Privately held Venado Oil & Gas CFO Branden Kennedy said, “We’re in a position where we are growing production and paying distributions, and all of that within cash flow. We were purposefully built for this environment.” (Source: Hart Energy)

[Editor's note: A version of this story appears in the December 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Since inception in September 2016, Venado Oil & Gas LLC has deployed some $2 billion in capital from New York private-equity firm KKR. The E&P is not, however, counting on a quick sale to capture return on investment, and never intended to. In fact, Venado is one of the earlier and more mature examples of how private equity is changing strategy in the E&P space.

“The biggest industry trend that we see and feel somewhat like we are leading is the transition on the business model,” said Branden Kennedy, Venado CFO. He joined the Austin, Texas, company a year ago.

Kennedy spoke at Hart Energy’s DUG Eagle Ford conference in September in San Antonio about how the company was constructed with the long view in mind.

“There have been so many private-equity portfolio companies that were built for a three, four or five-year exit, and that just hasn’t happened,” said Kennedy. “We’re hearing about the various capital providers pulling assets out from underneath teams; they’re having to combine teams to get synergies and scale. At Venado, we pride ourselves on being ahead of that. We took the fork in the road years ago when we decided we wanted to build a real business—cash-flow based and paying out distributions.”

RELATED:

DUG Eagle Ford: Venado Oil & Gas On Fast Cycle Times

The industry’s ability to “shift on a dime” away from a lease-and-sell model to an acquire-and-develop model is near impossible, he said, akin to trying to turn a large ship. “That’s what the industry has dealt with the last two or three years. There are significant assets, people and volume being moved straight ahead. We’re busy turning. We’re pivoting with this new model.”

The Venado Model is based on four distinct premises.

Built for duration. “It starts with alignment,” said Kennedy, referring to alignment of vision between the capital provider and the management team.

“We wanted something built for duration. We no longer want to hope for higher prices, and we don’t want to count on somebody else coming along to take us out.”

Venado’s founders, led by CEO Scott Garrick, hammered out an agreement in 2016 that does not include an exit window target and adjusts the method in which management is incentivized.

“We don’t have a clock. Everybody else, when they deploy their equity capital, they have a paid-in-kind dividend running in the background. It incentivizes a quick flip in four or five years because it’s eroding management’s equity interests. It presents the possibility for very bad decisions when you’re focusing on timing and exit.”

Instead, he said, Venado is a cash-on-cash machine.

“We pay back distributions, and when we actually pay that cash back, we’re reducing our equity cost basis. There’s no pressure to transact. In our partnership between KKR and Venado, we have to be aligned to want to hold it long term and not cause the management team to make poor decisions aimed at an early exit.”

Acquire and develop. Venado touts that it focuses on liquids-rich PDP assets with developmental upside and built its South Texas portfolio via three primary asset acquisitions that included significant existing production, i.e., cash flow.

In 2017, Venado acquired nonoperated assets from SM Energy Co. for $800 million that were producing 27,000 barrels of oil equivalent per day (boe/d) with a one-third mix of oil, gas and NGL. In early 2018, it added an additional 15,600 net boe/d in a $765 million combo deal for operated and nonoperated assets from Cabot Oil & Gas Corp. It tacked on another 4,500 boe/d of existing operated production in mid-2018.

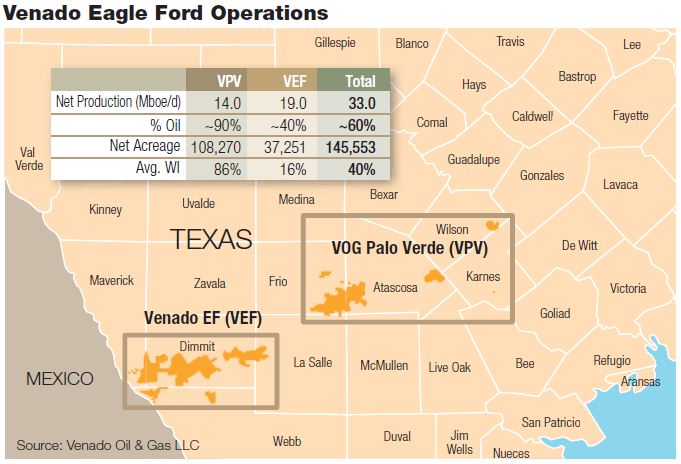

Today, Venado holds some 145,000 net acres in the Eagle Ford, with its largest positions in Dimmit, Frio and Atascosa counties. Net production stands at 33,000 boe/d (60% oil).

“One of the things that attracted me to Venado was how it targeted and located the assets it acquired,” Kennedy said. With some 21,000 horizontal wells drilled by industry in the Eagle Ford, and 2,900 with modern completions, Venado grappled with the question, “How do we create alpha?”

“We don’t want to hope for higher prices. How do we actually do something in our control to create that alpha and those excess returns?”

The answer was data—using data analysis to come back into previously drilled areas that had not been completed properly. On its operated assets, the company was able to yield 40% to 70% performance improvements to a legacy type curve by adjusting proppant, sand and water concentrations in its completions based on its data-driven approach.

Business and process-driven. The new business model needs a long duration view with multidisciplinary and system integration, Kennedy said. “Every single responsibility and discipline has a seat at the table, they have a voice, and that’s how we’re going to yield profitability.”

He further delineated the characteristics and disciplines needed in a long-duration business model.

Predictability—geologists, geophysicists and reservoir engineers. These disciplines are able to predict what’s going to come out of the ground 2 miles down and 3 miles out, he noted. “That’s absolutely impressive to me, but it’s that predictable nature that allows us to plan the organization. It creates actionable decision support.”

Repeatability—operations engineers. Their value resides in their ability to compress cycle times, do things faster with less and do it safely. “I would be remiss if I didn’t comment on safety here. If we don’t send our people home the same way they get to work, we have failed. So the expectation on the repeatability is doing this efficiently and safely.”

Dependability—marketing. “I don’t care how good the wells are, I don’t care how good that break in nature is, if we don’t have the appropriate midstream and marketing framework to provide product flow assurance and cash flow assurance, we will fail.”

Scalability—land. “I need them blocking and tackling on the acreage, increasing our working interest, giving us that scale so we can continue to drive down unit costs,” he said. “You’ve seen a lot of the operators talk about unit costs and how that drives margin, because that’s one of the few things they can control. So land has a seat at the table and a role in helping preserve that margin.”

Profitability—everyone. While Venado’s founders have backgrounds in engineering, geology and land, they are all business professionals first, he said. “The goal of any organization is to make money, so we need all the disciplines. It’s not going to be just a land-driven shop or an engineering-driven shop. I want them all. I’m going to give them all a voice.”

Capital steward focus. Once the process is working, Venado focuses on two goals. The first: create and preserve the cash margin.

Venado expends about $18/boe on its operated assets, including interest expenses, LOE, G&A and production taxes. At $56 West Texas Intermediate, it reaps some 67% cash margin, or $38/boe.

“So for every boe that’s generated, this is how much cash margin we have to make a decision with.”

Which leads to the second goal: capital allocation.

“With every single dollar of cash margin thrown off, we have an option. We consider all of them. We can lease acreage, we can build additional infrastructure, we can make acquisitions, we can pay down debt or we can pay distributions. All those items are on the table for us.”

And while the company does pay distributions back to KKR and to the limited partners, Kennedy emphasized that Venado is not an MLP and compared it instead to a variable rate MLP. “We have the option, on any given quarter, given a macro environment or capital opportunities, to turn it up, turn it down or turn it off.”

Thus the Venado Model is not just a return on capital, but a return of capital.

Is there any pressure to sell? No, said Kennedy.

“Everybody wants to transact at some point, because that’s how you get the fast payday. But by paying distributions, we continue to pay down and reduce our equity cost basis. If you want to build a long-term model focused on being here for 20 years, it’s all about making sure you have alignment up top.”

Further acquisitions are still on the table, but Kennedy said seller expectations remain too high for now. “We have to buy right. We’re not in a position where we have to act, but we’re actively still looking.”

The plan coming into the year was to operate one rig for the first six months and then lay it down, he said, but cash flow has been robust. “Given our ability to fund that rig out of cash flow and pay distributions, we’ve chosen to keep the rig and are looking at adding a second next year.”

The private operator estimates $300- to $350 million EBITDAX in 2019 with less than 2x debt-to-EBITDA, and it is on pace to grow production by 10% to 12%. Of that $2 billion of KKR capital previously deployed, “by year-end we will have returned approximately 10% of that back to equity holders,” Kennedy revealed.

“We’re in a position where we are growing production and paying distributions, and all of that within cash flow. We were purposefully built for this environment.”

Recommended Reading

Range Resources Holds Production Steady in 1Q 2024

2024-04-24 - NGLs are providing a boost for Range Resources as the company waits for natural gas demand to rebound.

Hess Midstream Increases Class A Distribution

2024-04-24 - Hess Midstream has increased its quarterly distribution per Class A share by approximately 45% since the first quarter of 2021.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.