Presented by:

Editor’s note: This is the third in a four-part series Oil and Gas Investor is featuring with Kenan-Flagler Energy Center at the University of North Carolina (UNC) at Chapel Hill. Read parts one and two here. Part four will appear in the November issue.

On July 29, Exxon Mobil Corp. announced its second-quarter earnings, and as part of the investor webcast, it disclosed further information about plans to pursue carbon capture, utilization and sequestration (CCUS). These disclosures included signing a memorandum of understanding for a Scotland CCUS project and work on new materials to improve the capture efficiency of CCUS technologies.

There were some mildly positive responses to these disclosures along with dismissive assessments. Parsing the dismissive responses offers an opportunity to explore the potential for a more constructive climate discussion. This discussion will center on the activity on which Exxon Mobil has chosen to focus: CCUS as the second pathway in the climate strategy.

The dismissive critiques offer several strands, which can usefully be highlighted:

- Exxon Mobil’s CCUS strategy amounts to “greenwashing,” a defensive strategy to defend its continuing to producing hydrocarbons, the use of which the world needs to reduce or eliminate;

- Exxon Mobil’s CCUS is aimed at shifting the decarbonization focus to its customers, those who emit Scope 3 CO₂. This will allow the company to concentrate on and tout its Scope 1 reductions, those directly attributable to its own production processes; and

- CCUS is expensive and uncompetitive with wind/solar power and therefore a diversion of capital better spent installing offshore wind turbines or utility scale solar arrays.

A sense of these critiques comes from climate and energy reporter Tim McDonnell’s piece in the “Quartz Daily Brief”: “Ultimately, the only way for Exxon to eliminate its Scope 3 emissions is to stop producing oil and gas. That’s the direction some of its European peers are headed, as they look to become titans of renewable energy. Until Exxon gets on board, it will never be the climate beauty queen.”

“Change is needed if the next phase of the energy transition is to progress.”

As gratifying as this critique is to some, it underscores an emerging problem. Arguments used by the environmental community to advance its causes are reaching diminishing returns. Change is needed if the next phase of the energy transition is to progress. For this to happen, the environmental community must undergo its own transition, one that involves moving away from stopping things to deciding what to enable.

Decarbonizing challenges

The environmental community’s climate strategy is also hitting diminishing returns because it is limited to backing wholly inadequate means to accomplish stated goals. If the aim is to limit global emissions to levels consistent with a 1.5 degrees Celsius or 2 degrees Celsius temperature increase from pre-industrial levels, wind/solar plus battery storage and electric vehicles (EVs) will not accomplish the targeted decarbonization.

The problems with the “renewables can decarbonize” vision are legion. Huge sectors such as aviation and heavy transportation are not easily electrified and are unlikely to be transformed any time soon. Other sectors such as heavy industry cannot be electrified. Renewables costs will not continue to drop as they are pushed further into the grid. Intensifying intermittency backup and load-following issues will see them rise instead. Battery costs were expected to drop with large-scale manufacturing of EVs. Now that prospect is in jeopardy as manufacturers awaken to the challenge of sourcing more copper, lithium and nickel from mines in the Congo, Chile and Peru. Taking these material inputs into account, an honest life-cycle analysis also suggests that installing renewables is less decarbonizing than implied.

All of this makes the challenge of decarbonizing economically advanced nations much harder than the dominant narrative acknowledges, and the chances for decarbonizing developing countries are even more remote. Those lands are decades behind the U.S. and Europe, prioritize development for their populations and lack the capital formation and decarbonization options, which OECD countries enjoy. Yet, they make enticing locations for relocating heavy emitting industries driven abroad by the decarbonization push in Europe, Japan and the U.S.

So, the first and biggest transition needed is for the environmental community to admit that the energy transition cannot be renewables plus storage plus EVs. As Daniel Yergin recently put it in his book, “The New Map”: “At this time at least, wind and solar cannot go it alone. They need partners.”

To say it another way, the energy transition will have to be hybrid. It will require contributions from more than a few sources, or it won’t happen as we need it to happen.

Some influential members of the environmental community have begun to undertake this transition. A paper, “The Nuclear Dilemma,” published by the Union of Concerned Scientists, points in this direction. The paper argues that allowing the current U.S. nuclear fleet to retire would amount to spinning our wheels on decarbonization. The article then discussed the safety measures needed for nuclear plant life extensions.

More recently, Gina McCarthy, the current White House climate adviser and former head of the Natural Resources Defense Council, publicly called for current and new nuclear energy to be part of a clean energy standard (CES) sought by the Biden administration. McCarthy called for the CES to be “robust and inclusive” and added carbon capture to the elements to be included.

McCarthy’s call for an inclusive CES is to be welcomed. New nuclear and CCUS will need to be contributors to the hybrid energy transition. The next step would be environmental community recognition on why CCUS is more than just a mention item. It is, instead, the needed second pathway to decarbonization.

CCUS drivers

There are four main reasons why CCUS must be the second pathway:

- It will be the only way to decarbonize emissions from large stationary industrial sources;

- It will be the only way to decarbonize the natural gas electricity generation needed for grid integrity and stability;

- It will be needed to decarbonize developing economies that have fewer energy options, weaker electricity grids and large heavy industry sectors emitting greenhouse gases (GHG); and

- It addresses large economic costs not recognized in most clean power economics. These include the costs of storage, backup power and forcing the retirement of existing assets with considerable remaining economic life.

Let’s review these four points in more detail. Stationary sources account for approximately 50% of U.S. CO₂ emissions. In 2017, U.S. emissions from stationary sources amounted to 2.6 billion tons. These sources include iron and steel, cement and concrete, refining and chemical manufacturing, and pulp and paper. However, by far the biggest share, almost 70%, comes from the electricity sector.

Two problems are at work here. First, the nonelectricity sector is hard to decarbonize. All of this manufacturing is based upon continuous operations supported by reliable power. In many cases, massive amounts of heat are also employed. Intermittent electricity backed by short-duration storage cannot provide these essential operating conditions. This constitutes a formidable decarbonization challenge for cement, refining, etc., in the U.S.

That challenge is only greater in less developed countries. The fact that China and India, which are major outsource destinations for these types of industries, still continue to build coal plants only magnifies the chances that U.S. decarbonization based on wind/solar largely amounts to shipping CO₂ to high GHG emission locations. It is not a coincidence that China, at 30%, is now the leading source of CO₂ releases and twice the size of U.S. emissions.

The second CCUS driver addresses the reliability and resiliency of electricity grids. Considerable progress has been made on decarbonizing the U.S. electricity sector. In fact, most of the reductions in annual U.S. emissions have been accomplished in the power sector. However, the harder challenges lie ahead.

More wind/solar on the grid has provided experience as to what that means for grid reliability. The problem is not just that the wind doesn’t always blow or the sun doesn’t always shine. It is also that renewable power cannot be counted on to follow electricity demand when that load increases.

Battery storage, demand management and smarter grids have all been proposed as solutions. To date, all have shown serious limitations. Lithium ion batteries need to be recharged every two to four hours. That leaves them of little use in a major power outage or for storing surplus solar for tomorrow, next week or next winter.

Demand management depends upon consumer cooperation at scale. Overwhelmingly, customers expect the lights or air conditioner to go on when they want it. Smarter grids face many challenges, from the decentralized nature of the U.S. power sector to the fact that surplus power from adjoining markets cannot always be counted on, as California continues to encounter as it battles drought and wildfires.

Decarbonizing electricity

For all of these reasons, multiple utilities (Calpine Corp., Duke Energy Corp.) have issued studies affirming the need for natural gas to remain in the electricity generation stack.

Natural gas is uniquely able to load follow and can be used to meet peak or baseload demand. The latest natural gas combined cycle plants are highly efficient. These show power conversion ratios (heat rates) of 65% and capacity factors of 85% or better. These characteristics mean that for many utilities, substituting natural gas for coal is their current and near-future decarbonization strategy.

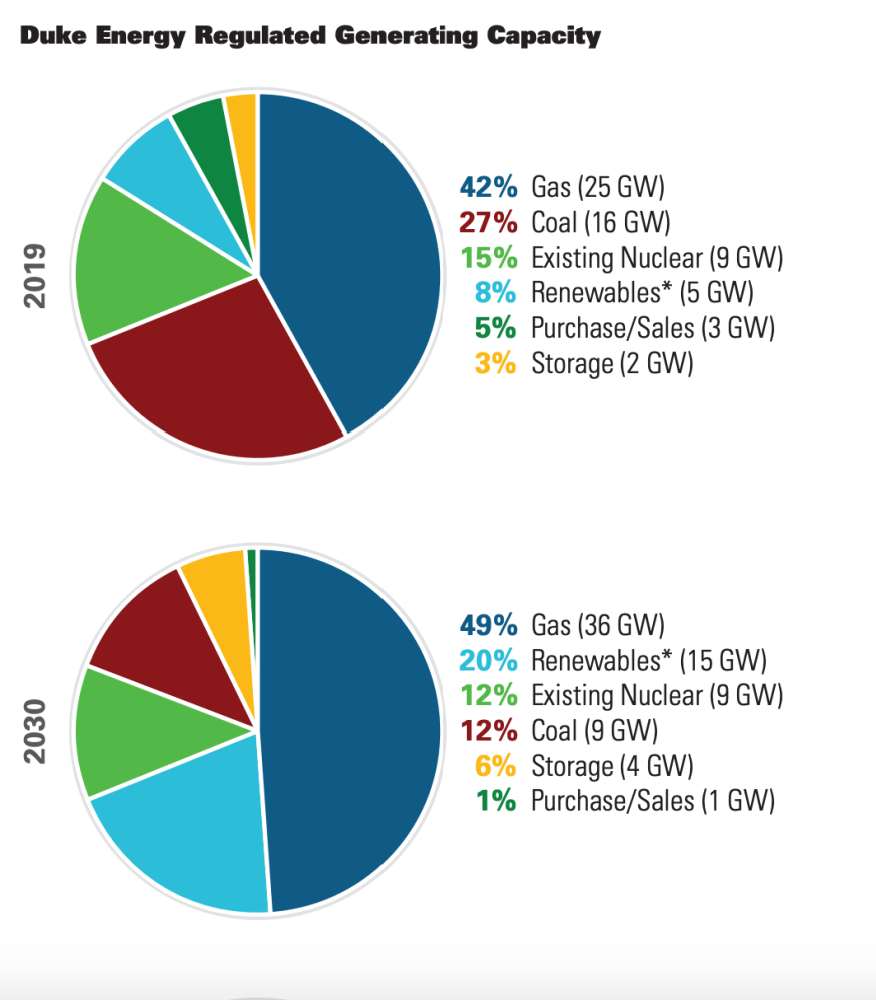

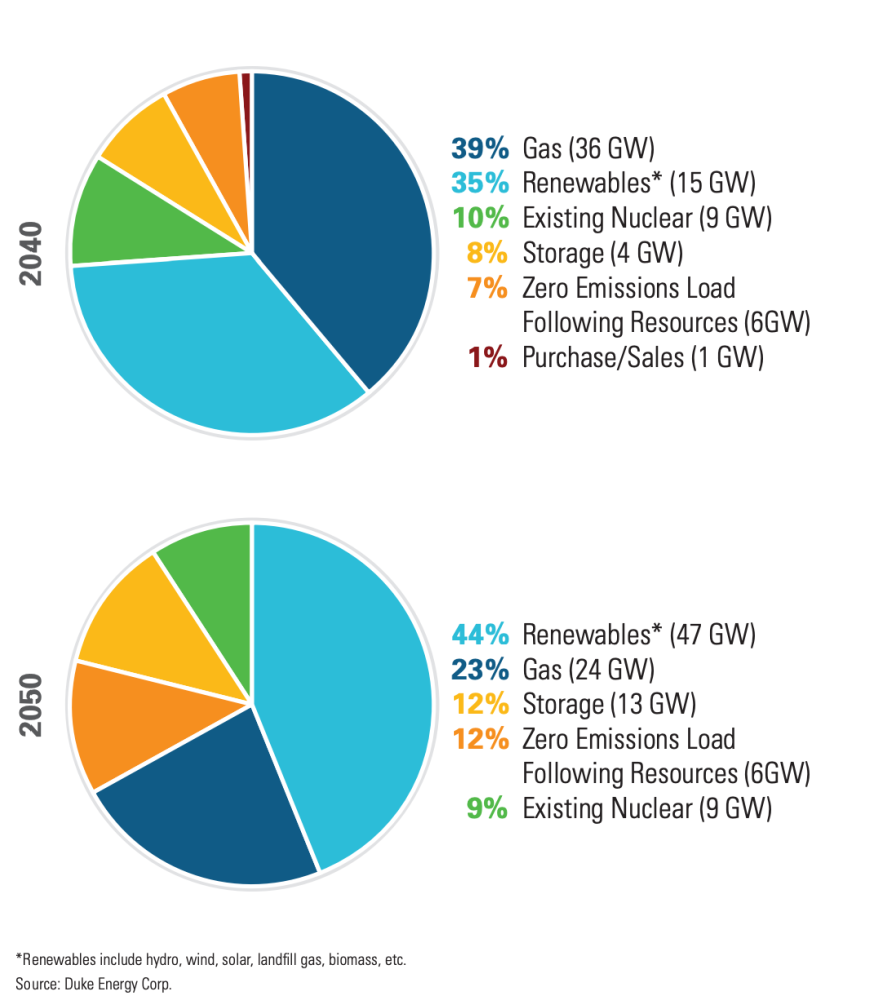

Today, Duke Energy has 25 gigawatts (GW) of natural gas power. The company’s 2030 plan envisions its presence rising to 36 GW as its coal capacity drops. More significantly, the plan foresees 24 GW of gas-fired capacity remaining in 2050. This doesn’t include additional gas capacity with carbon capture that would fill in its zero emissions load following resources (ZELFRs) gap.

Since all serious decarbonization plans start with decarbonizing electricity, the sector’s need for natural gas presents an ongoing challenge. How can utilities reconcile moving toward net-zero emissions while continuing to rely on natural gas for load following and backup? CCUS is the pathway that can reconcile these goals.

Failing to take this need for natural gas seriously will likely lead to events that can harden resistance to decarbonization efforts. An example is what happened in Texas during February 2021. This extreme cold weather event lasted seven to 10 days. Battery storage would not have helped in this crisis. Also wind and solar generation almost disappeared for days.

Finally, consider how natural gas responded to the large increase in load fostered by frigid temperatures. Much was made of the fact that, toward the end, even natural gas powered electricity was affected. Instead, consider what would have happened in this event if natural gas was no longer in the mix.

Reliability challenges such as this are more acute in most other countries. If electrification is the path to decarbonization, it has to be followed globally, not just in the U.S. or Europe. This reality is often ignored by climate activists who, when discussing means rather than goals, focus primarily on developed countries. Since, as the saying goes, the atmosphere is global, this brings up the question of how to decarbonize electricity in the developing world.

Developing countries such as China, Nigeria, South Africa and India face a more acute tradeoff between economic growth and decarbonization. With annual GDP growth targets as high as 6%-plus and large populations still living in poverty, these nations aspire to, and in many cases, achieve steep electricity load growth. They also face this challenge with less robust electricity grids than developed nations. These conditions leave them with little choice but to use dispatchable fossil fuels to meet rapidly rising power demands. In many cases, the fuel of choice is coal. While renewables are in the picture, these countries annually decide that rapid load growth cannot be met with intermittent power and short-term storage. For example, China continues to rely on coal for 60% of its total energy supply, and its new five year plan (2021 to 2025) reemphasizes its use. Given such facts, how will developing nations decarbonize in anything like the timetable climate activists assert to be essential?

Decarbonizing their existing and near-future power plants seems to be their best and perhaps only option. They are not going to dismantle their existing energy infrastructure and put their economies and populations at risk. This means global decarbonization is going to have to find a way to work with many electric generation assets that already exist. That pathway would see CCUS developed in the U.S. and Europe such that the capture technologies and project structures could then be exported to and assimilated by developing nations. Considering the way China and India have absorbed other developed world technologies, a maturing CCUS industry would find ready adoption in those lands.

“New nuclear and CCUS will need to be contributors to the hybrid energy transition.“

Finally, there is getting the costs of the energy transition tabulated correctly. CCUS has been criticized as an expensive option. A conclusion such as this can only be justified by continuing to propagate the flawed version of renewables economics that have surrounded their progress for over a decade. Properly evaluating CCUS versus more renewables requires a valid “apples to apples” comparison.

Wind and solar costs

Without question, wind and solar costs have declined rapidly during the past decade. Recent Energy Information Administration (EIA) figures put wind and solar unsubsidized levelized costs of electricity (LCOEs) in the 3 cent to 5 cent kilowatt-hour range. Many “renewables alone” advocates now cite these figures as proving that wind/solar are not only competitive with the most efficient combined cycle natural gas (CCNG) power plants but cheaper than either coal or nuclear power. However, look closely at the EIA’s tables and footnotes. They carefully distinguish between dispatchable and nondispatchable power with renewables being the latter. This means wind and solar LCOEs are tabulated for only when they are producing. The EIA is comparing wind and solar, with 30% to 40% capacity factors, to CCNG with an 87% capacity factor. What plugs the gap when wind/solar are not available? This means that the proper apples to apples comparison would be wind or solar plus storage versus CCNG, coal or nuclear.

Even this comparison fails to capture the extent to which wind and solar costs have been inaccurately assessed. Reported wind and solar LCOEs are further distorted by the following:

- They reflect the best wind and solar projects. Wind and solar are based on natural resources. Today’s projects are located in the best places. Check the maps and see wind projects in Oklahoma/Texas and solar in southern California, Arizona and other sun rich states. What are the costs of solar in Minnesota or wind in New Jersey? They are substantially higher, perhaps twice as expensive.

- Battery storage doesn’t fill the supply gap versus CCNG. Renewables plus battery storage economics still don’t address longer intermittency gaps such as the one visible in the Electric Reliability Council of Texas chart. This means the true costs of wind and solar versus CCNG would add a backup peaker natural gas plant to battery storage. Only then would a wind/solar-based system be able to equal the output supplied on demand by a CCNG plant. The alternative would be to massively overbuild both renewables and storage capacity, which would be hugely expensive.

- Wind/solar make existing plants run less efficiently and ultimately cause such plants to retire before the end of their economic lives. Because wind/solar can’t respond to load, fossil fuel plants must stand by and respond. At other times, wind/ solar generation is surplus to load, forcing other plants to curtail. In merchant markets, wind/solar’s zero marginal cost and tax subsidies allows them to always place their power on the grid by bidding next day prices down to zero. Fossil fuel and nuclear plants built to run in base load then run at lower usage levels. This forces some of these plants into a loss position and early retirement. Indeed, merchant power states such as Illinois are planning subsidies for nuclear plants threatened by shutdown.

In summary, a fair assessment of renewables costs would show a greater range of LCOEs to reflect regional disparities and then add battery storage, peaker backup and early retirement costs. These economics suggest that in many locations, especially those with access to EOR, CCNG with carbon capture will be competitive with or cheaper than renewables when allin costs are properly assessed.

The needed pathway

This brings us to the other side of the equation: If the case for CCUS as the necessary second pathway is strong and urgent, why has it not been unfolding? Here we must address the ambivalent posture of major oil companies. If the environmental community needs to undergo a transition on CCUS, so too must the major oil firms.

In the second article (see Oil and Gas Investor’s September 2021 issue), we talked about various reasons for major oil firm ambivalence on energy transition projects. This ambivalence has certainly been impacted by the intensifying pressure applied to those firms throughout 2021. Most are now signaling intentions to move forward with some CCUS projects. In most cases, final investment decisions still lie ahead. There is much going on behind the scenes. The industry continues to lobby for doubling the size of the 45Q tax credit.

The National Petroleum Council’s 2019 CCUS study essentially called for this to unlock project development. Technology selection is also to be determined, and research efforts are intensifying. While not quite “business as usual,” none of this conveys a serious industry sense of urgency.

What is missing here is a serious commitment to walk down the painful pathway of commercializing a new industry involving new technology. Long experience has oriented the industry to expect “first of a kind” projects to be expensive and economically disappointing. Looked at through the lens of “marginal economics,” many CCUS projects appear “out of the money.”

Here the industry would do well to factor defense of its existing asset base into its CCUS project economics. Either the industry learns to decarbonize its operations or those assets are going to face increasing regulatory and fiscal costs, possibly extinction. The industry also needs to pioneer CCUS so the electricity sector can follow suit, keeping natural gas in the generation mix. Yes, the first projects may be painful; however, the renewables industry has shown that perseverance will lead to declining costs and more viable project opportunities.

Major oil firms thus need to think in terms of seeing CCUS as a multi-decade program of walking down the experience curve. They will be taken seriously as transition contributors when they signal out loud their determination to progress on this path despite setbacks and disappointments with individual projects. For them and for the global economy, the payoff would be a big contribution to the affordable hybrid energy transition we need.

In the fourth and last article, we will look at the role of hydraulic fracturing in the energy transition and the case for driving CCUS forward on the basis of EOR.

Stephen Arbogast is the professor of the practice of finance and director of the Kenan-Flagler Energy Center at the University of North Carolina (UNC) at Chapel Hill.

Recommended Reading

Moda Midstream II Receives Financial Commitment for Next Round of Development

2024-03-20 - Kingwood, Texas-based Moda Midstream II announced on March 20 that it received an equity commitment from EnCap Flatrock Midstream.

Humble Midstream II, Quantum Capital Form Partnership for Infrastructure Projects

2024-01-30 - Humble Midstream II Partners and Quantum Capital Group’s partnership will promote a focus on energy transition infrastructure.

Mike Howard Joins Atlas Energy Solutions’ Board

2024-02-15 - Mike Howard brings more than 28 years of midstream energy experience to Atlas Energy Solutions’ board of directors.

Genesis Energy Declares Quarterly Dividend

2024-04-11 - Genesis Energy declared a quarterly distribution for the quarter ended March 31 for both common and preferred units.

Sunoco’s $7B Acquisition of NuStar Evades Further FTC Scrutiny

2024-04-09 - The waiting period under the Hart-Scott-Rodino Antitrust Improvements Act for Sunoco’s pending acquisition of NuStar Energy has expired, bringing the deal one step closer to completion.