Midstream-focused private equity has established an outsized slice of the sector’s capital market, and for some very good reasons. Financing the segment’s needed expansion in the past decade has required specialized knowledge, combined with a large Rolodex of prospective client operators and contacts. Meanwhile, there has been a fortuitous—for private equity providers—pullback by competing lenders that has allowed private equity the opportunity to make the most of its expertise.

A sure sign of private equity’s success comes from new players entering the game. Others want in on the action Financing the midstream buildout has been an attractive opportunity, according to Ben Davis, partner with Dallas-based Energy Spectrum Capital.

Crowded field

“There are more and more midstream funds coming on the scene,” Davis told Midstream Business. “There has been an increase in smaller funds, and the space of large funds that can do multi-hundred million-dollar deals is getting crowded.” The growth in midstream private equity probably peaked in 2014 with the zenith in commodity prices, Davis estimated, but the business is more crowded than it was, say, five years ago, and further expansion is likely as the energy sector returns to full health.

Energy Spectrum enjoys a unique view of the sector and its capital needs. It claims the distinction of being the first midstream-focused private equity shop in the U.S., dating from 1996. Davis has been with the firm since 1997. It has raised $3.5 billion of equity capital through seven funds to date.

“There has often been interest by the upstream funds to get into midstream," he noted, as well as general-interest private equity firms that count energy investments right along with cosmetics or cable television. But he emphasized midstream-focused investors enjoy an advantage over such competition.

Billy Lemmons, managing partner and founder of EnCap Flatrock Midstream, sees the same trends.

“We continue to see more capital come into the space from several different directions,” he told Midstream Business. “We see more groups trying to form more funds and other investors trying to make direct investments in the business. But the most significant thing we continue to see is that midstream is a very complicated business. To be successful you have to have the best management teams supported by a very experienced, high-quality capital provider. This allows you to see opportunities, take advantage of them and minimize missteps.”

EnCap Flatrock Midstream is another longer-term player in the niche. The San Antonio-based firm organized in 2008 through a partnership between EnCap Investments LP and Flatrock Energy Advisors. The firm manages nearly $6 billion in investment commitments from a broad group of institutional investors. It is currently making commitments to new management teams from its EFM Fund III, a $3 billion pool.

Regardless of the industry, the concept behind private equity is simple and owes its origins to the leveraged-buyout firms that emerged in the 1980s. A private equity firm creates a fund of capital that can then be invested in an operating company for any number of goals. Common investment strategies may include leveraged buyouts, venture capital, growth capital, distressed investments and various kinds of mezzanine capital—subordinated debt or preferred equity instruments. A private equity provider typically invests in a start-up or existing operating company that will later be taken public in an IPO or sold to another firm.

‘Quarterly capitalism’

Private equity, regardless of the industry, has advantages over commercial banks or publicly held companies, with numerous financial reporting requirements and a typical emphasis on shortterm financial returns; The Economist referred to this trait as “quarterly capitalism” in a recent feature article analyzing private equity. The story pointed out private equity’s ability to show long-term patience as an operating company starts up has proved to be a major advantage.

“The growth of private equity has been so strong that it has a bubblish feel,” The Economist added. “Private equity’s current appeal rests not on whether it can repeat the absolute returns achieved in the past (which for the big firms were often said to be in excess of 20% annually) but on whether it has a plausible chance of doing better than today’s lackluster alternatives. This is a particular issue for pension funds which often need to earn 7% or 8% to meet their obligations.”

Private equity firms’ investors— called limited partners (LP)—may include those pension funds, as well as various trusts, university endowments family offices and high-net worth individuals with sizeable amounts of money to invest and the patience to enjoy long-term investment horizons. Returns can be very attractive, although as with all investments, the greater the risk, the greater the potential reward.

Midstream-focused private equity can offer investors the potential for attractive returns that are hard to find via other investment vehicles due to a sluggish economy and historically low interest rates. The current 10-year U.S. Treasury note yields somewhere around 2.4%, roughly half what it paid five years ago. Also for energy investors, midstream offers a more stable business environment than upstream producers due to lessened commodity price exposure and the growing use of set, fee-forservice contracts.

Long-term focus

“Private equity funds often deploy capital over a five-year investment period within a ten-year fund life Davis explained.

“While the number of investors has grown over the years, our LP mix really hasn’t changed very much,” Lemmons said, noting EnCap Flatrock’s investors come almost exclusively from domestic institutions with a handful of foreign investors.

While private equity may be aggressive that trend differs from commercial banks’ growing reticence following regulatory oversight.

“Another change is that banks, which are under orders to curtail the risks that they face, are reducing the amounts available for highly leveraged deals. That means borrowing will cost more Economist noted.

“We are seeing commercial banks be much more conservative in their approach, which is restricting capital available to many companies,” David Cecere, principal with Tailwater Capital and an honoree in Hart Energy’s 2016 Thirty Under 40, told Midstream Business. “We have definitely seen opportunities created as commercial banks have pulled back, and that’s a good thing for private equity.”

Tailwater, based in Dallas, currently manages $1.7 billion in committed capital. It has handled some three-dozen transactions in both the midstream and upstream sectors worth $11 billion.

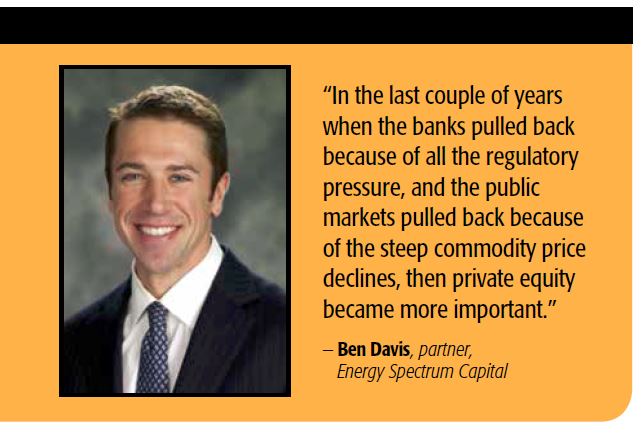

“I think of three primary capital sources for midstream: private equity, senior ‘private’ debt and the public markets, which could be debt or equity but the majority of what we see there is equity—MLPs in particular,” Davis said. “Anytime one or two of those is less available, then the remaining one or two become more important. In the last couple of years when the banks pulled back because of all the regulatory pressure and the public markets pulled back because of the steep commodity price declines, then private equity became more important. We saw a similar dynamic in 2010 during the financial crisis, when there was virtually no access to the public markets and the banks were not particularly active.”

Mitch Fane, U.S. energy transactions advisory services leader for Ernst & ung (EY), points to the impact of commodity prices from 2014 peaks.

“You have very specialized private equity that likes to invest in upstream, idstream and downstream,” Fane said in a recent interview with Privcap. The drop in commodity prices has “put a lot of pressure on the banks when they were going and having discussions with their regulators about their capital adequacy. eaning, are the assets that they’ve made loans on sufficient collateral for the loans that are outstanding to the banks?”

Capital vacuum

In that capital vacuum, “private equity is fairly sophisticated around energy, so it’s a natural bridge for private equity to come in and help finance some of these transactions. They also have a lot of capital available to do it,” Fane said.

Private equity—like all other midstream capital providers—has had to take into account the greater risk implied by the Sabine Oil & Gas bankruptcy case, in which a judge last March cast doubt on how solid the traditional gathering and processing agreements between upstream oil and gas producers and midstream operators are. The argument in that bankruptcy filing by the two midstream operators serving Sabine—that the “covenant running with the land” language in the contracts would preclude rejection by the debtor—was put aside by a judge’s ruling. Court decisions since then seem to indicate the case will stand as an exception rather than a new rule, but doubt and uncertainty remain. Investors don’t like uncertainty.

“It makes it a little bit harder to invest because you worry about whether you can count on the contracts, as they are, staying in place,” Cliff Vrielink partner with Sidley Austin LLP, told Midstream Business.

There also is the added variable of renegotiated contracts spurred by commodity price drops.

“From a private equity perspective, midstream company that has certain contracts introduces some uncertainty”

into a deal. “In a sale situation, the parties bidding on the business may put in either a conditional bid or a two-tier bid that contemplates what they would pay if they could get the contracts renegotiated,” Vrielink added.

Private equity’s view of a midstream investment counts on the sale of a client operating company or its IPO at some point. Such closure has been particularly hard to execute in the midstream recently, observers say.

“After driving much of the U.S. il and gas M&A last year, midstream segment deal activity continued to plummet in the second quarter of 2016,” PricewaterhouseCoopers (PwC) wote in an analysis the sector’s results for the period. “There were only eight announced midstream deals, compared to 11 in the first quarter of 2016, and 21 in the second quarter of 2015. The $3.3 billion total represented an 81% sequential fall, an 88% year-over-year decline.

Midstream companies continue to face the dual headwinds of constrained cash flow and reduced access to the debt and equity markets.”

Avoiding long shots

The report added that “conservative strategies dominated the deals market. Companies focused on core assets, not long shots. Most deal makers concentrated on rationalizing their portfolios and generating more cash flow. Divestiture proceeds have been earmarked for reducing debt or reinvesting back into investment opportunities, either via capex or acquisitions.”

That trend is understandable given the buffeting midstream’s customers—upstream producers—have endured due to the commodity collapse, Deloitte said in a 2016 oil and gas industry survey of energy professionals, published early in the fourth quarter.

“Contraction in the upstream sector has begun to wear on the midstream sector, which was once thought to be somewhat immune to commodity price volatility because much of its revenue is derived from fee-based contracts,” according to the survey.

“However, these contracts are at risk of being renegotiated or challenged in bankruptcy court, given the financial stress of upstream producers.”

Midstream operators with private equity backing might have pursued standard operating procedure with an IPO to form MLP by now in more normal times—but these haven’t been normal times, according to Deloitte.

“MLP-driven asset-acquisition activity has slowed considerably as MLPs have shifted from ‘grow’ to ‘maintain’ mode,” it said. “Consolidation could be on the way, taking many forms:

1) Upstream contraction created midstream overcapacity, making consolidation by financially strong MLPs incentivized to grow less costly than organic growth,

2) The corporation could roll up the MLP into its corporate structure to lower the cost of capital for the C-corporation and lower costs through scale and scope and

3) MLPs could acquire their general partner to eliminate incentive distribution rightsand lower the cost of capital.”

Selling upstream assets

EnCap Flatrock’s Lemmons said there are deals coming into midstream from upstream now due to the commodity price situation.

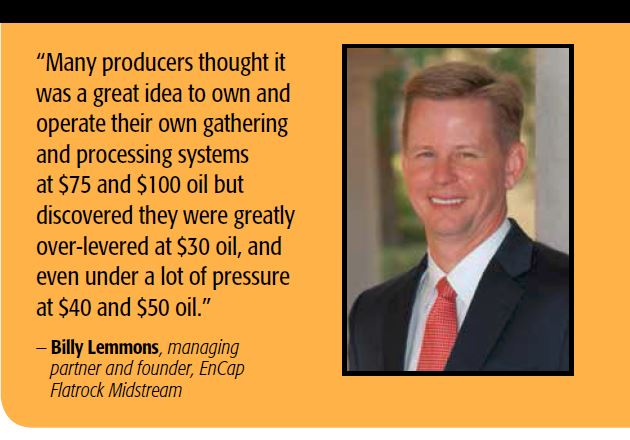

“Many producers thought it was a great idea to own and operate their own gathering and processing systems at $75 and $100 oil but discovered they were greatly over-levered at $30 oil, and even under a lot of pressure at $40 and $50 oil. This scenario has motivated several producers to divest midstream assets to get their balance sheets in order,” Lemmons explained. Weak commodity prices and the broad downturn in all energy issues on Wall Street have also challenged MLP players, particularly in areas that have slowed, Lemmons added.

“Many small and mid-size MLPs also find themselves over-levered and need to find ways to generate cash.”

Making a deal work requires that the seller and buyer agree on price—and that has been a challenge sometimes in the current environment.

“Companies are struggling with the financial reality of excess debt and squeezed profits that the lower price of oil and gas entails, leading to a rapid transformation of the sector,” EY said in a report on energy-industry private equity released earlier this year.

“However, this environment is also providing opportunities for astute investors, and private equity firms are striving to uncover the silver lining of a depressed commodity price environment. Much of global private equity firms’ dry powder is yet to be deployed, having grown to $971.4 billion” at midyear.

Favoring the buyer

EY added in its report that “we conclude that private equity firms believe that valuations will favor the buyer. This will ensure firms get the right assets—ones that are properly priced and valued.”

Energy Spectrum’s Davis “hasn’t seen a large bid/ask spread in the midstream currently” but added that “upstream has been different. We have been seeing aggressive numbers for upstream assets in the Permian, and the Scoop and Stack too.” On the midstream side, he added “only recently have we seen divestitures come to market.”

But there are midstream deals still getting done—via private equity.

ArcLight Capital Partners LLC, a major midstream private equity player, put together the recently announced merger between American Midstream Partners LP and JP Energy Partners LP. American Midstream will acquire 100% of JP Energy in a unit-for-unit merger, which American Midstream said is anticipated to have minimal, if any, tax recognition for unitholders.

Upon closing, it added the combined entity is expected to generate proforma adjusted EBITDA of approximately $185 million, assuming 2016 mid-point guidance from each respective company and including run-rate synergies of approximately $10 million from the combination.

Late in the third quarter, one of EnCap Flatrock’s portfolio companies, EagleClaw Midstream Ventures LLC, announced the acquisition of the PennTex Permian LLC subsidiary of PennTex Midstream Partners LLC. Primarily located in the Permian’s red-hot Delaware Basin, PennTex Permian’s assets included a cryogenic processing plant with a capacity of 60 million cubic feet of natural gas per day (MMcf/d), approximately 90 miles of gathering pipeline and approximately 35 miles of condensate pipeline. PennTex Permian’s assets are supported by long-term dedications of more than 75,000 acres.

The acquisition makes EagleClaw the largest privately held midstream operator in the Southern Delaware Basin. The company is connecting the PennTex system to its existing East Toyah System, bringing EagleClaw’s current processing capacity up to 120 MMcf/d (with an additional 200 MMcf/d under construction) and total gathering pipeline to more than 332 miles served by nine field compressor stations, with a total of 30,360 horsepower of low- and high-pressure compression.

“Our teams are making some great acquisitions, but we’re also continuing to put good-quality, greenfield investment dollars into the ground,” Lemmons said of the Eagle Claw/PennTex deal and Lucid Energy Group II’s recent acquisition of Agave Energy Company. Agave’s high-growth assets in New Mexico include 280 MMcf/d of natural gas processing capacity, more than ,300 miles of gas gathering pipeline and over 60,000 horsepower of compression supported by dedications and volume commitments from several major producers. Lucid II plans to expand Agave’s footprint in the Delaware Basin by adding new infrastructure in the near term, including a new 200 MMcf/d cryogenic processing plant.

Know the territory

Cecere emphasized the importance of a working knowledge of the oil and gas business in general—and the midstream in particular. Lemmons agreed and noted his operators “don’t have to spend a lot of time explaining to us what a compressor is, or what a processing plant is, or the different kinds of contracts in our business. We can move quickly past that and get onto the business of building a successful company. Our teams really appreciate the fact that we have decades of midstream experience and contacts in virtually every aspect of the business.”

Cecere added that “you have to go basin-by-basin because they are so different. We will pursue a variety of strategies to put growth capital behind businesses but those strategies can vary widely by play.

“You look at the Permian, there are lots of greenfield opportunities for private equity to have a role because there is growth,” he said. But on the other side of the state in the East Texas fields, “we have been very successful in buying noncore assets in less competitive situations consolidating them into a coherent set of assets and growing volumes by providing better solutions to producers in the region.”

That can include repurposing infrastructure, and East Texas has a lot of underused or misapplied midstream assets that have gone in the ground since the region first went on production some 80 years ago. Cecere cited one deal that included a section of pipeline originally built as a dry gas interstate transmission line that Align Midstream, a portfolio of Tailwater, purchased and converted to a wet-gas intrastate operation.

“We try to be flexible in how we approach now, but both present opportunities,” Cecere said.

Know the people

Lemmons emphasized that knowing notonly the business but its people are crucial for a private equity firm in working with its operating firms.

“We try to be helpful with contacts and ideas,” he said. “There have been times when our management teams tell us, ‘we’ve been trying to get a meeting set up with Producer X, but we can’t seem to crack the code.’ Then one of us will say, ‘I know someone over there, I’ll see if we can help.’ We’re very likely to have a meeting set up a week later.”

Likewise, a key part of the private equity-backed capital network is the identification and funding of experienced midstream management teams that can put together a functioning operating company that starts up thanks to the private equity provider’s capital.

Likewise, a key part of the private equity-backed capital network is the identification and funding of experienced midstream management teams that can put together a functioning operating company that starts up thanks to the private equity provider’s capital.

That Delaware Basin oil gathering system was put together in 2015 by Energy Spectrum portfolio company Frontier Energy Services LLC and producer Concho Resources Inc. It won project of the year honors in the first Midstream Business Excellence Awards competition.

Davis said the industry shakeout has produced a surplus of experienced midstream teams—some of whom have excellent expertise but can’t locate attractive deals. “In my opinion, the industry became oversupplied with midstream management teams in 2013 and 2014,” he said. “Energy Spectrum backed 11 teams in our Fund VI, which we raised in 2011. We unwound two of those portfolio companies at the end of 2015 because they hadn’t gotten traction after two-and-a-half to three years.”

Lemmons also sees the trend.

“As private equity becomes more prevalent in midstream, one thing we’ve seen is a weeding out of some of the weaker players and management teams. On the opposite side, we are beginning to see more and more high-quality executive talent in this business looking at the midstream opportunity and saying, ‘I am at the right point in my career, and I have the right experience and the right contacts to assemble a high-quality and build my own company with a high-quality capital partner,’” he said.

A strong management team coupled with a strong private equity provider creates synergy from the strengths of each, Cecere noted.

“We strive to be value-added partners,” he said of the management teams Tailwater works with. “That can vary by company, but it usually comes through board representation and close commercial and strategic involvement coupled with support from our deep network in the industry. We give our management teams the resources they need to pursue the opportunities for which they are most suited and jointly shape the long-term vision of our partnership.”

Given weak commodity prices, the drilling slowdown and an unusual capital market, what’s driving midstream deals right now? Attractive assets in active basins certainly create interest—if they can be found.

“We’re not buying debt,” Davis said. “We’d be happy to buy an asset, but there’s not a lot of size on the market right now. When there is a midstream divestiture of size, it seems to be getting bid up by potential buy-ers. We’re primarily continuing with the same model we’ve had for years: building assets for producers.”

Finding the exit

A private equity firm and its limited partners always share a common goal:create a profitable exit strategy. Their investment in an experienced team and capital to build or buy assets focus on an eventual sale or IPO that provides the desired return. But strategies can vary by situation and management style.

“It depends on the individual deal,” avis said. “We are often told by the market when it is time to sell, in which case we usually hire an investment bank and run a competitive sale process.

Sometimes we just realize how much value has been created and, if it calculates to return a certain value to our investors, then we decide to monetize that investment and take those chips off the table. Our general bias is toward the bird-in-hand opportunities vs. waiting for a greater return with its additional risk. There’s always risk in waiting.”

For EnCap Flatrock, “At a high level, our exit strategy is almost always a strategic ,” Lemmons said. “Having said that, there are some opportunities where an IPO might make more sense. You just have to look at where you are in the market cycle.”

Lemmons mentioned the slowing of acquisition activity in the past two years but added he sees capital markets are “are showing some strengthening and that opens up the opportunities for ams to go public.”

Cecere also sees the public markets strengthening. “We expect to continue to see a very healthy universe of MLP acquirers. Most of our exits will likely occur through sales to MLPs; there’s a robust universe of buyers there who can create additional value with the assets our portfolio companies have developed. But as we have seen, there will always be temporary dislocations where MLP equity markets will be more open or more tight.”

EY’s Fane emphasized “timing is key” in making deals.

“The first thing is, there are a lot of buyers out there, right? You would start getting some price tension where other bidders may come in and bid it up before you could actually get into the market and acquire those assets. So, it’s missed opportunity. The other healthy tension to that is that if commodity prices will remain flat to modest for many years, the uptick—or the gain, if you will—of acquiring those assets in the downtime is pretty thin.”

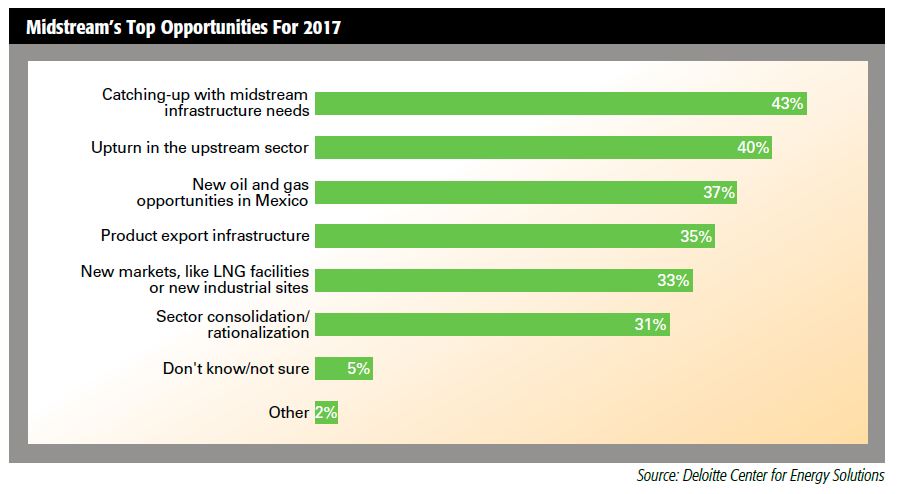

2017 outlook

Deal making may remain soft going into 2017 even as commodity prices continue to improve, according to Deloitte’s survey.

“A majority of respondents expect a moderate level of consolidation in both 2016 (62%) and 2017 (59%), but when asked about whether the midstream sector would consolidate significantly in 2017, affirmative responses increased from 15% to 23%,” Deloitte added. “However, MLP rollups into C-corporation structures were seen as unlikely (28%) or moderate (52%). Lowering costs and costs of capital, the impetus behind consolidation and rollups, is the biggest challenge facing midstream companies, 52% of professionals surveyed asserted.”

Lemmons reflected back on the past couple of years before looking ahead to 2017.

“When we look back, we’re likely to think about 2016 as a year of transition,” he said. “Coming out of 2014 and into 2015,

everyone in the industry was grappling with this downturn, trying to figure out what it would look like and, more importantly,

how long it would last. In 2016, many of the challenges the industry faced were rationalized into the system through bankruptcies and restructurings,” he said.

“The sector, including our teams, saw the development of several good greenfield opportunities in a handful of plays.” Lemmon added that, “We were also able to attract and close some privately negotiated deals,” such as the EagleClaw-PennTex and Lucid-Agave transactions.

“We participated in a deal with Plains All American Pipeline LP, a high-quality public company, and we closed on a very successful realization, the sale of Tall Oak Midstream I to EnLink,” he noted.

For EnCap Flatrock, “While we can’t be certain, it does feel that things are different now and more hopeful,” Lemmons said. If commodity price increases hold, he expects there will be “a cautious increase in activity and a pick-up in greenfield activity. There are still some problems and challenges in the industry that are not fully resolved, and we expect those to generate additional acquisitions and brownfield opportunities.”

And what’s going to happen in Mexico with its rapidly growing midstream?

“While the opportunity isn’t fully formed, and questions remain around the regulatory and business framework, I think some of the projects in development will be commissioned in the coming year,” Lemmons added.

“We’re participating in the opportunity by working with Rangeland Energy III to develop their South Texas Energy Products System, a terminal in Corpus Christi [Texas] that will facilitate the delivery of refined products, LPG and crude to locations in Mexico.

And to the north, “In Canada, we continue to look at opportunities to try find the right ones.”

Vrielink said he expects the sector’s contract uncertainty, post Sabine, to lessen in the new year.

“I think that it starts to diminish over time,” the attorney added. “People have already approached their counter parties and tried to renegotiate these contracts. e have been in a new price environment for a couple of years now, so that particular risk diminishes somewhat.”

Due diligence on prospective deals will remain very important, he emphasized.

“Some investors are saying ‘I prefer the midstream because I don’t have to worry about making decisions on where to drill,’ but I think people realize that you, in the midstream, are totally dependent on what’s happening upstream.

Investors in the midstream are much more cautious and doing much more work now, to try and figure out where the production comes from and who will be active upstream,” Vrielink added.

He also emphasized the point thatspecialized midstream private equity providers will continue to have an advantage going forward.

Adding risk

“People who really know the industry will do better and will feel more comfortable that they are making the right decisions than the people who are less familiar. But the underlying assets will have to take more risk,” he said.

At Energy Spectrum, “I don’t see a compelling story on why prices are going to improve dramatically in 2017,and by dramatically I mean north of $60,” Davis said. “Without a big pop in prices, I think the supply of opportunities will stay fairly consistent.

“Across the midstream private equity space, I think we will see the dissolution of teams that have not been able to get traction,” he added. “I think that will be a noticeable trend in 2017.”

For Tailwater’s part, “We think 2017 will be a good year with a more stable commodity backdrop,” Cecere said.

“Barring a broader economic recession, e don’t anticipate as much volatility as we have seen for the past two years, which should bolster transaction activity. One of the big macro trends is the re-equitization of the energy space. That’s going to come through restructurings and de-levered balance sheets and will create opportunity—a lot of opportunity—for private equity to provide capital to fix over-levered situations and then provide growth capital as companies get their feet back underneath them. It’s going to be a good year for private equity.”

Lemmons points to an overall maturing of the midstream private equity business that he expects will continue the new year.

“Right now, one of the things we talk about a lot is we see the midstream private equity model continuing to mature in a good way,” he said. “It’s a critical part of the aggregate balance sheet in the midstream business for a couple of reasons. irst, we can identify and season out the risk associated with developing a new area. And, when there are challenges in the business of the sort we’ve seen in the past couple of years, we can step in and fill the void on access to capital.

“All in all, equity-backed midstream companies are becoming more and more accepted by the customer groups they do business with. And, as the leadership of the energy industry matures, anaging a private-equity-backed venture is viewed as a very attractive career path for top-quality executives in our industry, and that will advance private equity’s growing role,” Lemmons said.

Recommended Reading

Going with the Flow: Universities, Operators Team on Flow Assurance Research

2024-03-05 - From Icy Waterfloods to Gas Lift Slugs, operators and researchers at Texas Tech University and the Colorado School of Mines are finding ways to optimize flow assurance, reduce costs and improve wells.

Fracturing’s Geometry Test

2024-02-12 - During SPE’s Hydraulic Fracturing Technical Conference, industry experts looked for answers to their biggest test – fracture geometry.

Haynesville’s Harsh Drilling Conditions Forge Tougher Tech

2024-04-10 - The Haynesville Shale’s high temperatures and tough rock have caused drillers to evolve, advancing technology that benefits the rest of the industry, experts said.

Exclusive: Silixa’s Distributed Fiber Optics Solutions for E&Ps

2024-03-19 - Todd Chuckry, business development manager for Silixa, highlights the company's DScover and Carina platforms to help oil and gas operators fully understand their fiber optics treatments from start to finish in this Hart Energy Exclusive.

2023-2025 Subsea Tieback Round-Up

2024-02-06 - Here's a look at subsea tieback projects across the globe. The first in a two-part series, this report highlights some of the subsea tiebacks scheduled to be online by 2025.