Berkshire Hathaway’s relentless buying spree had garnered about 13.6% of Phillips 66—shares valued at around $5.8 billion—as February began, a demonstration of faith in a midstream-downstream company at a time when investor confidence in energy equities in general is MIA.

Does Berkshire’s chairman and CEO, Warren Buffett, know something we don’t?

The short answer is: yes, he’s Warren Buffett, the world’s greatest investor who is worth around $59 billion. And we’re not.

The longer answer goes beyond Phillips’ refining assets, which thrive in a low commodity price environment. Berkshire made it clear that its big investment was inspired by midstream assets as well, along with its approval of the direction CEO Greg Garland is taking the company.

“Phillips 66 is actually a diversified company,” Ananth Chikkatur, manager, energy advisory and solutions for ICF International, told Midstream Business. “They have midstream as well as refining, downstream and chemicals. Assets in such a company act as a natural hedge against uncertainty and changes in prices.”

Raymond James & Associates concurred in a recent research note:

“With the added kicker of world-class chemical and midstream assets, Phillips 66 appears well-positioned for any commodity price environment with an excellent management team setting the company up for long-term returns,” the analysts wrote.

And while many public companies have taken a beating from investors for the perception of straying from core business expertise, the strategy of diversification may be a safer bet in tough times.

“I would tend to think that a pure shale play company would scare Berkshire Hathaway,” Kevin Petak, ICF’s vice president, oil and gas markets, told Midstream Business. “It’s strictly tied to commodity prices and whatever commodity prices do; that’s the risk that Berkshire Hathaway would have a difficult time hedging away. They would view Phillips 66 as being naturally hedged just because its business is more diverse.”

Downstream invasion

Expanding beyond a company’s core business may seem counterintuitive when industry economics are shaky, but it might be the best route to strengthening a balance sheet. All that’s needed is money—preferably lots.

“If the one market is challenged, then you try and find another market and if one market then recovers, then perhaps your others will follow as well,” Greg Haas, director with Stratas Advisors, told Midstream Business. “If you have the capital and the ability to manage diversification, it makes sense in a low commodity price environment.”

Last year’s purchase of MarkWest Energy Partners LP by Marathon Petroleum Corp.’s midstream unit, MPLX LP, signaled that downstream’s invasion of midstream was on in earnest. The deal joined Marathon’s refineries in Ohio and Kentucky with MarkWest’s dominant NGL production in the region. The refineries had been upgraded to process condensate from the Marcellus and Utica shales. The deal also provided a rich source of high-value isobutene, a feedstock in the alkylation process that augments the production of gasoline.

Low commodity prices benefit the refining sector, so it is no surprise that MPLX was not alone in pursuing acquisitions.

• Dallas-based Holly Energy Partners LP, which operates six refineries, acquired a 50%interest in Frontier Pipeline Co. from an affiliate of Enbridge. The 296-mile, 72,000 barrel-per-day (bbl/d) pipeline connects to the SLC Pipeline to supply Canadian and Rocky Mountain crudes to refiners in the Salt Lake City area.

• Valero Energy Corp. purchased a 50% interest in the Diamond Pipeline, a 20-inch, 444-mile pipe that will connect Cushing, Okla., to Memphis, Tenn. Plains All American Pipeline LP is building the $900 million line, which will provided a capacity of 200,000 bbl/d after expected completion in early 2017.

• Tesoro Corp. bought Great Northern Midstream LLC, a crude oil logistics provider that owns and operates the new 97-mile BakkenLink crude oil pipeline, as well as a 28-mile gathering system, 657,000-bbl storage facility and 154,000-bbl/d rail loading facility in Fryburg, N.D., in the Williston Basin. The rail facility can provide outbound deliveries to all three coasts.

• PBF Energy Inc. a New Jersey-based refiner purchased the Torrance, Calif., refinery from ExxonMobil along with related midstream logistics assets. The price was $537.5 million plus working capital to be determined at closing, probably in the second quarter.

Long term/short term

The advantages are clear from an operational perspective, but investors do not necessarily share the enthusiasm. From the point of each announced transaction into February, only PBF Energy in this group experienced a lift in unit price. MPLX saw its unit price lose most of its value from July 2015 to February.

That might indicate market displeasure with the transactions but then again, many energy boats have been sinking in this low equity tide. The short-term approach, personified by the proverbial “Dentist in Omaha” who may be unfamiliar with the volatility of the energy business but has a fondness for healthy returns, is countered by the approach of the proverbial “Oracle of Omaha,” Buffett himself.

“Berkshire Hathaway thinks much longer term when they’re buying assets,” said Petak. “They’re thinking 10 to 20 years, they’re not thinking three to five years. That’s what makes it difficult for some firms. Why have the private equity firms not really jumped in? It’s because their investment horizon is much shorter, typically. They’re looking for turning an asset within five years. They want to invest in an asset today, and then flip the asset three, four, five years down the road.”

Initiating the process of making a major investment decision in volatile times is difficult, which is why the private equity firms have held off, Petak said. Uncertainty breeds lower buying prices and the large bid-ask spreads are unattractive.

“Until the environment either gets more certain, or there’s more pain, I don’t think the PEs [private equity firms] will really jump in,” he said.

Unpopular debt

The more pain, the more the position of strength of the haves is reinforced in dealings with the have-nots.

“The companies that have capital or have the ability to raise capital, even today, are the ones that are going to have a huge advantage in a time when capital is constrained because the prices and investor sentiment is, at best, flat,” Haas said. “Right now we think investor sentiment is still very negative in the oil space.”

The appetite of banks to take on debt in this sector is likely limited, he said, and any thoughts by an upstream executive to launch a significant IPO are probably best left for another day.

“The ability of a midstream company to raise capital is somewhat better as long as it’s fee-related and not commodity-exposed,” he added. “The ability of a downstream company to raise capital is actually pretty good considering that low prices of crude oil actually help refining margins as long as there’s good demand for gasoline and the finished, refined product.”

‘Conveyor belt of projects’

Downstream players are well-positioned to expand into the midstream, especially in the purchase of assets already in close proximity, like pipelines that feed refineries. But downstream’s strong position also can make it an attractive destination for a midstream company.

Howard Midstream Energy Partners LLC sought to diversify its business from day one.\

“The companies that seemed to do the best, meaning those that trade at the lowest yields, the ones that have the most interest from investors, are the ones that have a diversified portfolio of assets, the ones that have steady cash flow, the ones that always have a conveyor belt of projects to announce,” company CEO Mike Howard told Midstream Business.

Howard Energy was founded in June 2011, but its executive team is comprised of industry veterans. They knew that to both expand their business and insulate themselves from price volatility, they would need to pursue opportunities away from the wellhead.

“When we started, we were 50% a construction company and 50% a midstream company,” Howard said. “We didn’t get diversified in downstream until 2012, but it was always our goal. We know that if you’re near the wellhead and there’s nothing being drilled, nothing being produced in a particular basin, you need something to stay in business while that particular business segment is down.”

Moving down that path meant moving toward long-term contracts, as well as building the company’s portfolio. That would give Howard Energy an edge over competitors of similar size in gaining access to capital at a lower cost.

“We have gathering and processing, we have stabilizing, condensate handling, crude oil handling with our stabilizer, bulk liquid storage with our Brownsville facility, bulk liquid storage with our GT Logistics facility—both of those have rail as well,” Howard said. “We moved into long-term natural gas transportation which we had in gathering and processing, but we didn’t have long-term, big pipe natural gas transportation.”

Independent segments

The strategy makes sense to Haas.

“It’s fully understandable why Howard [Energy] is looking to diversify,” he said. “They have a great footprint expertise in operations and development of new projects. They’re getting into the gas side of the business, they’re staying in the condensate stabilization business, getting into the rail business, as well, so move those barrels and products around.

“It totally makes sense to expand into other areas so that your core business is not the only one and so your core business potential is not affected by only one commodity price swing,” Haas said. “A little bit of diversification in times of low commodity pricing always tends to help.”

And while Howard waits for oil and gas prices to recover, he’s pleased that his plan came together.

“When you look up four years later from where we started, we have many different business segments that perform independently of each other,” he said. “Now of course, nobody’s happy right now with commodity prices. We all want drilling to come back because that does help everybody, but we’re able to sustain this low period in the market because we have so many business lines that aren’t dependent on a commodity price directly.”

Perception vs. reality

The strategy makes sense to Haas.

“It’s fully understandable why Howard [Energy] is looking to diversify,” he said. “They have a great footprint expertise in operations and development of new projects. They’re getting into the gas side of the business, they’re staying in the condensate stabilization business, getting into the rail business, as well, so move those barrels and products around.

“It totally makes sense to expand into other areas so that your core business is not the only one and so your core business potential is not affected by only one commodity price swing,” Haas said. “A little bit of diversification in times of low commodity pricing always tends to help.”

And while Howard waits for oil and gas prices to recover, he’s pleased that his plan came together.

“When you look up four years later from where we started, we have many different business segments that perform independently of each other,” he said. “Now of course, nobody’s happy right now with commodity prices. We all want drilling to come back because that does help everybody, but we’re able to sustain this low period in the market because we have so many business lines that aren’t dependent on a commodity price directly.”

Perception vs. reality

That diversity is well understood and appreciated among Howard Energy’s customers and clients and the 22 banks, led by RBC Bank, that support it with capital. If the company went public, that might not be the case.

“People will automatically say, ‘oh, they’re a gathering and processing company,’” Howard said. “And that’s true. When you look at our revenues and cash flows, the majority is based on gathering and processing.”

By 2017, however, the company expects to have achieved a 50:50 mix of midstream and downstream revenues. Try explaining that to the dentist in Omaha.

“If we were public, that’s great access to capital, but probably you would have people wanting to lump you into a category because they can’t think of you differently than what your peers are doing,” Howard said. Establishing a unique brand among 121 MLPs is not easy and companies with misunderstood identities have been taken to task by unforgiving investors for straying from their core businesses.

“Whenever you look back at the history of some of the big ones out there, whether it be Enterprise or Kinder Morgan or Energy Transfer, those guys didn’t start out being a diversified portfolio of assets, either,” Howard said. “Everybody started somewhere and moved toward that because it’s like diversifying your retirement portfolio. You want to be diversified across all industries or all business segments so if something is down, you’re not losing your retirement.”

The pullback from vertical integration is a market trend going back 20 years, Petak said, but the risk extends beyond Wall Street concerns. He cited the case of Florida Power & Light’s investment in a natural gas drilling project in Oklahoma that was brought before Florida’s Supreme Court in December.

The utility’s partnership with Petro-Quest Energy Inc. to develop up to 38 natural gas production wells in the Woodford Shale came with the expectation that its customers would save more than $100 million over the life of the investment. The project lost $5 million last year and consumer advocates took the utility to court, contending that it should not have been allowed to charge consumers for a deal with inherent risk.

Florida Power & Light purchases up to 2 billion cubic feet per day of gas at market prices for its gas-fired power plants. Over the 30-year expected life of the wells, the utility expects to be able save customers money by hedging a portion of the fuel in advance to protect against price fluctuations.

“That is just an example of one of the problems with vertical integration in that companies are getting away from their core businesses,” Petak said. “They’re not as comfortable with the business, they don’t know it as well, they also have to get approvals from their regulatory commissions potentially if they’re taking on assets, so there are regulatory risks associated with what they’re doing. Their management team just may not understand that part of the business unless some members from the management team have come out of that part of the business.

“So there are a lot of issues there with melding the assets together and managing two very different businesses that companies just don’t want to take on because it just doesn’t fit with what they’ve been doing historically,” he said.

Timing it wrong

Diversification may be part of a company’s long-term plan, but that doesn’t necessarily mean that sticking to that plan is the best idea. Howard Energy, for example, had already built a stabilizer, so it is well-positioned to capitalize when condensate exports find lucrative overseas markets. 2016, however, would not be a good time for a newcomer to the business to proceed with plans to build one, given the very low market prices for crude oil.

That may have been a factor in the sudden departure of Cheniere Inc. CEO Charif Souki late last year. Souki viewed condensate exports as an opportunity to be pounced on without delay. His board, led by members aligned with investor Carl Icahn, disagreed.

“In the case of Cheniere, they became the 800-pound gorilla in terms of Gulf Coast LNG exports,” Haas said. “When they started talking about the potential for expanding and diversifying into condensate exports out of Corpus Christi, the timing of that was very bad.

I can understand why Icahn and others on the board felt that it was not rational to invest in condensate splitters at the present time.”

Granted, Souki and other senior executives had also been aggressively selling their stock in the company, which reportedly did not enamor them to the board. The splitter, though, would have cost Cheniere about $500 million at a time when that segment is in rollback mode.

“In all things diversification, you have to be early and you have to time it properly,” Haas said. “If you’re late to the game and getting into an unattractive business, diversification will not help.”

Reorganizing diverse pieces

The strategy doesn’t have to be dramatic to be effective. In the case of Linde Engineering North America Inc. (LENA), it was a matter of joining the midstream and downstream units of the company to position it to take advantage of opportunities that the downcycle offered.

The U.S. engineering division of Germany-based The Linde Group, the world’s largest gases and engineering company with over 65,000 employees and 2014 revenues of $17.9 billion, builds natural gas separation, hydrogen, air separation and petrochemical plants. Prior to the reorganization, implemented last year, the separate units were subject to the harsh cycles of the industry.

“While natural gas was in a heavily invested time frame from 2010 onward for our organization, activity in the downstream area was not significant,” Steve Bertone, president and CEO of LENA, told Midstream Business. “Now, as oil and gas prices have gotten very low, we see the opposite happening. In the midstream, there’s not much investment in gas, but we see tremendous investment in the downstream—petrochemical plants to produce ethylene and then downstream of that, polyethylene and polypropylene. We also see an abundance of activity in ammonia plants, which use natural gas as a feedstock.

“As the industry cycles from one trend to another,” he said, “we always have an upside to the company.”

Even the recently voiced fears of a sustained low oil and gas prices do not concern Bertone very much because that environment encourages investment growth in the downstream, particularly petrochemicals, hydrogen and ammonia.

“That portion of the market is very robust,” he said. “The economics of these plants is much more favorable than it would have been eight to 10 years ago when we had high oil and gas prices.”

Investment in downstream was meager then in North America, with few expansions or new projects, he said. The market was mainly growing in the Middle East and the Far East.

“Now, with the drop in gas prices, which has led to a drop in the price of the materials used to feed these plants, it becomes much more economically advantageous for companies to build these plants in the U.S.” Bertone said. “We can compete now with other regions of the world. Ten years ago it would have been impossible.”

Solid and unspectacular

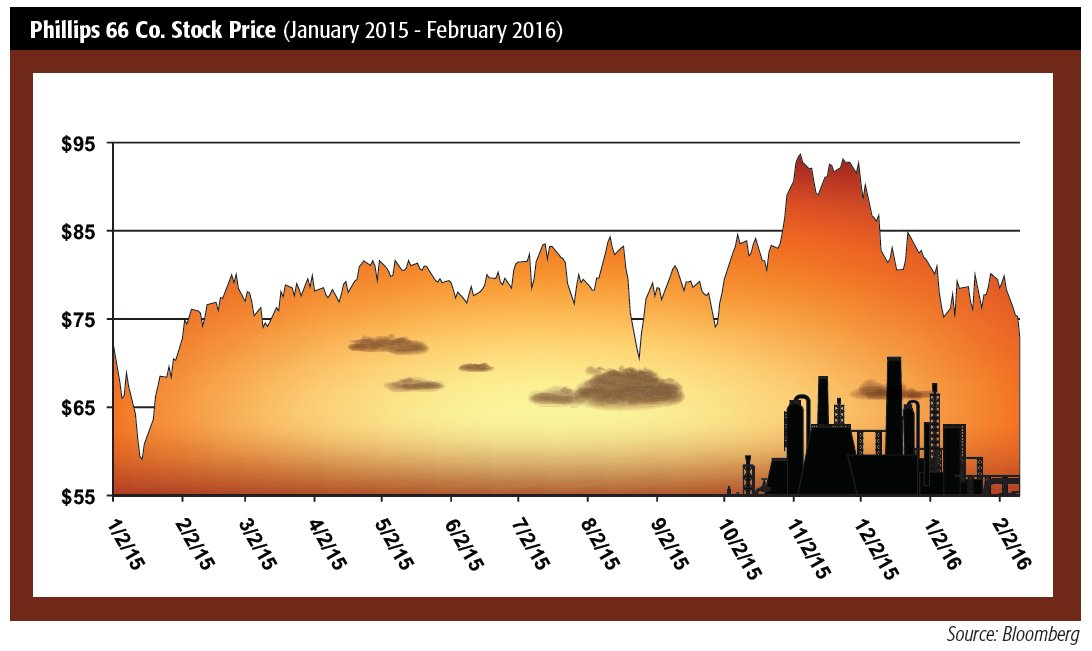

In 2015, the S&P Energy index declined by 31.9%. Same year, the unit price of Phillips 66, a Buffett favorite, rose by 14.1%, which was considered solid by J.P. Morgan, though its analysts noted that the company trailed other refiners.

Can’t please everyone all the time, which is a risk of diversification. When commodity prices recover and refining begins to suffer, the Phillips refining business may suffer as well, but its midstream business will likely experience a rally.

Berkshire and the second-largest holder of Phillips 66 stock, the Vanguard Group, value solid and unspectacular.

“Phillips and their partners are definitely looking to build best-in-class assets amid these high margins and amid these low, low feedstock price environments,” Haas said, listing what a company needs to navigate the low-price environment:

• Good base in assets;

• Good management; and

• Good access to capital.

“Those three things will help separate those who are more advantaged from those who are underadvantaged,” he said.

Howard, whose company is building gas pipelines to Mexico, sees that separation, too. His international lenders, in particular, are impressed that Howard Energy is not subject to a single business segment and has numerous operations that are not drilling-based.

“The companies that are diversified, that have a bunch of different ways to make money, seem to be the ones that have the most attractive list of banks, the most attractive list of investors,” Howard said. “It seems that those are the guys that always do well in these bad times. You can see a separation when you look at the market right now.

“The companies you’ll see come out of this are the ones that are diversified,” he said. “We want to lump ourselves in with those guys.”

Therein lies the paradox: diversify to gain an operational advantage in a downcycle and risk investor pushback for drifting away from the essence of the business.

“One of our biggest blessings right now is that we’re not public and so we don’t get gauged like that,” Howard said. “If we ever do go public, one of our sensitivities will be that we come out as a diversified portfolio of assets and the public will always know it is a diversified portfolio.”

Publicly owned companies must walk that equity market tightrope, however, and as the year progresses, expectations are that M&A volume will make a strong comeback. ICF projects that the uptick will begin in the third or fourth quarters of 2016. It has to do with reality setting in and the acceptance that 2014 was, well, two years ago.

“You’re longer into the turmoil,” Petak said. “There’s recognition of the new paradigm and that recognition period is now over and then there’s a reaction to the new paradigm and we’re in the initial stages of that reaction.

“This year will likely be a better transaction year,” he continued. “There will be more transactions, the bid-ask spreads will become more realistic. You will see that the PEs will become more active. It’s those bellwether companies like the Berkshire Hathaways that may be a little bit in the forefront of deals because they have a longer view. They will be driving some of the transactions and PEs will be watching that and reacting and getting into the game as a result.”

Will that create a more accepting environment for diversified companies?

Follow the leader

Perhaps, if the industry plays “follow the leader.” The leader is Berkshire Hathaway, a company that values stable, long-term growth in critical industries like energy, and whose favorite target is Phillips 66, with $42 billion of market cap solidly planted in the midstream and downstream.

“People watch bellwether holding companies like Berkshire Hathaway,” said Petak. “PEs are going to watch what the big holding companies are doing, the folks with the cash reserves are doing, like Berkshire Hathaway that take a much longer view. They’re going to watch what Berkshire Hathaway is doing and what it’s moving on because that is a metric that is key to their investment strategy.

“Some of the PEs may not want to get left behind in this environment,” he said. “There’s a risk of not moving, even though you may expect that assets will become more distressed this year. If you wait around forever, then you’re going to be left behind in this game.”

How To Build Out Without Really Building

Diversifying into the downstream makes sense from a strategic perspective, but the economics are lacking for most players to build a refinery from scratch.

That’s why the recent deal for ArcLight Capital Partners and Freepoint Commodities to purchase the moth-balled Hovensa refinery complex in St. Croix, U.S. Virgin Islands, has intrigued so many in the industry.

The 2,000-acre facility, with docks that jut into Limetree Bay and that sits just across the road from the Captain Morgan Rum Distillery, houses about 32 million barrels (bbl) of crude and petroleum product storage, refining units with a peak capacity of 650,000 barrels per day (bbl/d), a deepwater port with nine docks, six tugboats and other related equipment. It was closed in 2012 and purchased during a bankruptcy auction for $190 million.

“They’ve indicated that with a couple hundred million dollars of investment, they can make that facility work as a terminal to receive crude from various parts of the world, blend it and then send it over to other parts of the world to be refined later,” Greg Haas, director with Stratas Advisors, told Midstream Business. “It will become a new hub, and a very important new hub in the Caribbean area.”

The Limetree Bay Terminals project already has a major customer waiting when it relaunches operations. China Petroleum and Chemical Corp. (Sinopec) the Chinese oil company, has taken a 10-year lease for 10 million bbl, or about 75% of crude oil storage capacity. Sinopec’s eagerness to sign on enabled ArcLight and Freepoint to purchase the facility.

“One way [to diversify] in low-price environments is to find existing facilities so that you can make small incremental investments and repurpose facilities into new uses,” he said. “It had been a refining site, it’ll now be a crude oil blending terminal, and it’s under long-term contract even through these prices.”

Sinopec’s motivation comes from its production deal with Venezuela. The company needed a terminal to blend, ship and load the crude and the former Hovensa plant became available.

“ArcLight is helping to make that happen on U.S. soil, rather than Venezuela or other nations that could have potentially put together a package to serve as China’s shipping grounds,” Haas said.

ArcLight and Freepoint will reportedly spend more than $300 million to purchase the site and bring storage tanks back into service in batches throughout this year. Fully repurposing the facility would cost quite a bit more if the partners choose to do that, but the cost will still be miniscule compared to building such a complex from the ground up.

For example, the latest cost estimate for Kuwait’s full-service Al-Zour refinery, scheduled to open in 2019 with a capacity of 615,000 bbl/d (similar to Hovensa) is $16 billion. Even for ArcLight, that might be a bit much. In the 15 years of its existence, the sum of ArcLight’s investments in some 90 projects totals less than $14 billion.

Plenty Of Interest Before The ‘For Sale’ Sign Goes Up

Got $7.4 trillion? Consider Saudi Aramco.

As of mid-February, that was the potential equity valuation of Saudi Aramco’s reported 261.1 billion barrels (bbl) of crude reserves if realized in the market at the same rate as the 11.76 billion bbl of reserves reported by publicly traded ExxonMobil.

Then again, perhaps lower those expectations.

It appears that the IPO concept leaked last year may only apply to the Saudi energy giant’s international refining operations that are already joint ventures. That a government-run energy entity of this magnitude—estimated values range from $800 billion to $10 trillion—would even consider sales on the open market, however, is a stunner, compelling many to wonder why.

All signs point to diminished revenues resulting from low oil prices.

“They are raising cash, we think, for upstream operations,” Kevin Petak, Virginia-based vice president, oil and gas markets for ICF International, told Midstream Business. “They’re looking at selling some of their international refining operations. We think that it’s to raise cash to focus on their core business. It is surprising because companies like Saudi Aramco and ExxonMobil generally move relatively slowly. From that standpoint, this does come as a surprise to most folks.”

It’s a matter of economics—domestic economics, Ananth Chikkatur, manager, energy advisory & solutions for ICF International, told Midstream Business.

“Saudi Aramco provides a lot of financial support, budgetary support for the government of Saudi Arabia,” he said. “Continued low oil prices are leading to budget deficits, and some of these moves could be a way to raise funds for domestic spending. We need to view this not just from a pure economics angle, but also from a political, economic angle.”

That angle could be influenced by the reintroduction of Iranian oil onto global markets, Stratas Advisors’ Washington-based analyst Thomas Buonomo told Midstream Business.

“A plausible geopolitical motive for the IPO would be to draw foreign investment away from Iran’s oil industry and maintain Saudi Arabia’s leadership role within OPEC by sustaining a low cost of production over the long term,” he said. “It also should be considered within the context of increasing domestic energy demand, limited refining capacity and fuel subsidies, which will place increasing burdens on the budget if greater efficiencies are not introduced and profit margins not generated.”

Domestic considerations are critical following the recent 67% hike in the subsidized price of 91-octane gasoline (the local regular grade) at the end of last year to the equivalent of 75 cents per gallon. Raising cash to expand the kingdom’s engagement with the downstream sector plays a role in that, Greg Haas, Houston-based Stratas director, told Midstream Business.

“It makes sense in that they can employ Saudi nationals in the refining and construction,” he said. “A barrel of gasoline is typically more valuable than a barrel of raw crude oil, so if they can refine more inside the kingdom and employ their people, they can capture some of that extra margin of refining gasoline and diesel and jet fuel and other things beyond simply selling crude oil.”

Low oil prices have placed Saudi Aramco in the unfamiliar position in which selling parts of itself is considered a viable option.

“That’s a very common situation where companies say, ‘we have tremendous growth prospects, we have good projects, but how do we fund it?’” said Haas. “That’s what the capital markets are for. If Saudi Aramco can carve out some of its refining assets and the growth aspects related to future refineries and IPO the refining side of Saudi Aramco, then that would make a much more reasonable IPO and still be very large.”

Dr. Petr Steiner, Stratas’ Brussels-based director and refining expert, agrees that domestic sensitivities are a driver in the Saudis’ strategy.

“Politically and domestically, the Saudis might want to send a signal that they are becoming more open to international capital—and money from something other than the sale of oil could help the economy,” he told Midstream Business. “This could be expanded to their other companies, for example, petrochemicals [Rabigh Refining and Petrochemical Co., or Petro Rabigh, which is co-owned by Saudi Aramco and Sumitomo Chemical, and began selling shares in 2008], electricity, etc. They will need to build quite a few refineries in the next decade to keep demand in balance. At the same time, they are looking into investing into even more JVs [joint ventures] in Chinese refining—so this might become a new model for their JVs.”

A trend along these lines is irrelevant because the sheer size of Saudi Aramco defies comparison. Its proved reserves of oil and condensate are 22 times that of ExxonMobil.

“The big state-run companies internationally may all react very differently because it depends on what their own governments are doing, the situation their own governments are in with cash and with political issues,” Petak said. “Reaction across the board could be very different in this low commodity price environment.”

Recommended Reading

Nebula Energy Buys Majority Stake in AG&P LNG

2024-01-31 - AG&P will now operate as an independent subsidiary of Nebula Energy with key offices in UAE, Singapore, India, Vietnam and Indonesia.

JMR Services, A-Plus P&A to Merge Companies

2024-03-05 - The combined organization will operate under JMR Services and aims to become the largest pure-play plug and abandonment company in the nation.

Flame Acquisition Holders Approve Merger with Sable Offshore

2024-02-14 - The business combination among Flame Acquisition Corp., Sable Offshore Holdings and Sable Offshore Corp. will be renamed Sable Offshore Corp.

Enerplus Increases Quarterly Cash Dividend

2024-02-23 - Enerplus Corp. increased its dividend 8% to US$0.065 (CA$0.088) per share.

SilverBow Rejects Kimmeridge’s Latest Offer, ‘Sets the Record Straight’

2024-03-28 - In a letter to SilverBow shareholders, the E&P said Kimmeridge’s offer “substantially undervalues SilverBow” and that Kimmeridge’s own South Texas gas asset values are “overstated.”