We frequently discuss shoulder seasons—basically the early fall and spring periods between winter and summer when heating/cooling demand are at their lowest. In 2015, we’re in the midst of another form of shoulder season: one in the center of the market’s nominal peak demand season, but instead of park prices, we see lower prices from an oversaturated market.

The outlook for crude prices has been mixed with several analysts, perhaps most notably Goldman Sachs, forecasting that values could fall below $40 per barrel (bbl). However, other firms, such as Barclays Capital, En*Vantage and Global Hunter Securities, are predicting prices above this threshold.

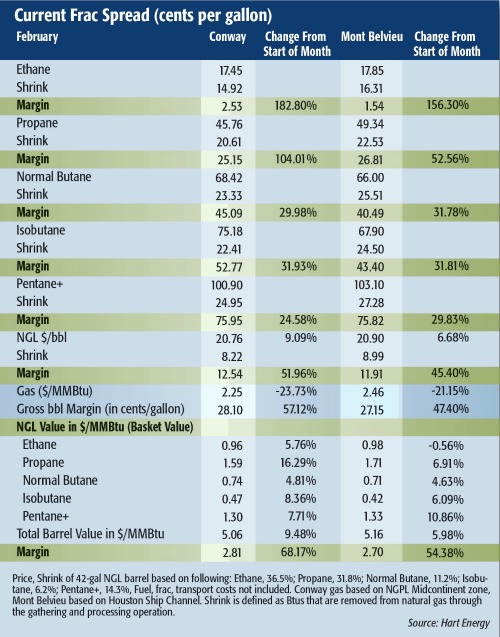

According to En*Vantage, geopolitical risks in economically weak oil-producing nations could cause production declines or disruptions. Barclays Capital also anticipates crude prices will consolidate, as it retained a neutral outlook. Global Hunter Securities anticipates a near-term drop in values with West Texas Intermediate prices falling to the mid-$40s per bbl. While the outlook for crude remains uncertain, the outlook for ethane has a bright side for the first time in more than a year as margins turned positive after struggling for much of the past two years. Granted, these positive margins are quite slim and once transportation fees are calculated, they are no longer positive, but it is an upside for the market.

The ethane sector has experienced tremendous headwinds the last year-and-a-half as cracking capacity was reduced by expansions and turnarounds. This was especially troubling to producers as it increased storage and resulted in widespread rejection.

But this strategy was successful as ethane prices held firm while the rest of the NGL barrel took a downturn in value in late 2014 and early 2015. Since ethane makes up the bulk of the NGL barrel and is expected to begin to post gains later in the first quarter when cracking capacity peaks, it is a positive sign for NGL producers.

On the opposite end of the spectrum is propane, which has lost more than $1 per gallon (gal) in value in the past year at the Mont Belvieu, Texas, hub and nearly $2.50 per gal at the Conway, Kan., hub. Last year, propane had record demand from both the home heating and LPG export markets. This year, heating demand isn’t as high, even after the much vaunted “Blizzard of 2015” that failed to live up to expectations in many regions. LPG export demand has dropped significantly, leaving a large storage overhang.

It’s been a staggering decline, and prices will likely remain flat or possibly decrease further before they improve.

Frank Nieto can be reached at fnieto@hartenergy.com or 703-891-4807.

Recommended Reading

Oceaneering Won $200MM in Manufactured Products Contracts in Q4 2023

2024-02-05 - The revenues from Oceaneering International’s manufactured products contracts range in value from less than $10 million to greater than $100 million.

E&P Highlights: Feb. 5, 2024

2024-02-05 - Here’s a roundup of the latest E&P headlines, including an update on Enauta’s Atlanta Phase 1 project.

CNOOC’s Suizhong 36-1/Luda 5-2 Starts Production Offshore China

2024-02-05 - CNOOC plans 118 development wells in the shallow water project in the Bohai Sea — the largest secondary development and adjustment project offshore China.

TotalEnergies Starts Production at Akpo West Offshore Nigeria

2024-02-07 - Subsea tieback expected to add 14,000 bbl/d of condensate by mid-year, and up to 4 MMcm/d of gas by 2028.

US Drillers Add Oil, Gas Rigs for Third Time in Four Weeks

2024-02-09 - Despite this week's rig increase, Baker Hughes said the total count was still down 138 rigs, or 18%, below this time last year.