycling capacity in the Haynesville Shale and the Rockies across three acquisitions in January.

SCF Acquires Flowchem, Val-Tex and Sealweld

2024-03-04 - Flowchem, Val-Tex and Sealweld were formerly part of Entegris Inc.

Weyerhaeuser, Lapis Energy Enter Carbon Sequestration Exploration Pact

2024-02-29 - The exploration agreement covers 187,500 acres across three states with five potential carbon sequestration sites.