Drilling operations for Devon’s Energy’s JV in the Stack are expected to commence mid-2020 in northern Canadian County, Okla. (Source: Hart Energy)

Devon Energy Corp. agreed to a drilling joint venture (JV) on Dec. 10 in the Stack play considered by analysts to be a creative solution as E&Ps remain focused on capital discipline.

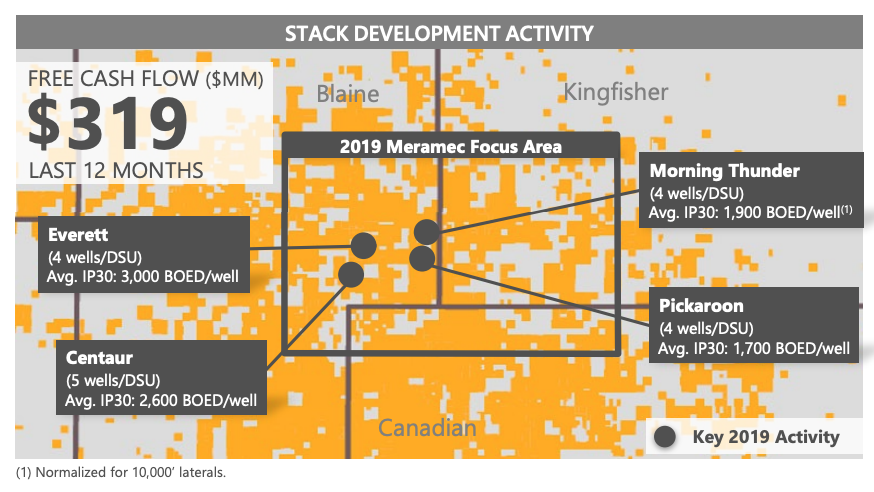

The JV, with Dow, spans 133 undrilled locations in the liquids-rich portion of Devon Energy’s Stack position in central Oklahoma. As part of the deal, Devon monetized half of its working interest in the locations in exchange for a $100 million drilling carry over the next four years.

The partnership is the second Devon Energy has formed with Dow in recent years as E&Ps are increasingly left with fewer capital options. The earlier agreement was for a JV partnership in the Barnett Shale the companies entered into in May 2018.

Paul Sankey, managing director of Mizuho Americas, called the deal a type of “creative thinking” he said he continues to see from operators with properties not currently competing for capital with core positions.

“[Devon] gets immediate cash flow in the door from an asset that it would not otherwise have been investing in for reduced capital investment, similar to [Devon’s] prior deal with DOW in the Barnett,” Sankey wrote in a Dec. 10 research note.

Devon estimates the average working interest monetized in the JV at 60% across a mix of standard and extended-reach lateral drilling locations. The company will also serve as operator and retain 100% of its production and cash flow from existing operations in the Stack play.

According to Phillips Johnston, senior E&P analyst with Capital One Securities Inc., the JV allows Devon to focus most of its capital allocation to its three other major plays that include the Permian, Powder River and Eagle Ford shale basins. He added the agreement also mitigates natural declines in the Stack with a program that offers better economics relative to the alternative of a standalone program with some activity in the play.

JV activity is set to begin in 2020 with the development of two drilling units in northern Canadian County, Okla. Drilling operations are expected to commence mid-year.

Overall, Johnston views the deal as a mild positive for Devon but not a significant needle-mover.

“[Devon’s] near-term financial picture should be largely unchanged as a result of this deal, as there are no up-front cash proceeds and [Devon’s] net activity related to the JV will be minor relative to its activities in its three other major plays over the next few years,” he wrote in a Dec. 10 research note.

Devon anticipates no change to its production targets or capital spending outlook in 2020 as a result of the JV agreement, according to the company press release.

Vinson & Elkins LLP was legal adviser to Devon and Latham & Watkins LLP acted as legal adviser to Dow.

Recommended Reading

Report: Crescent Midstream Exploring $1.3B Sale

2024-04-23 - Sources say another company is considering $1.3B acquisition for Crescent Midstream’s facilities and pipelines focused on Louisiana and the Gulf of Mexico.

For Sale? Trans Mountain Pipeline Tentatively on the Market

2024-04-22 - Politics and tariffs may delay ownership transfer of the Trans Mountain Pipeline, which the Canadian government spent CA$34 billion to build.

Energy Transfer Announces Cash Distribution on Series I Units

2024-04-22 - Energy Transfer’s distribution will be payable May 15 to Series I unitholders of record by May 1.

Balticconnector Gas Pipeline Back in Operation After Damage

2024-04-22 - The Balticconnector subsea gas link between Estonia and Finland was severely damaged in October, hurting energy security and raising alarm bells in the wider region.

Wayangankar: Golden Era for US Natural Gas Storage – Version 2.0

2024-04-19 - While the current resurgence in gas storage is reminiscent of the 2000s —an era that saw ~400 Bcf of storage capacity additions — the market drivers providing the tailwinds today are drastically different from that cycle.