With all the cash Chesapeake Energy Corp. has raked in from divesting most of its Eagle Ford portfolio, will the company buy something? (Source: Shutterstock.com)

With all the cash Chesapeake Energy Corp. has raked in from divesting most of its Eagle Ford portfolio, will the company buy something?

The operator isn’t opposed to buying right now, said Nick Dell’Osso, president and CEO. But deals, “they’re hard, especially in a down-market.”

The 12-month strip has declined from more than $7 last year to less than $3 today.

Potential sellers “are not wanting to think about the current market conditions and [are] wanting to look forward to an assumed improvement in market conditions,” Dell’Osso said.

Chesapeake has transitioned in the past few years to focus its portfolio fully on natural gas, producing an average 4.1 billion cubic feet equivalent per day currently. It sold its oil-weighted property in the Eagle Ford earlier this year, while keeping its liquids-rich gas property in the far southern play for now.

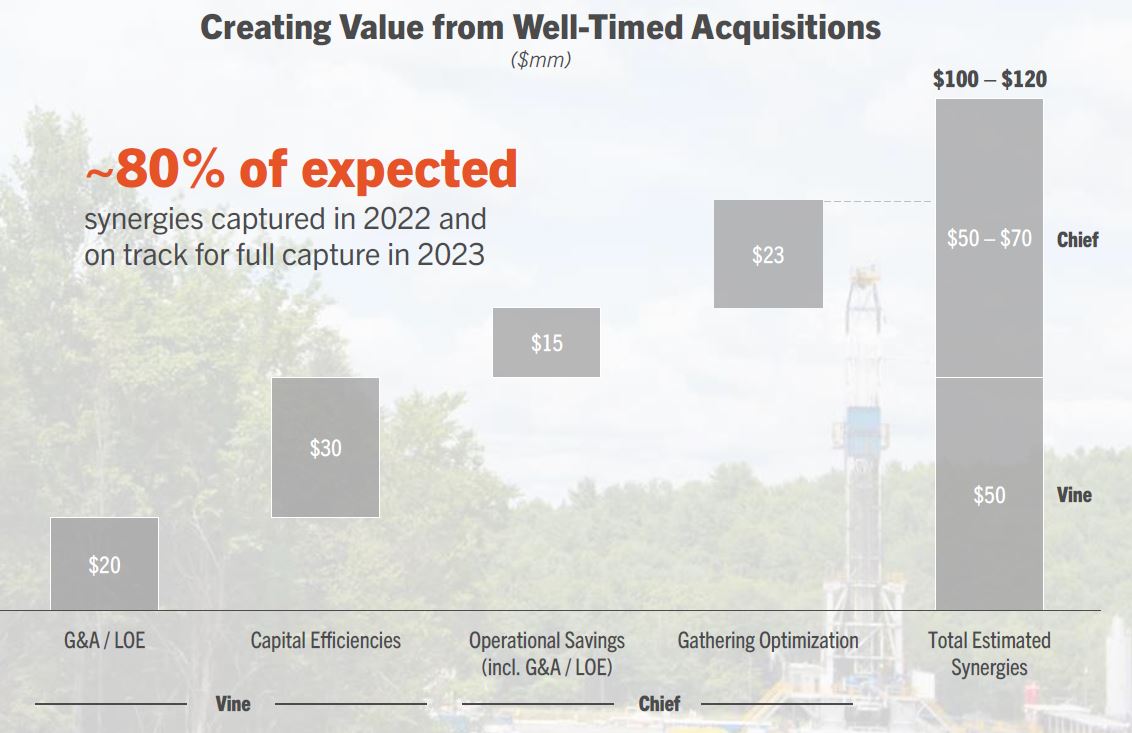

The company also added two gas portfolios—that of Vine Energy Inc. in the Haynesville Shale and Chief E&D Holdings in the Marcellus Shale —in late 2021 and January 2022.

The strip wasn’t much better than today. But gas futures were on their way up at the time after having been depressed for many years, so buyers’ expectations weren’t as great as today.

“We stay engaged on the A&D front,” Dell’Osso said. “We do believe in consolidation. We think there’s value in consolidation—when you follow our [dealmaking] non-negotiables so you don’t overpay and you buy good assets where you can have real synergies that are not just theoretical, but they’re driven by operational realities in the field.

“If we can do any of those things, then we’ll absolutely continue to pursue them.”

Chesapeake has $1.2 billion of cash on hand from cash flow and from selling two-thirds of its Eagle Ford portfolio this year for $2.8 billion. The E&P’s total available liquidity is $3 billion.

RELATED: Chesapeake Finds ‘Much Better Deal’ in Eagle Ford Sale to INEOS

With some of its cash, it’s retired 1 million shares since Feb. 21.

But just having cash in the bank doesn’t mean it should be used for buying property, Dell’Osso said. “It’s not a justification for doing a deal. The deal has to stand on its own.”

As for selling the remaining part of its Eagle Ford portfolio—the rich-gas Austin Chalk play in Webb County, Texas— “we remain in active dialogue with the interested parties there,” said Mohit Singh, Chesapeake CFO.

Dealmaking these days has more than gas-price volatility in play, he noted. The Fed rate was 5% during the analyst call Wednesday morning and was raised to 5.25% later in the day.

“So the financing market remains challenged,” Singh said. “The good news is the buyers that we have been engaged with all throughout the process have been actively in dialogue with us.

“That bodes well. We’ve said all along we are prepared to hold onto the asset if we don’t get to the right price. So again, all those options are on the table, and we are continuing to work through all of that.”

Recommended Reading

Segrist: The LNG Pause and a Big, Dumb Question

2024-04-25 - In trying to understand the White House’s decision to pause LNG export permits and wondering if it’s just a red herring, one big, dumb question must be asked.

Texas LNG Export Plant Signs Additional Offtake Deal With EQT

2024-04-23 - Glenfarne Group LLC's proposed Texas LNG export plant in Brownsville has signed an additional tolling agreement with EQT Corp. to provide natural gas liquefaction services of an additional 1.5 mtpa over 20 years.

US Refiners to Face Tighter Heavy Spreads this Summer TPH

2024-04-22 - Tudor, Pickering, Holt and Co. (TPH) expects fairly tight heavy crude discounts in the U.S. this summer and beyond owing to lower imports of Canadian, Mexican and Venezuelan crudes.

What's Affecting Oil Prices This Week? (April 22, 2024)

2024-04-22 - Stratas Advisors predict that despite geopolitical tensions, the oil supply will not be disrupted, even with the U.S. House of Representatives inserting sanctions on Iran’s oil exports.

Association: Monthly Texas Upstream Jobs Show Most Growth in Decade

2024-04-22 - Since the COVID-19 pandemic, the oil and gas industry has added 39,500 upstream jobs in Texas, with take home pay averaging $124,000 in 2023.