(Illustration by Robert D. Avila)

[Editor's note: A version of this story appears in the December 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

If you were happy to have 2019 almost in the rearview mirror, don’t let your “lead foot” begin to press on the pedal in anticipation of a smooth ride in 2020. It’s time to downshift, moderate your speed and try to avoid the many potholes you may encounter on the way. The good news is that the danger signs are already well-posted. And perhaps not all the predicted perils will prove to be true.

Simply put, E&Ps are being advised to plan for the worst and hope for the best, according to some analysts.

The number of variables on the horizon seems to be mounting by the minute. Of course, the supply/demand balance is of foremost concern, and here the start-up of several key offshore projects—notably in Norway and Brazil—has compounded projected growth in Lower 48 production and added newfound momentum to supply. This has many analysts projecting risk to crude prices in 2020.

Elsewhere, the range of issues is wide. Public capital markets are largely shut, and there is uncertainty around redeterminations on reserve-based loans from commercial banks. Mergers, in theory a source of optimism, seem to leave stocks tying the knot suffocated by negative market sentiment. As one observer said, investors are now prone to “default to pessimism” upon M&A announcements.

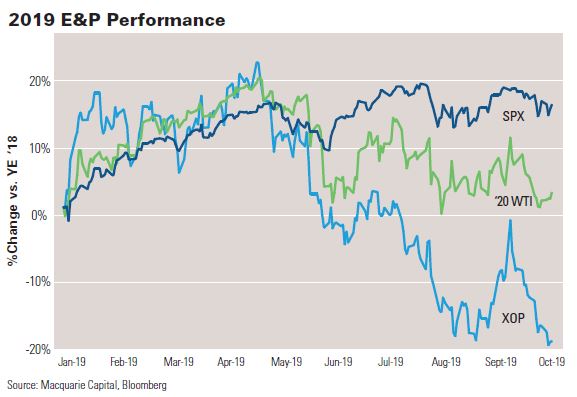

Regaining relevance—a relevance beyond energy’s recent meager weighting of about 4.5% in the S&P 500 Index—is also on the table. Investors are adamant that free cash flow (FCF) is the key metric they want to see from E&Ps. If rising to levels competitive with the broader market, FCF is seen as the lure that attracts the generalist investor who otherwise says, “Why bother?” with a 4.5% energy position.

A shadow over energy

Adding to all this is the issue of electoral uncertainty. Almost a year away, the election has already cast a shadow over the energy sector, as some Democratic candidates this year have called for a hydraulic fracturing ban. This has caused some investors to project its possible implementation on federal lands in several states, with a particular focus on New Mexico, zeroing in on Eddy and Lea counties.

A comparison of global supply/demand estimates by three agencies—the International Energy Agency (IEA), the Energy Information Administration (EIA) and OPEC— showed the market to be oversupplied in 2020 in all three cases. The lowest margin of surplus was roughly 200,000 barrels per day (bbl/d) (OPEC estimate, holding its output flat at August level), while the largest was an IEA estimate of 800,000 bbl/d.

As an example, the EIA in early October forecast global supply at 102.4 MMbbl/d in 2020, up 1.64 MMbbl/d year-over-year, spurred by U.S. production growth of 1.58 MMbbl/d and more than offsetting a decline in OPEC volumes. Global demand is projected to rise to 102.1 MMbbl/d, up 1.31 MM-bbl/d year-over-year, driven largely by growth in non-OECD economies.

“At $50 to $55/bbl, most of the industry is doing okay; they’re surviving, not thriving. But below $50/bbl, a lot of business models really start to have pretty significant issues.”

—Matt Portillo, Tudor, Pickering, Holt & Co.

But several research firms have been quick to say global demand estimates are too optimistic, pointing to a slowdown in global growth and negative-leaning economic indicators in key countries. At the same time, as the freezing up of public capital markets forces capital discipline on U.S. producers, analysts have taken an axe to their estimates of U.S. E&P capex and, in turn, projections of growth for 2020.

Tudor, Pickering, Holt & Co. (TPH) is among the earliest to ring an alarm bell on the risk of rising U.S. and international production overwhelming a faltering outlook for demand. TPH forecasts an average price for West Texas Intermediate (WTI) in 2020 of $45 to $50/bbl, a range that will significantly slow U.S. production growth, according to Matt Portillo, managing director of E&P research for TPH.

The reality is that “another year of U.S. growth is just not needed in 2020,” said Portillo. Growth in U.S. “black oil” vs. NGL was about 1.6 MMbbl/d in 2018 and is expected to be around 1.1 MMbbl/d in 2019. For 2020, at a WTI price of $50/bbl, black oil growth is projected to slow down to 650,000 bbl/d; and at $45/bbl, it would go “ex-growth” (i.e. zero growth), he predicted.

A confluence of new projects

A confluence of several major offshore oil projects starting up is a major factor in the outlook for 2020.

“There are three key areas we’re watching that are likely to affect crude prices in 2020, and this is one of the reasons why we believe there’s further downside risk to the forward commodity curve,” observed Portillo. These involve projects in Norway, Brazil and Guyana, he said, whose combined new capacity is expected to “far outpace” projected demand growth of 750,000 bbl/d for black oil in 2020.

“another year of

U.S. growth is

just not needed

in 2020,” said

Matt Portillo,

managing

director, E&P

research, for TPH.

One of the projects, the initial phase of the Johan Sverdrup project in Norway, started up in October. It is designed to ramp up from 200,000 bbl/d to 440,000 bbl/d over the summer. The crude market likely has priced in “part of, but not all” of the new production, said Portillo. “We’ll have to monitor the field to see how it ramps up to full volumes. There’s often a variance in performance with offshore projects.”

In Brazil, a real surprise to the upside has come from the energy sector’s ability to “kick into high gear in terms of growing production,” according to Portillo. “In the last two months it’s added about 430,000 bbl/d of oil production from a number of pre-salt fields. And in the next quarter or two, on a risked basis, we think there’s another 150,000 bbl/d of crude production that is likely to come on from facilities just getting to average projected utilization rates.”

After underperforming expectations regularly in the past, the recent track record in Brazil “has been a huge aberration from the trends we’ve seen of late,” he commented. “Brazil is coming on just as the market doesn’t need the incremental growth in oil supply.”

The final project is the Liza project in Guyana, which is expected to start up in late first quarter/early second quarter with a first phase capacity of 120,000 bbl/d. In total, noted Portillo, “we foresee up to 1 MMbbl/d of production coming onstream from those three key areas over the next six months on an unrisked basis. This eclipses our entire black oil demand forecast of some 750,000 bbl/d in 2020.”

In addition to black oil demand of 750,000 bbl/d, TPH forecasts about 500,000 bbl/d of demand for NGL, for total liquids demand of 1.25 MMbbl/d day in 2020. But with up to 1 MMbbl/d of demand already met by offshore projects, this leaves little room for growth in U.S. NGL supply, “until you get past some of these bigger projects and get into the latter part of 2020 and beyond,” said Portillo.

valuations down,

and crude prices

around $55/

bbl, free-cashflow yields are

pretty stout,” said

Marshall Adkins,

head of energy

investment

banking at

Raymond James

& Associates.

A silver lining?

If there is a silver lining to be found, according to Portillo, it’s that “2021 is not set to repeat this huge ramp in non-OPEC volume growth,” he commented.

Importantly, these supply factors are viewed as approaching an inflection point where a material slowdown in the deployment of drilling and completion capital is expected to occur in 2020, according to Portillo. For example, if WTI prices drop to $50/bbl, capex cuts on the order of 12% from last year’s levels of drilling would follow, he predicted.

“At $55 to $60/bbl, everyone’s business looks great,” observed Portillo. “And at $50 to $55/bbl, most of the industry is doing okay; they’re surviving, not thriving. But below $50/bbl, a lot of business models really start to have pretty significant issues. We expect 2020 capex to fall 12% at a $50/bbl price deck. That’s for our research coverage, which accounts for about 63% of U.S. oil production.”

If private operators are included, the decline in capex is likely to widen to closer to 15%,” he added.

A host of headwinds

What are the likely ramifications of lower commodity prices and markedly softer market conditions?

Portillo doesn’t hesitate in previewing the host of headwinds the industry may face.

“The punch line is that the industry is getting hit from every side: No access to equity, the high-yield market seizing up, the credit market is tightening its standards and lowering its price decks materially; a lot of commercial banks’ oily decks are being set at $46 to $48/bbl for WTI and at $2.10 to $2.20 per thousand cubic feet (Mcf) for natural gas. And that’s going to ultimately force the industry to live within its means.”

The fallout from the narrower netbacks earned in a lower commodity environment is that E&Ps will be facing “tightening credit and a lack of liquidity,” continued Portillo. As for public capital markets, “the equity market is all but frozen, and there’s little to no access to the high-yield market for most E&Ps that have over 2.5x debt/EBITDA leverage at this point.”

With the high-yield market having “seized up,” he continued, “as debt starts to come due, most of these operators don’t generate enough FCF to pay off the principal. They can make the interest payments on the debt, but they don’t really have a game plan to pay off the principal. And that is going to cause further and further distress in the high-yield market for energy.”

The unsettled outlook for energy is reflected in levels at which some high yield energy bonds are trading, noted Portillo. “A lot of the bonds are trading at bigger and bigger discounts to par. Some of the debt has traded down to 10% to 15% yield-to-maturities, which is usually a more distressed level versus some of the higher quality upstream names still able to access the debt market at a 4% to 5% yield.”

What’s happening at the commercial banks is “probably the most important factor for private operators” in the energy sector in 2019, according to Portillo.

Tightening loan standards

“The lending market is really beginning to tighten its standards for loans in RBL [reserve-based loan] facilities,” he said, “and the banks are lowering their price decks. Ultimately, that’s going to reduce the PUDs [proved undeveloped reserves] that banks are willing to lend against, so they won’t get credit for that in their facilities. And you’ll start to see the amount they’re willing to lend against PDP [proved developed production] also decline due to the lower price decks.”

In terms of prospects for further M&A, Portillo outlined two likely paths.

One path would involve industry consolidation among mainly private operators to gain scale, ultimately creating “super privates,” while another would involve a “significant number of mergers of equals,” according to Portillo. “What investors want to see are equity-for-equity swaps, where there are tangible synergies to reduce overhead and the potential for improvements to company balance sheets.”

Portillo foresees 2020 as being “a big year for industry consolidation.” But, he cautioned, it’s also going to be “a big year for industry distress, which may actually create further opportunities to consolidate assets, particularly if E&Ps are overlevered and are forced into a situation of having to sell themselves.”

Marshall Adkins, who heads up energy investment banking at Raymond James & Associates, offered a markedly more upbeat view of prospects for 2020, citing reasons why U.S production growth is moderating from the rapid levels of prior years and why crude prices may not only stabilize, but move higher.

Factors cited by Adkins, until recently the director of energy research at Raymond James, include: a meaningful slowing in well productivity gains in the U.S.; much lower than consensus growth in 2020 U.S. oil production; and expected drawdowns in global oil inventories over the next 18 months—all of which is expected to combine to drive crude prices significantly above the commodity curve.

From a commodity perspective, the bottom line is that the Raymond James price deck calls for WTI and Brent to average $70/bbl and $75/bbl, respectively, in 2020, some 30% to 40% above the commodity curve. For producers, a more moderate pace of growth coupled with higher crude prices may result in more FCF for some E&Ps, allowing them to make returns to investors as their output grows.

“With equity valuations down, and crude prices around $55/bbl, FCF yields are pretty stout,” said Adkins. “Producers are doing all the right things. They’ve slowed their drilling plans modestly due to slowing well productivity. Companies are buying back their stock. They’re giving cash back to their shareholders. We’ve never seen that in the E&P world.”

To be clear, the new Raymond James price deck is down substantially from its earlier deck ($92.50/bbl for WTI and $100/bbl for Brent). However, Adkins is no less bullish than before, attributing the lower deck to concerns over oil demand and poor sentiment. These are “so bearish that the overwhelmingly bullish supply side of the equation is essentially being ignored,” he commented.

Productivity gains slowing

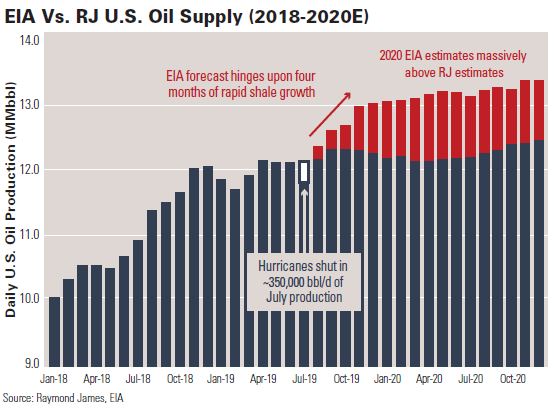

What does he think could help alleviate concerns over loose supply/demand balances in 2020? U.S. well productivity has been on an upward trend, averaging over 30% per annum, for this first half of this decade, but productivity gains have slowed sharply of late. For example, in the first half of 2019, EIA data show IP-30 rates to have risen just 2% vs. initial expectations by Raymond James of 10%. They may “even go negative,” commented Adkins.

A slowing pace of well productivity gains is attributed to several factors and has severe implications for future U.S. growth. Driving the productivity slowdown are stagnating lateral lengths, sand volumes and frack stages; parent-child spacing issues; and accessing “lower-quality acreage” ahead of expectations due to the need to adopt wider spacing to avoid parent-child interference.

If well productivity levels “flatline” going forward, “we see far below consensus 2020 U.S. supply growth even at our well-above consensus oil price expectations and activity assumptions,” said Raymond James. “More importantly, if the oil price strip stays near $50/bbl, U.S. oil supply growth will essentially be nonexistent over the next five years. This is way below consensus expectations.”

The relative tightness or slackness of oil markets going into 2020 will also reflect activity levels in the second half of 2019, when investors have emphasized capital discipline and not outspending cash flow. The sector had some 20% fewer active land rigs running on a year-to-date basis through the third quarter. (Exceptions to the trend included Exxon Mobil Corp. and Chevron Corp.)

producers “with

the optimal free

cash flow and

cash-per-share

growth metrics

are going to be

the winners,” said

Shawn Reynolds,

portfolio manager

at Van Eck

Associates Corp.

For 2020, the Raymond James forecast calls for U.S. production growth of only 300,000 bbl/d. Described as “meager,” the tepid growth figure is tacked on to projected growth of just 60,000 bbl/d for the final five months of 2019. By contrast, the EIA model similarly projects 300,000 bbl/d of 2020 growth, but this follows an increase of as much as 700,000 bbl/d in the same five-month period of 2019.

“If E&Ps can stick to their discipline and deliver a FCF yield, I think there is significant fundamental upside to the group.”

—Shawn Reynolds, Van Eck Associates Corp.

Math changes ‘dramatically’

Given an assumption by the EIA of a much higher production base at the end of 2019, the math going into 2020 changes “dramatically,” noted Raymond James. “On a full-year basis, this difference between our forecast and the EIA’s forecast equates to nearly 1% of global supply.”

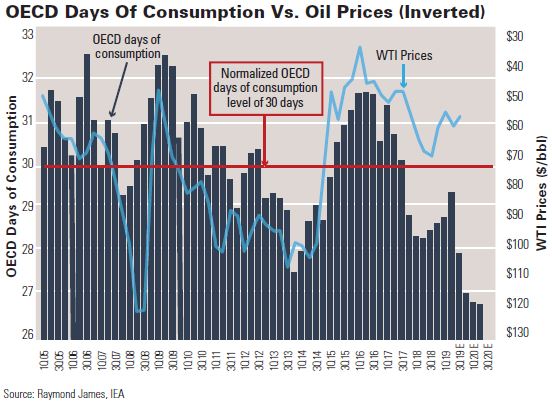

In terms of global oil supplies, the drone attack on Saudi Arabia’s Abqaiq stabilization facilities and the Khurais oil field is expected to have a more lasting effect—measured in months vs. days—than that conveyed in initial official announcements. An early Raymond James estimate estimated the disruption would result in a production shortfall of about 150 MMbbl (1.5 MMbbl/d for about 100 days).

As measured by days of OECD consumption, the norm for global inventories is about 30 days, while the attack on Saudi operations is expected to accelerate an inventory drawdown toward an unprecedented 25 days. However, historical patterns show crude prices tend to rise ahead of a drop to such a low level of days of consumption—a major reason that Raymond James sees support for higher crude prices.

According to Adkins, the disruption resulting from the attack on the Saudi infrastructure could effectively reverse part of the impact of an anomalous drop in second-quarter 2019 demand for oil. The drop in crude and product demand was precipitated by a number of factors, including the spring flooding of farmland in the Midwest and the drawdown of petrochemical inventories in China.

If demand in the second quarter of 2019 was pushed back by six months, “the Saudi attack may bring it back by six months” or so into early 2020, observed Adkins.

Of course, only time will tell. But if confirmed, a tightening commodity backdrop will be a welcome sign for a sector already headed in the right direction, according to Adkins.

“The opportunities are clear,” he said. “The sector is now return-focused. There’s a clear path on the E&P side to generate real FCF yield, to generate real return of capital to investors on top of growth. You get both growth and return of capital, which this industry hasn’t seen in my lifetime. That is a major structural shift.”

Shawn Reynolds, portfolio manager with Van Eck Associates Corp., pointed to four areas of uncertainty—two more macro in nature, and two more operational—that may be clouding the outlook for 2020.

The two macro issues involve OPEC and the U.S. elections. For OPEC, the question centers on the extent to which excess capacity of certain key member countries represents an overhang on the market. As regards the U.S. elections in late 2020, this issue is straightforward: Wouldn’t it make sense to see the elections play out before investing in the energy space?

On the operations side, one issue at hand centers on the sustainability of an E&P strategy to deliver returns to investors. Another focuses on the pace of productivity gains in energy. Some observers seem to automatically assume well productivity is dropping in absolute terms, when in fact the pace of gains may be slowing, but still “going up and to the right,” he said.

Sustainable free cash flow

“I believe the shale model works,” said Reynolds, responding to the latter issues where E&Ps have a degree of control. “In my view, it’s proven that it works. There are E&Ps that are generating FCF today. And once they can prove that to a broader group of investors, those investors are going to come back and start investing in E&Ps that can deliver FCF sustainably. And that’s a huge group of new investors.”

Over time, the energy sector should be viewed—and valued—in line with the industrial sector, according to Reynolds.

“If E&Ps can stick to their discipline and deliver a FCF yield, I think there is significant fundamental upside to the group,” he argued. “You’re going to start seeing E&Ps that can achieve those goals being valued more in line with an industrial company, where investors place a much higher multiple on the FCF yield than they do on the growth component.”

Ultimately, those producers “with the optimal FCF and cash-per-share growth metrics are going to be the winners,” he continued. “And once it’s been shown to be sustainable, potential investors that are on the sidelines are going to gravitate to those names. But instead of investing in a large number of names, that dry powder is likely to be invested in a narrower group of, say, 10 to 12 names.”

For the energy sector to be competitive with the broader S&P 500, it needs to generate a FCF yield on the order of 4% to 5%, but not the growth rate it historically has targeted, said Reynolds.

Taking growth rates down

“That’s one thing E&P managements still need to recognize. They may generate 4% to 5% FCF yield, but still think they need to grow at 10% to 15%. That’s not the case,” he said. “They need to take the growth rate down to 4% to 5% and generate a higher FCF yield. As I said earlier, the yield for the industrial sector is capitalized at a much higher multiple than the 2% to 3% growth rate that the industrials deliver. And 3% to 4% growth rate on a large industrial company is a big deal.”

On potential M&A activity, “I would hope there will be more M&A,” commented Reynolds. “It makes long-term strategic sense to have combinations and to create companies with scale: first, from an operational perspective, and second, from a financial perspective. Anyone involved in this industry knows that scale matters. Scale even matters in the exploration world.”

As for 2020 elections, in the event of a Democratic party win, “one of the big winners would be the Appalachian gas guys,” said Reynolds. A ban on fracking on federal lands, coupled with a possible tightening of flaring rules under the Clean Air Act, could have an impact on fedeal lands in several states, including New Mexico, as well as on associated gas production at large.

“You’d see a huge pushback” in a number of states, including Texas, Oklahoma, North Dakota and others, he predicted, but any moves that would end up restricting gas-oriented drilling or associated gas production would be “a positive for the Appalachian gas guys.”

A ‘singular focus’

The theme of FCF is one that has been integral to the E&P research at Macquarie Capital (USA) Inc. for some years, but not until recently has the point been driven home quite so emphatically.

“Free Cash Flow Yield is the Singular Focus” read the headline of a recent Macquarie report. The authors went on to say that while investor focus previously emphasized a combination of FCF and per-share production growth, this has now been “replaced with a nearly solitary focus on FCF yield.” What’s more, investors are “keenly looking for ways to verify compliance with the FCF mantra.”

Why focus solely on FCF? And what happened to such metrics as EV/EBITDA or NAV (net asset value)?

“For lack of a better term, it’s the metric of last resort,” said Paul Grigel, CFA, formerly with Macquarie. “What we mean by that is that other metrics vary depending on a host of underlying assumptions. A NAV metric for an E&P depends on its rig count, how much it grows, what commodity prices are, etc. There is a multitude of assumptions going into it, as is similarly the case with EV/EBITDA.”

number of

management

incentives, FCF

continues to be

of “paramount

importance

to generalist

investors,”

according to

Paul Grigel, CFA,

formerly with

Macquarie Capital

(USA) Inc.

By contrast, using FCF as a metric offers a degree of certainty needed by a sector deeply out of favor.

“We have to go back to basics,” said Grigel. “Any sector that is viewed as having destroyed a large amount of capital has to prove it can create value, and that’s what this does. If an E&P is able to hold production flat year-over-year and—all other things being equal—generate a certain amount of operating FCF, then a generalist investor can say the E&P created value.”

While this may represent a going concern in its simplest form, if an E&P can go to generalist investors and put FCF numbers on the table and prove that it has created value, “they can’t ignore you,” he said. “That’s what generalist investors are looking at. They still may not want to invest with you. But at the very least, the main point where you’re under attack goes away.”

‘Verifiable outcome’

Macquarie’s energy team has been recognized for its role in examining management incentives at E&Ps.

As one of a number of such incentives, FCF continues to be of “paramount importance to generalist investors,” according to Grigel. “It absolutely ties management compensation to the verifiable outcome of FCF,” he noted. “And once you’ve put it in there, and the market has seen that focus, it becomes very sticky in terms of a metric. It becomes very difficult to remove or alter that metric.”

The commodity team at Macquarie currently has a $55/bbl price deck for 2020 and views $50/bbl as the likely benchmark on which budgets will generally be set. However, at $55/bbl, many players in the E&P sector are still struggling to generate a level of FCF that competes with the broader market, according to Grigel. “We need to continue to push for additional FCF generation.”

As E&Ps look to enhance FCF, Grigel encourages them to wage “a two-front war.” On one front are measures to lower general and administrative expense and operating expenses, which are “more easily controlled” short term, but have more limited impact. The other includes mitigating corporate decline rates and raising capital efficiency, which offer greater scope but take longer to implement.

Pending further FCF being generated by the energy sector, how scarce are generalist investors venturing into energy?

“Investors have touched the stove many times, and they’ve learned that the stove is hot. And they don’t like touching the stove anymore,” commented Grigel to a generalist investor.

“Touch the stove?” questioned the generalist investor in reply. “Most won’t even enter the kitchen.”

Recommended Reading

Defeating the ‘Four Horsemen’ of Flow Assurance

2024-04-18 - Service companies combine processes and techniques to mitigate the impact of paraffin, asphaltenes, hydrates and scale on production—and keep the cash flowing.

Tech Trends: AI Increasing Data Center Demand for Energy

2024-04-16 - In this month’s Tech Trends, new technologies equipped with artificial intelligence take the forefront, as they assist with safety and seismic fault detection. Also, independent contractor Stena Drilling begins upgrades for their Evolution drillship.

AVEVA: Immersive Tech, Augmented Reality and What’s New in the Cloud

2024-04-15 - Rob McGreevy, AVEVA’s chief product officer, talks about technology advancements that give employees on the job training without any of the risks.

Lift-off: How AI is Boosting Field and Employee Productivity

2024-04-12 - From data extraction to well optimization, the oil and gas industry embraces AI.

AI Poised to Break Out of its Oilfield Niche

2024-04-11 - At the AI in Oil & Gas Conference in Houston, experts talked up the benefits artificial intelligence can provide to the downstream, midstream and upstream sectors, while assuring the audience humans will still run the show.