In 2006, when I started following the MLP space, the lurking industry fear was about peak oil. Then the combination of horizontal drilling and hydraulic fracturing led to booming shale production, which eventually created an oversupply so dra- matic that production is now falling.

We have returned—in a way—to an infrastructure outlook reminiscent of peak oil, although supply is now constrained due to pricing, not availability. Existing pipelines still carry hydrocar- bon-based energy, but unless we see a material improvement in pricing, the demand for new infrastructure will be limited to shifts in demand areas due to urbanization or shifts in geographic loca- tions of energy-intensive industries.

As an example of continued-although-muted, supply-based infrastructure demand, Saddlehorn and Grand Mesa decided to combine pipeline projects that individually would providetakeaway capacity from the Denver-Julesburg Basin to theCushing, Okla., crude trading hub. The expected production now only supports one pipeline instead of two. As a combined project, construction costs are decreased on both sides, pipeline capacity aligns with revised production expectations (reducing overbuilding concerns) and future expansion is still possible.

Those MLPs that serve the demand needs of North America have growth prospects despite the unit price contagion from falling oil prices. Examining the multiyear Transco pipeline expansion (owned by The Williams Cos. Inc. family of companies) reveals 13 sep- arate expansion projects, most of which serve the demand-pull need of electricity generation for residential heating. Only two of these projects—Appalachian Connector and Gulf Trace—serve the supply-push side.

Just like the Transco system, few MLPs are entirely on the demand-pull or supply-push side of the midstream business.

In 2005, energy demand in the U.S. had grown by roughly 1% per year since the petroleum shortages in the 1970s. Today, the U.S. Energy Information Adminis- tration predicts that total energy use over the next 25 years will grow by around 7%, or only 0.3% annually. Residential energy consumption is expected to remain flat over the period as en- ergy efficiency standards offset population growth. (We plug in more devices than ever before, but energy-efficient appliances are also now commonplace.) Commercial and industrial en- ergy demand will grow modestly, while domestic transportation demand will fall.

While there has been a two-thirds reduction in expectations for energy demand growth, it’s also important to look at the changing composition of our energy consumption and who stands to bene- fit. Natural gas now accounts for the largest share of U.S. electricity generation and is expected to continue to take market share from coal in the coming decades—a positive for MLPs operating natural gas infrastructure assets.

Change is constant in the energy industry, but MLPs will always have a foundation in the demand for transportable energy.

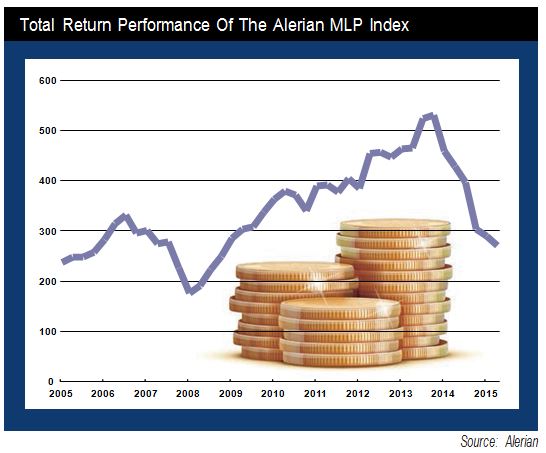

Maria Halmo is the director of research at Alerian, an independent provider of MLP and energy infrastructure market intelligence. Over $13 billion is directly tied to the Alerian Index Series. For additional commentary and research, visit www.alerian.com/alerian-insights.

Recommended Reading

Deepwater Roundup 2024: Offshore Australasia, Surrounding Areas

2024-04-09 - Projects in Australia and Asia are progressing in part two of Hart Energy's 2024 Deepwater Roundup. Deepwater projects in Vietnam and Australia look to yield high reserves, while a project offshore Malaysia looks to will be developed by an solar panel powered FPSO.

Exclusive: Carbo Sees Strong Future Amid Changing Energy Landscape

2024-03-15 - As Carbo Ceramics celebrates its 45th anniversary as a solutions provider, Senior Vice President Max Nikolaev details the company's five year plan and how it is handling the changing energy landscape in this Hart Energy Exclusive.

TotalEnergies Starts Production at Akpo West Offshore Nigeria

2024-02-07 - Subsea tieback expected to add 14,000 bbl/d of condensate by mid-year, and up to 4 MMcm/d of gas by 2028.

CNOOC’s Suizhong 36-1/Luda 5-2 Starts Production Offshore China

2024-02-05 - CNOOC plans 118 development wells in the shallow water project in the Bohai Sea — the largest secondary development and adjustment project offshore China.

Equinor Receives Significant Discovery License from C-NLOPB

2024-02-02 - C-NLOPB estimates recoverable reserves from Equinor’s Cambriol discovery at 340 MMbbl.