Ralph E. Davis Associates believes that improved disclosure about how a type well profile, also known as a type curve, was created would help users better understand the quality and reliability of the estimate. (Source: Hart Energy/Shutterstock.com)

Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

[Editor's note: A version of this story appears in the September 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Unconventional oil and gas reservoirs present challenging problems for reservoir engineers tasked with predicting the future performance of undrilled and recently completed wells. In conventional reservoirs, there are many analytical techniques that can be used, but unconventional reservoirs present too many complexities, variations and unknowns to apply these methods. In particular, the extent, geometry and conductivity of the fracture network are unknown, and perhaps impossible to model.

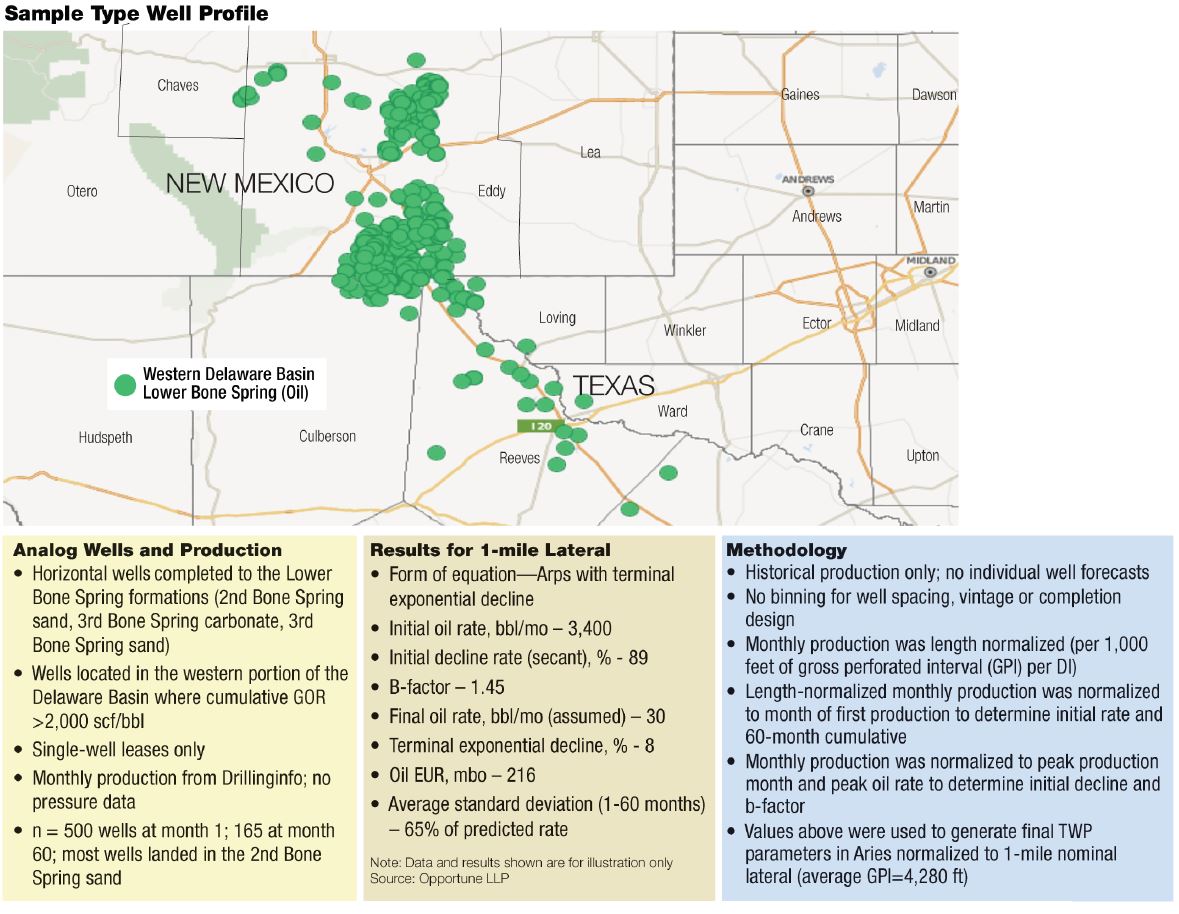

A common solution used by many engineers is to use production data from existing wells nearby as analogues for future wells to generate a type well profile (TWP), also known as a type curve. These type curves are an important bit of information that appears often in company presentations.

They are derived by selecting analogous wells, collecting their production history and key well information, and applying several mathematical adjustments to generate the prediction.

The adjustments include steps like estimating the future production of existing wells, normalizing the data to the first month of production, scaling the data to account for differences in lateral length or fracture design, and binning the data according to other parameters, such as formation or operator.

The scaled and normalized production can be used to generate average production forecasts for each of the bins.

Operators use TWPs to make investment decisions, prepare reserve estimates and to inform their investors about the expected economics of their undrilled wells. Many of them are disclosed to the public in investor presentations and public filings.

But although they are widely used, typically there is very little disclosure about how they are derived. There are no industry standards for the preparation of TWPs. Rather, they are created under many different circumstances, and engineers have personal opinions about the best way to prepare them. However, some of these opinions are certainly better than others.

A committee of the Society of Petroleum Evaluation Engineers is currently considering a solution through development of best practices for TWP generation. Ahead of that work, however, we at Ralph E. Davis Associates believe that improved disclosure about how a TWP was created would help users better understand the quality and reliability of the estimate. Disclosure would also provide more transparency to help users understand why different engineers in the same play and area generate different TWPs.

Recommendations For Better TWPs

We recommend that TWPs presented to the public, to investors or to other consumers be accompanied by a voluntary disclosure that explains or addresses the following items. A sample disclosure is provided here as well.

- Selection of analogous wells – A list of API numbers, a map or a description of the area that includes the analogous wells. If certain well types, operators, vintages, etc., were used to filter the list of wells, that should be disclosed. If the list of API numbers is not disclosed, the number of wells used should be disclosed for each TWP. The goal is to make it clear which wells were used and why.

- Source of the production data – Describe whether the data came from internal or public sources and cite the source. If lease-level data has been allocated to individual wells, this should be disclosed.

- Frequency of the production data – Describe whether daily or monthly production was used. Some public data is reported quarterly, so if the monthly data is calculated from quarterly values, that should be disclosed.

- Months of production history used – The disclosure should discuss how many months of production data was available and used in the TWP. One approach would be to provide the minimum, maximum and median number of producing months.

- Scaling and binning – How was the production data for each analogue well scaled to account for variations in relevant variables (lateral length, for instance), and how were the analogues binned to generate the TWPs?

- “Project the average” or “average the projections”? – Petroleum engineers may average the analogue wells’ production-month-normalized historical data and then project the average into the future, or, they may project the future performance of the analogues and then average the wells’ combined history/projection data. If projections were used, what engineering methods were used to make them? Engineers that have access to detailed production and pressure history data will sometimes employ additional reservoir engineering techniques to project the analogue wells before aggregating them.

- Form of TWP equation – What form of production rate vs. time equation (Arps, etc.) is used to represent the type well?

- TWP parameters – What are the relevant parameters of the resulting TWP? For example, initial rate, initial effective decline, b-factor, minimum decline, final rate, well life, expected ultimate recovery, etc.

- Reliability measures – Statistical measures should be presented that allow the user to understand the uncertainty and reliability of the TWP. These could include confidence intervals around the TWP or standard deviation as a function of time (absolute or a percentage of the expected value).

There are many approaches to creating TWPs, and they often rely on very limited data. We believe that their users should have enough information to understand how they were made, and which specific parameters were involved, so they can make informed investment decisions. A thorough disclosure of the data and methods used would be a good first step, as outlined here.

Steve Hendrickson is president of Ralph E. Davis Associates, an Opportune LLP company. He has more than 30 years of experience in engineering, acquisitions and operations. Before joining Opportune, he was principal of Hendrickson Engineering LLC, a licensed petroleum engineering firm focused on reserves assessment and property valuation. He began his career at Shell Oil as an engineer in Permian Basin water floods and CO2 floods, and was an executive at several E&P companies, including El Paso Production Co. and Eagle Rock Energy Partners LP. He holds an M.S. in finance from the University of Houston and a B.S. in chemical engineering from The University of Texas at Austin.

Recommended Reading

Deepwater Roundup 2024: Offshore Europe, Middle East

2024-04-16 - Part three of Hart Energy’s 2024 Deepwater Roundup takes a look at Europe and the Middle East. Aphrodite, Cyprus’ first offshore project looks to come online in 2027 and Phase 2 of TPAO-operated Sakarya Field looks to come onstream the following year.

E&P Highlights: April 15, 2024

2024-04-15 - Here’s a roundup of the latest E&P headlines, including an ultra-deepwater discovery and new contract awards.

Trio Petroleum to Increase Monterey County Oil Production

2024-04-15 - Trio Petroleum’s HH-1 well in McCool Ranch and the HV-3A well in the Presidents Field collectively produce about 75 bbl/d.

Trillion Energy Begins SASB Revitalization Project

2024-04-15 - Trillion Energy reported 49 m of new gas pay will be perforated in four wells.

Exxon Ups Mammoth Offshore Guyana Production by Another 100,000 bbl/d

2024-04-15 - Exxon Mobil, which took a final investment decision on its Whiptail development on April 12, now estimates its six offshore Guyana projects will average gross production of 1.3 MMbbl/d by 2027.