With all the cash Chesapeake Energy Corp. has raked in from divesting most of its Eagle Ford portfolio, will the company buy something? (Source: Shutterstock.com)

With all the cash Chesapeake Energy Corp. has raked in from divesting most of its Eagle Ford portfolio, will the company buy something?

The operator isn’t opposed to buying right now, said Nick Dell’Osso, president and CEO. But deals, “they’re hard, especially in a down-market.”

The 12-month strip has declined from more than $7 last year to less than $3 today.

Potential sellers “are not wanting to think about the current market conditions and [are] wanting to look forward to an assumed improvement in market conditions,” Dell’Osso said.

Chesapeake has transitioned in the past few years to focus its portfolio fully on natural gas, producing an average 4.1 billion cubic feet equivalent per day currently. It sold its oil-weighted property in the Eagle Ford earlier this year, while keeping its liquids-rich gas property in the far southern play for now.

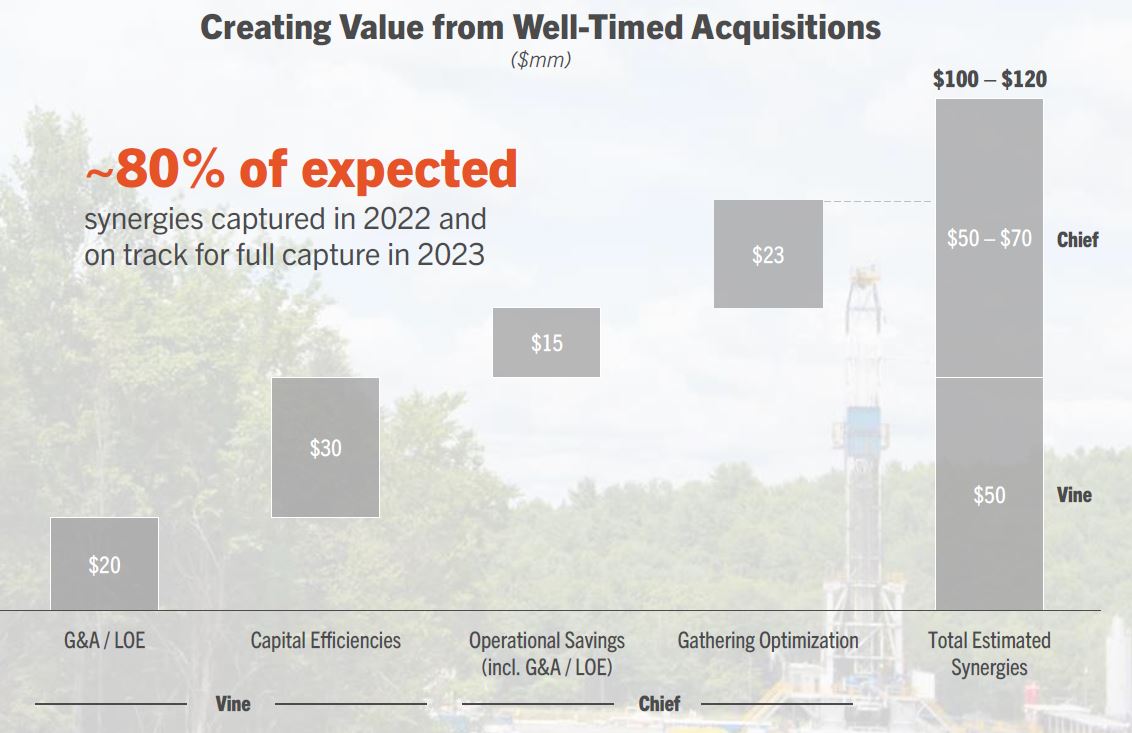

The company also added two gas portfolios—that of Vine Energy Inc. in the Haynesville Shale and Chief E&D Holdings in the Marcellus Shale —in late 2021 and January 2022.

The strip wasn’t much better than today. But gas futures were on their way up at the time after having been depressed for many years, so buyers’ expectations weren’t as great as today.

“We stay engaged on the A&D front,” Dell’Osso said. “We do believe in consolidation. We think there’s value in consolidation—when you follow our [dealmaking] non-negotiables so you don’t overpay and you buy good assets where you can have real synergies that are not just theoretical, but they’re driven by operational realities in the field.

“If we can do any of those things, then we’ll absolutely continue to pursue them.”

Chesapeake has $1.2 billion of cash on hand from cash flow and from selling two-thirds of its Eagle Ford portfolio this year for $2.8 billion. The E&P’s total available liquidity is $3 billion.

RELATED: Chesapeake Finds ‘Much Better Deal’ in Eagle Ford Sale to INEOS

With some of its cash, it’s retired 1 million shares since Feb. 21.

But just having cash in the bank doesn’t mean it should be used for buying property, Dell’Osso said. “It’s not a justification for doing a deal. The deal has to stand on its own.”

As for selling the remaining part of its Eagle Ford portfolio—the rich-gas Austin Chalk play in Webb County, Texas— “we remain in active dialogue with the interested parties there,” said Mohit Singh, Chesapeake CFO.

Dealmaking these days has more than gas-price volatility in play, he noted. The Fed rate was 5% during the analyst call Wednesday morning and was raised to 5.25% later in the day.

“So the financing market remains challenged,” Singh said. “The good news is the buyers that we have been engaged with all throughout the process have been actively in dialogue with us.

“That bodes well. We’ve said all along we are prepared to hold onto the asset if we don’t get to the right price. So again, all those options are on the table, and we are continuing to work through all of that.”

Recommended Reading

Sinopec Brings West Sichuan Gas Field Onstream

2024-03-14 - The 100 Bcm sour gas onshore field, West Sichuan Gas Field, is expected to produce 2 Bcm per year.

Trio Petroleum to Increase Monterey County Oil Production

2024-04-15 - Trio Petroleum’s HH-1 well in McCool Ranch and the HV-3A well in the Presidents Field collectively produce about 75 bbl/d.

US Drillers Cut Oil, Gas Rigs for First Time in Three Weeks

2024-02-02 - Baker Hughes said U.S. oil rigs held steady at 499 this week, while gas rigs fell by two to 117.

Tech Trends: SLB's Autonomous Tech Used for Drilling Operations

2024-02-06 - SLB says autonomous drilling operations increased ROP at a deepwater field offshore Brazil by 60% over the course of a five-well program.

Rystad: More Deepwater Wells to be Drilled in 2024

2024-02-29 - Upstream majors dive into deeper and frontier waters while exploration budgets for 2024 remain flat.