A positive sign for oilfield service companies may be a bit of blood in the water, analysts said.

While analysts say upstream companies are poised to restore power to their A&D engines, service and supply companies will be looking for cover.

The 12 months of 2015 have shown that the days of magical thinking—wishing in something to make it happen—are over.

J. David Anderson, analyst with Barclays Capital Inc., said higher oil prices and bottoming cost curves will be positive signs for oilfield services and equipment. So will a little shark bait.

“The credit markets are telling us there will be blood in the water,” Anderson said, “probably fairly soon.”

The market cap of small- and mid-cap companies has shriveled by 70% in the past 18 months—a revealing statistic that illustrates the challenge of finding “investable small- and mid-cap ideas with liquidity.”

In the past 12 months, land drillers have fallen the least, by 30%, and proppant and service companies the most.

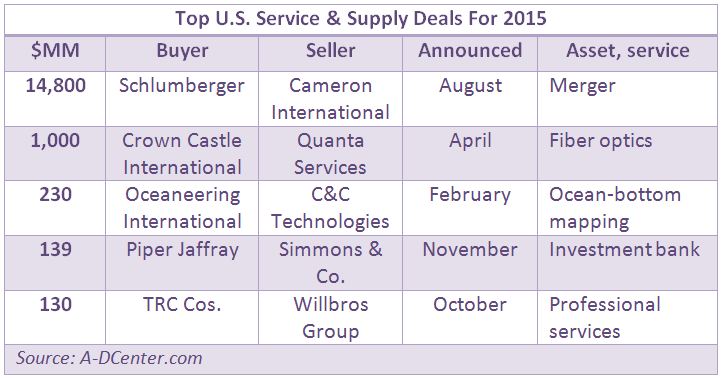

The services industry needs to see companies close up shop or consolidate in a sector with too many companies and too much equipment.

“The oilfield services industry is at the epicenter of the recalibration of the supply cost curve,” he said. “As the depth of the oil price downturn approaches the 18 month mark [longer than any other downturn over the past 20 years], it’s just a matter of time for the industry to go through a phase of bankruptcies and mergers of desperation.”

Small- to mid-cap companies’ leverage ratios have spiked from 1.2x EV/EBITDA to 11.6x over the past year.

“Credit markets smell imminent trouble with high yield oilfield service index trading over 1,000 basis points above corporate levels, by far the widest spread seen,” Anderson said. “There needs to be blood: with too many companies, too much equipment, and not enough capital in the face of weaker upstream demand over the next several years.”

A Natural Selection

For middle market oilfield service companies, 2016 looks to be a “year of reckoning” after E&Ps settled in for a winter too warm for its own good.

“The oilfield services sector is no exception to Darwinism—the weakest middle market companies did not survive in 2015 and it is likely that more will not survive in 2016,” said Chris Wolfe, oilfield services practice group lead at Haynes and Boone in Houston.

Wolfe predicts:

- Middle market oilfield services companies will see significant contraction in business;

- The oilfield services industry may well bottom out in 2016 and start to recover in the second half of 2017; and

- As a result of M&A transactions and asset sales, many established relationships with E&P customers will be disrupted.

Supply companies, particularly proppant sand companies, were quite for much of 2015. The first major sand acquisition was executed in late December as Emerge Energy Services LP purchased assets and interests in 94 million tons of Northern White silica sand reserves in Jackson County, Wis.

U.S. Silica Holdings has consistently said it wants to take part in industry consolidation, said Marc Bianchi, analyst with Cowen and Co.

However, “depending on price and financing, consolidation may not be well received by investors,” he said.

Roughneck Roll Up

Among drillers, a roll-up may occur and contractors will look to consolidate, but only so many cost efficiencies can be squeezed out of combining drilling equipment companies. The biggest expense is capital that is tied up in equipment, said Osmar Abib, global head of oil and gas at Credit Suisse.

“Part of the challenge will be relative value issues and part of the challenge will be a number of those companies have a lot of debt,” Abib said at a December media roundtable in Houston.

Buyers will have to be wary of debt laden targets that could add to their leverage, he said.

“I think that’s going to inhibit a lot of activity, which might mean a lot of those companies might have to be restructured,” Abib said. In bankruptcy or through negotiations with lenders, debt could be reduced to a more manageable level that would enable M&A.

However, potential acquirers also may lack incentives. Since rig counts have fallen, the question becomes why a company would shut down equipment just to add more, Abib said.

“You only do it if you see a really good relative value and benefits in greater size and asset diversification,” he said.

Due to the uncertainty of commodity prices, service and equipment M&A is likely to be limited until the roughest part of the ride is over.

“I will tell you that in this business and in this type of environment, companies are thinking about it,” Abib said. “However, the current level of uncertainty and volatility really makes M&A challenging at least in the near term.”

Contact the author, Darren Barbee, at dbarbee@hartenergy.com.

Recommended Reading

Hess Midstream Increases Class A Distribution

2024-04-24 - Hess Midstream has increased its quarterly distribution per Class A share by approximately 45% since the first quarter of 2021.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.

Murphy Oil Names Eric Hambly as President, COO

2024-02-08 - Murphy Oil has promoted Eric M. Hambly to president and COO and E. Ted Botner to executive vice president. Both will continue to report to CEO Roger W. Jenkins.