After a strong, and in some cases record-breaking, opening quarter for earnings, the midstream sector continued expansion projects in the booming Permian Basin.

Otherwise, companies showed caution in a market with softening natural gas prices. In 2022, according to the U.S. Energy Information Administration, the Permian Basin reached an annual record high of 22 Bcf/d, 14% above the 2021 average.

High gas and crude production translate into high earnings for midstream companies, which earn fees from shipments.

Analysts said a substantial supply of cash does not automatically translate into capital spending but does allow companies to build where it is needed.

“… [The] relationship between good earnings and management teams focusing on building more infrastructure is not really one-to-one,” said Hinds Howard, a portfolio manager at CBRE Investment Management. “Midstream operators build new infrastructure based on utilization of their infrastructure being very high and their customers needing more capacity to process, transport or store hydrocarbons.”

As production in the Permian Basin continues to grow, midstream companies with a large footprint in the area will continue to meet the need to process and ship the product to the Gulf Coast, Howard said. America’s busiest oil and gas-producing region will remain the primary area of infrastructure development for now.

New plants continue to open in the region to meet the needs for capacity. Targa Resources plans to open six new natural gas plants in the basin, and Enterprise Products Partners is building two. On May 31, Enterprise also announced the completion of its Acadian Haynesville Extension natural gas pipeline in Texas and Louisiana, increasing its capacity to around 2.5 Bcf/d.

On the coast, Kinder Morgan announced on May 31 a plan to expand working gas storage capacity at the Markham, Texas, salt dome between Houston and Corpus Christi. The company will lease an additional cavern and add more than 6 Bcf of incremental working gas storage capacity and 650 MMcf/d of incremental withdrawal capacity on its Texas intrastate pipeline system.

‘Temporary glut’

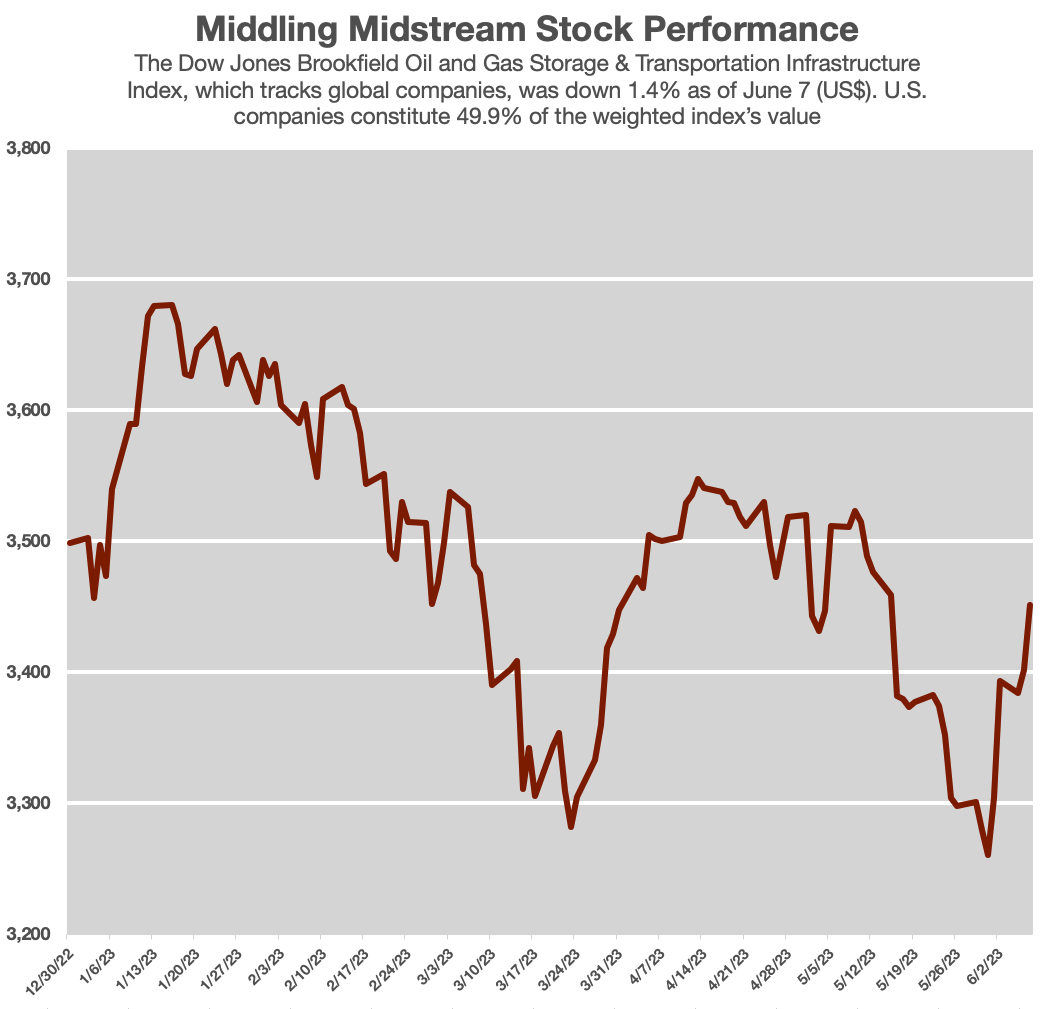

However, the high natural gas production numbers have not translated into a surge in stock prices for midstream companies. As the increase in supply over the past year has led to a collapse in gas prices, investors have been holding down the price of midstream stocks because they expect production to tail off in response in the coming months. On June 7, the benchmark Henry Hub natural gas spot price had fallen to $1.95/MMBtu from a high of $9.43/MMBtu one year ago.

The expectation is for an eventual slowdown in natural gas production, though not immediately in the Permian.

“A mismatch between natural gas supply and demand growth in 2023 is likely to create a temporary glut of gas supply, which we believe will continue to pressure natural gas prices,” Wells Fargo reported in its Midstream Monthly Outlook for June. The company expected production to slow primarily in the Haynesville and Midcontinent areas generally.

As any production cuts eventually affect midstream earnings, stock prices over the first quarter reflected the marketplace’s caution in the gas market.

In the first quarter, the stocks of midstream companies with a heavier stake in natural gas infrastructure did not perform as well as those emphasizing oil transport. Enterprise, Cheniere Energy and Energy Transfer all posted stock price gains of over 5%. Magellan Midstream gained 8% on its stock price in the first quarter, rising to $55.41. (After the announcement of its acquisition by ONEOK in mid-May, the price had hit $62.51 by June 7.)

Equity repurchases slow

Meanwhile, natural gas-heavy Targa, Enbridge and Kinder Morgan saw their stock prices drop slightly. Several investors saw ONEOK’s purchase of Magellan as a move into oil.

“Most of the (gathering and processing) players highlighted continued activity by crude-focused (exploration and production) in the liquid basins despite recent softness in oil prices, as the current price range still allows economic drilling. For gas, some curtailment in activity is expected in the dry gas basins, and midstream players are hoping for some firming up in gas prices for activity levels to resume,” Seaport Research said.

While commodity prices fell, the strong demand for their services has generally allowed infrastructure companies to keep sharing solid-to-excellent earnings with their investors, though equity repurchases slowed in the year’s first quarter.

About three-quarters of the Alerian Midstream Energy Index (AMNA) companies had buyback authorizations in place at the end of May. Led by Cheniere, eight of those companies spent a combined $780 million on buybacks in the first quarter, according to industry analyst VettaFi. At $450 million, Cheniere outspent all others combined, while Kinder Morgan spent $113 million.

The purchases showed a steady, if slowing, rate of equity purchases in the market. Over the three prior quarters, buyback expenditures had averaged $1.4 billion with the same companies.

The slowdown showed that, while buybacks will continue to be essential to returning money to investors, companies with a more opportunistic approach will be less active, VettaFi said.

Projects’ progress

Companies with large stakes outside of the Permian otherwise moved to shore up their share of the marketplace or move important projects forward.

Enbridge currently moves the majority of Canadian crude through the U.S., and at the start of June, the company began slashing its shipment rates in anticipation of new competition coming online next year.

The long-delayed and embattled Trans Mountain Pipeline received $2.25 billion in loan guarantees at the end of May from the Canadian government, which owns the line. Once open, the project will move an additional 590,000 bbl/d of crude from Alberta to the coast of British Columbia.

Enbridge will implement a rate cut in July of about 12%, to $28.80/cu. m, to move oil from its Hardisty, Alberta, hub along its Mainline to Flanagan, Ill., Enbridge reported in a regulatory filing. Enbridge officials said the move was a way to shore up its customer base well before the opening of the Trans Mountain project, which has been hit with cost overruns and has been a political football for the Canadian government.

In the U.S., Energy Transfer moved forward with a government appeal to the Department of Energy. The company’s Lake Charles, La., LNG project ran into difficulties in April, when the DOE refused to grant an extension to start exporting beyond 2025.

The government said Lake Charles LNG had not shown good cause for “an unprecedented second extension” beyond 2025.

However, according to Citi, Energy Transfer made a “strong appeal” on June 7, which put the company on a 30-day “positive catalyst watch.”

In its appeal, Energy Transfer outlined that it had already spent $350 million on the project and expected to sign an engineering, procurement and construction contract by July.

Also in June, Williams Cos. CEO Alan Armstrong said the first phase of the expansion of the Regional Energy Access pipeline would be complete in the fourth quarter. The expansion will provide an addition 830 MMcf/d to customers in New Jersey, Pennsylvania and Maryland. The second phase of the $1 billion project is scheduled to enter service in late 2024.

Another Williams project, the Louisiana Energy Gateway pipeline is on track for completion in fourth-quarter 2024. The 1.8 Bcf/d project will connect Haynesville Shale producers to LNG facilities on the Gulf Coast.

Overall, midstream companies continued with a cautious approach. The demand for infrastructure remains high and natural gas continues to have high demand overseas, but the high production rates of natural gas are expected to drop, following the trend in prices.

“… The lower commodity prices we’ve experienced this year will have midstream operators being cautious when it comes to their outlook for pipeline volumes and for new project developments that depend on growing volumes,” Howard said. “Midstream companies have been much more disciplined when it comes to deploying capital lately and I would expect them to stay disciplined in light of weaker commodity prices.”

Recommended Reading

Report: Freeport LNG Hits Sixth Day of Dwindling Gas Consumption

2024-04-17 - With Freeport LNG operating at a fraction of its full capacity, natural gas futures have fallen following a short rally the week before.

Permian NatGas Hits 15-month Low as Negative Prices Linger

2024-04-16 - Prices at the Waha Hub in West Texas closed at negative $2.99/MMBtu on April 15, its lowest since December 2022.

BP Starts Oil Production at New Offshore Platform in Azerbaijan

2024-04-16 - Azeri Central East offshore platform is the seventh oil platform installed in the Azeri-Chirag-Gunashli field in the Caspian Sea.

US Could Release More SPR Oil to Keep Gas Prices Low, Senior White House Adviser Says

2024-04-16 - White House senior adviser John Podesta stopped short of saying there would be a release from the Strategic Petroleum Reserve any time soon at an industry conference on April 16.

Core Scientific to Expand its Texas Bitcoin Mining Center

2024-04-16 - Core Scientific said its Denton, Texas, data center currently operates 125 megawatts of bitcoin mining with total contracted power of approximately 300 MW.